The High-Income Tax Challenge: Breaking Free from W-2 Limitations

When your W-2 income climbs into the higher brackets, tax season can feel like watching your hard-earned money disappear. As a high-income earner, you’re likely familiar with that sinking feeling when you see how much goes to taxes each year.

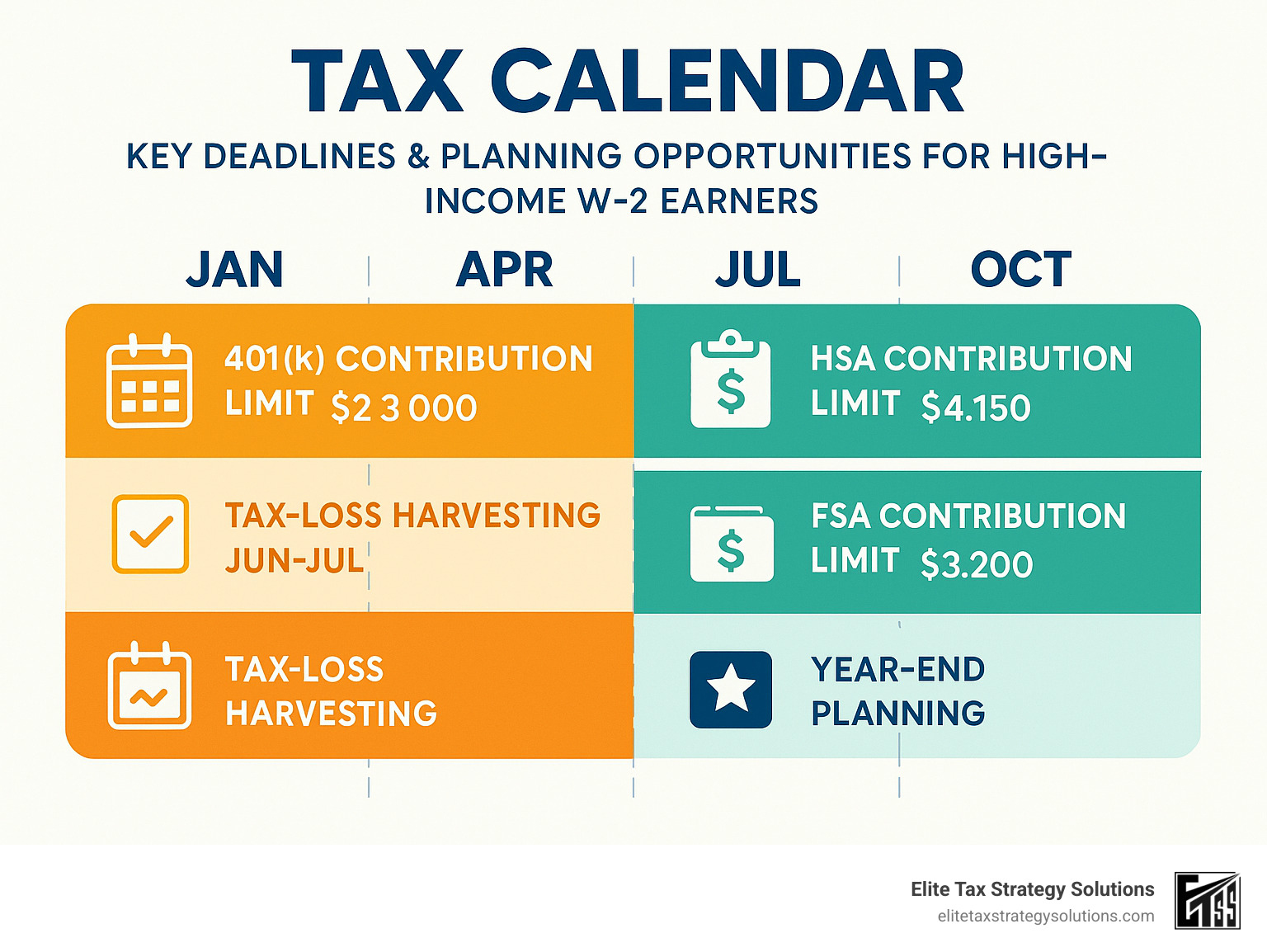

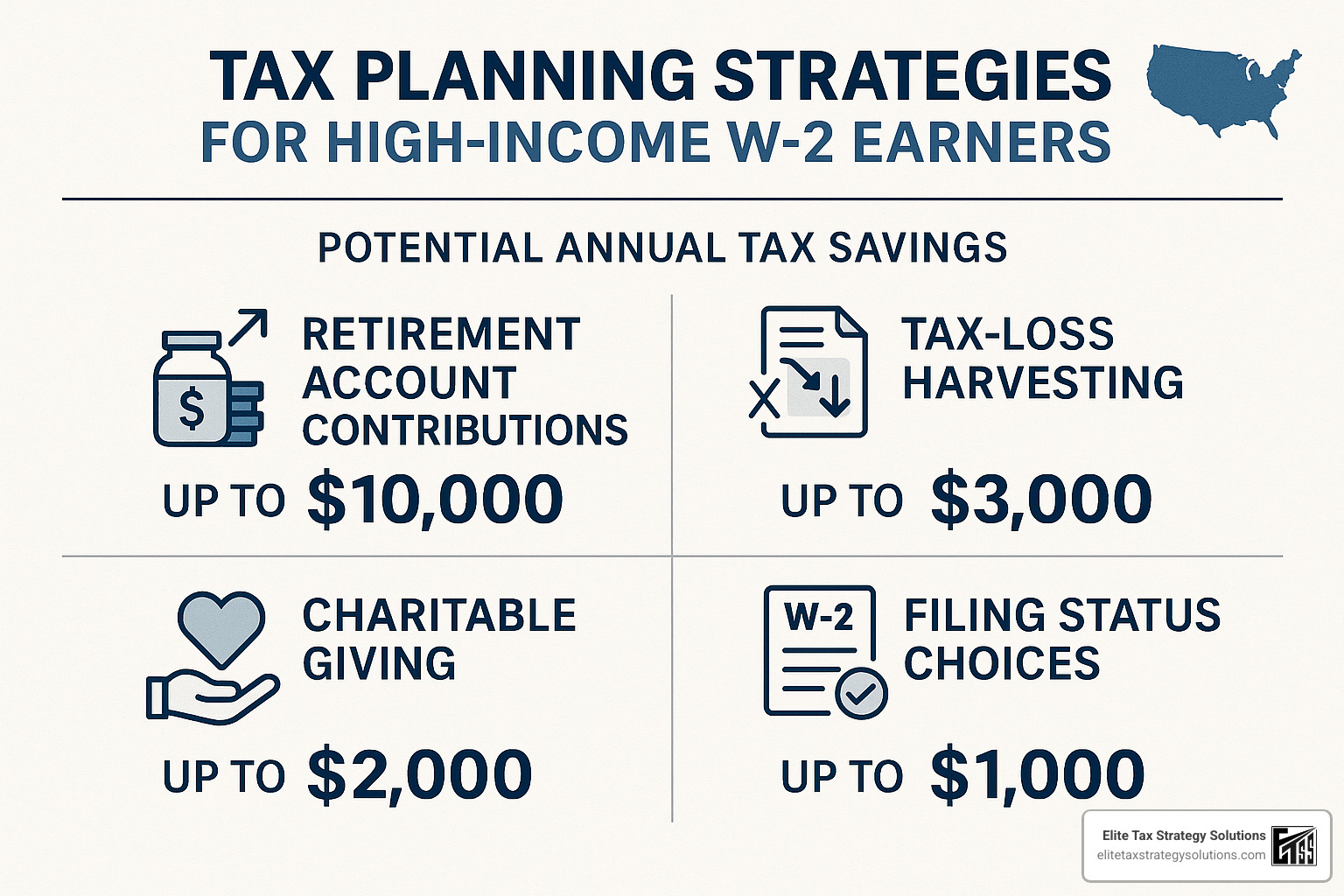

Here’s the good news: you have more control than you might think. The most powerful tax strategies for high-income W2 earners include maxing out pre-tax retirement accounts like 401(k)s, 403(b)s, and 457(b)s with their $23,000 limit for 2024 ($30,500 if you’re over 50). HSAs offer triple tax advantages with $4,150 individual and $8,300 family limits this year. Many of my clients have found success with backdoor Roth IRA strategies and even mega backdoor Roth conversions when their employer plans allow after-tax contributions.

For those with substantial income, nonqualified deferred compensation plans can strategically shift income to lower-tax years. I’ve seen tremendous tax savings when clients bunch charitable contributions using donor-advised funds to maximize itemized deductions. And don’t overlook the power of strategic tax-loss harvesting to offset gains and up to $3,000 of ordinary income.

The tax landscape is particularly challenging for W-2 employees earning substantial incomes. You’re facing federal rates up to 37%, plus those sneaky add-ons like additional Medicare taxes, state income taxes, and potential AMT exposure. Unlike business owners who can deduct expenses before paying taxes, you’re taxed on your gross income first – making strategic planning not just helpful, but essential.

I’ve always told my clients: “It’s not what you make but what you keep that counts.” While the IRS considers $200,000+ as “high-income,” most financial advisors see $500,000+ as the threshold where advanced tax planning becomes truly critical. Without proper planning, thousands of your hard-earned dollars could be unnecessarily flowing to the IRS each year.

Let me share what’s possible: A high-earning W-2 employee using layered tax strategies could reduce taxable income by over $125,000 and save more than $45,000 in taxes annually. The key is proactive planning throughout the year—not just scrambling during tax season.

I’m David Fritch, and I’ve spent 40 years as both a CPA and attorney specializing in tax strategies for high-income W2 earners. From my early days at Arthur Andersen to decades running my own practice, I’ve helped countless professionals like you optimize their tax situations while staying fully compliant with constantly changing tax laws. My approach is personalized – because your tax situation is as unique as your fingerprint.

If you’re diving deeper into tax strategies for high-income W2 earners, you might want to understand some key concepts like the extra Medicare tax for high earners, specialized tax planning for high salaried employees, or comprehensive financial planning for high income earners.

Smart tax planning isn’t about finding loopholes – it’s about making informed choices with the tax code that exists. Let’s explore how you can keep more of what you earn, legally and ethically.

What Counts as “High-Income” for W-2 Filers?

If you’ve been wondering whether you qualify as a “high-income” earner, you’re not alone. This question comes up frequently in my conversations with clients who want to know if they need more advanced tax planning.

From the IRS perspective, they officially consider you a high-income earner if you report $200,000 or more in total positive income on your tax return. But in my 40 years of tax practice, I’ve found that the practical threshold where sophisticated tax strategies for high-income W-2 earners become truly essential is closer to the $500,000 annual income mark.

Why does this distinction matter? Because once your income crosses certain thresholds, you enter the land of what I like to call “stealth taxes” – additional taxes and phase-outs that can significantly increase what you actually pay:

The federal income tax brackets climb to 37% for 2024 when you earn above $609,350 (single) or $731,200 (married filing jointly). But that’s just the beginning.

You’ll also face an additional 0.9% Medicare surtax on earned income exceeding $200,000 (single) or $250,000 (married). Then there’s the 3.8% Net Investment Income Tax (NIIT) that applies to investment earnings when your modified adjusted gross income crosses those same thresholds.

Many of my clients are surprised by the Alternative Minimum Tax (AMT) that can hit especially hard when exercising incentive stock options. And don’t forget the numerous phase-outs of deductions and credits that effectively push your marginal rate even higher.

I remember working with Sarah, a senior software engineer from Chicago, who was caught off guard when her promotion to VP of Engineering pushed her salary from $190,000 to $225,000. “I expected to pay more taxes with my raise,” she told me, “but I didn’t anticipate the extra Medicare tax or how dramatically it would affect my take-home pay.”

This challenge is particularly acute for W-2 employees. Unlike business owners who can deduct expenses before calculating their taxable income, employees are taxed on their gross income with fewer opportunities for deductions. As one of my clients bluntly put it: “No group in America pays more taxes than high-salary wage-earning W-2 employees.”

The good news? If you fall into this high-income category, you don’t have to simply accept a higher tax bill. With thoughtful planning and the right strategies, you can significantly reduce your tax burden while remaining fully compliant with tax laws.

In my practice at Elite Tax Strategy Solutions, I’ve seen how proper planning can help clients in the highest tax brackets save tens of thousands of dollars annually. The key is understanding which strategies apply to your specific situation and implementing them proactively throughout the year – not just during tax season.

Top Tax Strategies for High-Income W-2 Earners

When you’re bringing home a substantial W-2 paycheck, Uncle Sam wants his share—often a very large share. But with thoughtful planning, you can legally keep more of what you earn. Let’s explore the most powerful tax-reduction strategies that have helped my clients save tens of thousands each year.

Max Out Workplace Retirement Plans

The foundation of smart tax planning starts with maxing out your employer-sponsored retirement accounts. These contributions reduce your taxable income dollar-for-dollar while growing tax-deferred until retirement.

For 2024, you can contribute up to $23,000 to your 401(k), 403(b), or 457(b)—and if you’re 50 or older, you get an extra $7,500 catch-up contribution, bringing your total to $30,500. The overall limit including employer matches is a whopping $69,000!

I’ve had clients find creative ways to maximize these benefits. Take Andre, a tech executive who front-loads his contributions early in the year.

“I actually enjoy seeing those $0 paychecks in April and May,” he told me with a laugh. “My money starts working for me sooner, and I never risk missing my full employer match if something unexpected happens later in the year.”

For those working in education or non-profits, there’s an even bigger opportunity—you can often contribute to both a 403(b) AND a 457(b) plan simultaneously. This strategy allowed my client Dr. Williams to shelter over $46,000 from taxes in a single year. Talk about a tax bill reduction!

More info about Traditional IRA for High-Income Earners

The Classic & Mega Backdoor Roth Playbook — Tax Strategies for High-Income W2 Earners

High earners face a frustrating roadblock—you make too much to contribute directly to a Roth IRA (phased out at $146,000 for singles and $230,000 for married couples in 2024). But there are two powerful workarounds: the classic backdoor Roth and its bigger sibling, the mega backdoor Roth.

The classic backdoor Roth is a two-step dance:

1. Contribute $7,000 ($8,000 if 50+) to a traditional IRA without taking a tax deduction

2. Convert that contribution to a Roth IRA shortly afterward

While $7,000 might seem small compared to your income, the tax-free growth over decades can be substantial. Just watch out for the “pro rata rule” if you have existing pre-tax IRA balances—this can trigger unexpected taxes. I typically recommend rolling any pre-tax IRA funds into your employer’s 401(k) before implementing this strategy.

The mega backdoor Roth is where things get really exciting. Michael, a product manager I work with, explained it best:

“After maxing out my pre-tax 401(k), I contribute another $32,000 after-tax, which automatically converts to my Roth 401(k) daily. This gives me over $55,000 in retirement contributions each year, and a huge chunk will grow completely tax-free for decades.”

To use this strategy, your employer plan must allow after-tax contributions (beyond the standard $23,000 limit) and either in-plan Roth conversions or in-service withdrawals. Not all plans offer these features, so check with your HR department.

Harness HSAs & FSAs for Triple Tax Wins — Tax Strategies for High-Income W2 Earners

Health Savings Accounts (HSAs) offer what I consider the holy grail of tax advantages: triple tax benefits. Your contributions are tax-deductible, the growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. No other account offers this trifecta!

For 2024, you can contribute up to $4,150 for individual coverage or $8,300 for family coverage, plus an extra $1,000 if you’re 55 or older.

Jennifer, a CFO client, uses a brilliant strategy with her HSA:

“I pay all my current medical expenses out-of-pocket and save the receipts. Meanwhile, I invest my HSA funds for long-term growth. Years from now, I can reimburse myself for those old expenses with no time limit, essentially creating a tax-free investment account.”

To qualify for an HSA, you need a high-deductible health plan with a deductible of at least $1,600 for individual coverage or $3,200 for family coverage in 2024.

If HSAs aren’t an option—or you want additional tax savings—consider a Healthcare FSA, which allows you to set aside up to $3,200 pre-tax in 2024. Unlike HSAs, FSAs typically have a “use it or lose it” rule, though some plans offer a grace period or small carryover amount.

For families with young children or dependent adults, a Dependent Care FSA lets you set aside up to $5,000 pre-tax for qualifying care expenses. One couple I work with, James and Maria, combines all these accounts to reduce their taxable income by $16,500 annually just through healthcare and dependent care strategies!

More info about Extra Medicare Tax for High Earners

Layer on Nonqualified Deferred Compensation

For executives and highly compensated employees, Nonqualified Deferred Compensation (NQDC) plans can be a game-changer. These employer-sponsored plans let you postpone receiving a portion of your income until a future date—often when you’ll be in a lower tax bracket.

Unlike 401(k)s, NQDC plans aren’t subject to the same contribution limits. Some plans allow you to defer 50% or more of your base salary and up to 100% of bonuses.

Robert, a pharmaceutical executive earning $450,000 annually, uses his company’s NQDC plan strategically:

“I’m currently in the 37% federal bracket, but I’m moving to Florida in five years when I retire. By deferring $100,000 of my compensation now, I’ll pay taxes when I’m in a much lower bracket—and avoid state income tax entirely.”

There are some important considerations with NQDC plans. You must specify your distribution timing upfront, and the deferred money remains an asset of your company (meaning it could be at risk if the company faces financial difficulties). Election deadlines are also strict—typically December 31 for the following year’s compensation.

For many of my executive clients, combining NQDC deferrals with maxed-out qualified retirement plans results in six-figure tax deferrals annually.

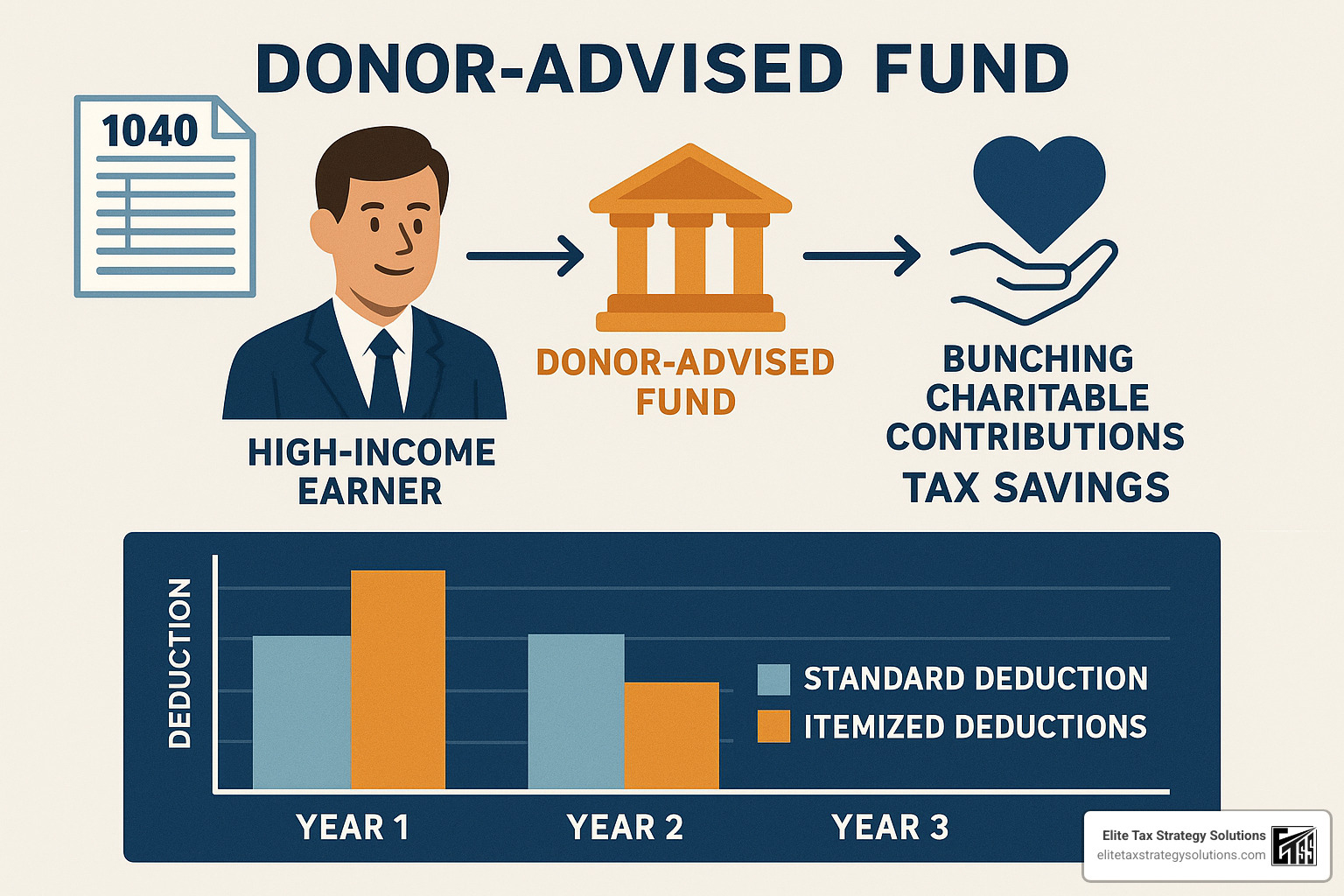

Boost Charitable Impact with Donor-Advised Funds

If you’re charitably inclined, strategic giving can significantly reduce your tax burden while supporting causes you care about. A Donor-Advised Fund (DAF) is one of my favorite tools for this purpose.

A DAF allows you to make a charitable contribution, receive an immediate tax deduction, and then recommend grants to your favorite charities over time. This separation creates powerful planning opportunities, especially through “bunching”—concentrating multiple years of giving into a single tax year.

My client Catherine’s experience illustrates this perfectly:

“I typically donate about $15,000 annually to various charities. With the standard deduction for married couples at $27,700 in 2023, my charitable contributions alone weren’t enough to make itemizing worthwhile. My advisor suggested I bunch three years of donations ($45,000) into my DAF in a single year. Combined with my state and local taxes and mortgage interest, this pushed me well above the standard deduction threshold, saving me over $12,000 in taxes that year. I then took the standard deduction for the next two years while continuing to support my charities from my DAF.”

DAFs offer additional benefits too. You can donate appreciated securities to avoid capital gains tax while still receiving a deduction for the full market value. Your record-keeping simplifies dramatically—just one receipt instead of many. And if privacy matters to you, DAFs can allow anonymous giving.

For high-income earners, charitable contributions can be deducted up to 60% of your adjusted gross income for cash donations and 30% for appreciated securities, with five-year carryforward for excess amounts.

Investment & Real-Estate Tactics to Reduce Ongoing Tax Drag

When you’re earning a high W-2 income, it’s not just about what you save in retirement accounts or give to charity. The way you structure your everyday investments can make a tremendous difference in your after-tax returns. Let’s explore how to minimize that pesky “tax drag” that silently eats away at your investment growth year after year.

Tax-Efficient Asset Location

Think of your investment accounts as different types of containers—each with its own tax rules. Asset location is the art of putting each investment in its optimal tax container.

I remember working with Alex, a marketing executive earning $300,000 annually, who had a well-diversified portfolio but had never considered which investments belonged where. After restructuring his holdings, he was amazed by the results.

“I moved all my bond funds and REITs into my IRA, and kept my low-turnover index ETFs in my taxable account,” Alex told me. “My advisor estimates this saves me about $3,500 annually in taxes without changing my overall asset allocation.”

For your taxable accounts, prioritize investments that naturally minimize tax impact: tax-efficient ETFs that rarely distribute capital gains, municipal bonds generating tax-exempt interest, and stocks you plan to hold long-term to benefit from lower capital gains rates when you eventually sell.

In your tax-advantaged accounts like 401(k)s and IRAs, house the investments that would otherwise create the biggest tax headaches: taxable bonds, REITs with their high dividend distributions, actively managed funds with frequent trading, and anything else generating significant ordinary income.

When it’s time to rebalance your portfolio, try to do so within your tax-advantaged accounts whenever possible. This prevents triggering taxable events that can erode your returns.

Year-Round Tax-Loss Harvesting

Tax-loss harvesting isn’t just a December activity—it’s a year-round opportunity to turn market dips into tax advantages.

Michael, a physician in our practice earning $450,000 annually, made this a regular part of his investment strategy. During the market volatility of 2022, we identified over $80,000 in losses we could harvest from his portfolio.

“We immediately reinvested in similar but not identical funds to maintain my market exposure,” Michael explained. “Those losses offset $80,000 in capital gains from some company stock I sold, saving me over $19,000 in taxes.”

The beauty of tax-loss harvesting is its flexibility. You can use these losses to:

- Offset capital gains from other investments

- Reduce your ordinary income by up to $3,000 per year

- Carry forward excess losses to future tax years

- Reset your cost basis while maintaining similar market exposure

Just be careful to avoid the “wash sale rule” by not repurchasing the same or “substantially identical” security within 30 days before or after selling at a loss. And always ensure that any transaction costs don’t outweigh the tax benefits you’re seeking.

For high-income earners facing the 23.8% long-term capital gains rate (20% plus the 3.8% Net Investment Income Tax), effective tax-loss harvesting can lead to significant tax savings that compound over time.

Using Real Estate for Paper Losses & Cash Flow

Real estate might be the most tax-advantaged investment vehicle available to high-income W-2 earners. Through the magic of depreciation and other real estate tax provisions, you can generate “paper losses” that offset your ordinary income while potentially enjoying positive cash flow from the properties.

Jennifer, an executive client earning $350,000 annually, purchased a $500,000 rental property and used a cost segregation study to identify $150,000 of components eligible for accelerated depreciation.

“In the first year, I generated over $70,000 in paper losses while the property was actually cash-flow positive,” she shared with a smile. “These losses offset a portion of my W-2 income, saving me nearly $26,000 in taxes that year alone.”

The key tax advantages of real estate include:

Depreciation allows you to deduct the cost of residential rental property over 27.5 years, creating a non-cash deduction that shelters rental income. It’s like getting a tax deduction for something that might actually be appreciating in value!

Cost segregation takes depreciation to the next level by identifying components of your property that can be depreciated over shorter periods—5, 7, or 15 years instead of 27.5. This engineering-based approach accelerates your deductions significantly.

Bonus depreciation under current tax law allows for 80% bonus depreciation in 2023 (reducing to 60% in 2024) on certain qualifying property improvements, creating substantial upfront deductions.

Short-term rental strategy can be particularly powerful. Properties rented for an average of 7 days or less are considered businesses rather than rental properties, potentially allowing you to avoid passive activity loss limitations that normally apply to rental real estate.

For W-2 earners with income above $150,000, rental real estate losses are typically limited by passive activity loss rules. However, you might qualify for exceptions:

If you or your spouse qualify as a Real Estate Professional (750+ hours and more than half your working time in real estate activities), you can deduct unlimited real estate losses against your ordinary income.

With active participation and moderate income (modified AGI below $150,000), you can deduct up to $25,000 of rental losses against ordinary income.

Even without these exceptions, suspended passive losses don’t disappear—they can offset future rental income or be fully deducted when you sell the property.

By combining these tax strategies for high-income w2 earners with proper asset location and tax-loss harvesting, you create a powerful system that minimizes tax drag across your entire investment portfolio, potentially saving tens of thousands in taxes annually while building wealth more efficiently.

Navigating Equity Compensation & Bonus Income

Many high-income W-2 earners find that equity awards and bonuses make up a substantial portion of their total compensation. While these can significantly boost your wealth, they also create unique tax challenges that require thoughtful planning and precise timing.

Managing RSU & ESPP Tax Bills

When it comes to equity compensation, Restricted Stock Units (RSUs) and Employee Stock Purchase Plans (ESPPs) each come with their own tax implications that can catch even financially savvy professionals off guard.

Restricted Stock Units (RSUs)

RSUs are taxed as ordinary income at the moment they vest—whether you sell the shares or not. This creates an immediate tax liability that many executives aren’t fully prepared for.

One of the biggest surprises for my clients is the withholding gap. Most companies automatically withhold taxes on RSUs at just 22% federally (or 37% for amounts over $1 million). If you’re in the highest tax bracket, that’s significantly less than your actual tax rate.

James, a tech executive client, learned this lesson the expensive way: “When my RSUs vested, the company only withheld 22%, but I was in the 37% bracket. I ended up owing an additional $45,000 at tax time and faced an underpayment penalty. Now I either sell enough shares immediately to cover the full tax bill or set aside cash in advance.”

Many of my clients now use what’s called a sell-to-cover strategy, where they immediately sell just enough shares at vesting to cover their full estimated tax liability—not just the amount automatically withheld. This prevents nasty surprises at tax time.

There’s also the issue of concentrated position risk. When RSUs make up a significant portion of your compensation, you can quickly end up with a dangerously large percentage of your wealth tied to a single company—the same company that provides your salary. This creates a double risk that’s worth addressing through thoughtful diversification.

Employee Stock Purchase Plans (ESPPs)

ESPPs can be a fantastic benefit, typically allowing you to purchase company stock at a discount of up to 15%. However, the tax treatment depends on how long you hold the shares:

With a qualifying disposition—holding shares for at least 1 year from purchase and 2 years from the offering date—only the discount is taxed as ordinary income, with additional appreciation taxed at the more favorable long-term capital gains rates.

With a disqualifying disposition—selling before meeting those holding requirements—both the discount and any additional bargain element get taxed as ordinary income.

I’ve noticed an interesting trend among my more risk-averse clients: many choose to sell ESPP shares immediately after purchase, accepting the ordinary income tax treatment in exchange for locking in that guaranteed discount while avoiding market risk. As one client put it, “A bird in the hand is worth two in the bush—especially when the bush could catch fire at any moment!”

ISO Exercise Timing & AMT

Incentive Stock Options (ISOs) offer potentially significant tax advantages, but they’re also where I see the most expensive tax mistakes made by high-earning professionals.

The fundamental challenge with ISOs is balancing regular tax benefits against Alternative Minimum Tax (AMT) exposure:

From a regular tax perspective, no tax is due when you exercise ISOs (unlike non-qualified stock options). Better yet, if you hold the shares for at least 1 year from exercise and 2 years from grant, your entire gain receives favorable long-term capital gains treatment when you sell.

But here’s the trap: while no regular tax applies at exercise, the bargain element—the difference between your exercise price and the stock’s fair market value—counts as an AMT adjustment. This can unexpectedly trigger substantial AMT liability, sometimes running into tens or even hundreds of thousands of dollars.

The silver lining is that any AMT paid due to ISO exercises generates an AMT credit that you can use in future years when your regular tax exceeds your AMT. However, it may take many years to fully recover this credit.

Over the years, I’ve developed several approaches to help clients manage ISO tax exposure:

Exercise timing is crucial. I often recommend exercising ISOs early in the calendar year, which gives you several months to evaluate the potential AMT impact before year-end. If the AMT hit looks too severe, you can sell the shares before December 31 (a “disqualifying disposition”) to avoid AMT.

Spreading exercises across tax years can significantly reduce your overall tax burden compared to exercising all options at once. This strategy helps minimize your exposure to AMT in any single year.

Sarah, a VP at a software company, came to me planning to exercise $200,000 worth of ISOs all at once. After analyzing her situation, I showed her that this would trigger over $50,000 in AMT. “Instead,” Sarah told me later, “we spread the exercises over three years and timed them with my planned parental leave when my income would be temporarily lower. This reduced my AMT exposure by more than 60%.”

For executives with substantial equity compensation, integrating these tax strategies for high-income w2 earners with your overall financial plan isn’t just nice-to-have—it’s essential for protecting and optimizing your after-tax wealth.

Section 83(i) elections can also provide tax deferral opportunities for qualifying private company equity, while state sourcing rules for equity compensation and bonuses can create planning opportunities for those who relocate during the vesting period.

With equity compensation, timing isn’t just about market conditions—it’s about tax conditions too.

State Residency, Upcoming Law Changes & Coordination with Family

For high-income W-2 earners, state income taxes can take a surprisingly large bite out of your paycheck. In fact, when I work with clients who’ve recently relocated from high-tax states like California or New York to no-tax states like Florida or Texas, they’re often amazed at how much their take-home pay increases. But changing residency isn’t as simple as buying a vacation home, and with major tax law changes on the horizon, strategic planning has never been more important.

Changing Domicile the Right Way

“The day I officially became a Florida resident was like getting a 13% raise,” Michael, a tech executive who relocated from California, told me with a laugh. But his journey wasn’t just about packing boxes and heading east.

States with no income tax can offer significant savings for high earners. These tax-friendly havens include:

Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming.

However, your former state won’t let you go without a fight – especially if you’re a high earner. States distinguish between “domicile” (your permanent home) and “residency” (where you might temporarily live), and high-tax states are notorious for aggressively auditing former residents.

The 183-day rule (spending more than half the year in your new state) is just the beginning. To successfully establish a new domicile, you need to create what I call a “preponderance of evidence” that your life is truly centered in your new state.

Robert, a finance executive who moved from California to Nevada, learned this the hard way: “California’s Franchise Tax Board came after me two years after I moved. Thankfully, we had created a comprehensive relocation plan that documented everything from my gym membership to my dentist appointments in Nevada. When they requested proof, I had a three-inch binder ready to go.”

For a successful domicile change, focus on these key areas:

Physical presence – Track your days carefully using a location diary, travel records, and receipts. The burden of proof is on you.

Meaningful connections – Establish real ties in your new state: join clubs, attend local events, build relationships with neighbors, and engage in community activities.

Official documentation – Change your driver’s license, voter registration, car registration, and insurance policies. Update your address on all financial accounts, estate documents, and with the IRS.

Home sweet home – Your new residence should be comparable or larger than your previous home. If you keep property in your former state, consider renting rather than maintaining a second home.

For those who work across multiple states but can’t completely relocate, understanding state-specific sourcing rules becomes crucial. Some states have reciprocity agreements that simplify tax filing for cross-border workers, while others will tax every dollar earned while physically working in their state.

Planning for the TCJA Sunset & Estate Exemption Drop

The clock is ticking on the Tax Cuts and Jobs Act (TCJA). When key provisions expire after 2025, high-income earners will face a very different tax landscape:

The top federal income tax rate will jump from 37% to 39.6%. The standard deduction will approximately be cut in half. Personal exemptions will return after being eliminated. The $10,000 SALT (state and local tax) cap may increase or disappear entirely. And perhaps most significantly for wealthy families, the lifetime estate and gift tax exemption will drop from the current $13.61 million per person to approximately half that amount.

“This sunset creates both urgency and opportunity,” explains Jennifer, who began working with us after inheriting significant family assets. “We’re implementing a strategic giving plan now, while the exemption is at historic highs.”

For forward-thinking taxpayers, here are the most valuable pre-sunset strategies:

Consider income acceleration in 2024-2025 rather than deferring to 2026 when rates will likely be higher. This might mean exercising stock options, recognizing capital gains, or converting traditional IRAs to Roth IRAs.

Time your deductions strategically by postponing major deductible expenses until 2026 when they may provide greater tax benefit due to higher rates.

Gift now while the exemption is high. This doesn’t mean you need to give assets directly to heirs – you can use irrevocable trusts that provide continued access and control while removing assets from your taxable estate.

529 plan superfunding allows you to front-load up to five years of gift tax exclusions into a college savings plan in a single year – that’s $85,000 per beneficiary in 2024, or $170,000 for married couples, without using any lifetime exemption.

A recent planning opportunity worth noting is the ability to roll over up to $35,000 from a 529 plan to a Roth IRA for the beneficiary, subject to certain conditions. This provides welcome flexibility if education funds aren’t fully used.

For families with significant wealth, advanced estate planning techniques like Grantor Retained Annuity Trusts (GRATs) and Spousal Lifetime Access Trusts (SLATs) can provide additional opportunities to lock in the current higher exemption amounts while maintaining some access to those assets.

Sarah and David, business executives with a combined estate of $22 million, implemented what I call a “spouse strategy”: “We each created SLATs for the benefit of the other spouse and our children. This removed $12 million from our estate while giving us indirect access to those funds if needed. With the exemption scheduled to drop in 2026, acting now saved our family potentially millions in future estate taxes.”

The bottom line? For high-income earners, proactive planning before the TCJA sunset can yield significant tax savings for both you and future generations.

More info about High-Income Tax Planning

Common Mistakes & When to Hire a Pro

Even the most financially savvy high-income earners can fall into tax traps that cost thousands of dollars. After helping hundreds of clients steer these waters, I’ve seen how understanding common pitfalls and knowing when to bring in experts can make all the difference in your financial life.

Red Flags to Avoid

That sinking feeling when you realize you’ve made a costly tax mistake is something I help clients avoid every day. Jessica, a technology executive making $380,000 annually, came to me after receiving an unexpected IRS notice about her backdoor Roth conversions. “I had no idea I needed to file Form 8606 each year to track my non-deductible contributions,” she told me. Without this documentation, the IRS was treating her Roth withdrawals as fully taxable—essentially double-taxing her money.

This is just one of the common mistakes I see regularly. Missing Roth basis tracking can lead to paying tax twice on the same money. Underpayment penalties hit high earners particularly hard, especially those with significant bonuses or equity compensation that push them into higher brackets than their regular withholding covers. You generally need to pay at least 90% of your current year tax or 100% of your prior year tax (110% if your AGI exceeded $150,000) to avoid these penalties.

Wash sale violations happen when well-intentioned investors repurchase substantially identical securities within 30 days before or after selling at a loss, inadvertently disallowing valuable tax deductions. Mark, a physician client, learned this lesson when his automated investment platform purchased shares of an ETF just 18 days after he sold the same fund at a loss in his brokerage account. The $12,000 tax loss he was counting on was disallowed.

Excess retirement contributions trigger a 6% penalty that continues each year until corrected. This commonly happens when high earners don’t realize their income has phased them out of certain contribution options, or when they change jobs and lose track of total contributions across multiple employer plans.

Perhaps most frustrating are the late elections and missed deadlines that simply can’t be fixed retroactively. As Gio, a CPA specializing in high-income clients, often tells me: “The most common mistakes I see are failing to file Roth conversion forms correctly, not claiming startup losses within the three-year statute of limitations, and incorrect basis reporting for RSUs resulting in paying excess tax.”

The remedy? Implement a year-round tax strategies for high-income w2 earners approach rather than the typical “tax season scramble.” Your financial life deserves more than just an annual check-in.

Building Your Dream Team

“I wish I’d hired a professional sooner,” is something I hear constantly from new clients. Often they’ve been doing their own taxes for years, using consumer software that’s simply not designed for complex situations. The turning point usually comes when they realize how much money they’re leaving on the table.

For high-income W-2 earners, certain situations almost always justify professional help. Consider bringing in experts if:

Your income exceeds $300,000. At this level, the potential tax savings from professional planning typically far outweigh the cost. Michael, a sales executive, invested $3,500 in comprehensive tax planning that ultimately saved him over $22,000 in his first year working with us.

You have equity compensation. The tax implications of RSUs, stock options, and ESPPs create layers of complexity that benefit from specialized knowledge. One missed election or poorly timed exercise can cost tens of thousands in unnecessary taxes.

You’re approaching retirement. The 5-10 years before retirement represent a critical window for tax planning. Optimizing the tax efficiency of your retirement income and setting up Roth conversion strategies requires careful multi-year planning that most self-directed investors miss.

You’ve experienced a major life change. Marriage, divorce, relocation to a new state, or significant income increases all warrant professional tax review. These transitions create both pitfalls and planning opportunities that are easy to overlook.

You own multiple properties or have complex investments. Real estate strategies and investment tax optimization benefit from expert guidance that goes well beyond what tax software can provide.

Your ideal tax team might include a CPA or Enrolled Agent for tax compliance and planning, a Financial Advisor with tax expertise for investment and retirement planning, an Estate Planning Attorney for wealth transfer strategies, and possibly an Insurance Specialist for certain tax-advantaged protection strategies.

When selecting tax professionals, look for experience with clients in similar financial situations, proactive communication throughout the year (not just at tax time), appropriate credentials, willingness to collaborate with your other advisors, and transparent fee structures.

“The difference between a tax preparer and a true tax strategist is that one documents history while the other helps you write it,” as I often tell prospective clients. At Elite Tax Strategy Solutions, we focus on building long-term relationships with our clients, providing proactive tax strategies for high-income w2 earners rather than just reactive tax preparation.

The right professional relationship shouldn’t feel transactional—it should feel like a partnership in your financial success. When you find that, the value extends far beyond just reducing your tax bill.

High-Income Tax Reduction Strategies

Frequently Asked Questions about Tax Strategies for High-Income W-2 Earners

What tax credits can high earners still claim?

When my clients first come to me, they often assume they’ve “phased out” of all tax credits. The good news? There are still several valuable credits available even at higher income levels.

The reformed Electric Vehicle Credit is a favorite among my environmentally-conscious clients. You can receive up to $7,500 for new electric vehicles and up to $4,000 for used EVs. Just be aware of the income limits: $300,000 for married couples ($150,000 for singles) for new vehicles, and $150,000 for couples ($75,000 for singles) for used vehicles.

Making your home more energy-efficient can also pad your wallet. The Energy Efficiency Home Improvement Credit covers 30% of qualified improvements to your primary residence. My client Rebecca recently installed new energy-efficient windows and received a $1,200 credit against her tax bill.

For those ready to make a bigger commitment to renewable energy, the Residential Clean Energy Credit offers a generous 30% credit for solar panels, wind, geothermal systems, and more—with no dollar limit. One executive I work with installed a $30,000 solar system and received a $9,000 tax credit, significantly offsetting his installation costs.

Don’t forget about business credits if you have self-employment income alongside your W-2 earnings. I always remind my clients with side businesses to carefully document mixed-use assets like vehicles. Proper documentation of business use can transform personal expenses into valuable tax deductions.

How does the 3.8% Net Investment Income Tax apply?

The Net Investment Income Tax (NIIT) often comes as an unwelcome surprise to my clients crossing certain income thresholds. This 3.8% tax applies to investment income when your modified adjusted gross income exceeds $200,000 for singles or $250,000 for married couples filing jointly.

What counts as investment income for NIIT purposes? Interest, dividends, capital gains, rental income, royalties, non-qualified annuities, income from passive activities, and income from trading financial instruments all fall under this umbrella.

“I had no idea this tax existed until I sold some long-held stock to fund a home renovation,” shared Michael, a software engineer who came to me after receiving an unexpectedly large tax bill. “It was an expensive lesson in tax planning.”

To help clients like Michael minimize their NIIT exposure, I recommend several strategies:

Municipal bonds can be your friend here, as the interest they generate is exempt from both regular federal income tax and NIIT. For many of my clients in high-tax states, the tax-equivalent yield makes these an attractive option despite their generally lower stated yields.

Tax-loss harvesting remains one of the most powerful tools in our arsenal. By strategically offsetting capital gains with capital losses, we can reduce the net investment income subject to this additional tax.

Many clients find success with retirement account contributions. Not only do these pre-tax contributions build your retirement nest egg, but they can also reduce your MAGI enough to stay below the NIIT threshold in some cases.

When possible, timing income recognition across multiple tax years can prevent large spikes that trigger additional taxes. I worked with a client planning to sell her rental property and helped her structure an installment sale that spread the gain over three years, significantly reducing her overall NIIT burden.

For philanthropically-minded clients, charitable giving of appreciated assets accomplishes two goals: avoiding capital gains tax and reducing income potentially subject to NIIT.

Should married high earners ever file separately?

Most tax professionals will tell you that married filing jointly is almost always the better option. But in my practice, I’ve found several situations where filing separately actually benefits high-income couples.

SALT deduction optimization is a big one since the Tax Cuts and Jobs Act capped state and local tax deductions at $10,000. If one spouse has significantly higher state and local taxes, filing separately might allow that spouse to use more of their individual $10,000 SALT cap.

I’ve seen dramatic savings for couples where one spouse has significant federal student loans on an income-driven repayment plan. By filing separately, the loan payments are calculated based only on that spouse’s income, potentially saving thousands in annual payments.

For couples with substantial medical expenses, filing separately might help the spouse with high medical costs exceed the 7.5% of AGI threshold needed to claim these deductions. This strategy worked particularly well for a surgeon client whose spouse had chronic health conditions requiring expensive treatments not fully covered by insurance.

Some clients also value the liability protection that comes with separate filing. As one client put it, “I love my spouse, but I don’t love their approach to tax reporting.”

Before rushing to file separately, however, I always make sure clients understand the downsides:

– Higher tax rates apply at lower income thresholds

– Many valuable credits and deductions are reduced or eliminated

– Both spouses must either take the standard deduction or both must itemize

One of my clients, Taylor, a marketing executive married to a medical resident with substantial student loans, saved over $9,000 annually in loan payments by filing separately. “The tax hit was about $1,800 more filing separately, but we saved $9,000 in student loan payments. That’s a trade-off I’ll take every time.”

For most high-income married couples, filing jointly remains the more advantageous option, but it’s always worth running the numbers both ways when these specific situations apply.

Conclusion

Navigating tax strategies for high-income w2 earners is a bit like conducting an orchestra – it takes coordination, timing, and expertise to make all the instruments work in harmony. As we’ve explored throughout this guide, reducing your tax burden isn’t about a single magic solution but rather implementing multiple strategies that work together and evolve with your life circumstances.

The difference between paying the legal minimum in taxes versus what most high earners actually pay can be staggering – often tens or even hundreds of thousands of dollars annually. That’s money that could be funding your children’s education, accelerating your path to financial independence, or supporting causes you care deeply about.

I’ve seen how transformative proper tax planning can be. One client, a surgeon earning $750,000 annually, implemented just four of the strategies we discussed – maxing out his retirement accounts, utilizing a backdoor Roth, implementing a donor-advised fund strategy, and restructuring his investment portfolio for tax efficiency. The result? His federal tax bill decreased by over $42,000 in the first year alone.

Effective tax planning isn’t a once-a-year scramble before April 15th. The most successful approach involves ongoing attention throughout the year and regular adjustments as your income, family situation, and the tax laws themselves change. With major shifts on the horizon when the TCJA provisions sunset in 2025, staying proactive will be more important than ever.

Your takeaway should be simple: start implementing these strategies now. You’ve worked incredibly hard to earn your income – you deserve to keep as much of it as legally possible. Whether you begin with maximizing your 401(k) contributions, exploring backdoor Roth options, or implementing tax-loss harvesting in your investment accounts, taking action today can significantly impact your financial future.

At Elite Tax Strategy Solutions, we’re passionate about helping professionals like you develop comprehensive, personalized tax strategies that align with your broader financial goals. Our team combines technical expertise with genuine care for our clients’ well-being – we’re not just looking to save you money on taxes (though we’re very good at that!), but to help you use those savings to build the life you want.

As one of our long-time clients recently told us, “I used to dread tax season and writing those big checks to the IRS. Now I look forward to my annual tax planning meeting because I know we’re going to find new ways to legally reduce my tax burden and put more money toward my family’s future.”

Ready to take control of your tax situation? We’d love to help you identify the strategies that will have the biggest impact for your specific circumstances. The peace of mind that comes from knowing you’re not overpaying your taxes is invaluable – and it starts with a conversation.