Understanding Tax Strategies for High Income Couples

For high-income couples seeking immediate tax relief, here are the most effective strategies:

- Maximize retirement contributions (401(k), IRA, HSA) – up to $23,000 per spouse in 401(k) plus catch-up contributions

- Manage investment income through tax-loss harvesting and strategic capital gains timing

- Consider charitable giving via donor-advised funds or qualified charitable distributions

- Explore income deferral or acceleration to optimize tax brackets

- Use advanced planning tools like trusts or family limited partnerships when appropriate

Tax strategies for high income couples have become increasingly important as couples face progressive tax brackets that can claim a significant portion of their earnings. When you earn a higher income as a couple, you don’t just make more money—you face more complex tax situations, higher marginal rates, and potentially more scrutiny from the IRS.

For married couples with combined incomes exceeding $383,900 (2024 threshold for high-income earners filing jointly), strategic tax planning isn’t just helpful—it’s essential. The highest federal tax bracket of 37% applies to couples with taxable income over $731,200, not including additional taxes like the 3.8% Net Investment Income Tax or state and local taxes.

The good news? With thoughtful planning, high-income couples can legally reduce their tax burden through various strategies that take advantage of the tax code’s provisions. From maximizing retirement account contributions to strategic charitable giving, income timing, and investment tax management, there are numerous approaches that can help you keep more of what you earn.

I’m David Fritch, and with over 40 years of experience as both a CPA and attorney specializing in tax strategies for high income couples, I’ve helped countless clients steer the complexities of tax planning to optimize their financial outcomes while ensuring full compliance with tax laws.

Glossary for tax strategies for high income couples:

– tax planning for partnerships

– financial planning for high income earners

– wealth management tax planning

Mapping the High-Income Landscape for Couples

Welcome to the sometimes confusing world of high-income tax brackets! Before diving into strategies, let’s get clear on where you and your spouse actually stand in the eyes of the IRS.

The IRS typically considers you “high-income earners” when you report $200,000 or more in total positive income (TPI) on your tax return. For married couples filing jointly, this threshold effectively doubles to $400,000. But here’s where things get interesting.

When planning your taxes, we usually focus on your Adjusted Gross Income (AGI) rather than TPI. Your AGI represents your total income minus specific adjustments like retirement contributions and self-employment taxes. Looking ahead to 2025, married couples filing jointly will hit the highest federal tax bracket of 37% when their taxable income exceeds $751,600.

But regular income tax is just the beginning. High-income couples also face:

- A 3.8% Net Investment Income Tax when your Modified AGI exceeds $250,000

- An additional 0.9% Medicare surtax on wages above $250,000

- Potential Alternative Minimum Tax (AMT) exposure

- State and local taxes ranging from 0-13% depending on where you live

Most high-income couples benefit from filing jointly, but the infamous “marriage penalty” can still bite when both spouses earn substantial incomes. This happens because you might reach higher tax brackets faster as a married couple than you would as two single filers.

Here’s how different filing scenarios typically play out:

| Income Scenario | Married Filing Jointly | Married Filing Separately | Potential Savings |

|---|---|---|---|

| One high earner ($400K), spouse no income | Lower overall rate | Higher overall rate | Up to $15,000 filing jointly |

| Both high earners ($250K each) | Potential bracket creep | May avoid some surtaxes | Varies by deduction profile |

| Uneven incomes ($350K and $100K) | Lower overall rate | Higher overall rate | Up to $10,000 filing jointly |

Where you live adds another layer to consider. States like Florida, Texas, and Nevada have no income tax, while California, New York, and New Jersey can take more than 10% of your income. If one of you works remotely or travels frequently for work, keeping detailed records of your physical presence in different states can significantly reduce your state tax burden.

Audit & Record-Keeping Hotspots for High Earners

Let’s be honest – the more you make, the more attention you get from the IRS. They audit about 1% of returns with income between $200,000 and $1 million, but that jumps to nearly 2% for incomes above $1 million.

What tends to trigger these audits? For high-income couples, these red flags stand out:

Large charitable donations (especially non-cash contributions), home office deductions (particularly when both spouses claim them), cryptocurrency transactions without proper reporting, rental property losses claimed as active participants, significant business expenses on Schedule C, and discrepancies between your reported income and information returns.

Your best defense is meticulous record-keeping. Keep digital and physical copies of all tax documents for at least seven years. Document business expenses with receipts and purpose notes. For charitable gifts over $250, always get written acknowledgments. If you have business vehicles, maintain usage logs separating personal and business miles. And if you split time between multiple states, document your days spent in each location.

One of our clients recently turned what could have been a stressful audit into a simple verification process. When questioned about a large charitable donation, they calmly provided their donor acknowledgment letter, appraisal documentation, and transfer records—resulting in no changes to their return and a quick conclusion to the audit.

Understanding where you stand in this complex landscape is the foundation of effective tax strategies for high income couples. With this knowledge, you’ll be better equipped to make informed decisions about the specific strategies we’ll explore in the following sections.

Tax Strategies for High Income Couples: Core Income-Reduction Tactics

The heart of smart tax planning is knowing how to legally reduce your taxable income. For high-income couples, this isn’t just about saving a few dollars—it’s about potentially keeping tens of thousands more of your hard-earned money.

Maximizing Retirement & Health Accounts

Think of retirement accounts as your first line of defense against high taxes. In 2024, you and your spouse can each stash away $23,000 in your 401(k) plans—that’s $46,000 of income you won’t pay taxes on this year! If you’re 50 or older, that catch-up contribution adds another $7,500 per person.

“One of our clients, a surgeon and her engineer husband, were amazed when we showed them how sheltering $77,000 in retirement accounts dropped their effective tax rate by nearly 4%,” shares our lead tax strategist.

But why stop there? If you have a high-deductible health plan, an HSA is truly the unicorn of tax accounts. With family coverage, you can contribute $8,300 ($9,300 if you’re 55+), and enjoy what we call the “triple crown” of tax benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Many of our savvy clients pay medical costs out-of-pocket while letting their HSA investments grow untouched for decades. It’s like having an extra retirement account hiding in plain sight!

For those bumping against income limits for Roth IRAs, the backdoor Roth strategy remains viable. You contribute to a traditional IRA (without taking a deduction) and then convert those funds to a Roth. When done properly, you’ll enjoy tax-free growth and withdrawals in retirement.

Self-employed? Your options expand dramatically with SEP IRAs or Solo 401(k)s allowing contributions up to $66,000 in 2024 ($73,500 for those 50+). That’s serious tax-sheltering power!

More info about retirement tactics

For more information on retirement account eligibility and contribution limits

Charitable Giving That Pays You Back

Being generous can also be financially smart. For couples passionate about giving back, strategic charitable planning offers significant tax advantages.

Donor-Advised Funds (DAFs) are perhaps the most flexible tool in your charitable arsenal. They allow you to “bunch” multiple years of giving into a single tax year, claim the full deduction immediately, but distribute the funds to charities gradually over time.

“I remember working with a couple who normally donated $20,000 annually,” recalls our senior tax advisor. “By contributing $60,000 to a DAF in one year instead of spreading it over three years, they itemized deductions that year and took the standard deduction the next two years. This simple shift saved them over $12,000 in taxes!”

When donating, consider giving appreciated securities instead of cash. If you donate stock you’ve held for over a year, you’ll avoid capital gains tax completely while still deducting the full fair market value. For couples in the highest tax brackets, this double benefit can increase the impact of your donation by up to 37%.

For those over 70½, Qualified Charitable Distributions (QCDs) let you donate directly from your IRA to charity—up to $105,000 annually. This counts toward your Required Minimum Distribution but doesn’t increase your taxable income. It’s especially powerful for couples who don’t need their IRA distributions for living expenses.

Income Shifting & Timing for Bracket Control

One of the most overlooked tax strategies for high income couples is strategic timing of when you recognize income and take deductions.

Think of tax brackets as buckets. Once one bucket fills up, additional income spills into the next bucket at a higher tax rate. By controlling when income flows in and deductions flow out, you can optimize which buckets get filled each year.

In years when your income peaks (perhaps due to a bonus or business success), consider maxing out retirement contributions, deferring additional income to January of the next year if possible, and accelerating deductible expenses like property taxes (keeping SALT limitations in mind).

Conversely, in lower-income years, consider pulling income forward through Roth conversions or realizing capital gains at potentially lower rates. This “tax bracket arbitrage” can save substantial amounts over time.

“We helped a dual-physician couple time their sabbaticals to fall in the same tax year,” shares our planning director. “During that year of reduced income, they converted $200,000 from traditional to Roth IRAs at the 24% bracket instead of their normal 37% rate. That single move saved them approximately $26,000 in lifetime taxes.”

The key is looking beyond the current tax year. With thoughtful multi-year planning, you can smooth out tax spikes and take advantage of temporary dips in income to position yourself for long-term tax efficiency.

Tax Planning Strategies for High-Income Earners

Managing Capital Gains, Losses, and Investment Income

Investment income can make up a hefty chunk of your financial picture when you’re a high-earning couple. Understanding how these dollars get taxed is essential for keeping more of what your investments earn.

When it comes to investment returns, timing makes all the difference. Long-term capital gains from assets you’ve held longer than a year enjoy preferential tax rates (0%, 15%, or 20%), while short-term gains from assets held a year or less get taxed as ordinary income—potentially up to that hefty 37% top rate.

Similarly, qualified dividends (typically from stocks you’ve held long enough) receive the same favorable rates as long-term gains, while non-qualified dividends face ordinary income rates. Many couples find municipal bond interest particularly attractive since it’s generally exempt from federal taxes and sometimes state taxes too.

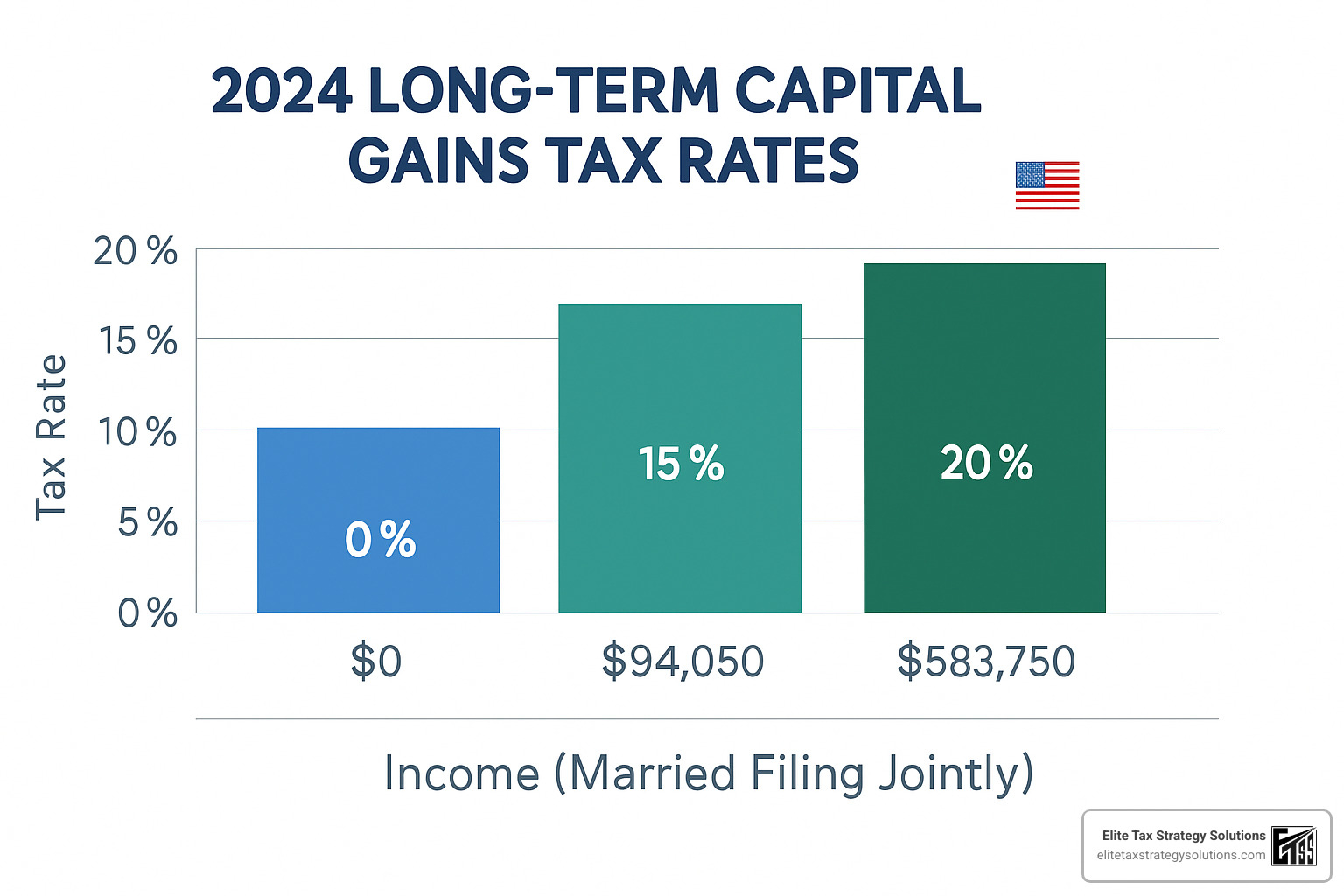

For 2024, married couples filing jointly will see these long-term capital gains brackets:

– 0% rate applies to taxable income up to $94,050 (yes, even high earners can have some gains tax-free if they plan carefully)

– 15% rate covers income between $94,051 and $583,750

– 20% rate kicks in above $583,750

Don’t forget that additional 3.8% Net Investment Income Tax that applies when your Modified Adjusted Gross Income exceeds $250,000. This effectively creates maximum rates of 18.8% or 23.8% on your investment gains.

Harvest Gains & Losses Like a Pro

Tax-loss harvesting isn’t just a fancy term—it’s a powerful strategy that can save high-income couples thousands in taxes each year.

The concept is straightforward: sell investments that have dropped in value to offset gains from your winners. There’s no limit to how much in capital gains you can offset with losses, and if your losses exceed your gains, you can deduct up to $3,000 against your ordinary income. Any excess losses don’t disappear—they carry forward indefinitely to future tax years.

Just watch out for those pesky wash-sale rules. If you sell a security at a loss and buy the same or a “substantially identical” security within 30 days before or after the sale, the IRS won’t let you claim that loss.

“Most of our clients know about harvesting losses, but they’re surprised when we talk about harvesting gains,” says our tax director with a smile. “In years when your income dips temporarily—maybe between jobs or during a sabbatical—consider selling appreciated assets to lock in gains at lower tax rates, even 0% in some cases.”

The beauty of gain harvesting? Unlike with losses, there’s no wash-sale rule, so you can immediately repurchase the same securities, effectively resetting your cost basis higher without waiting a month.

One couple we worked with sold $50,000 of appreciated stock during a gap year between executive positions. They paid just 15% on those gains instead of the 23.8% they would have paid the following year—saving nearly $4,400 in taxes with this simple move.

Tax-Efficient Asset Location & Diversification

Where you hold your investments matters just as much as what you invest in—something many high-income couples overlook.

Think of your various account types as different buckets, each with unique tax treatment:

Tax-deferred accounts like 401(k)s and traditional IRAs work best for investments that generate ordinary income or frequent short-term gains. Your REITs, high-turnover funds, and taxable bonds belong here, where their income won’t trigger annual tax bills.

Tax-free accounts such as Roth IRAs and HSAs are perfect homes for your highest-growth investments. Since you’ll never pay taxes on these gains, put assets here that you expect to appreciate the most over time.

Taxable brokerage accounts are ideal for tax-efficient investments like index funds, municipal bonds, and stocks you plan to hold for years. These investments naturally minimize taxable events, and when gains do occur, they often qualify for those lower long-term capital gains rates.

I recently worked with a physician and her attorney husband who moved their corporate bond fund from their taxable account to their IRAs and replaced it with a total market index fund. This simple switch—without changing their overall asset allocation—saved them approximately $3,200 annually in taxes.

Tax strategies for high income couples should always include creating tax diversification across account types. Having money in different tax buckets gives you tremendous flexibility in retirement, allowing you to manage your tax bracket by strategically choosing which accounts to tap each year.

Tax Diversification Strategy for High Income

Advanced Planning Tools & Risk Management

When your financial picture becomes more complex, it’s time to explore sophisticated planning tools that can provide both tax advantages and protection for your wealth. As a high-income couple, these strategies can make a substantial difference in your long-term financial outcomes.

Let me share something I’ve observed over my years working with successful couples: those who implement advanced planning tools often express the same sentiment – “I wish we’d done this sooner.” The peace of mind that comes from knowing you’ve optimized your tax situation while protecting your family’s financial future is truly invaluable.

Trusts offer particularly powerful planning opportunities for high-income couples. Grantor trusts can help shift income to family members in lower tax brackets, potentially keeping more money in the family instead of sending it to the IRS. Charitable remainder trusts (CRTs) provide you with income for a set period before the remainder goes to your chosen charity – giving you an immediate partial tax deduction while supporting causes you care about. For those with significant home equity, qualified personal residence trusts (QPRTs) can transfer your home to beneficiaries at a reduced gift tax value.

Many of our clients with family businesses or investment portfolios have benefited from family limited partnerships (FLPs). These structures excel at transferring business interests or investment assets to the next generation while allowing you to maintain control. They can shift both income and appreciation to family members in lower tax brackets and may qualify for valuation discounts for gift tax purposes – a significant advantage when planning generational wealth transfers.

If you have children or grandchildren, 529 college savings plans deserve serious consideration. These plans offer tax-free growth for education expenses and allow for “superfunding” – contributing five years of annual gift tax exclusions upfront ($85,000 per donor per beneficiary in 2024). One couple I worked with funded their grandchildren’s education while simultaneously reducing their taxable estate by over $500,000 using this strategy.

Don’t overlook the power of life insurance in your advanced planning toolkit. Beyond providing tax-free death benefits to your loved ones, cash value policies can offer tax-deferred growth and tax-free access to funds through policy loans during your lifetime. This creates what some call a “private family bank” that can provide liquidity when needed without triggering taxable events.

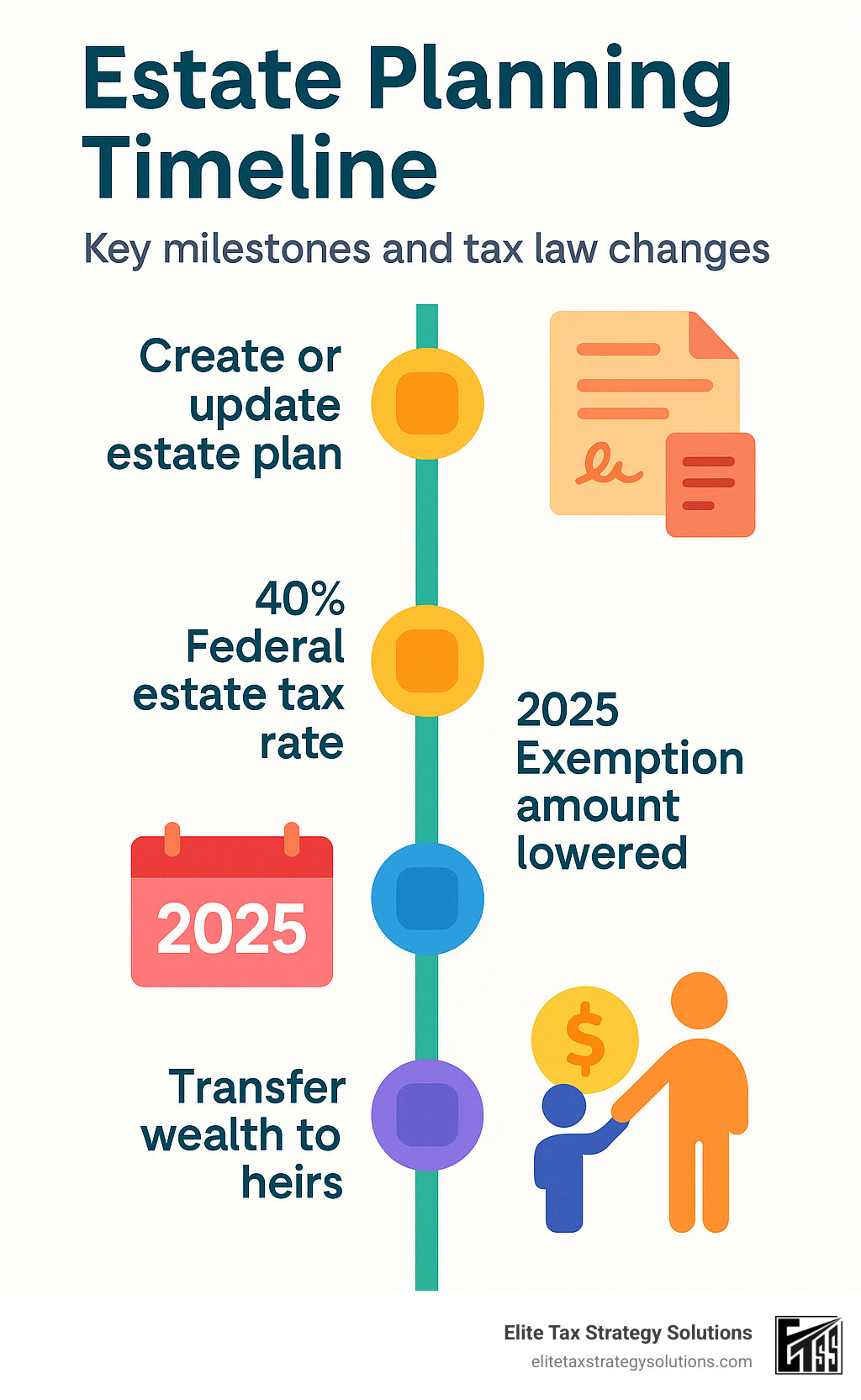

Here’s something urgent to consider: the estate tax exemption is scheduled to sunset at the end of 2025, potentially dropping from approximately $13.6 million per person to around $7 million (adjusted for inflation). If your net worth approaches these figures, now is the time to consider accelerating wealth transfer strategies. The window of opportunity is closing, and proper planning takes time to implement.

For more comprehensive information on these approaches, visit our Advanced Tax Planning Strategies page, or review scientific research on charitable trusts from the IRS.

Safeguarding Against Future Tax Law Changes

“The only constant in tax law is change,” as we often remind our clients. Building flexibility into your planning isn’t just smart – it’s essential. Recent significant changes include the SECURE Act 2.0, which modified retirement account rules including RMD ages and catch-up contribution limits, and the Tax Cuts and Jobs Act (TCJA) provisions, many of which expire after 2025.

To protect yourself against future changes, focus on tax diversification across accounts (pre-tax, Roth, and taxable). This creates flexibility regardless of future tax rates. Build flexibility into estate planning documents with provisions that adapt to changing laws. Consider Roth conversions before potential tax rate increases – many of our clients are accelerating these conversions now, believing rates may increase after 2025.

Most importantly, stay informed about proposed legislation and work with advisors who monitor tax law changes and proactively recommend adjustments. At Elite Tax Strategy Solutions, we provide quarterly updates on tax law changes and their potential impact on your planning strategies – because being proactive rather than reactive can save you thousands.

State & Local Tax Optimization

When we talk about tax strategies for high income couples, many focus exclusively on federal taxes while overlooking the significant impact of state and local taxes. Since the Tax Cuts and Jobs Act capped the state and local tax (SALT) deduction at $10,000, managing these taxes has become even more critical.

For property tax management, consider prepaying property taxes when beneficial (though still subject to the SALT cap). Don’t hesitate to appeal assessments when property values are overstated – one client saved over $4,000 annually by successfully challenging an inflated assessment. Also, evaluate the timing of home improvements that might increase assessments.

When it comes to income tax planning, remote work has created new opportunities and challenges. If you’re working remotely, understand how telecommuting affects your state tax obligations – some states have different rules that could result in double taxation if not carefully managed. For those splitting time between homes in different states, document your physical presence carefully with a day-counting app or calendar system.

Considering a move to a lower-tax state? Be aware that high-tax states often aggressively challenge residency changes. To establish new residency convincingly, change your voter registration, driver’s license, and vehicle registrations. Update estate planning documents to reflect your new state. Join local organizations and establish community ties. Document days spent in each state with receipts, travel records, and digital footprints. And don’t forget to change primary healthcare providers to those in your new location.

I’ll never forget the couple who saved over $70,000 annually by properly establishing Florida residency after retiring from their New York careers. The key wasn’t just moving – it was creating a comprehensive documentation trail and making a clean break from their former state. When New York initiated a residency audit (as they often do), this couple was fully prepared with evidence that withstood scrutiny.

With thoughtful planning and expert guidance, these advanced strategies can help you protect what you’ve worked so hard to build while ensuring more of your wealth benefits you and your loved ones rather than the tax collector.

Frequently Asked Questions about Tax Strategies for High Income Couples

What qualifies us as a “high-income couple” for IRS purposes?

Wondering if you fall into the “high-income” category? You’re not alone. While the IRS doesn’t have a single definition, there are several important thresholds to be aware of.

For audit purposes, the IRS typically considers couples reporting $400,000 or more in Total Positive Income (TPI) to be high-income earners. But that’s just one measure. If you’re filing jointly in 2024, you’ll hit the highest tax bracket of 37% once your income exceeds $731,200.

Beyond these basic thresholds, you’ll face additional taxes when your Modified Adjusted Gross Income (MAGI) crosses $250,000 – that’s when both the 3.8% Net Investment Income Tax and the 0.9% additional Medicare tax kick in.

In our experience at Elite Tax Strategy Solutions, we’ve found that tax planning needs increase significantly once your combined income exceeds $400,000. At this level, you’re not just dealing with higher marginal rates – you’re also navigating additional surtaxes and watching valuable deductions and credits phase out.

How can we minimize capital gains taxes while still investing aggressively?

“I want to invest for growth, but I’m worried about the tax bill.” We hear this concern from clients all the time, and fortunately, you don’t have to choose between growth and tax efficiency.

Hold investments for more than a year whenever possible to qualify for those lower long-term capital gains rates instead of paying ordinary income rates. Strategic tax-loss harvesting throughout the year (not just in December!) can offset gains while keeping your investment strategy intact.

Where you hold investments matters tremendously. Consider placing your most tax-efficient investments in taxable accounts while keeping assets that generate ordinary income in tax-advantaged accounts. For the taxable portion of your portfolio, municipal bonds can provide tax-exempt income – especially valuable for those in higher brackets.

I recently worked with Sarah and Michael, technology executives with significant stock options. By combining several of these strategies, we reduced their effective capital gains tax rate from 23.8% to under 15%, saving them over $40,000 in a single year. They were able to maintain their aggressive growth strategy while keeping more of their investment returns.

Donating appreciated securities to charity instead of cash provides a double tax benefit – you get the deduction and avoid the capital gains tax entirely. And for those with significant gains, opportunity zone investments can provide both tax deferral and potential reduction of capital gains.

When should we seek professional tax advice?

Tax software works well for simple situations, but high-income couples often leave thousands of dollars on the table by going the DIY route. Here’s when professional advice becomes particularly valuable:

During major life events like marriage, divorce, having children, or approaching retirement, your tax situation can change dramatically. The same applies to career changes – especially when they involve equity compensation, starting a business, or significant promotions.

Before making large investment decisions like buying or selling real estate or businesses, consult with a tax professional. Years with unusual income fluctuations – whether unusually high (bonus, stock option exercise) or low (sabbatical, job transition) – present special planning opportunities that shouldn’t be missed.

As your net worth approaches the estate tax exemption, estate planning needs become more complex and intertwined with income tax planning. And if you’re dealing with multi-state issues or international considerations, professional guidance is absolutely essential.

The best approach is proactive planning – not just annual tax preparation. At Elite Tax Strategy Solutions, our most successful clients meet with us quarterly, allowing us to implement strategies well before December 31st deadlines. This ongoing relationship typically pays for itself many times over.

Take James and Elena, for example. Through quarterly planning sessions, we’ve helped them save approximately $47,000 annually – a substantial return on their advisory fees. More importantly, they sleep better knowing their tax strategy is being actively managed throughout the year, not just at tax time.

Tax strategies for high income couples work best when implemented as part of a comprehensive financial plan that reflects your unique situation and goals.

Conclusion

Effective tax strategies for high income couples require a comprehensive, proactive approach. By understanding your unique tax situation and implementing the appropriate strategies, you can significantly reduce your tax burden while building wealth and achieving your financial goals.

Remember these key principles:

- Be proactive, not reactive—tax planning should happen year-round

- Stay informed about tax law changes that could affect your strategies

- Coordinate your tax planning with your overall financial and estate planning

- Document everything carefully to support your positions if questioned

- Review and adjust your strategies as your circumstances and tax laws change

At Elite Tax Strategy Solutions, we specialize in helping high-income couples steer the complexities of tax planning. Our team of experienced professionals works closely with each client to develop customized strategies that align with their specific goals and circumstances.

Whether you’re looking to optimize your current tax situation, plan for retirement, or create a legacy for future generations, we have the expertise to help you achieve your objectives while minimizing your tax burden.

Contact us today to schedule a consultation and find how we can help you implement effective tax strategies for high income couples to keep more of what you earn and build lasting wealth.