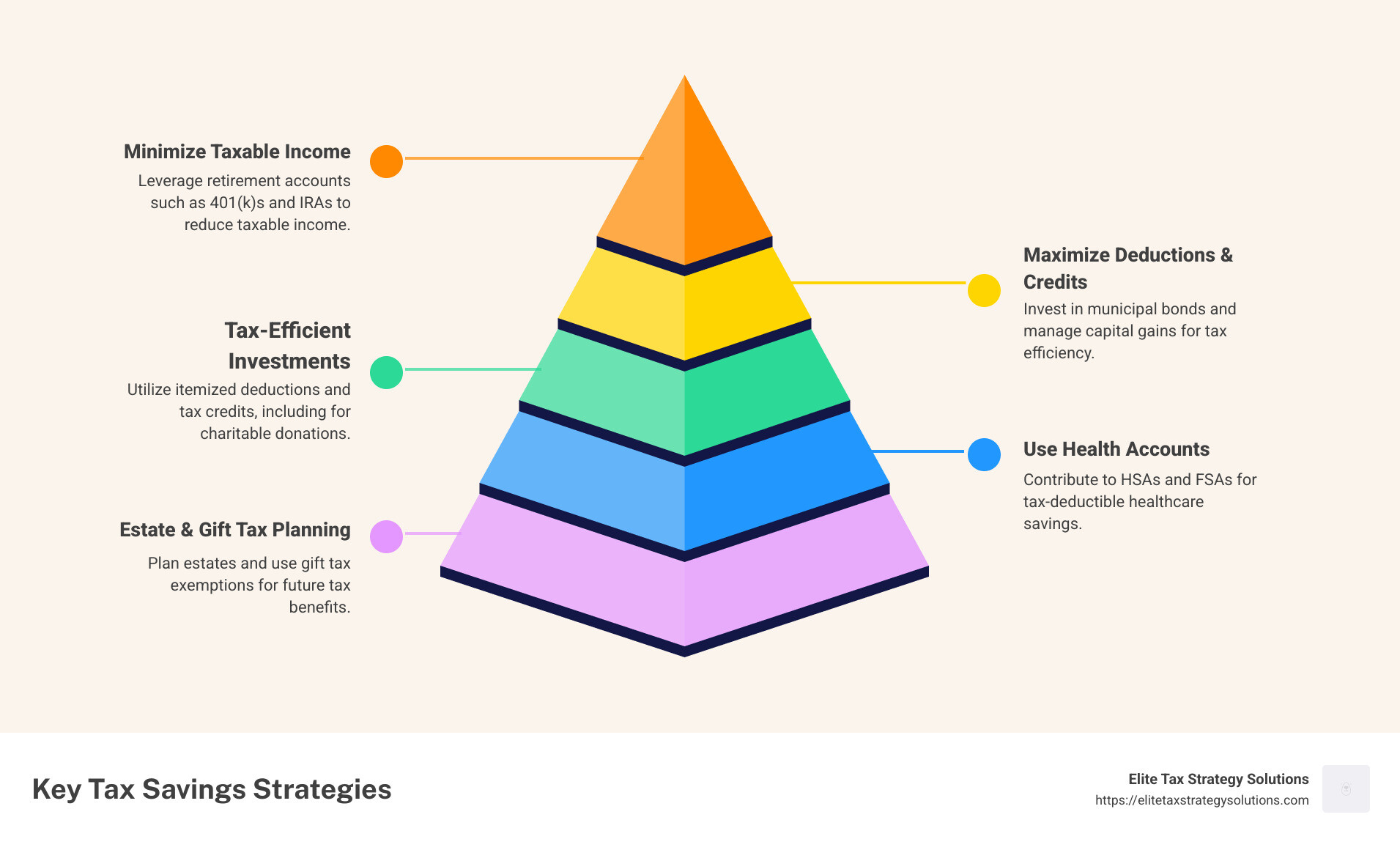

Tax savings strategies are crucial for anyone looking to maximize income while minimizing tax liabilities. These strategies involve a range of actions, such as minimizing taxable income, taking advantage of credits and deductions, and investing in tax-efficient accounts. For a quick overview, keep in mind these key steps:

- Minimize taxable income through smart retirement planning.

- Maximize deductions and credits by bunching expenses.

- Invest in tax-efficient accounts such as Roth IRAs.

- Use HSAs and FSAs for healthcare-related tax savings.

- Consider estate and gift tax planning for long-term benefits.

Navigating the intricate tax system can be challenging, but implementing effective strategies can lead to significant savings and financial stability. Staying informed and proactive with your tax planning can make a meaningful difference in your financial life.

As an expert in tax savings strategies, I’m David Fritch, and I’ve spent over 40 years helping clients like you steer the complexities of tax law. My goal is to provide planning that aligns with both current needs and future financial stability. Let’s explore how you can effectively implement these strategies.

Tax savings strategies terms made easy:

– maximize tax savings

– advanced tax strategies

– tax planning for small businesses

Minimize Taxable Income

Reducing your taxable income is a powerful way to save on taxes. One of the most effective methods for doing this is through retirement accounts. By contributing to these accounts, you not only save for the future but also reduce your taxable income today. Here’s how you can make the most of these opportunities:

Employer-Sponsored Plans

If your employer offers a retirement plan like a 401(k) or 403(b), take full advantage of it. Contributions to these plans are made with pretax dollars, which means the money goes into your account before taxes are taken out. For 2024, you can contribute up to $23,000. If you’re 50 or older, you can add an extra $7,500 as a catch-up contribution.

Example: Jane earns $100,000 a year. By contributing $23,000 to her 401(k), her taxable income drops to $77,000. This not only lowers her tax bill but also boosts her retirement savings.

Individual Retirement Accounts (IRAs)

An IRA is another excellent way to lower your taxable income. You can contribute up to $7,000 annually, with an additional $1,000 catch-up contribution if you’re over 50. Contributions to a traditional IRA are tax-deductible, reducing your taxable income for the year.

If you or your spouse have access to an employer-sponsored retirement plan, the rules for deducting IRA contributions can vary based on your income level. Be sure to check the latest IRS guidelines to see how much you can deduct.

Roth IRAs

While contributions to a Roth IRA are not tax-deductible, the growth and withdrawals during retirement are tax-free, provided certain conditions are met. This can be a strategic part of your long-term tax planning, especially if you expect to be in a higher tax bracket when you retire.

Simplified Employee Pension (SEP) Plans

For self-employed individuals, a SEP plan offers a flexible and straightforward way to save for retirement while reducing taxable income. You can contribute up to 25% of your net earnings from self-employment, up to a maximum of $66,000 in 2024.

Key Takeaway: By maximizing contributions to retirement accounts, you can significantly reduce your taxable income. This not only decreases your current tax liability but also improves your financial security for the future.

By integrating these strategies into your financial plan, you can effectively minimize your taxable income and set yourself up for a more secure financial future. Next, we’ll explore how to maximize deductions and credits to further improve your tax savings.

Maximize Deductions and Credits

Once you’ve minimized your taxable income, it’s time to focus on maximizing deductions and credits. This can further reduce your tax bill and increase your savings.

Charitable Donations

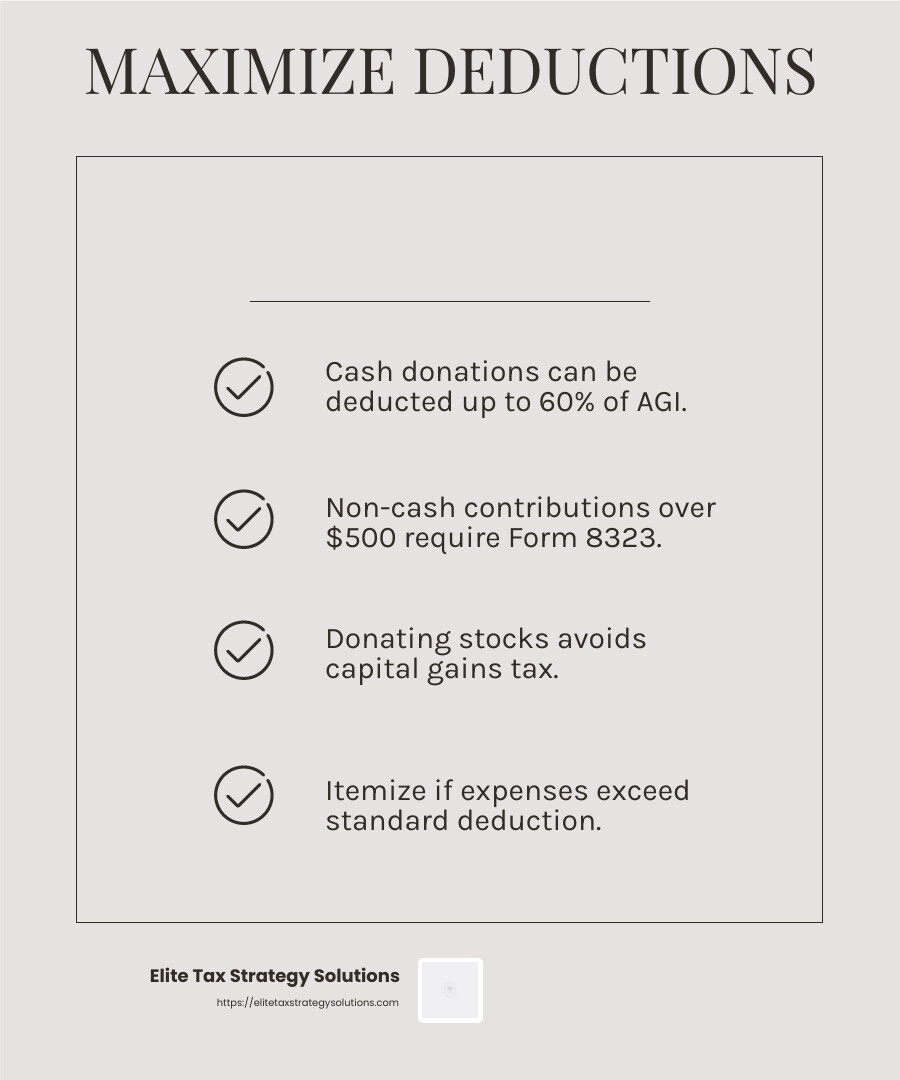

Giving to charity is a wonderful way to help others and potentially lower your tax liability. Donations to qualified organizations can be deducted from your taxable income, but you’ll need to itemize your deductions to take advantage of this.

-

Cash Donations: These can be deducted up to 60% of your adjusted gross income (AGI). Always keep receipts or acknowledgment letters from the charities for your records.

-

Non-Cash Contributions: Items like clothing or furniture may also be deductible. If these exceed $500 in value, you’ll need to complete Form 8323 with your tax return.

-

Appreciated Assets: Donating stocks or other appreciated assets can be a smart move. You can deduct the fair market value and avoid paying capital gains tax on the appreciation.

Itemized Deductions

The Tax Cuts and Jobs Act increased the standard deduction, making it less common for taxpayers to itemize. However, if your deductible expenses exceed the standard deduction, itemizing can be worthwhile.

-

Medical Expenses: You can deduct unreimbursed medical expenses that exceed 7.5% of your AGI. This includes things like doctor visits, prescriptions, and certain medical equipment.

-

State and Local Taxes (SALT): You can deduct up to $10,000 ($5,000 if married filing separately) for state and local property, income, or sales taxes.

-

Mortgage Interest: Interest paid on a mortgage can be deducted, which is especially beneficial for homeowners.

Tax Credits

Tax credits are powerful because they reduce your tax bill dollar-for-dollar. Here are a few to consider:

-

Child Tax Credit: Worth $2,000 per qualifying child, this credit can significantly lower your tax bill. There are income limits, so check if you qualify.

-

Earned Income Tax Credit (EITC): Designed for low- to moderate-income earners, the EITC can provide substantial savings. The amount varies based on income and the number of children.

-

Education Credits: The American Opportunity Tax Credit offers up to $2,500 per year for eligible students in higher education. The Lifetime Learning Credit provides up to $2,000 per return for qualified education expenses.

-

Saver’s Credit: This is for moderate- and lower-income individuals saving for retirement. You can receive a credit of up to 50% of your contributions to a retirement plan or IRA.

Key Takeaway: By maximizing deductions and credits, you can effectively lower your tax liability. This not only saves you money but also helps you allocate more resources towards your financial goals.

Next, we’ll dive into tax-efficient investments that can further optimize your tax savings strategy.

Tax-Efficient Investments

When it comes to tax savings strategies, investing wisely can make a big difference. Let’s explore how you can use municipal bonds, manage capital gains, and invest tax-efficiently to keep more of your money.

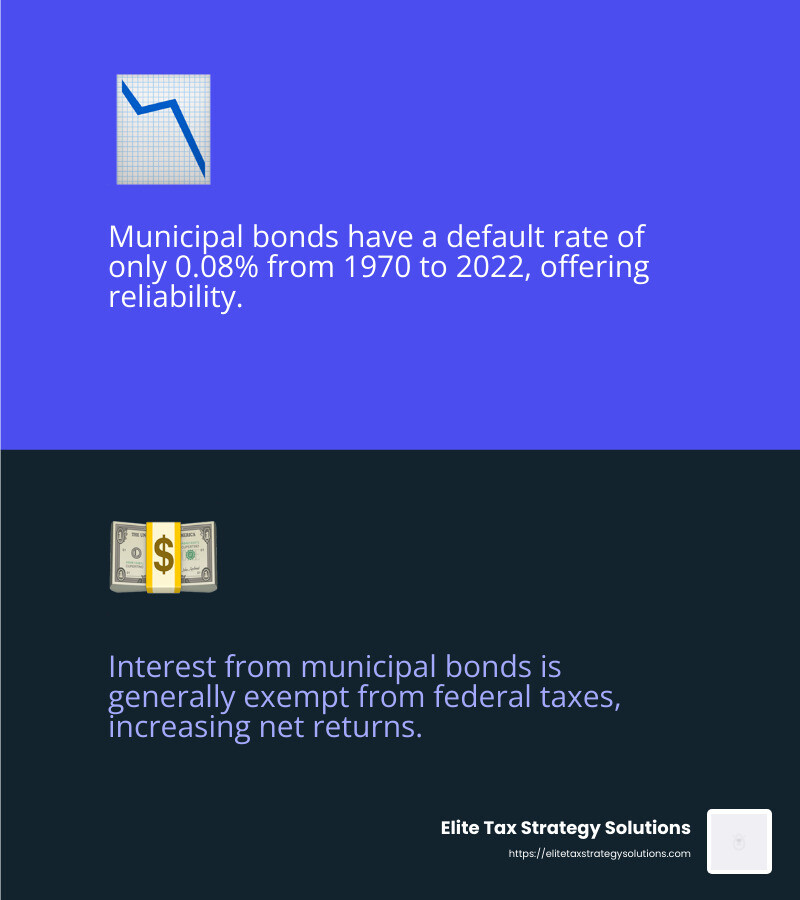

Municipal Bonds

Municipal bonds, or “munis,” are an attractive option for tax-conscious investors. These bonds are issued by local governments to fund public projects like schools and roads.

Why Consider Munis?

The interest income from municipal bonds is generally exempt from federal taxes. If you live in the state where the bond is issued, you might also avoid state and local taxes.

Example: If you’re in a high tax bracket, the tax-equivalent yield of a muni bond could be higher than that of a taxable bond. This can increase your overall return.

Note: Be aware of exceptions like the “de minimis” tax if you buy bonds at a discount. This could affect their tax-free status.

Capital Gains Management

Managing capital gains is crucial for minimizing taxes on your investments. Here’s how you can do it:

Hold for the Long Term

Assets held for more than a year are taxed at lower capital gains rates (0%, 15%, or 20%) compared to short-term gains, which are taxed as ordinary income.

Example: For married couples filing jointly, the zero-rate bracket for long-term capital gains applies to taxable income up to $94,050 in 2024.

Tax-Loss Harvesting

This involves selling investments at a loss to offset gains. You can use up to $3,000 of net capital losses to reduce other income each year and carry forward any excess to future years.

Tip: Be mindful of the wash-sale rule, which disallows a loss if you buy a substantially identical security within 30 days of the sale.

Tax-Efficient Investing

Tax-efficient investing aims to minimize taxes on your investment returns. Here’s how you can do it:

Choose the Right Accounts

Place tax-efficient investments in taxable accounts and tax-inefficient ones (like bonds or REITs) in tax-advantaged accounts like IRAs.

Consider Index Funds

Index funds typically have lower turnover rates, resulting in fewer taxable events. This can help reduce your tax bill.

Reminder: Always stay informed about tax law changes, as they can impact your investment strategy.

By focusing on tax-efficient investments, you can optimize your portfolio and improve your financial well-being. Next, we’ll look at how Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) can help you save on healthcare costs.

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs)

Healthcare costs can add up quickly, but tax savings strategies like HSAs and FSAs offer a way to manage these expenses while saving on taxes.

Health Savings Accounts (HSAs)

What is an HSA?

An HSA is a savings account that lets you set aside pre-tax money for medical expenses. It’s available to those with high-deductible health plans (HDHPs).

Key Benefits

– Triple Tax Advantage: Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free.

– Rollover Funds: Unlike FSAs, HSA funds roll over year to year, so you can save for future healthcare costs.

Eligibility and Contribution Limits

To qualify, you need a high-deductible plan. For 2024, the deductible must be at least $1,600 for individuals or $3,200 for families. You can contribute up to $4,150 for individuals or $8,300 for families.

Tip: You can make contributions up until tax filing day of the following year and still get the deduction for the current year.

Flexible Spending Accounts (FSAs)

What is an FSA?

FSAs are employer-sponsored accounts where you can contribute pre-tax dollars to pay for out-of-pocket healthcare expenses.

Key Points

– Use-It-or-Lose-It Rule: Generally, FSA funds must be used within the plan year. Some employers allow a rollover of up to $640 for 2024 or a 2.5-month grace period.

– Contribution Limits: Contribution limits are set by your employer, but the IRS caps them annually.

Example: If you have an FSA balance, plan your healthcare spending to use up those funds. Check if you can get reimbursed for expenses paid earlier in the year.

Choosing Between HSAs and FSAs

- HSAs are great for saving long-term due to rollover benefits and investment options.

- FSAs can be useful for predictable, short-term healthcare expenses.

Note: You can’t contribute to both an HSA and a general-purpose FSA. However, a “limited purpose” FSA, which covers only dental and vision expenses, can be paired with an HSA.

By leveraging HSAs and FSAs, you can manage healthcare costs efficiently and save on taxes. Next, we’ll explore estate and gift tax planning to help protect your wealth for future generations.

Estate and Gift Tax Planning

Estate and gift tax planning is crucial for protecting your wealth and ensuring a smooth transfer to your heirs. Let’s explore some tax savings strategies that can help you manage these taxes effectively.

Estate Planning Strategies

Why Plan Your Estate?

Estate planning helps you control how your assets are distributed after your death. It also minimizes the taxes your heirs might have to pay.

Key Strategies

– Wills and Trusts: A will specifies how your assets are distributed, while trusts can help manage estate taxes. Trusts can also provide for minor children or special needs dependents.

– Gifting: Giving away assets during your lifetime can reduce the size of your estate. This can help lower potential estate taxes.

Example: If you own a family business, setting up a trust can ensure its smooth transition while minimizing taxes.

Gift Tax Exemption

What is the Gift Tax Exemption?

The gift tax exemption allows you to give a certain amount of money or assets each year without paying taxes.

Annual and Lifetime Limits

– Annual Exclusion: For 2024, you can give up to $17,000 per person without triggering gift taxes.

– Lifetime Exemption: The lifetime exemption is $12.92 million in 2024. This amount is the total you can give away during your lifetime without incurring gift taxes.

Tip: Use the annual exclusion to make tax-free gifts to multiple people, reducing your estate’s size over time.

Life Insurance

How Can Life Insurance Help?

Life insurance can provide liquidity to pay estate taxes, ensuring that your heirs don’t have to sell assets to cover tax bills.

Smart Uses of Life Insurance

– Estate Liquidity: The death benefit from a life insurance policy can cover estate taxes and other expenses.

– Tax-Free Payouts: Properly structured, life insurance proceeds are generally free from income and estate taxes.

Case Study: A family with significant real estate holdings used life insurance to cover estate taxes, allowing them to keep the properties intact.

By incorporating estate planning strategies, utilizing gift tax exemptions, and leveraging life insurance, you can effectively manage estate and gift taxes. These steps help ensure that your wealth is preserved for future generations. Next, we’ll address some frequently asked questions about tax savings strategies.

Frequently Asked Questions about Tax Savings Strategies

How can I decrease my taxable income?

Decreasing your taxable income can be achieved through a few smart tax savings strategies. One effective method is contributing to retirement accounts. By maximizing your contributions to 401(k) plans or IRAs, you can reduce your taxable income while saving for the future.

Another way to lower taxable income is through financial gifts. You can take advantage of the annual gift tax exemption to make tax-free gifts, reducing your estate size and potentially lowering future estate taxes.

What are some tax-saving strategies for high-income earners?

High-income earners have several options to reduce their tax burden. Investing in municipal bonds is a popular choice since the interest income from these bonds is generally exempt from federal taxes. If you live in the state where the bond is issued, you might also avoid state and local taxes.

Advanced investment strategies, like tax-loss harvesting, can also be beneficial. This involves selling underperforming investments to offset capital gains from other investments.

How do LLC owners avoid taxes?

LLC owners can reduce their tax liability by choosing the right business structure. Many LLCs opt for a pass-through entity status, where the income is reported on the owner’s personal tax return, potentially lowering the overall tax rate.

Alternatively, LLCs can elect to be taxed as an S Corporation. This structure allows owners to pay themselves a salary and distribute the remaining profits as dividends, which may be taxed at a lower rate. This strategy can help minimize self-employment taxes.

By understanding these strategies and choosing the right approach, individuals and business owners can effectively manage their tax liabilities.

Conclusion

In the changing world of taxes, having a solid plan is key to maintaining financial stability. At Elite Tax Strategy Solutions, we focus on providing personalized tax planning custom to your unique needs. Our goal is to help you maximize your tax savings and achieve long-term financial stability.

Our proactive approach involves staying ahead of tax law changes and identifying the best strategies to optimize your tax position. Whether you’re a high-income earner or a small business owner, our team is dedicated to helping you steer the complexities of tax regulations with ease.

By integrating tax planning with your broader financial goals, we ensure that your tax strategy aligns with your aspirations. This means not just looking at taxes in isolation but as a part of your overall financial strategy. From retirement planning to estate management, our comprehensive services cover every aspect of your financial journey.

For more information on how we can assist you with your tax planning needs, visit our Comprehensive Financial Planning page. Let us help you take control of your financial future with confidence and clarity.