Tax strategies for high income individuals are crucial to managing the hefty burden they face every tax season. High-income earners often see a significant portion of their hard-earned money going towards taxes, which can be disheartening. To mitigate this, here are a few starting strategies:

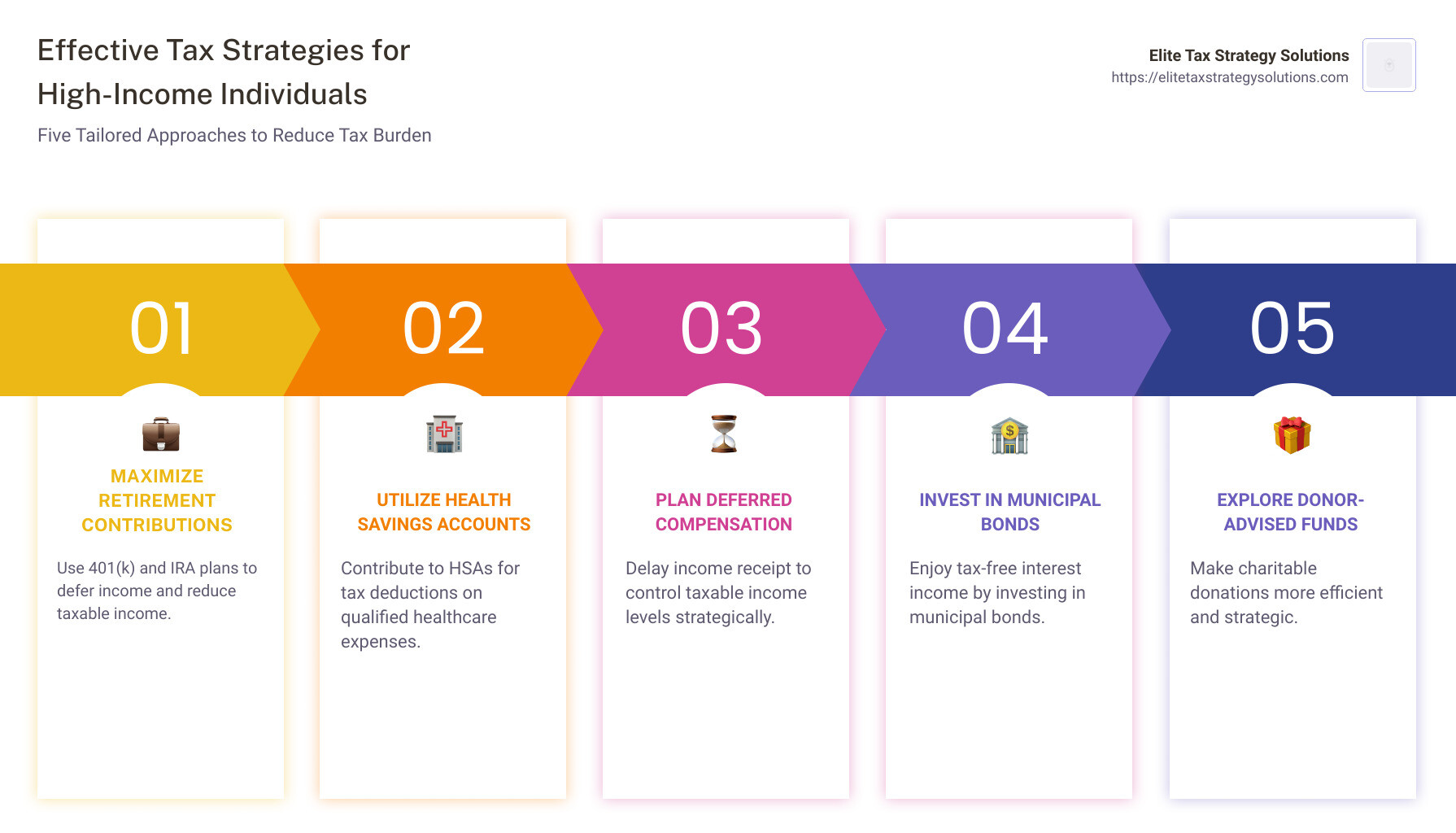

- Maximize Retirement Contributions: Using 401(k) and IRA plans to defer income and reduce taxes.

- Health Savings Accounts (HSAs): Contribute to HSAs for tax deductions on healthcare expenses.

- Deferred Compensation Plans: Delay income receipt to manage taxable income levels.

- Municipal Bonds: Invest in these to enjoy tax-free interest income.

Each of these strategies can help you keep more of your money without needing to dig into every detail.

For a deeper understanding of these techniques and more, this article dives into the various methods that can help high-income earners ease their tax burdens while working toward long-term financial well-being.

As David Fritch, I bring decades of experience in developing tax strategies for high income individuals. My expertise aims to ensure that these strategies are efficient and comprehensive, helping clients steer complex tax codes seamlessly.

Tax strategies for high income individuals vocab to learn:

– high income tax reduction strategies

– financial planning for high income earners

– tax advice for high earners

Understanding High-Income Taxation

When it comes to taxes, being a high-income earner means navigating a complex landscape. So, let’s break it down in simple terms.

IRS Definition

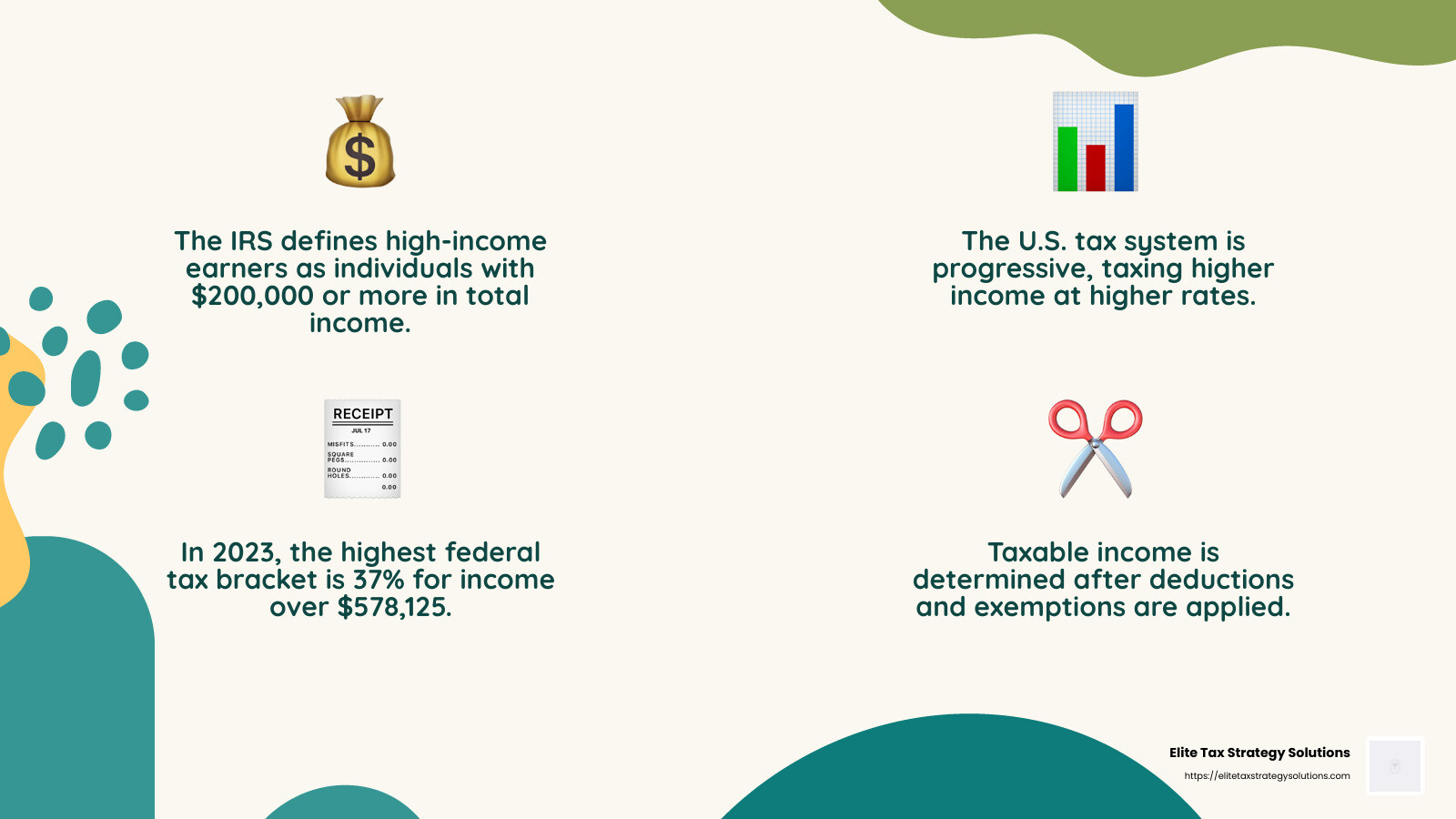

The IRS considers anyone with a total income of $200,000 or more as a high-income earner. This isn’t just your salary; it includes bonuses, dividends, rental income, and more. The total income is the sum of all your earnings from various sources.

Tax Brackets

In the U.S., the tax system is progressive. This means the more you earn, the higher the percentage of your income you pay in taxes. For high-income individuals, this can mean falling into one of the top tax brackets.

For instance, in 2023, the highest federal tax bracket is 37%. This applies to any income over $578,125 for single filers. So, if you earn more than this, every dollar above that threshold is taxed at 37%.

Taxable Income

Taxable income is what remains after subtracting deductions and exemptions from your total income. This is the number that determines your tax bracket.

For example, if you earn $250,000 but manage to deduct $50,000 through various strategies, you’ll only be taxed on $200,000. This is why maximizing deductions and credits is so important.

Understanding these basics helps in crafting effective tax strategies for high income individuals. By knowing how your income is taxed, you can make informed decisions to reduce your tax burden.

Next, we’ll explore specific strategies that can help you do just that, including retirement contributions and Roth IRA conversions.

Tax Strategies for High-Income Individuals

Being a high-income earner comes with its own set of challenges, especially when it comes to taxes. Let’s explore some tax strategies for high-income individuals that can help you keep more of what you earn.

Retirement Contributions

One of the simplest ways to reduce your taxable income is by maximizing contributions to retirement accounts.

-

Traditional 401(k): Contributing up to $23,000 in 2024 (or $30,500 if you’re over 50) can significantly lower your taxable income. For example, if you earn $250,000 and contribute $20,000, you’ll only be taxed on $230,000.

-

Traditional IRA: You can contribute up to $7,000 (or $8,000 if over 50). This also helps in reducing the income that is subject to taxes.

Roth IRA Conversions

High-income earners often can’t directly contribute to a Roth IRA due to income limits. However, there’s a workaround known as a Roth IRA conversion.

You can contribute to a Traditional IRA and then convert it to a Roth IRA. This allows your investments to grow tax-free. Timing is crucial, so consult with a tax advisor to make sure this strategy aligns with your financial goals.

Municipal Bonds

Investing in municipal bonds can be a smart move for high-income individuals. These bonds, issued by local and state governments, often offer interest that is exempt from federal income taxes. Depending on where you live, they might also be exempt from state and local taxes.

This can be a valuable part of your tax plan, especially if you are in a high tax bracket.

Donor-Advised Funds

If you’re charitably inclined, consider setting up a donor-advised fund. You can contribute to this fund and claim the full tax deduction in the year you make the contribution. Then, you have the flexibility to decide when and where to distribute the funds to charities over time.

This strategy is particularly beneficial in years when you have higher-than-normal income, such as receiving a bonus or inheritance.

Health Savings Accounts

For those with high-deductible health insurance plans, a Health Savings Account (HSA) offers a triple tax advantage. Contributions are tax-deductible, the growth is tax-free, and withdrawals for qualified medical expenses are also tax-free.

In 2024, you can contribute up to $4,150 for individuals and $8,300 for families, with an additional $1,000 catch-up contribution if you’re 55 or older.

By leveraging these strategies, high-income earners can effectively reduce their tax burden and improve their financial well-being. Next, we’ll dive into maximizing deductions and credits to further optimize your tax situation.

Maximizing Deductions and Credits

High-income earners have unique opportunities to reduce their tax liability through smart use of deductions and credits. Let’s explore some effective strategies.

Itemized Deductions

For many high earners, itemizing deductions can lead to significant tax savings. This involves listing specific expenses like mortgage interest, medical expenses, and state and local taxes instead of taking the standard deduction. However, the state and local tax (SALT) deduction is capped at $10,000, so planning is crucial.

-

Mortgage Interest: If you own a home, you can deduct interest on up to $750,000 of mortgage debt. This can provide a substantial tax break, especially in the early years of a mortgage when interest payments are higher.

-

Medical Expenses: You can deduct medical expenses that exceed 7.5% of your adjusted gross income (AGI). This can include everything from doctor visits to prescription medications, but keep meticulous records.

Charitable Contributions

Charitable giving is not only good for the community but also for your tax bill. You can deduct donations of cash, stocks, or other assets to qualified charities. Consider these strategies:

-

Donor-Advised Funds: As mentioned earlier, these funds allow you to make a large donation and get the tax deduction upfront, while distributing the funds to charities over time. This is perfect for years when your income spikes.

-

Bunching Contributions: If your charitable donations typically fall short of the standard deduction, consider bunching several years’ worth of donations into one year to maximize your tax benefit.

Business Write-Offs

If you have a side business or earn 1099 income, you can take advantage of numerous business write-offs. These deductions help offset business expenses and reduce taxable income.

-

Home Office: Deduct a portion of your home expenses if you have a dedicated space for business activities.

-

Business Travel and Meals: Deduct travel expenses and meals related to business, but ensure you keep detailed records and receipts.

-

Vehicle Expenses: Deduct costs for using a personal vehicle for business purposes, either by tracking actual expenses or using the IRS’s standard mileage rate.

Real Estate Losses

Real estate can be a powerful tool for reducing taxes through paper losses like depreciation. Even if your property generates positive cash flow, depreciation can create a tax loss.

- Depreciation Deductions: This non-cash deduction accounts for the decrease in property value over time. It can significantly reduce your taxable income on paper, even if the property’s market value is increasing.

By strategically using these deductions and credits, high-income individuals can effectively lower their taxable income and keep more of their hard-earned money. Next, we’ll explore investment strategies for tax efficiency.

Investment Strategies for Tax Efficiency

Investing wisely is key for high-income earners who want to minimize their tax burden. Let’s explore some tax strategies for high-income individuals that focus on investment options.

Long-term Capital Gains

One of the most effective strategies is to aim for long-term capital gains. Long-term capital gains are taxed at a lower rate compared to short-term gains, which are taxed as regular income. By holding investments like stocks or real estate for more than a year, you can benefit from these favorable rates.

- Example: If you sell a stock after holding it for over a year, you might pay only 15% in taxes on the profit, versus up to 37% for short-term gains.

Tax-Exempt Bonds

Investing in tax-exempt bonds, such as municipal bonds, can offer a steady income stream without the burden of federal taxes. These bonds are particularly beneficial for high-income earners living in states with high tax rates, as they often provide state and local tax exemptions as well.

- Tip: Look for bonds issued in your state to maximize tax savings.

Dividend-Paying Companies

Investing in companies that pay qualified dividends can also be a tax-efficient strategy. Qualified dividends are taxed at the same lower rates as long-term capital gains, providing a tax advantage over ordinary income.

- Strategy: Focus on companies with a history of stable and growing dividends. This can provide both income and tax benefits over time.

Opportunity Zones

Opportunity Zones are designated areas that offer tax incentives to encourage investment. By investing in these zones, you can defer taxes on prior capital gains and potentially reduce future tax liabilities.

- Benefit: If you hold your investment in an Opportunity Zone for at least ten years, any additional gains on that investment can be tax-free. This can be a powerful tool for long-term tax planning.

Here’s a quick recap of these strategies:

| Investment Type | Tax Benefit |

|---|---|

| Long-term Capital Gains | Lower tax rates compared to short-term gains |

| Tax-Exempt Bonds | Federal and often state/local tax exemptions |

| Dividend-Paying Companies | Lower tax rates on qualified dividends |

| Opportunity Zones | Tax deferral and potential tax-free growth |

By incorporating these investment strategies for tax efficiency, high-income individuals can optimize their portfolios for both growth and tax savings. Next, we’ll address some frequently asked questions about tax strategies.

Frequently Asked Questions about Tax Strategies

Navigating taxes can be tricky, especially for high-income earners. Here, we’ve gathered some common questions and answers to help you understand tax strategies for high-income individuals.

How to reduce taxes for high-income earners?

-

Retirement Plan Contributions: Maximize your contributions to retirement accounts like Traditional 401(k)s and IRAs. These contributions reduce your taxable income, lowering your tax bill. For instance, in 2024, you can contribute up to $23,000 to a Traditional 401(k) if you’re under 50, or $30,500 if you’re over 50.

-

Strategic Asset Sales: Timing is everything. Sell assets strategically to take advantage of lower tax rates on long-term capital gains. If you have a year with lower income, consider realizing gains to “fill up” your tax bracket without pushing yourself into a higher one.

What are the biggest tax loopholes?

-

Backdoor Roth IRAs: High-income earners often can’t contribute directly to a Roth IRA due to income limits. However, you can use a backdoor Roth IRA strategy. This involves contributing to a Traditional IRA first, then converting it to a Roth IRA. This way, you can enjoy tax-free growth and withdrawals in retirement.

-

Carried Interest: This is a tax loophole often used by investment managers. It allows them to pay taxes on their earnings from managing investments at the lower long-term capital gains rate rather than the higher ordinary income tax rate.

-

Life Insurance: Permanent life insurance policies, like whole life, can be used as a tax-efficient savings vehicle. The cash value grows tax-deferred, and you can borrow against it tax-free.

How to avoid the 32% tax bracket?

-

Income Management: Carefully manage your income to avoid jumping into a higher tax bracket. This can include deferring bonuses or other income to future years when you might be in a lower bracket.

-

Timing Income and Expenses: Align your income and expenses to minimize tax liability. For instance, if you’re expecting a large bonus, consider accelerating deductible expenses into the current year to offset the additional income.

By understanding and utilizing these strategies, high-income earners can effectively manage their tax liabilities and maximize their financial well-being.

Conclusion

Navigating the complexities of tax planning as a high-income earner can be challenging, but it doesn’t have to be overwhelming. At Elite Tax Strategy Solutions, we specialize in crafting personalized tax plans that align with your financial goals and ensure long-term stability. Our team of experts is dedicated to helping you maximize your tax savings while maintaining compliance with changing tax laws.

We understand that each individual’s financial situation is unique, which is why we take a proactive approach to tax optimization. By integrating tax planning with your broader financial strategy, we aim to improve your overall financial well-being. Whether it’s maximizing deductions, utilizing strategic retirement contributions, or exploring investment strategies for tax efficiency, our comprehensive services are designed to meet your specific needs.

Our commitment to staying informed about the latest tax legislation ensures that we can offer innovative solutions custom to your circumstances. As tax laws change, we adjust our strategies to keep you ahead of the curve, helping you achieve financial stability and peace of mind.

If you’re ready to take control of your tax situation and secure your financial future, we invite you to explore our Innovative Tax Planning services. Let us partner with you to develop a tax plan that not only saves you money but also supports your long-term goals. Together, we can turn the complexities of tax planning into opportunities for growth and success.