Navigating the Complex World of Transfer Pricing

Transfer pricing compliance refers to the process of documenting, reporting, and ensuring that prices charged between related companies for goods, services, or intellectual property meet the “arm’s length” standard required by tax authorities worldwide.

Key Elements of Transfer Pricing Compliance:

- Documentation Requirements:

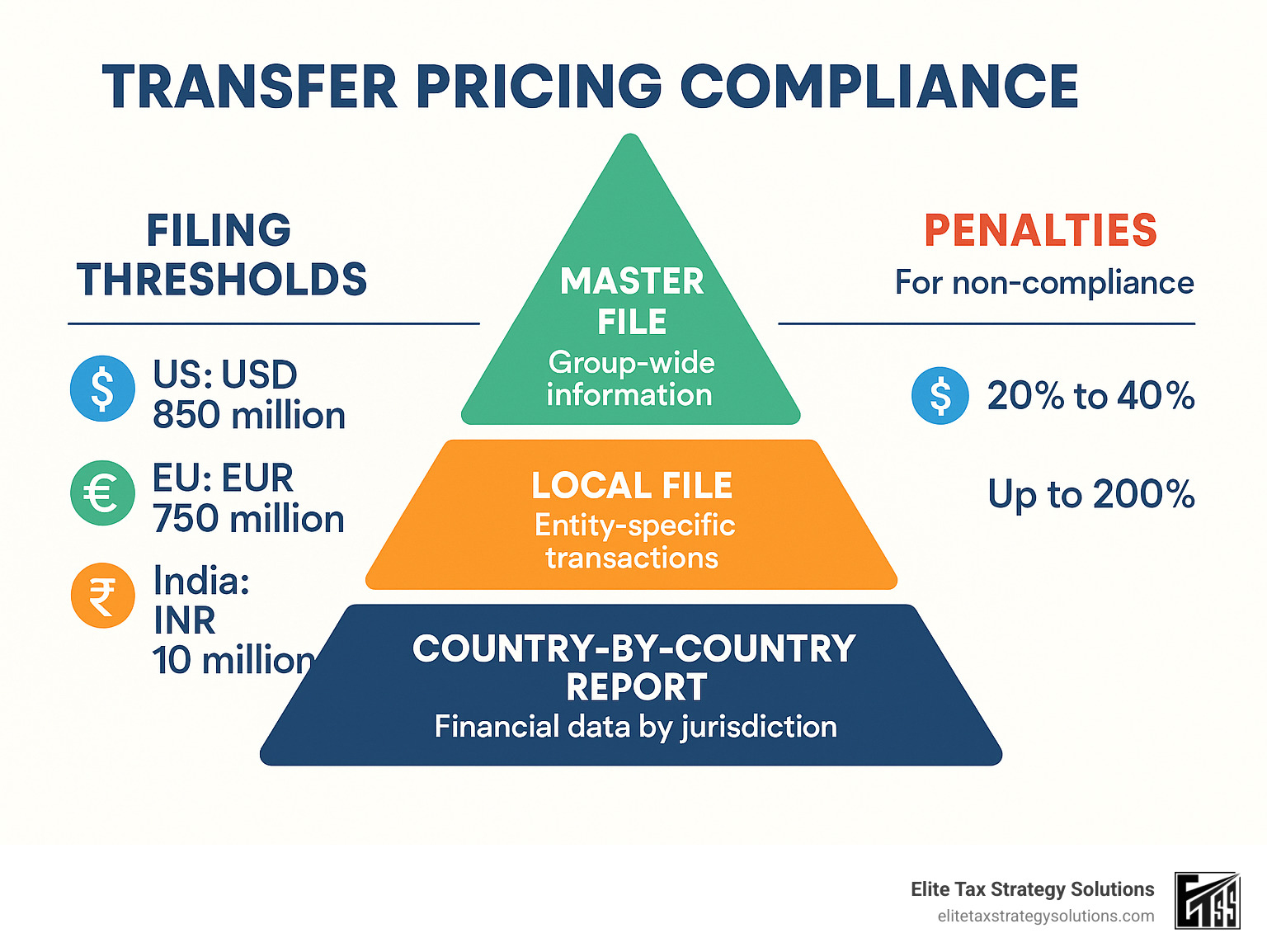

- Master File (group-wide information)

- Local File (entity-specific details)

-

Country-by-Country Report (for large multinationals)

-

Major Thresholds:

- US: USD 850 million in group revenue for CbC reporting

- EU: EUR 750 million in group revenue for CbC reporting

-

India: INR 10 million for transaction-specific documentation

-

Compliance Risks:

- Penalties ranging from 20% to 40% of unpaid taxes in the US

- Up to 200% penalties in countries like India

- Double taxation and reputational damage

In today’s interconnected global economy, transfer pricing compliance has evolved from a mere tax requirement into a critical strategic function for multinational businesses. With tax authorities worldwide intensifying their scrutiny of cross-border transactions, the stakes have never been higher. Over 100 countries can now issue tax adjustments for companies that shift profits offshore through incorrect transfer prices, and the IRS alone issued 180 voluntary compliance letters to foreign-owned distributors in 2024.

The OECD’s Base Erosion and Profit Shifting (BEPS) initiative has fundamentally changed how tax authorities view intercompany transactions, shifting focus from legal contracts to economic substance. This means your documentation must not only exist but also tell a coherent story about how profits align with actual value creation.

I’m David Fritch, a CPA with 40 years of experience helping businesses steer complex tax regulations including transfer pricing compliance as part of comprehensive tax planning strategies for high-income earners and small business owners through Elite Tax Strategy Solutions.

Transfer pricing compliance basics:

– international tax compliance

– foreign tax compliance

– tax compliance audit

What You’ll Learn

In this comprehensive guide, we’ll explain transfer pricing compliance by breaking down:

- The fundamental concepts of transfer pricing and the arm’s-length principle

- Global documentation requirements and jurisdiction-specific thresholds

- Practical strategies to transform compliance from a burden into a strategic advantage

- Technology solutions that can streamline your documentation process

- Best practices for audit defense and risk mitigation

Whether you’re a CFO of a multinational enterprise or a business owner with international subsidiaries, this guide will help you steer the complex world of transfer pricing without the headaches typically associated with compliance.

The Fundamentals: Transfer Pricing, Arm’s-Length & Why It Matters

At its core, transfer pricing refers to the prices at which related entities within the same corporate group exchange goods, services, or intangible assets. While this might sound like an internal accounting matter, it has profound tax implications because these prices directly affect where profits are recognized and taxed.

Consider this scenario: Company A in the US (with a 21% corporate tax rate) sells widgets to its subsidiary, Company B, in a country with a 10% tax rate. If Company A artificially underprices these widgets, more profit ends up with Company B in the lower-tax jurisdiction. This is precisely what tax authorities worldwide are trying to prevent.

As one tax expert noted, “Transfer pricing is far more than ‘just another tax compliance issue.’ It impacts cash flow and stakeholder interests across the organization, not just tax liability.”

The solution? The arm’s-length principle.

Anatomy of an Arm’s-Length Deal

The arm’s-length principle is the international standard that requires related parties to set transfer prices that would have been agreed upon between unrelated parties in similar circumstances. It sounds simple, but implementation is complex.

To determine an arm’s-length price, you must conduct a thorough analysis of:

- Functions performed by each entity (manufacturing, distribution, R&D)

- Assets employed (facilities, equipment, intellectual property)

- Risks assumed (market risk, inventory risk, credit risk)

This “FAR analysis” forms the backbone of any transfer pricing documentation. Once completed, you’ll need to find comparable transactions between unrelated parties to benchmark your intercompany prices.

“The most useful transfer pricing documentation reports include full data explanations in functional format, detailed risk and profit allocation analyses, and summaries that speed examiner review,” according to IRS guidance.

Economic Substance vs. Legal Form

One of the most significant shifts in transfer pricing enforcement is the emphasis on economic substance over legal form. The OECD’s BEPS initiative has driven this change, requiring that profit allocation align with actual value creation.

This means that simply having contracts in place is no longer sufficient. Tax authorities want to see that the entity reporting the profits is actually performing the functions, employing the assets, and managing the risks that generate those profits.

For example, if your Irish subsidiary owns valuable intellectual property but all R&D activities occur in the United States, tax authorities may challenge the arrangement, arguing that profits attributable to that IP should be recognized where the value-creating activities actually occur.

Who Must Play by the Rules?

While large multinational enterprises (MNEs) face the most comprehensive requirements, transfer pricing compliance affects businesses of all sizes with cross-border related-party transactions.

Consider these examples:

- A U.S. manufacturer with a small sales office in Canada

- A technology company licensing software to its foreign subsidiaries

- A family-owned business with production facilities in Mexico

- A startup with R&D operations in multiple countries

Surprisingly, even relatively small companies can face significant documentation requirements. In Mexico, businesses with annual revenue of approximately USD 720,000 must prepare full transfer pricing documentation. In India, the threshold is even lower—around USD 123,000 for related-party transactions.

As one practitioner observed, “Start-ups in certain jurisdictions face the same documentation burden as much larger enterprises due to low thresholds.”

The Compliance Toolkit: Global Rulebook, Documentation & Thresholds

When it comes to transfer pricing compliance, the OECD’s BEPS Action 13 has been a game-changer. It created a standardized three-tiered approach that many countries have acceptd, though with their own unique twists. Think of it as a global recipe where each country adds its own special ingredients:

- Master File: Your bird’s-eye view of the entire multinational group’s operations

- Local File: The detailed story of specific intercompany transactions

- Country-by-Country Report (CbCR): A global snapshot showing where you earn money, pay taxes, and conduct business

These three elements work together like a well-orchestrated symphony – when done right, they create harmony with tax authorities worldwide. But miss a note, and you might find yourself facing some serious consequences.

Transfer Pricing Compliance Requirements by Jurisdiction

The thresholds for documentation vary dramatically depending on where you do business. It’s a bit like speed limits – they change when you cross borders, and exceeding them can be costly.

In the United States, you’ll need to prepare a CbCR if your group’s annual revenue tops USD 850 million. While Uncle Sam doesn’t formally require Master and Local Files, you’ll still need similar documentation to avoid penalties under IRC §6662(e). It’s like saying “we don’t require formal evening wear, but you still can’t show up in pajamas.”

Across the pond in the European Union, the CbCR threshold sits at EUR 750 million in annual revenue. Most EU countries require Master and Local Files for companies exceeding certain thresholds, though these vary by country – making compliance a bit like navigating a maze with constantly shifting walls.

In India, the bar is set much lower – entities with related-party transactions exceeding INR 10 million (about USD 123,000) must prepare detailed documentation. And the stakes are high: India can impose penalties up to 200% of the tax sought to be evaded. That’s not a typo – 200%!

Down under in Australia, entities with annual global income of AUD 1 billion or more must lodge CbC statements, including Master and Local Files. Australia does offer simplified record-keeping options for smaller entities – a welcome relief for mid-sized businesses.

As one of our tax advisors often quips, “The question isn’t whether to prepare transfer pricing documentation, but how to make the process as painless and effective as possible.” This is especially true given the severe penalties for non-compliance.

Core Files & What Goes Inside

Each component of the three-tiered documentation tells a different part of your company’s story:

Your Master File provides the big picture – think of it as the establishing shot in a film. It includes your organizational structure, business descriptions, intangible assets overview, intercompany financial activities, and overall financial and tax positions. It helps tax authorities understand where your company fits in the global economy.

The Local File zooms in on the details – like a close-up shot. It contains specific information on intercompany transactions, functional analysis of the local entity, your chosen transfer pricing methods, financial data, comparability analysis, and copies of material intercompany agreements. This is where you justify the pricing of specific transactions.

Your Country-by-Country Report is like the credits roll showing who did what where – providing revenue data for each jurisdiction, profit before income tax, income tax paid and accrued, stated capital and accumulated earnings, employee numbers, and tangible assets. This gives tax authorities a quick way to spot potential mismatches between economic activity and reported profits.

Beyond these three core documents, well-crafted intercompany agreements are essential. These should clearly outline the rights, responsibilities, and risks of each party and align perfectly with your functional analysis. As one transfer pricing specialist puts it, “Good intercompany agreements need clarity, precision, alignment with your analyses, transparent pricing terms, local compliance, and regular updates.”

Timing, Updates & Contemporaneous Rules

Transfer pricing compliance isn’t a “set it and forget it” exercise – it’s more like gardening, requiring regular attention and care. Your documentation must be:

Contemporaneous – prepared by the time you file your tax return, not hastily assembled when an audit notice arrives. In the tax world, hindsight isn’t 20/20; it’s potentially costly.

Available – ready to provide to tax authorities within a specified timeframe, often just 30 days. This is not the time to be scrambling through digital files or dusty cabinets.

Updated – refreshed annually or whenever significant changes occur in your business. Yesterday’s documentation rarely fits today’s business reality.

What might trigger the need for updates? Several scenarios come to mind: business restructuring like mergers or internal reorganizations; launching new product lines or services; shifting key functions or risk allocations between entities; significant market changes affecting comparability; or evolving transfer pricing regulations.

One of our advisors likes to say, “A transfer pricing documentation project isn’t just checking a compliance box; it’s an opportunity to gain insights into operational weaknesses and potential improvements.” This perspective transforms what might seem like a burden into a strategic opportunity.

Penalties for Getting It Wrong

The stakes for non-compliance are higher than many realize:

In the United States, the IRS can impose penalties ranging from 20% to 40% of underpaid taxes, depending on how serious they consider the violation.

India takes an even harder line, with penalties potentially reaching a staggering 200% of the tax sought to be evaded.

Across the European Union, many countries calculate penalties based on a percentage of the adjustment or apply a fixed amount for each missing document.

But financial penalties are just the beginning. Other risks include the headache of double taxation when adjustments in one country aren’t matched by corresponding adjustments in another; extended audits that drain valuable management time and resources; and potential reputational damage affecting relationships with stakeholders, investors, and even customers.

The enforcement landscape is intensifying too. In 2024, the IRS has already issued 180 voluntary compliance letters to foreign-owned distributors by mid-November – a clear signal they’re taking a more proactive approach to transfer pricing enforcement. Their message is clear: get your house in order before we come knocking.

For more information about navigating these complex requirements, check out the OECD’s research on BEPS or the IRS Transfer Pricing Documentation FAQs.

From Risk to Advantage: Best Practices, Technology & Audit Defense

Let’s face it – transfer pricing compliance often feels like a burden. But what if I told you it could actually become a competitive advantage? Many of our forward-thinking clients have transformed what was once a defensive tax exercise into a strategic business tool.

The secret lies in shifting your perspective. Instead of viewing transfer pricing compliance as just another box to check, consider how proper documentation can provide valuable insights into your business operations and supply chain.

One of my clients recently told me, “Once we started looking at transfer pricing proactively, we finded inefficiencies in our intercompany relationships we never would have noticed otherwise.” This is exactly the mindset shift that can turn compliance into opportunity.

More info about Tax Compliance Services

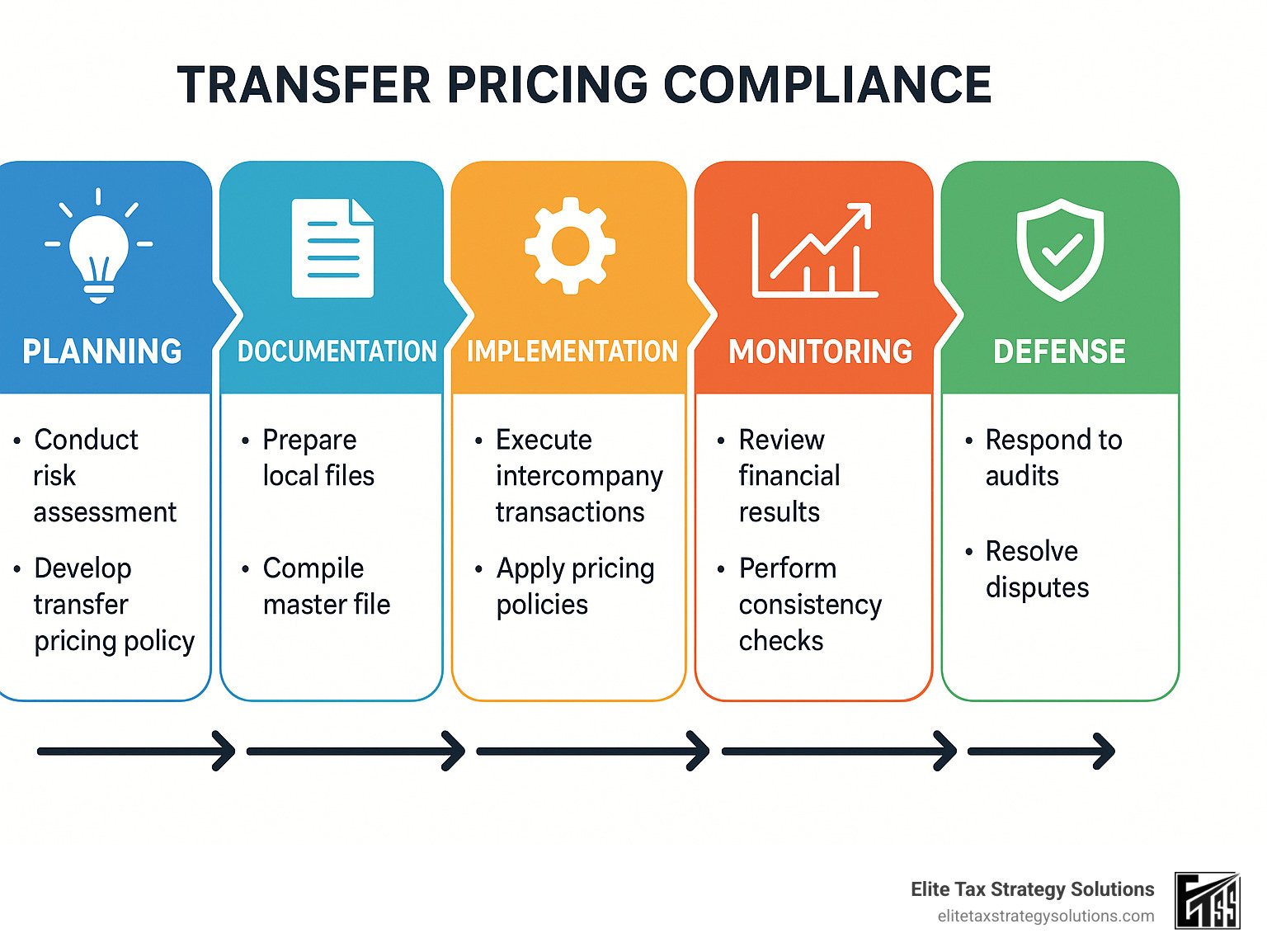

Building a Transfer Pricing Compliance Playbook

Creating a structured approach to transfer pricing compliance doesn’t have to be overwhelming. At Elite Tax Strategy Solutions, we help clients develop frameworks that are thorough yet practical.

Your compliance playbook should start with clear policies and governance. Document who’s responsible for what, and establish approval processes for intercompany transactions. This creates accountability and ensures nothing falls through the cracks.

Aim for global consistency with local flexibility. While your overall approach should be standardized, you’ll need to accommodate jurisdiction-specific requirements. Tax authorities in different countries often have different priorities.

Be realistic about what you document. As one of my colleagues wisely puts it, “While a perfect matrix is admirable, focusing on key intercompany transactions often suffices. Supporting 75-80% of intercompany transactions is typically sufficient.” This materiality-based approach saves time and resources.

An annual compliance calendar is worth its weight in gold. Map out key deadlines, review periods, and update requirements to avoid last-minute scrambles. Your tax team will thank you!

Transfer Pricing Compliance in the Digital Age

Technology has been a game-changer in the transfer pricing compliance world. The days of manually extracting data from multiple systems and creating documentation from scratch are (thankfully) behind us.

Modern solutions can now automatically pull transaction data from your ERP systems, apply analytics to identify outliers, and even generate standardized reports from templates. One client reduced their documentation time by 60% using these tools – time they now spend on strategic tax planning instead.

Real-time monitoring is particularly valuable. Rather than finding problems after year-end, you can track transfer pricing outcomes throughout the year and make adjustments as needed. This proactive approach significantly reduces audit risk.

The technology doesn’t have to be expensive or complex. Options range from specialized transfer pricing software to simpler cloud-based platforms. We can help you find the right fit based on your size, complexity, and budget.

Staying Ahead of the Audit Curve

The best audit defense is preparation before you ever receive that dreaded notice. Think like a tax authority – what would they question in your documentation?

Start with a thorough self-assessment. Run sensitivity analyses on your comparable sets and profit-level indicators to identify potential weak spots. Update your benchmarking studies regularly – typically every three years, though some jurisdictions require more frequent updates.

Focus on the quality of your documentation. Tax authorities consistently look for:

The IRS specifically recommends including a clear intercompany transaction summary at the beginning of your documentation. This helps examiners quickly understand your business and can sometimes lead to early deselection during risk assessment. In other words, good documentation might keep you off the audit list entirely!

I’ve seen this with a manufacturing client who faced an IRS transfer pricing examination. Their comprehensive documentation, which clearly linked their pricing policies to their business model, resulted in no adjustments and a much shorter audit process than anticipated.

Transfer pricing compliance might never be your favorite business activity, but with the right approach, it can become much more than just a tax requirement. It can provide valuable insights, improve operational efficiency, and ultimately protect your bottom line.

Scientific research on IRS TP FAQs

Frequently Asked Questions about Transfer Pricing Compliance

How often should we update documentation?

If there’s one question I hear from almost every client, it’s about documentation frequency. The simple answer is that transfer pricing documentation should typically be updated annually in most countries. But let me share a practical perspective on this.

Think of your documentation like your car’s maintenance schedule. Sometimes you need a complete overhaul, other times just routine service:

For full updates, look at significant changes in your business – maybe you’ve restructured operations, shifted key functions between entities, or experienced major market disruptions. These situations call for a comprehensive refresh of your documentation.

When your business remains relatively stable, light updates often suffice. You can reference your previous studies while refreshing the financial data and addressing any minor operational changes.

I had a client who thought their stable manufacturing business could skip updates for three years. Unfortunately, they missed documenting a small but significant shift in their supply chain decision-making that later triggered a costly audit. As one of my colleagues puts it, “Proactive, annual reviews of transfer pricing files are essential to stay ahead of evolving regulations.”

What triggers a transfer-pricing audit?

Understanding what catches a tax authority’s attention can help you stay off their radar. In my experience working with multinational clients, several red flags consistently attract unwanted scrutiny.

Persistent losses in local entities while the global group reports healthy profits often raise eyebrows. Tax authorities naturally question why a rational business would continue operations that consistently lose money.

Significant transactions between related parties, especially involving intangibles or financing arrangements, attract attention due to their profit-shifting potential. I’ve seen cases where a single large royalty payment triggered a comprehensive audit of all intercompany transactions.

Business restructuring that shifts functions, risks, or valuable assets between jurisdictions often signals potential profit shifting to tax authorities. One manufacturing client’s seemingly routine shift of procurement decisions to a low-tax jurisdiction triggered a multi-year examination.

Unusually low effective tax rates in high-tax jurisdictions compared to industry norms often trigger automatic selection in many countries’ risk assessment systems.

Industry focus matters too – if you’re in a sector currently under scrutiny, you’re more likely to be selected. As one audit defense specialist told me, “Auditors expect consistent subsidiary profits even during downturns, potentially forcing parent companies to absorb losses via price adjustments.”

Can technology really cut compliance time in half?

Yes – but with an important caveat that I always share with clients considering technology investments. The results depend heavily on your implementation approach and organizational readiness.

I’ve seen companies achieve remarkable efficiency gains – between 40-60% reduction in data gathering time alone – when they approach technology implementation strategically. The key is ensuring your data sources are well-structured and accessible before automation.

One mid-sized manufacturing client of ours reduced their documentation time from eight weeks to just three by implementing specialized transfer pricing software after we helped them standardize their intercompany data collection processes.

Beyond time savings, good technology improves accuracy through automated consistency checks and improves audit readiness with on-demand reporting. As my technology specialist colleague often says, “Automation and data analytics are key levers to streamline transfer pricing processes.”

At Elite Tax Strategy Solutions, we take a practical approach to technology. We help clients evaluate whether sophisticated software makes sense for their situation or if simpler solutions might deliver better ROI. Sometimes a well-designed spreadsheet template with clear processes can deliver significant improvements without the complexity of enterprise software.

We focus on solutions that deliver meaningful efficiency without unnecessary complexity – because transfer pricing compliance should support your business strategy, not consume it.

Conclusion

The journey through transfer pricing compliance might seem daunting at first glance, but it doesn’t have to be overwhelming. When approached thoughtfully, what starts as a tax obligation can actually become a valuable business asset that protects your company while supporting your broader financial goals.

After working with countless businesses on their transfer pricing challenges, I’ve seen how the right strategy makes all the difference. The companies that thrive don’t view compliance as just another box to check – they integrate it into their business DNA.

The most successful approach to transfer pricing compliance starts with being proactive. Don’t wait until you receive that audit notice to start organizing your documentation. By then, you’re already playing defense. Instead, build your strategy before problems arise, ensuring your intercompany pricing aligns with actual value creation across your business.

Technology has transformed what used to be months of manual spreadsheet work into streamlined processes that save both time and headaches. The companies I see getting the most value from their compliance efforts are those embracing digital tools – not just for documentation, but for ongoing monitoring that keeps them ahead of potential issues.

Not all transactions carry equal risk. A thoughtful, risk-based approach lets you focus your resources where they matter most. Your Australian subsidiary selling $10 million of product to your U.S. parent company deserves more attention than the $5,000 management fee charged to your Canadian office.

Business never stands still, and neither should your transfer pricing compliance strategy. Regular updates to your documentation ensure it reflects your current business reality – not how things looked three years ago. This ongoing maintenance is far less painful than scrambling to recreate history during an audit.

At Elite Tax Strategy Solutions, we view transfer pricing not as an isolated tax issue but as a key piece of your overall financial puzzle. Our approach integrates compliance seamlessly with your broader tax planning, helping you steer global requirements while maximizing legitimate tax benefits.

Whether you’re a growing business with your first international subsidiary or a seasoned multinational with operations across dozens of countries, we bring decades of practical experience to your specific challenges. Our goal is simple: turn what many see as a compliance burden into a strategic advantage for your business.

Ready to make transfer pricing compliance work for you instead of against you? Let’s talk about creating a custom approach that protects your business while supporting your growth objectives.