Why 2019 Tax Strategies Still Matter for 2025’s High-Income Americans

“Tax strategies for high income earners 2019” may sound dated, but the lessons from that pivotal year are still driving meaningful savings for wealthy Americans in 2025. Back in 2019, IRS data showed that more than one-quarter of filers with Adjusted Gross Income (AGI) above $500,000 managed to push their federal effective tax rate below 20% by combining smart retirement-plan use, capital-gains harvesting, and proactive charitable planning. Those pillars remain just as powerful—if not more so—under today’s similar marginal-rate environment.

Key 2019 principles that continue to work in 2025:

- 401(k) and cash-balance plan maximization – annual limits have risen, creating even larger upfront deductions.

- Roth IRA and “backdoor” Roth strategies – higher income thresholds make conversion timing critical.

- Income-splitting through S-corporations and family partnerships – core concepts still allowed under current IRS rules.

- Capital-gains management – the 0%/15%/20% federal brackets remain unchanged.

- Qualified Business Income (QBI) deduction – Section 199A planning continues to benefit high-earning pass-through owners.

- Alternative Minimum Tax (AMT) planning – the TCJA’s higher exemptions are scheduled to sunset after 2025, making AMT projections essential.

I’m David Fritch, CPA/JD and founder of Elite Tax Strategy Solutions in Jasper, Indiana. Over four decades I’ve guided physicians, executives, and closely held-business owners earning $200,000 to $2 million through exactly this type of multi-year planning—ensuring they keep more of what they earn while staying fully compliant with the IRS.

Further reading on tax-reduction fundamentals:

Understanding 2019 High-Income Definitions—and Why They Still Matter in 2025

In 2019 the IRS treated single filers with AGI above $200,000 (or $250,000 married filing jointly) as “high-income” for many surtaxes, including the 3.8% Net Investment Income Tax. Crossing $510,300 single or $612,350 joint put taxpayers into the top 37% federal bracket—levels that remain similar today after inflation adjustments.

(Note: The table above illustrates marginal-rate differences from a historical perspective. 2025 brackets are slightly higher because of annual IRS inflation indexing.)

How Different Income Streams Were Taxed in 2019—and Are Still Taxed Today

- Ordinary salary and bonus income faced full marginal rates (plus payroll taxes).

- Long-term capital gains and qualified dividends benefited from preferential 0%/15%/20% brackets.

- Section 1202 gains on Qualified Small Business Stock allowed up to 100% federal exclusion.

Alternative Minimum Tax: The 2019 Wake-Up Call

Although the TCJA greatly increased AMT exemptions, high earners exercising incentive stock options or realizing large capital gains in 2019 still tripped AMT. With TCJA provisions expiring after 2025, understanding the old 2019 rules gives a clear playbook for what could come back.

IRS 2019 inflation adjustments

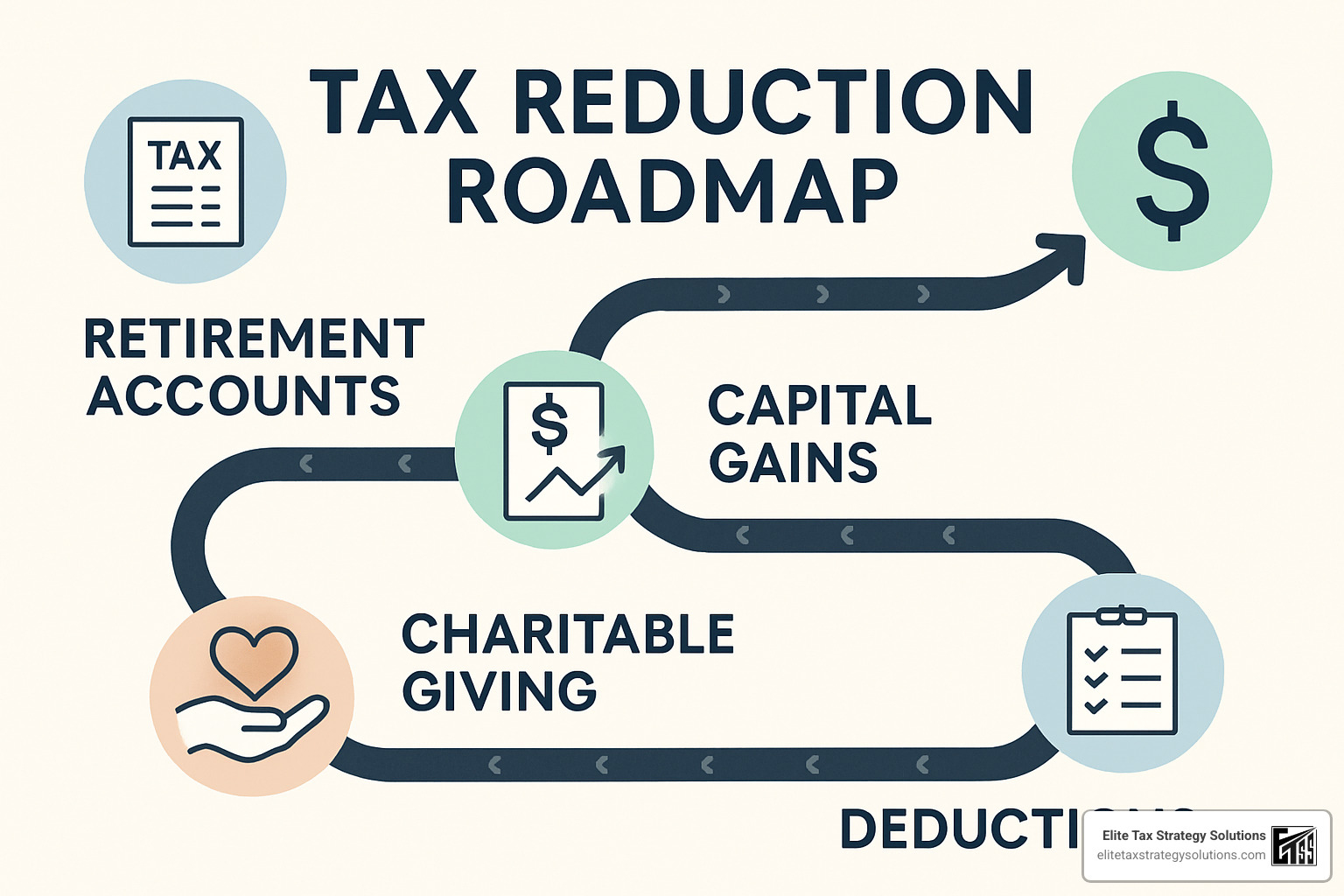

Proven 2019 Tax Strategies and Their 2025 Applications

The most effective tax strategies for high income earners 2019 revolved around deferral, conversion, and deduction maximization. Those same pillars drive 2025 planning:

More info about Tax Planning Strategies

Maximizing Deductions & Credits: Lessons That Never Age

- Home-office deduction (actual-expense method) can save $2,000–$5,000 annually for consultants and remote executives.

- Investment-interest expense and margin-loan interest remain deductible up to net investment income.

- Health Savings Accounts (HSAs) allow a triple tax break—deductible contributions, tax-free growth, and tax-free medical withdrawals.

- Accelerating charitable gifts with a Donor-Advised Fund still pairs well with itemized-deduction bunching.

More info about Strategies to Reduce Taxes

Registered & Qualified Accounts: 401(k), Roth & Cash-Balance Power Plays

- 401(k) salary deferral limits have climbed from $19,000 in 2019 to $23,000 in 2025 (plus $7,500 catch-up).

- Mega-backdoor Roth contributions remain viable for plan sponsors that permit after-tax deposits and in-plan conversions.

- Cash-balance or defined-benefit plans let profitable small firms shelter $100,000 + per owner each year.

Business-Owner Toolkit—S-Corporations, 199A & Entity Optimization

- S-corp salary vs. distribution optimization balances payroll taxes with reasonable-compensation rules.

- Section 199A QBI deduction offers up to 20% off the top for qualified pass-through income.

- Electing to be taxed as an S-corp can still slash Medicare tax for high-margin service businesses.

More info about High Income Self Employed Tax Strategies

Income-Shifting & Trusts: Keeping Wealth in the Family

- Family limited partnerships (FLPs) and intentionally defective grantor trusts (IDGTs) help push growth to the next generation while freezing estate values.

- Intra-family loans pegged to the AFR (as low as 4.69% long-term in early 2025) remain attractive compared to market rates.

Capital-Gains Management & Deferral Tactics

- Tax-loss harvesting pairs losers with winners to net out gains.

- Section 453 installment sales spread gain over multiple years.

- Qualified Opportunity Zones (QOZs) still allow gain deferral until 2027 and possible exclusion on future appreciation.

Scientific research on capital-gain timing

More info about Tax Diversification Strategy High Income

Compliance Lessons from 2019: Staying on the IRS’s Good Side in 2025

2019 audits reminded high earners that the line between savvy and aggressive can be thin. The same warning holds true in 2025.

- Legitimate planning leverages the Internal Revenue Code exactly as Congress intended—maxing savings plans, tracking real business expenses, and structuring entities for bona-fide economic reasons.

- Aggressive avoidance often relies on questionable basis inflation, artificial losses, or transactions lacking economic substance. The IRS can disallow benefits under the economic-substance doctrine or step-transaction doctrine.

Essential Record-Keeping Lessons

- Digitize receipts and invoices.

- Maintain contemporaneous business mileage logs.

- Keep corporate minutes and shareholder resolutions up to date.

- Retain trust distribution schedules for at least seven years.

Common Mistakes to Avoid

- Waiting until December to explore strategies.

- Ignoring AMT exposure when exercising stock options.

- Failing to substantiate the reasonableness of S-corp officer compensation.

- Overfunding retirement accounts and triggering 6% excise penalties.

2019 Lessons for 2025 Tax Planning

The most durable tax strategies for high income earners 2019 shared three traits: rate arbitrage, timing, and integration. Those concepts are just as powerful now that we’re approaching the TCJA sunset in 2026.

- Rate arbitrage – changing wages taxed at 37% + payroll into long-term capital gains taxed at 20% (or 0%/15% for lower brackets).

- Timing strategies – accelerating deductions (charity, retirement) into high-income years while deferring income into lower-bracket years.

- Bracket management – smoothing income spikes from equity grants or business sales across multiple years or taxpayers.

The biggest 2019 takeaway was that integrated planning beats isolated tactics. Coordinating entity structure, retirement plans, trusts, and investment portfolios as one system routinely produced six-figure lifetime savings.

Applying 2019 Insights Today

With marginal rates set to rise if Congress lets the TCJA lapse, 2025 is the time to lock in lower rates through Roth conversions, accelerated income, and estate-freeze strategies—exactly the moves that worked so well back in 2019.

Frequently Asked Questions about Tax Strategies for High Income Earners 2019

What income level did the IRS consider “high” in 2019?

For surtax purposes, the IRS tagged single filers with AGI above $200,000 (or $250,000 MFJ) as high earners. That threshold is still where the 3.8% Net Investment Income Tax and additional 0.9% Medicare tax kick in.

How did high earners legally push their federal rate below 20% in 2019?

- Maximizing 401(k), SEP-IRA, and defined-benefit contributions to cut taxable wages.

- Harvesting long-term capital gains subject to a 15% or 20% maximum rate instead of 37% ordinary.

- Utilizing the Section 199A QBI deduction for up to 20% off qualified pass-through income.

- Donating appreciated securities to eliminate the embedded gain and claim a full fair-market-value deduction.

All four remain available in 2025, though dollar limits have increased.

Which qualified plan offered the biggest 2019 deduction?

For business owners, a cash-balance or traditional defined-benefit plan often allowed tax-deductible contributions exceeding $100,000—more than triple the 2019 401(k) cap. Today, maximums are even higher, making these plans an indispensable tool for profitable professional practices.

Conclusion

The tactics that let smart taxpayers legally reduce huge 2019 tax bills are still saving Jasper-area physicians, executives, and entrepreneurs real money in 2025. When you defer taxed income, convert salary into preferential forms, and maximize every legitimate deduction and credit, you create an integrated strategy that holds up under IRS scrutiny.

Elite Tax Strategy Solutions delivers that coordinated approach—from entity selection to retirement-plan design—so you never leave money on the table.

Ready for a lower-stress April? Let’s talk today.