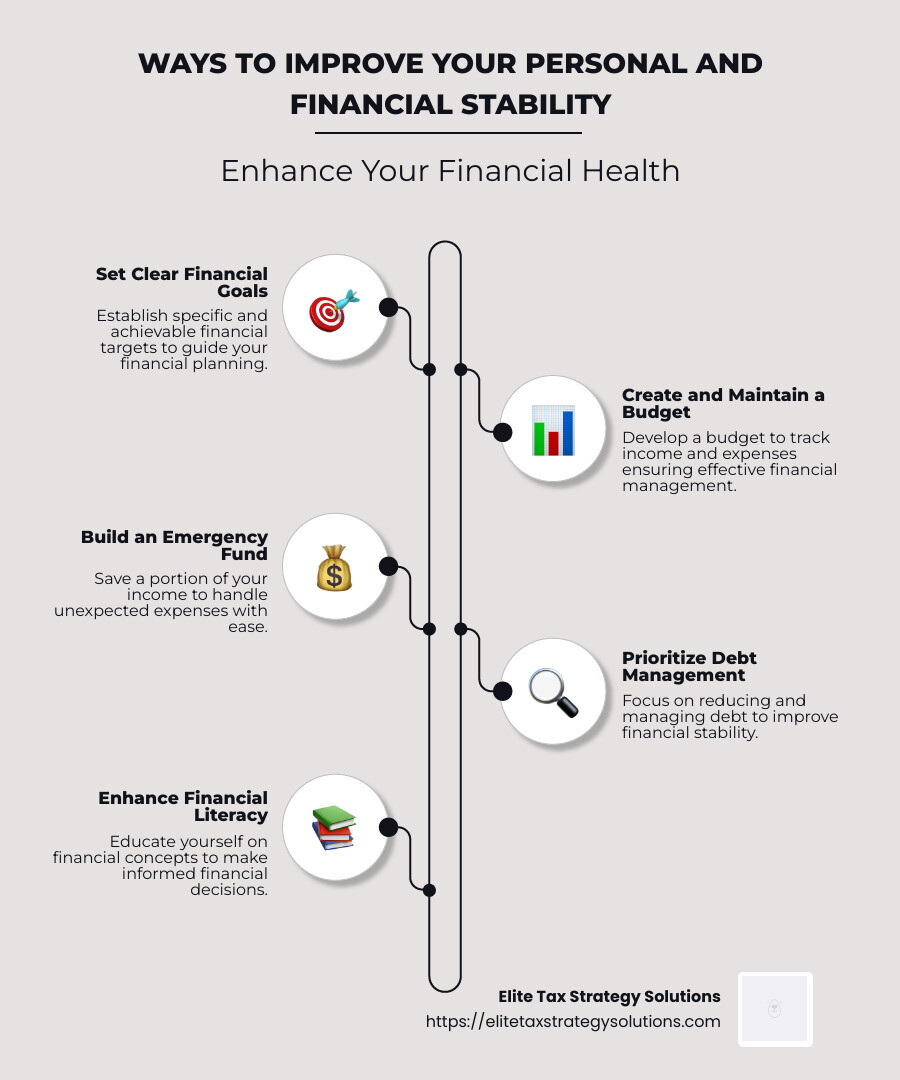

Ways to improve your personal and financial stability and planning are crucial for a solid financial future. Many individuals find this aspect of life overwhelming, but following simple steps can make a significant difference:

- Set clear financial goals

- Create and maintain a budget

- Build an emergency fund

- Prioritize debt management

Understanding and implementing these actions can lead to improved financial health.

Financial health is more than just having money; it’s about creating stability and freedom in your life. With strategic personal finance management and deliberate financial planning, you can avoid stress and make empowered decisions. These practices not only ensure that you are prepared for unexpected expenses but also position you to grow your wealth over time.

As David Fritch, with 40 years of experience in helping business owners and high-income earners optimize their financial outcomes, I’m here to guide you through the ways to improve your personal and financial stability and planning.

Ways to improve your personal and financial stability and planning terms to remember:

– financial stability plan

– financial stability planning

– maximize tax savings

Ways to Improve Your Personal and Financial Stability and Planning

Improving your personal and financial stability requires a clear plan and commitment to healthy financial habits. Let’s explore some key strategies that can help you achieve a stable and secure financial future.

Budgeting

Creating a budget is the first step in gaining control over your finances. A budget helps you track your income and expenses, ensuring you live within your means. Start by listing all your income sources and expenses. Categorize them into essentials like housing, food, and utilities, and non-essentials like entertainment and dining out.

Tip: Review and adjust your budget regularly to reflect changes in your financial situation.

Net Worth

Knowing your net worth is crucial for understanding your financial health. Calculate it by subtracting your liabilities from your assets. This number gives you a snapshot of where you stand financially. Regularly tracking your net worth can highlight progress and areas for improvement.

Fast Fact: Younger individuals often have a lower net worth due to student loans and early career stages. Over time, as you pay down debt and accumulate assets, your net worth should increase.

Emergency Fund

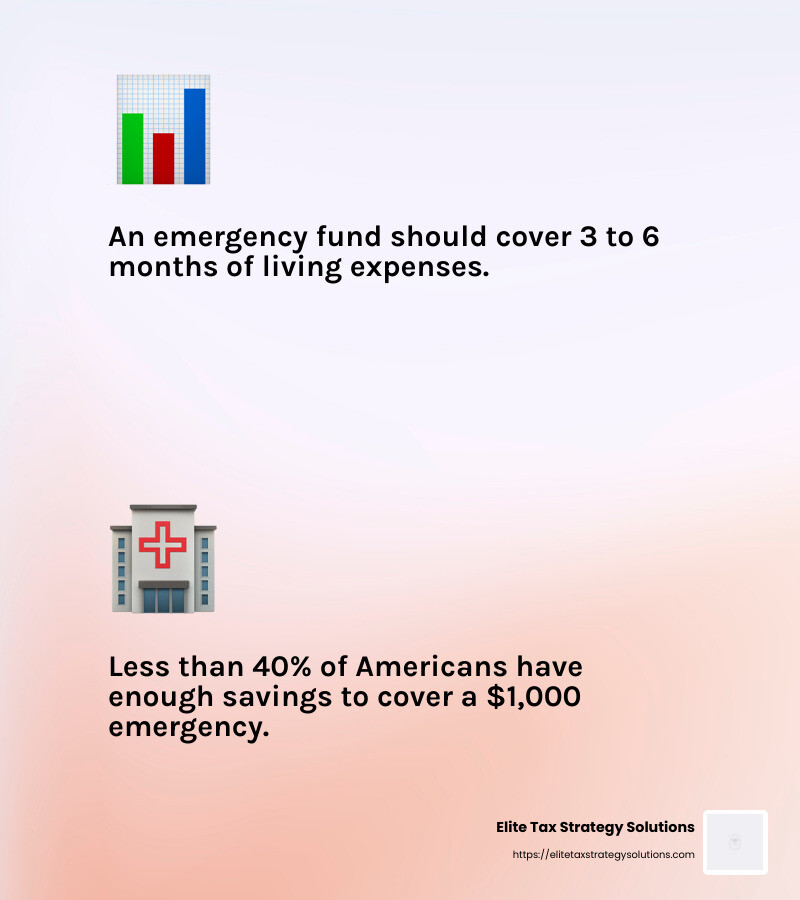

An emergency fund acts as a financial safety net. Aim to save at least three to six months’ worth of living expenses. This fund is essential for unforeseen expenses like medical emergencies or car repairs. By having an emergency fund, you can avoid going into debt during unexpected situations.

Lifestyle Inflation

As your income grows, it’s tempting to increase your spending. This is known as lifestyle inflation. To maintain financial stability, avoid the trap of spending more just because you earn more. Instead, focus on saving and investing the extra income.

Advice: Keep your lifestyle consistent, even as your income increases, to build wealth over time.

Needs vs. Wants

Understanding the difference between needs and wants is vital for financial planning. Needs are essentials like housing and groceries, while wants are non-essentials like luxury items or dining out. Prioritize your spending on needs and be mindful of how much you allocate to wants.

Exercise: Before making a purchase, ask yourself if it’s a need or a want. This simple question can help you make more intentional spending decisions.

By focusing on budgeting, understanding your net worth, maintaining an emergency fund, controlling lifestyle inflation, and distinguishing between needs and wants, you can improve your personal and financial stability. These strategies will empower you to make informed financial decisions and build a secure future.

Next, we’ll explore how to build a strong financial foundation through education, career advancement, and financial literacy.

Building a Strong Financial Foundation

To achieve a stable financial future, lay down a strong foundation. This involves focusing on education, career advancement, financial literacy, and effective income management. Let’s break down each component.

Education

Education is the cornerstone of financial success. Whether it’s formal education like college or vocational training, or informal learning through books and online courses, expanding your knowledge can significantly boost your earning potential.

Invest in yourself. Taking courses on financial literacy can help you make smarter money decisions. Books like “Rich Dad Poor Dad” offer insights into building wealth and financial independence.

Career Advancement

Your career is a major factor in your financial stability. Advancing in your career can lead to higher income and more opportunities. Stay proactive in seeking promotions or new roles that align with your skills and interests.

Tip: Continuously update your skills. As industries evolve, learning new technologies or methodologies can make you more valuable in the job market.

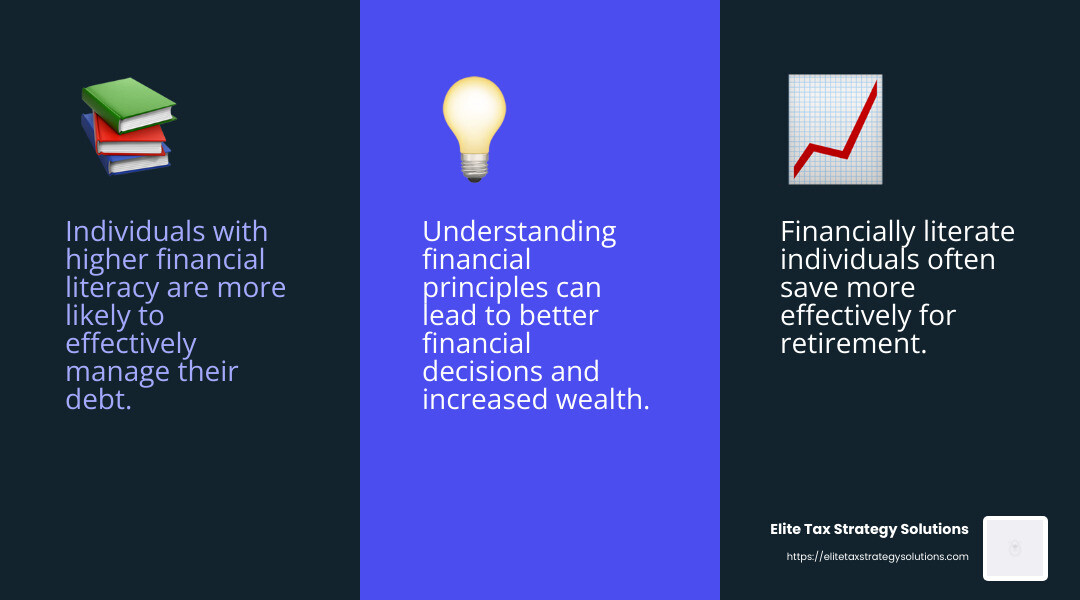

Financial Literacy

Understanding how money works is crucial. Financial literacy involves knowing how to budget, save, invest, and manage debt. The more you know, the better equipped you’ll be to make sound financial decisions.

Fact: Those with higher financial literacy are more likely to save for retirement and manage debt effectively.

Income Management

Managing your income wisely is key to building wealth. This means not just earning money, but also knowing how to allocate it efficiently.

Strategy: Use the 75/15/10 budgeting rule. Allocate 75% of your income to living expenses, 15% to savings and investments, and 10% to debt repayment or other financial goals. This balanced approach helps in maintaining financial health.

By focusing on education, career advancement, financial literacy, and income management, you can build a robust financial foundation. These elements are interlinked, each supporting and enhancing the others.

Next, we’ll dig into effective budgeting and saving strategies to further bolster your financial stability.

Effective Budgeting and Saving Strategies

Creating a personal budget is like drawing a map for your money. It shows you where your money is going and helps you decide where it should go instead. Start by listing all your sources of income and then track your expenses. Categorize these expenses into needs (like rent and groceries) and wants (like dining out or new gadgets). This will help you see where you can cut back if needed.

One popular method is the 50/30/20 rule:

- 50% for needs

- 30% for wants

- 20% for savings

Saving Early and Compounding

Saving early is a powerful strategy. The earlier you save, the more time your money has to grow. This is because of something called compounding. Compounding is when you earn money on the money you’ve already saved or invested. Over time, this can turn a small amount of savings into a large sum.

Here’s a quick example: If you start saving $100 a month at age 25, with a 5% annual return, you could have about $150,000 by age 65. If you start at age 35, you’d have about $82,000. That’s the magic of starting early!

Building an Emergency Fund

Having an emergency fund is like having a safety net. It’s money set aside for unexpected events, like car repairs or medical expenses. Aim to save three to six months’ worth of living expenses. This can help you avoid going into debt when life throws a curveball.

Tip: Set up automatic transfers to your savings account. Even small amounts add up over time.

By focusing on effective budgeting and saving strategies, you can improve your personal and financial stability. These steps ensure you’re prepared for both expected and unexpected financial situations, setting you on the path to a secure future.

Next, let’s explore how to manage debt and make smart investments to further improve your financial planning.

Managing Debt and Investments

When it comes to debt reduction, the key is to have a clear plan. Start by listing all your debts, including credit cards, student loans, and any other obligations. Prioritize paying off high-interest debt first, as it costs you the most over time. This approach is often called the “avalanche method.”

Another option is debt consolidation, which combines multiple debts into one loan with a lower interest rate. This can make payments more manageable and reduce the total interest paid.

Investment Profile

Creating an investment profile is like building a personalized strategy for growing your wealth. It considers your financial goals, risk tolerance, and time horizon. For example, if you’re young and have a long time before retirement, you might choose more stocks, which can offer higher returns but come with more risk. If you’re closer to retirement, you might prefer bonds, which are generally safer.

Diversification is also crucial. By spreading your investments across different asset types, you reduce the risk of losing money if one investment doesn’t perform well.

Retirement Planning

Retirement planning is about ensuring you have enough money saved to live comfortably when you stop working. Start by contributing to retirement accounts like 401(k)s or IRAs. These accounts offer tax advantages that can help your savings grow faster.

Consider how much you’ll need in retirement. Think about your desired lifestyle, healthcare costs, and other expenses. Use this information to set a savings goal and adjust your contributions as needed.

Pro tip: The earlier you start saving for retirement, the more you can benefit from compound interest. Even small contributions can grow significantly over time.

Managing debt and making smart investments are essential steps in enhancing your personal and financial stability. By reducing debt, creating a solid investment profile, and planning for retirement, you set the foundation for a secure financial future.

Next, we’ll dive into frequently asked questions about financial stability to address common concerns and provide further guidance.

Frequently Asked Questions about Financial Stability

What are the five steps to effective personal financial planning?

-

Set Clear Financial Goals: Start by defining what you want to achieve financially. Whether it’s buying a house, paying off student loans, or saving for retirement, having specific goals gives you direction.

-

Save and Invest Wisely: Begin saving early to take advantage of compounding interest. This is when your money earns interest, and then you earn interest on that interest. Consider opening a 401(k) or IRA to save for retirement with tax benefits.

-

Build an Emergency Fund: Aim to save enough to cover 3 to 6 months of living expenses. This fund acts as a financial cushion in case of unexpected events like job loss or medical emergencies.

-

Manage Debt Effectively: Focus on paying off high-interest debts first to minimize the total interest paid. Avoid new debt when possible, and consider consolidation if it helps lower interest rates and simplify payments.

-

Plan for Retirement: Contribute regularly to retirement accounts and adjust your savings based on your retirement goals. The earlier you start, the more you can benefit from the power of compound interest.

How do you plan to achieve financial stability?

-

Conduct a Financial Inventory: List all your assets, liabilities, income, and expenses. This gives you a clear picture of your current financial situation.

-

Leverage Compound Interest: Take advantage of compound interest by saving and investing early. The longer your money has to grow, the more you’ll accumulate over time.

-

Use Retirement Accounts: Maximize contributions to retirement accounts like 401(k)s and IRAs. These accounts offer tax advantages and help you build a nest egg for the future.

-

Create an Investment Profile: Tailor your investments based on your financial goals and risk tolerance. Diversify your portfolio to manage risk and increase the potential for returns.

How to improve your personal finances?

-

Follow the 75/15/10 Budgeting Rule: Allocate 75% of your income to needs and wants, 15% to savings and investments, and 10% to debt repayment. This balanced plan can help you manage money wisely.

-

Practice Practical Money Management: Track your spending, cut unnecessary expenses, and focus on living within your means. Regularly review your budget to ensure you’re on track.

-

Set Realistic Goals: Write down both short-term and long-term financial goals. Break them into smaller, manageable steps to make progress more achievable.

By following these steps and strategies, you can improve your personal and financial stability. This sets you on the path to achieving financial success and security.

Next, we’ll explore more about building a strong financial foundation through education, career advancement, and financial literacy.

Conclusion

Achieving financial success isn’t an overnight feat. It’s a journey that requires careful planning, consistent effort, and informed decision-making. At Elite Tax Strategy Solutions, we understand the importance of not just reaching financial goals but maintaining financial stability over time. Our approach is rooted in proactive tax planning, which is essential for optimizing your finances and securing your future.

With our personalized services, we help high earners and closely held businesses steer the complexities of the tax system. Our strategies are designed to maximize tax savings and align with your long-term financial objectives. Whether you’re aiming to reduce debt, build an emergency fund, or plan for retirement, we have the expertise to guide you every step of the way.

The key to financial stability is a solid foundation. This includes effective budgeting, smart saving, and strategic investing. By leveraging these principles and working with a team that understands your unique needs, you can improve your personal and financial planning.

For more insights and to start your journey toward financial stability, explore our comprehensive financial planning services. Let us help you take control of your financial future.