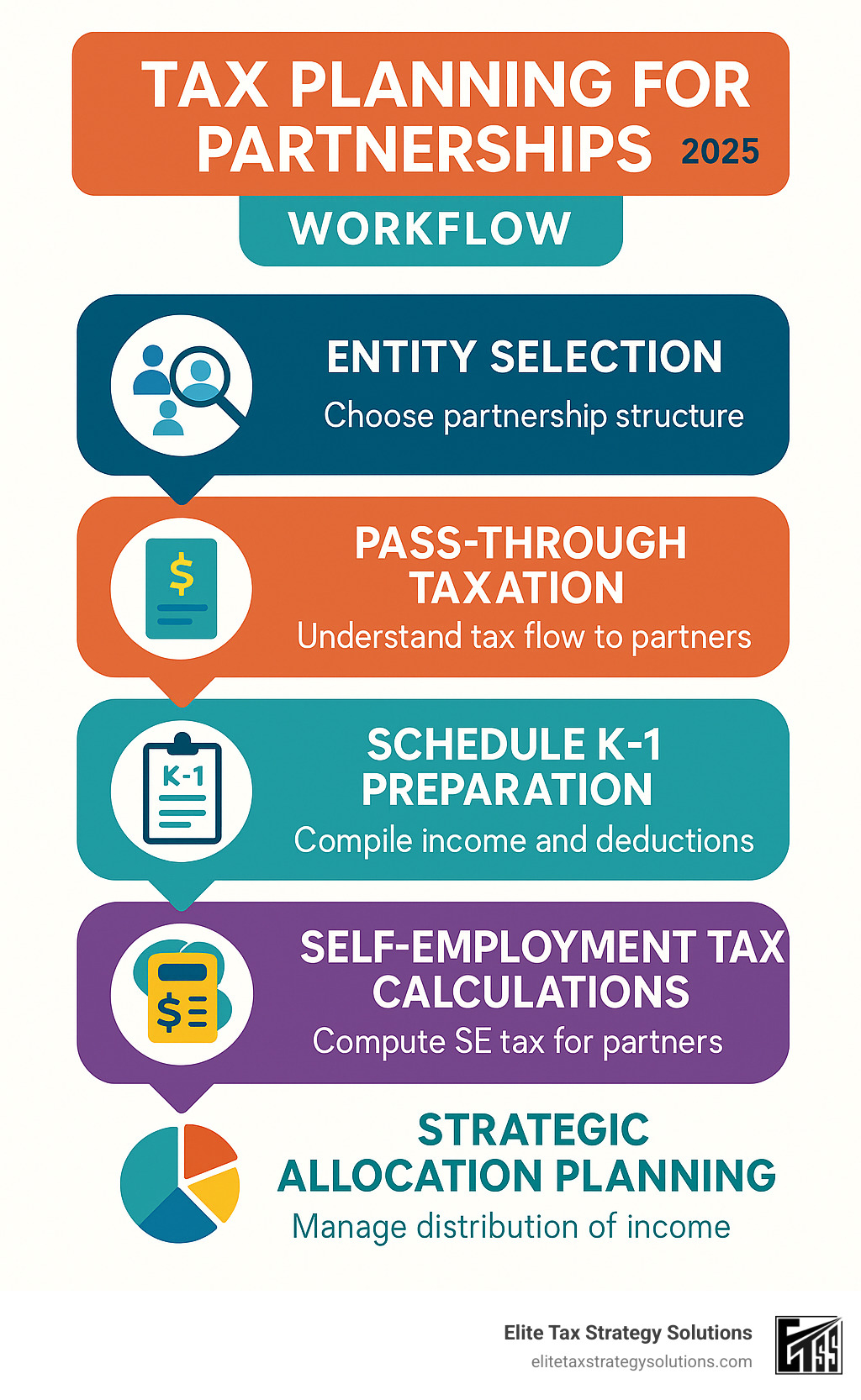

Why Tax Planning for Partnerships is Critical for Business Success

Tax planning for partnerships requires a strategic approach that can save thousands of dollars annually while ensuring compliance with complex regulations. Here’s what you need to know:

Key Partnership Tax Planning Elements:

- Pass-through taxation – Profits and losses flow directly to partners’ personal tax returns

- Schedule K-1 reporting – Each partner receives detailed income and deduction information

- Self-employment tax considerations – General partners typically pay SE tax on their share of income

- Special allocations – Ability to distribute profits and losses disproportionately to ownership

- Basis management – Tracking each partner’s tax basis for deduction limitations

Partnership taxation operates differently than corporate structures, creating unique opportunities and challenges. Unlike corporations that face double taxation, partnerships are pass-through entities where income flows directly to partners’ individual tax returns.

The complexity lies in the details. Partners must steer self-employment taxes, basis calculations, and distribution strategies while maximizing available deductions. Without proper planning, partnerships often miss valuable tax-saving opportunities or face unexpected tax burdens.

Many business owners find partnership tax rules overwhelming. The interplay between partnership-level elections, individual partner circumstances, and ever-changing tax laws requires expertise to steer effectively.

I’m David Fritch, and with 40 years of experience as both a CPA and attorney, I’ve helped countless partnerships optimize their tax strategies while ensuring compliance. Through Elite Tax Strategy Solutions, I specialize in tax planning for partnerships and have developed proven strategies that help business owners maximize their tax savings while working less.

Key Tax planning for partnerships vocabulary:

Understanding Partnership Taxation

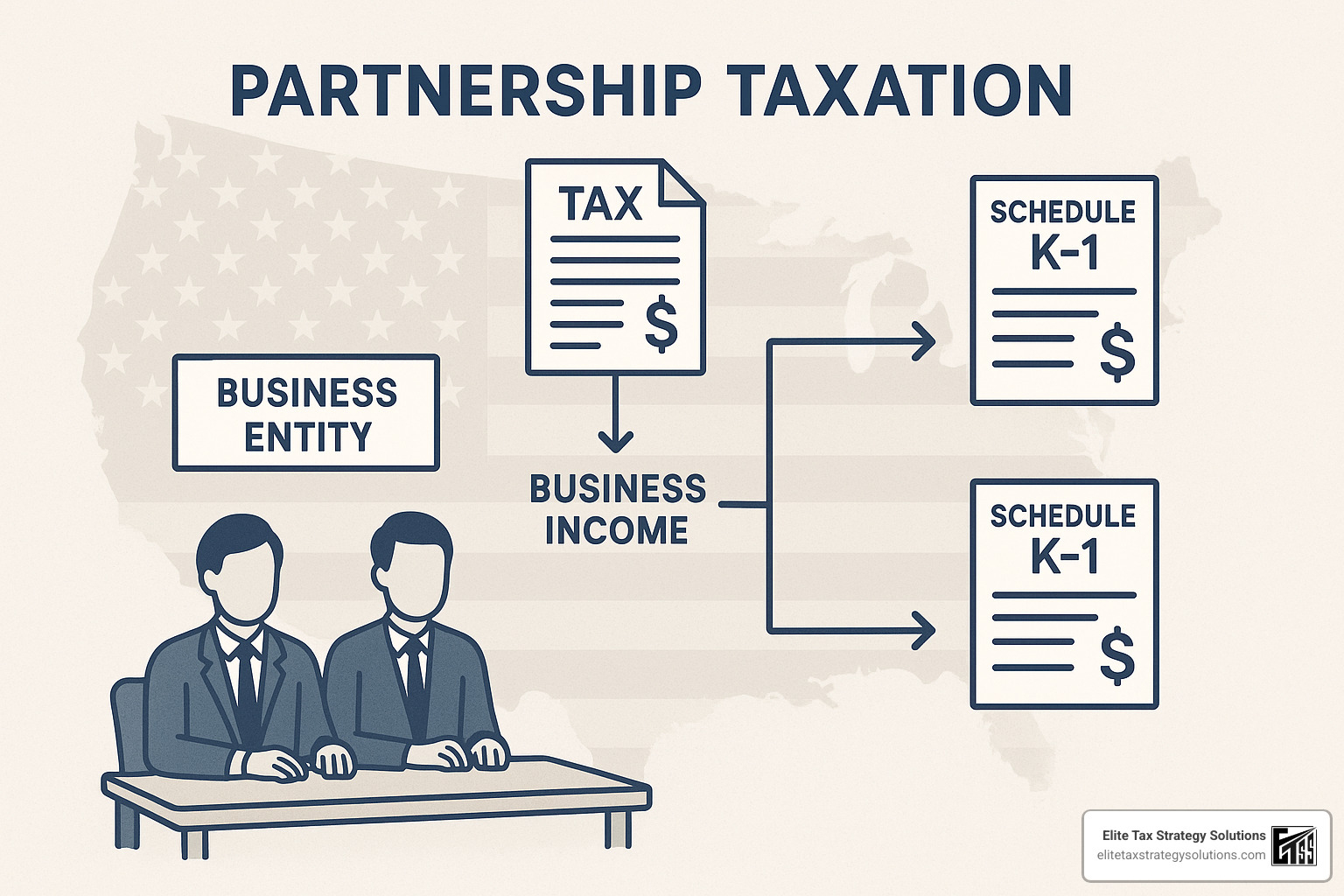

Partnership taxes work differently than what most business owners expect. Think of a partnership like a funnel – all the money flows through to the partners, but the partnership itself doesn’t pay federal income tax.

This pass-through taxation system means you’ll report your share of partnership income on your personal tax return. Here’s where it gets tricky: you owe taxes on your share whether you actually took money out of the business or not.

Let’s say your partnership made $100,000 profit this year, and you own 50%. You’ll pay taxes on $50,000 even if the partnership kept all the money to buy new equipment. This “phantom income” catches many partners off guard during their first tax season.

Schedule K-1 becomes your best friend (or worst enemy) during tax time. This form tells you exactly what to report on your personal return. Your K-1 shows your slice of the partnership’s ordinary business income or loss, capital gains and losses, deductions and credits, special allocations, and basis adjustments.

The partnership must send you this form by March 15th, which is why many partners file extensions – they’re waiting for their K-1 to arrive.

Self-employment tax adds another wrinkle to partnership taxation. If you’re a general partner actively working in the business, you’ll typically pay self-employment tax on your share of partnership income. That’s an extra 15.3% on top of your regular income tax. The IRS provides detailed guidance on self-employment tax calculations and requirements.

Limited partners often dodge this bullet. If you’re just an investor without day-to-day involvement, you might avoid self-employment tax entirely. This difference can save thousands of dollars annually.

The timing issue trips up many partners. You report income when the partnership earns it, not when you receive cash. This means careful tax planning for partnerships must include cash flow planning to ensure partners can pay their tax bills even when profits stay in the business.

Understanding these basics helps you make smarter decisions about distributions, reinvestment, and year-end planning. The key is staying ahead of the tax implications rather than scrambling at year-end.

Tax Planning for Partnerships

Smart tax planning for partnerships is like putting together a puzzle where every piece affects the whole picture. The secret is understanding how decisions made at the partnership level ripple through to each partner’s individual tax situation.

Tax optimization begins before you even start operating. Your partnership agreement becomes the foundation for all future tax planning. Think of it as your roadmap for navigating complex tax rules while keeping maximum flexibility.

The partnership agreement should address how you’ll handle special allocations of income and losses. Maybe one partner needs more depreciation deductions this year, while another could benefit from additional income. With proper planning, you can make this happen legally and beneficially.

Deductions work differently in partnerships than you might expect. The partnership takes deductions at the entity level, then passes them through to partners via Schedule K-1. But here’s the catch – just because the partnership can deduct something doesn’t mean each partner can fully use that deduction on their personal return.

Common partnership deductions include business expenses, depreciation, Section 179 deductions, interest expenses, professional fees, and equipment purchases. The key is timing these deductions when partners can maximize their benefit.

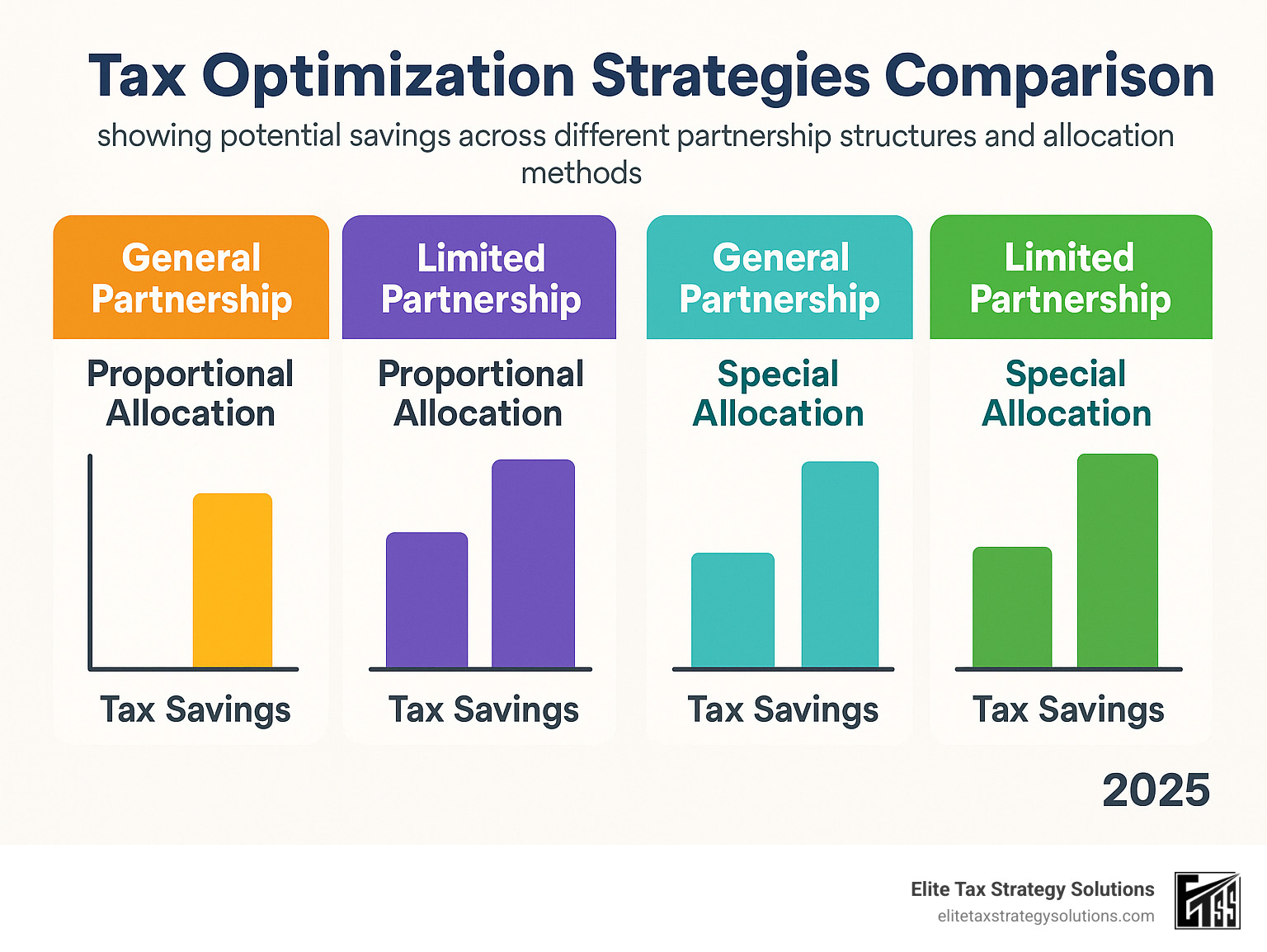

Special allocations give partnerships a superpower that other business structures don’t have. You can allocate specific items of income, loss, or deduction in ratios completely different from ownership percentages. One partner owns 50% but gets 70% of the depreciation deductions? Perfectly legal with proper documentation.

We regularly help partnerships use special allocations to allocate depreciation to partners who can best use the deductions, distribute losses to partners with other income to offset, and manage the impact of debt-financed income. The IRS requires these allocations to have “substantial economic effect,” which means they must make real economic sense beyond just saving taxes.

Your partnership’s tax year selection might seem like a minor detail, but it can significantly impact your tax planning opportunities. Most partnerships must use the calendar year, but some can elect fiscal years with proper planning and IRS approval. This decision affects when partners report income and opens up year-end planning strategies.

The timing difference between when partnerships earn income and when partners receive cash creates unique planning opportunities. You might strategically time distributions or defer income to optimize each partner’s individual tax situation.

Key Tax Forms for Partnerships

Getting your partnership tax forms right isn’t just about staying compliant—it’s the foundation of effective tax planning for partnerships. Think of these forms as your partnership’s financial storytelling tools, each one serving a specific purpose in the complex world of partnership taxation.

Form 1065 is your partnership’s main annual tax return, even though partnerships don’t actually pay federal income tax. This comprehensive form tells the IRS everything about your partnership’s financial year, including all income and expenses, balance sheet details, and how profits and losses get allocated among partners.

Here’s something that catches many partnerships off guard: Form 1065 is due by March 15th for calendar-year partnerships. That’s a full month earlier than individual tax returns. Miss this deadline, and you’ll face penalties of $200 per partner per month for each month you’re late. With a three-partner business, that’s $600 monthly in penalties alone.

The good news? You can request an automatic six-month extension, giving you until September 15th to file. Smart partnerships use this extension strategically as part of their tax planning process.

Schedule K-1 works hand-in-hand with Form 1065, serving as each partner’s personal tax roadmap. This form breaks down exactly what each partner needs to report on their individual tax return. Your partners are counting on receiving their Schedule K-1 by the same March 15th deadline so they can complete their own tax planning.

Schedule K-1 covers everything from ordinary business income and guaranteed payments to special deductions and self-employment earnings. It’s like a detailed receipt showing each partner’s share of the partnership’s tax year activities.

Form 941 enters the picture when your partnership has employees. This quarterly form handles all the payroll tax reporting, including federal income tax withholding and Social Security and Medicare taxes. Even if your partnership only has one employee, you’ll need to stay on top of these quarterly filings.

State requirements add another layer of complexity that varies dramatically depending on where you do business. Some states require partnership returns even when no tax is owed, while others have completely different filing deadlines. We regularly help partnerships steer these varying requirements across multiple states, ensuring nothing falls through the cracks.

The key to mastering partnership tax forms is understanding how they work together. Form 1065 captures the big picture, Schedule K-1 distributes the details to partners, and Form 941 handles the employment side. When these forms align properly, they create a solid foundation for your partnership’s tax planning strategy.

Strategies for Effective Tax Planning

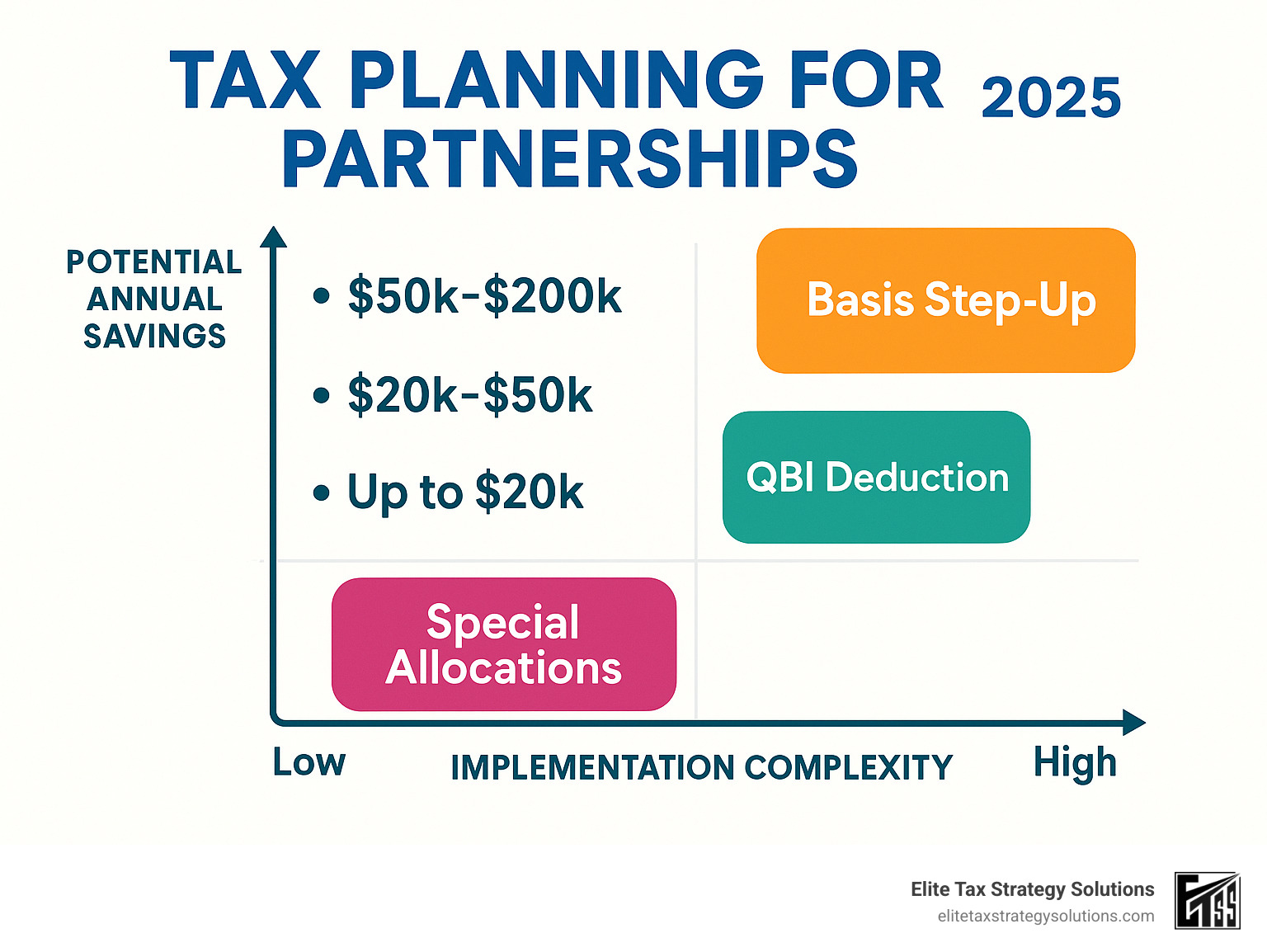

When it comes to tax planning for partnerships, the real magic happens with advanced strategies that can save you thousands of dollars each year. These aren’t your basic tax tips – they’re sophisticated approaches that require careful planning but deliver impressive results.

Let’s start with basis step-up opportunities, which sound complicated but are actually quite powerful. When partners contribute property to the partnership or when someone buys into the partnership, you can make a Section 754 election. This election allows the partnership to increase (or “step up”) the basis of partnership assets, creating additional depreciation deductions that benefit the incoming partners.

Think of it this way: if someone joins your partnership and pays $100,000 for their interest, but the partnership’s assets are recorded at lower historical costs, the step-up election lets you adjust those asset values upward. This creates more depreciation deductions, which means more tax savings.

The basis step-up election becomes particularly valuable when partners contribute appreciated property, when partnership interests are sold or transferred, or when partners have significantly different tax situations. We’ve seen this strategy save partnerships tens of thousands of dollars annually.

QBI deduction under Section 199A is another game-changer. This provision allows up to a 20% deduction for qualified business income from partnerships. The IRS Section 199A regulations provide comprehensive guidance on eligibility and calculation requirements. Imagine reducing your taxable income by 20% – that’s substantial tax savings right there.

However, the QBI deduction comes with strings attached. There are income limitations and restrictions based on your type of business. Some service businesses face additional problems, and the deduction is limited by W-2 wages and depreciable property in certain situations.

To maximize QBI benefits, we help partnerships structure their operations to qualify for the deduction, manage those tricky W-2 wages and depreciable property limitations, and plan distributions to optimize each partner’s individual QBI calculations. It’s like solving a puzzle where all the pieces need to fit together perfectly.

Special tax allocations go way beyond basic profit-sharing ratios. These sophisticated allocations can allocate tax credits to partners who can actually use them, distribute depreciation deductions strategically to partners in higher tax brackets, manage the impact of debt cancellation income, and optimize state tax consequences across different jurisdictions.

The key word here is “substantial economic effect.” The IRS requires that these special allocations have real economic consequences beyond just tax benefits. When done properly, they provide incredible flexibility that you simply can’t get with other business structures.

Distribution planning affects both partnership and partner-level taxes in ways that might surprise you. Distributions of cash generally aren’t taxable to partners unless they exceed the partner’s basis in the partnership. However, distributions of property or disproportionate distributions can trigger unexpected taxable events.

We regularly implement distribution strategies that minimize taxable gain recognition, preserve partnership flexibility for future decisions, optimize cash flow for tax payments, and coordinate with each partner’s individual tax situation. The goal is to get money to partners when they need it without creating unnecessary tax burdens.

These strategies work best when they’re part of a comprehensive approach to tax planning for partnerships. Each partnership is unique, and what works for one might not work for another. That’s why we take the time to understand your specific situation and develop a customized strategy that fits your business goals and tax circumstances.

Frequently Asked Questions about Partnership Taxation

What are the types of partnerships?

When it comes to partnerships, there are two main types that affect how you’ll handle your taxes and business operations.

General partnerships are the most straightforward structure. Here, all partners roll up their sleeves and actively participate in running the business. Everyone shares management responsibilities, which means everyone also shares unlimited personal liability for partnership debts. From a tax perspective, this means general partners typically pay self-employment tax on their share of partnership income – something to keep in mind when planning your overall tax strategy.

Limited partnerships offer more flexibility and protection. These include both general partners who manage the day-to-day operations and limited partners who act as passive investors. Limited partners get liability protection but can’t participate in management decisions without risking that protection. The tax benefit? Limited partners usually avoid self-employment tax on their partnership income, making this structure particularly attractive for passive investors.

You’ll also encounter other partnership variations like limited liability partnerships (LLPs), limited liability limited partnerships (LLLPs), and master limited partnerships (MLPs). Each has different tax implications, liability protections, and operational requirements.

The choice depends on your specific situation – your role in the business, how much risk you’re comfortable with, and your tax objectives. Tax planning for partnerships starts with selecting the right structure for your goals.

How are profits and losses distributed?

One of the most powerful features of partnerships is their flexibility in distributing profits and losses. Unlike corporations with rigid structures, partnerships can be creative with their allocations.

Special allocations allow you to distribute profits and losses differently than ownership percentages. This flexibility can be a game-changer for tax planning, but the IRS has complex requirements that must be satisfied. These allocations need to have “substantial economic effect” – essentially, they need to make business sense beyond just saving taxes.

Ownership percentage typically serves as the starting point for profit and loss sharing, but your partnership agreement can modify these ratios in various ways. Partners might share equally, proportionally to their capital contributions, based on their participation in operations, or through hybrid approaches that combine multiple factors.

Your partnership agreement should clearly specify how you’ll allocate ordinary income and losses, capital gains and losses, depreciation and other deductions, and special items like Section 179 deductions. Getting this right from the start prevents confusion and potential disputes later.

We regularly help partnerships design allocation formulas that achieve their business objectives while satisfying tax requirements. This often involves balancing what makes sense economically with opportunities for tax optimization.

What is the role of Schedule K-1?

Think of Schedule K-1 as the messenger between your partnership and your personal tax return. This form provides detailed information about your share of partnership items that you’ll need to complete your individual tax return.

Income reporting through Schedule K-1 shows your allocated share of partnership income, deductions, and credits. You’ll report this information on your personal tax return, regardless of whether you actually received cash distributions from the partnership. This is where that “phantom income” situation can arise – you might owe taxes on partnership income even if the money stayed in the business.

Deductions flow through to you via Schedule K-1, but individual limitations may apply. For example, if you’re a passive investor, passive activity loss rules might limit your ability to deduct partnership losses against other income sources.

Schedule K-1 also provides crucial information for basis calculations, at-risk limitations, alternative minimum tax adjustments, state tax allocations, and foreign tax credits. All of this information plays into your overall tax picture and planning strategies.

The accuracy and timeliness of Schedule K-1 preparation is crucial for your tax compliance. We make sure our clients receive accurate K-1s that properly reflect their partnership allocations and provide all the information needed for effective individual tax planning.

Conclusion

Tax planning for partnerships doesn’t have to feel overwhelming, even though the rules can seem complex. With the right guidance and a solid plan, you can turn those complicated tax codes into real savings for your business.

Think of partnership tax planning like tending a garden – it needs regular attention throughout the year, not just at tax time. The strategies we’ve covered can save you thousands of dollars, but they work best when someone keeps an eye on them and makes adjustments as your business grows and changes.

At Elite Tax Strategy Solutions, we believe in a proactive approach that keeps you ahead of tax deadlines and opportunities. We don’t just prepare your returns and send you on your way. Instead, we work with you year-round to make sure your partnership structure is working as hard as your business does.

Our partnership clients appreciate how we handle everything from partnership agreement reviews to complex special allocations. We coordinate multi-state tax requirements, track basis calculations, and plan distributions so you can focus on running your business instead of worrying about tax compliance.

Financial stability comes from having a tax strategy that makes sense for your specific situation. Every partnership is different, and cookie-cutter approaches rarely deliver the best results. We take time to understand your business, your goals, and your partners’ individual circumstances.

The partnership structure offers incredible flexibility and tax advantages when managed properly. You shouldn’t have to miss out on these benefits because the rules seem too complicated. With four decades of combined CPA and legal experience, we’ve helped countless partnerships in Jasper, Indiana, and surrounding areas turn tax complexity into tax savings.

Ready to see what a well-planned partnership tax strategy can do for your business? Contact Elite Tax Strategy Solutions today to find how our personalized approach can help you maximize tax savings while keeping everything compliant and stress-free. Your future self will thank you for taking action now.