In the complex world of taxation, navigating tax savings for high earners can be daunting. If you’re a high-income individual seeking to lower your tax burden, here are some essential strategies:

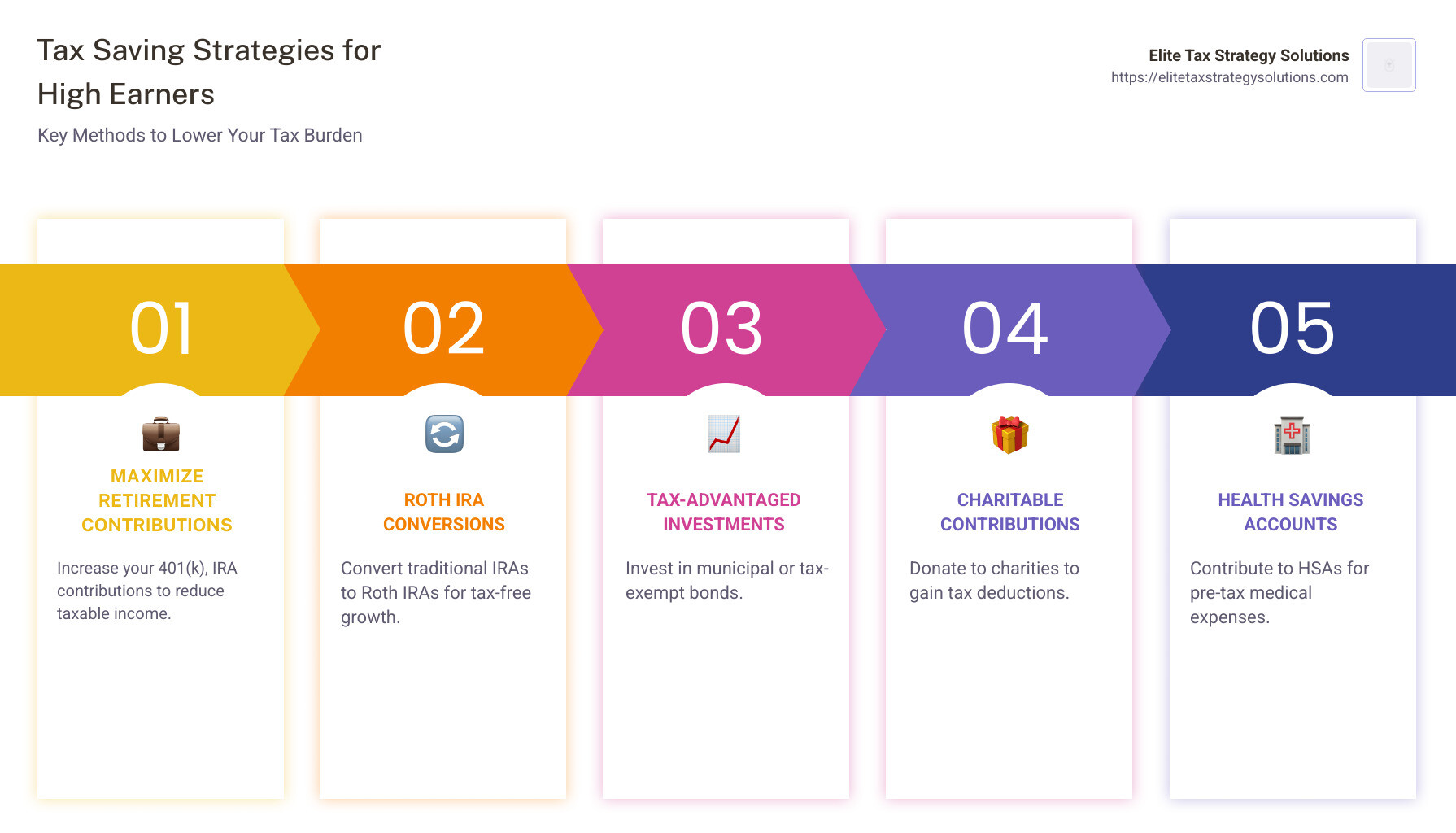

- Maximize Retirement Contributions: Leverage your 401(k), IRA, or other retirement accounts.

- Consider Roth IRA Conversions: Benefit from tax-free growth.

- Explore Tax-Advantaged Investments: Look into municipal bonds or tax-exempt bonds.

- Use Charitable Contributions: Deduct eligible donations to reduce taxable income.

- Use Health Savings Accounts (HSAs): Save pre-tax dollars for medical expenses.

Understanding tax savings for high earners is crucial for optimizing your financial outcomes while ensuring compliance with evolving tax regulations. This guide aims to simplify the process and provide actionable strategies to make the most of your income.

I’m David Fritch, a seasoned tax professional with decades of experience in tax planning and advising high earners on maximizing their tax savings. My background in navigating tax codes allows me to provide valuable insights into simplifying the complex field of taxation for high-income individuals.

Easy tax savings for high earners word list:

– benefits of tax planning

– business tax savings strategies

– proactive tax planning opportunities

Maximize Retirement Contributions

Retirement accounts are a powerhouse for tax savings for high earners. By contributing to plans like 401(k), 403(b), or SIMPLE IRA, you can significantly reduce your taxable income. Let’s break down how you can make the most of these opportunities:

401(k) and 403(b) Plans

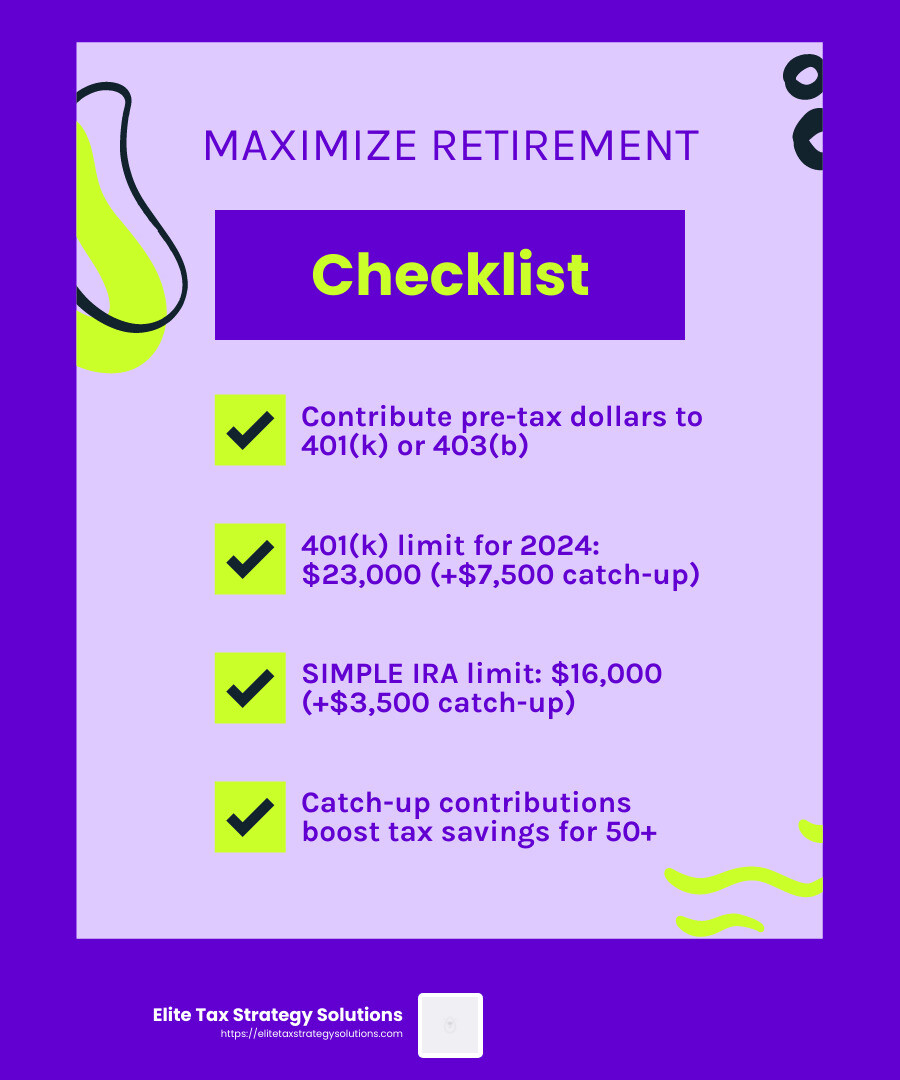

These employer-sponsored retirement plans allow you to contribute pre-tax dollars, which means the money you save isn’t taxed until you withdraw it in retirement. For 2024, you can contribute up to $23,000. If you’re over 50, you can add an extra $7,500 as a catch-up contribution.

Why does this matter? If you’re earning $150,000 and max out your 401(k) contributions, you’ll only be taxed on $127,000. This can make a big difference in your tax bracket and overall tax bill.

SIMPLE IRA

For those with access to a SIMPLE IRA, the contribution limit is $16,000 for 2024. If you’re over 50, you can add an additional $3,500 in catch-up contributions. While these plans have lower contribution limits than 401(k)s, they still offer a great way to reduce taxable income.

Catch-Up Contributions

If you’re 50 or older, catch-up contributions are a fantastic way to boost your retirement savings while enjoying additional tax benefits. For 401(k) and 403(b) plans, you can contribute an extra $7,500. SIMPLE IRAs allow an additional $3,500.

Pro Tip: Always aim to contribute at least enough to get the full employer match in your 401(k) or 403(b). It’s essentially free money and boosts your retirement savings.

By maximizing your retirement contributions, you’re not just saving for the future; you’re also strategically reducing your current tax burden. This approach is a cornerstone of effective tax planning for high earners.

Roth IRA Conversions

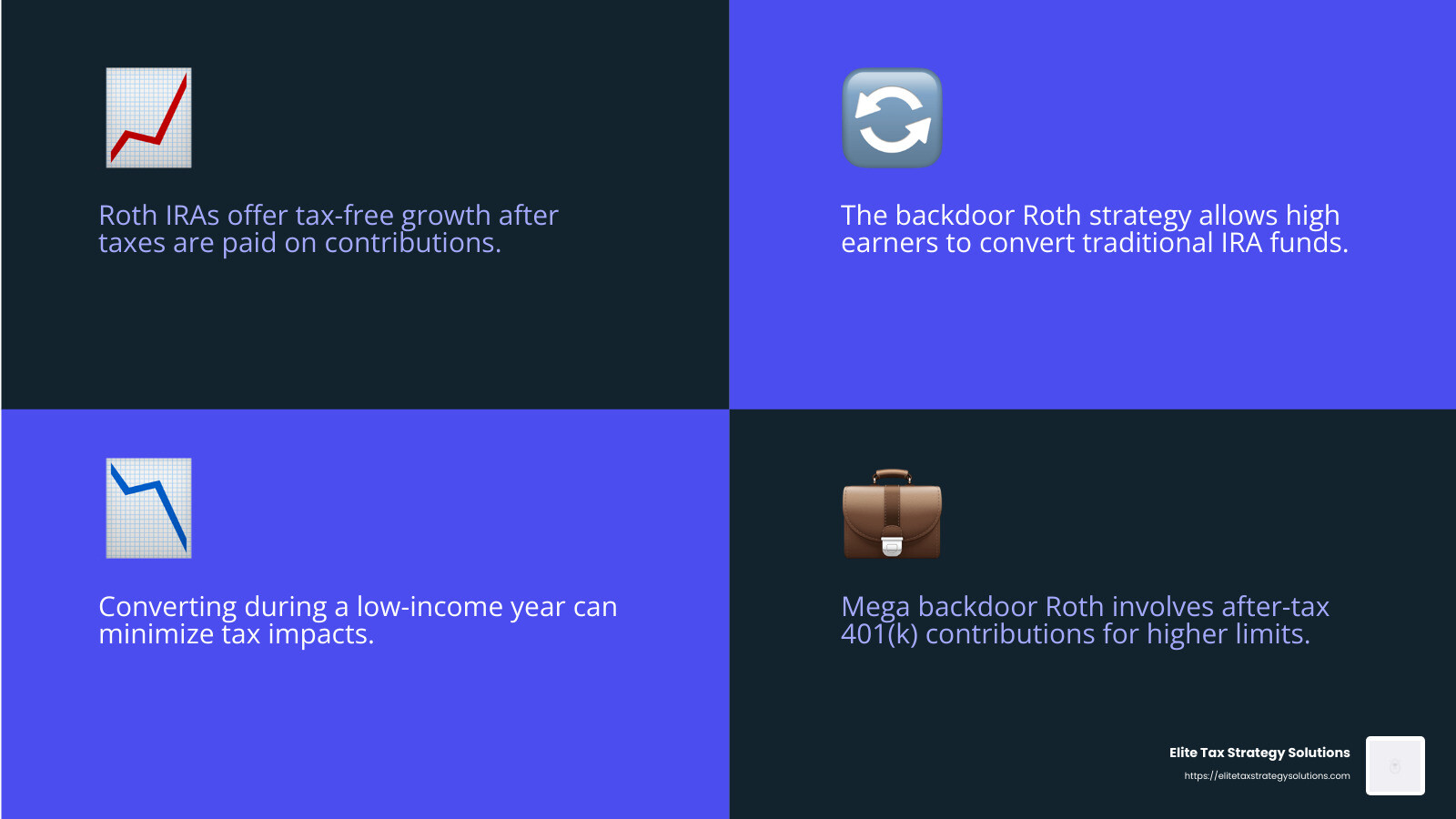

Roth IRAs are a powerful tool for tax savings for high earners. They offer the unique advantage of tax-free growth. This means that once you’ve paid taxes on the money you contribute, any growth in the account is tax-free when you withdraw it in retirement.

Why Consider a Roth IRA Conversion?

For high-income earners, a direct contribution to a Roth IRA might not be possible due to income limits. However, there’s a workaround: the Roth IRA conversion strategy. This involves converting a traditional IRA into a Roth IRA, allowing you to enjoy tax-free growth on your investments.

Imagine you’ve been diligently saving in a traditional IRA, and now you’re considering the benefits of a Roth. By converting, you pay taxes on the converted amount now, but you won’t have to worry about taxes on the earnings later. This can be particularly advantageous if you expect to be in a higher tax bracket in the future.

When to Convert?

Timing is key. Consider converting during a year when your income is lower than usual, such as during a career transition or after retirement. This can help minimize the tax impact of the conversion.

Another strategic time to convert is when the market is down. Lower account values mean a smaller tax bill at conversion, and you can potentially benefit from tax-free growth when the market rebounds.

The Backdoor Roth IRA Strategy

For those who earn too much to contribute directly to a Roth IRA, the backdoor Roth IRA strategy is a popular choice. This involves making non-deductible contributions to a traditional IRA and then converting those contributions to a Roth IRA.

Important Note: Be aware of the pro-rata rule, which requires you to consider all your traditional IRA balances when calculating taxes on a conversion. This means you may owe taxes on a portion of the conversion if you have other pre-tax IRA funds.

The Mega Backdoor Roth

If you’re fortunate enough to have access to a 401(k) plan that allows after-tax contributions, you might be able to take advantage of the mega backdoor Roth strategy. This involves contributing after-tax dollars to your 401(k) and then rolling them over to a Roth IRA. This can significantly boost your Roth savings.

By understanding and implementing these Roth IRA conversion strategies, high earners can optimize their tax planning and secure a more tax-efficient retirement.

Tax Savings for High Earners: Investment Strategies

Investing wisely can lead to significant tax savings for high earners. Let’s explore some key strategies involving municipal bonds, tax-exempt bonds, and dividend-paying companies.

Municipal Bonds

Municipal bonds, or “munis,” are issued by local governments to fund public projects like schools and roads. The big perk? The interest earned is generally free from federal income tax. If you live in the state where the bond is issued, you might also dodge state and local taxes.

For high-income earners, this can mean substantial savings. Imagine you’re in a high tax bracket; the tax-equivalent yield of a muni can be much more appealing than taxable bonds. Plus, municipal bonds have a lower default rate compared to corporate bonds, making them a safer investment.

Tax-Exempt Bonds

Tax-exempt bonds, similar to munis, offer interest income that’s not subject to federal taxes. These can be a great addition to an investment portfolio for those looking to reduce taxable income.

When considering these bonds, not all are created equal. Some may still be subject to alternative minimum tax (AMT), so it’s crucial to check the specifics of each bond.

Dividend-Paying Companies

Investing in dividend-paying companies can also be a smart move for tax savings. Qualified dividends are taxed at the lower capital gains tax rates, which are typically 0%, 15%, or 20%, depending on your income level. This is often lower than the rates on ordinary income.

High earners can benefit by focusing on companies with a history of paying and increasing dividends. This not only provides a steady income stream but also takes advantage of favorable tax treatment.

Putting It All Together

Combining these strategies can optimize your investment portfolio and maximize tax savings. For instance, a balanced mix of municipal bonds and dividend-paying stocks can provide both regular income and tax benefits.

Always remember, the key to successful tax planning is understanding the tax implications of your investments. Regularly reviewing and adjusting your strategy with a financial advisor can ensure you’re making the most of these opportunities.

Next, we’ll dive into how charitable contributions and donor-advised funds can further improve your tax strategy.

Charitable Contributions and Donor-Advised Funds

Charitable giving is not just a way to support causes you care about; it’s also a smart strategy for tax savings for high earners. Let’s explore how charitable contributions and donor-advised funds can maximize your tax deductions.

Charitable Donations

When you make a charitable donation, you can often deduct the amount from your taxable income. This is especially beneficial for high earners who itemize deductions on their tax returns. The IRS allows you to deduct cash donations up to 60% of your adjusted gross income (AGI).

Here’s a quick example: If your AGI is $500,000, you could potentially deduct up to $300,000 in charitable donations. This significant deduction can greatly lower your taxable income and, consequently, your tax bill.

Donor-Advised Funds

A donor-advised fund (DAF) is like a personal charitable savings account. You contribute money to the fund, receive an immediate tax deduction, and then decide over time which charities will receive the money.

Imagine putting $100,000 into a DAF. You get a $100,000 tax deduction in the year you contribute, even if you distribute the funds to charities over several years. This is a fantastic option if you have a year with unusually high income, like from a bonus or inheritance, and want to offset that income with a large deduction.

Moreover, the money in a DAF can be invested and grow tax-free, potentially increasing the amount you can eventually donate.

Comparing to Private Foundations

For those with significant wealth, creating a private family foundation is another option. While similar to a DAF in offering tax deductions, a private foundation gives you more control over the funds and allows family involvement. However, it also comes with more administrative responsibilities.

Making the Most of Charitable Giving

To maximize your tax benefits from charitable giving:

- Plan Ahead: Consider your income and potential deductions for the year.

- Choose the Right Vehicle: Decide between direct donations, DAFs, or a private foundation based on your goals and financial situation.

- Consult a Tax Professional: They can help you steer the complexities and ensure you’re maximizing your deductions.

By strategically using charitable contributions and donor-advised funds, high earners can significantly reduce their tax burden while supporting the causes they care about.

Next, we’ll explore how Health Savings Accounts (HSAs) can further improve your tax strategy.

Health Savings Accounts (HSAs)

Health Savings Accounts (HSAs) are a fantastic tool for tax savings for high earners. They offer a triple tax advantage that can make a significant difference in your financial planning.

HSA Contributions

To contribute to an HSA, you must be enrolled in a high-deductible health plan (HDHP). For 2024, the minimum deductible for an individual is $1,600, and for a family, it’s $3,200. The maximum contribution limits are $4,150 for individuals and $8,300 for families, with an additional $1,000 catch-up contribution if you’re 55 or older.

Why contribute to an HSA?

-

Tax Deduction: Contributions to an HSA are tax-deductible, lowering your taxable income for the year. This is true even if you don’t itemize deductions on your tax return.

-

Employer Contributions: If your employer contributes to your HSA, those funds are not counted as taxable income.

Tax-Free Withdrawals

The funds in your HSA grow tax-free and can be withdrawn tax-free for qualified medical expenses. This includes a wide range of expenses like doctor visits, prescription medications, and even some over-the-counter items.

Consider this: If you contribute to an HSA for several years and invest the funds, you could build a substantial balance. When you need to pay for medical expenses, you can withdraw from your HSA without paying any taxes on the growth.

High-Deductible Plans

While HDHPs have higher out-of-pocket costs, they often come with lower premiums. This can be beneficial if you’re generally healthy and don’t expect frequent medical expenses.

Balancing the Risks and Rewards:

- Risk: Higher deductibles mean you’ll pay more out-of-pocket before insurance kicks in.

- Reward: Lower premiums and the ability to contribute to an HSA, which offers tax savings and long-term growth potential.

Strategic Use of HSAs

For high-income earners, an HSA can be a powerful part of a broader tax strategy. Here’s how to make the most of it:

-

Maximize Contributions: Contribute the maximum allowed each year to take full advantage of the tax deduction.

-

Invest the Funds: If you don’t need to use the funds immediately, consider investing them. This allows your HSA to grow tax-free over time.

-

Plan for Retirement: After age 65, you can use HSA funds for non-medical expenses without a penalty, though you’ll pay income tax on those withdrawals. This makes an HSA a versatile tool for retirement planning.

HSAs provide both immediate and long-term tax benefits, making them an excellent choice for high earners looking to reduce their tax burden while planning for future healthcare costs.

Next, we’ll dive into tax residency planning and how it can impact your overall tax strategy.

Tax Residency Planning

Tax residency can have a big impact on your tax bill, especially if you live in a high-tax state like California or New York. Understanding tax residency rules can help you save money and manage your taxes more effectively.

State Income Tax

Each state has its own income tax rates, and they can vary widely. Some states, like Texas and Florida, have no state income tax, while others have high rates. If you’re a high earner, moving to a state with no income tax can save you a lot of money.

States with No Income Tax:

- Florida

- Texas

- Nevada

- Washington

However, it’s not just about moving. You need to establish tax residency in the new state, which involves meeting specific residency requirements.

Residency Requirements

Most states use the “183-day rule” to determine residency. This means you need to live in the state for at least 183 days to be considered a resident. But it’s not just about counting days. You also need to show ties to the state, like:

- Registering to vote

- Getting a state driver’s license

- Changing your address on financial accounts

Case Example:

Imagine Jane, a high-income earner from New York, who decides to move to Florida. She needs to spend at least 183 days in Florida and establish ties there to avoid New York taxes. This might include buying a home or renting long-term, registering her car in Florida, and updating her mailing address.

Tax Residency Challenges

Be careful! Some states, like California, are known for aggressively pursuing taxes from former residents. They might audit your tax return to ensure you’re not trying to dodge taxes by claiming residency in a low-tax state.

Key Tip:

Keep detailed records of your days spent in each state and any documents that show your intent to make a new state your home. This can protect you if your residency status is questioned.

Tax Planning with Residency

Planning your residency can be a smart way to reduce your tax burden. But remember, it’s not just about taxes. Consider the overall cost of living, lifestyle, and family needs before making a move.

Working with a tax professional can help you steer the complexities of tax residency and ensure you’re meeting all requirements. This is especially important if you have income from multiple states or work remotely.

Next, we’ll explore tax savings strategies for business owners, including how choosing the right business structure can impact your taxes.

Tax Savings for High Earners: Business Strategies

For high-income earners, especially those owning businesses, choosing the right business structure can be crucial for tax savings. Let’s explore some strategies that can make a significant difference.

Business Structure

The type of business entity you choose affects how your income is taxed. Here are a few common structures:

- Sole Proprietorship: Simple to set up, but income is taxed at your personal rate.

- Partnership: Income is passed through to partners and taxed at their individual rates.

- C Corporation: Offers limited liability, but income is taxed at both corporate and personal levels.

- S Corporation: Combines benefits of a corporation with pass-through taxation.

Choosing the right structure can help reduce your tax burden. For instance, an S Corporation might be beneficial for high earners.

S-Corp Benefits

An S Corporation provides pass-through taxation, meaning the business itself isn’t taxed. Instead, income is reported on the owners’ personal tax returns. This avoids double taxation seen in C Corporations.

Key Advantages:

- Pass-Through Taxation: Only taxed once at the individual level.

- Self-Employment Tax Savings: Only your salary (not distributions) is subject to self-employment tax.

- Qualified Business Income Deduction: You may qualify for a 20% deduction on business income, depending on your total income and other factors.

Example:

Consider Alex, a high-income earner running a consulting firm. By electing S-Corp status, Alex can pay themselves a reasonable salary and take additional profits as distributions. This reduces their self-employment tax liability compared to being a sole proprietor.

Pass-Through Entities

Pass-through entities, like partnerships and S-Corps, allow income to “pass through” to owners, who pay taxes at their individual rates. This can be advantageous for high-income earners, as it may result in lower overall taxes compared to a C Corporation.

Why Choose a Pass-Through Entity?

- Simplified Taxation: Avoids the complexity of corporate tax returns.

- Flexibility in Income Distribution: Owners can decide how to allocate income and losses.

- Potential Tax Deductions: Access to deductions and credits that might not be available to C Corporations.

Fact:

According to the IRS, pass-through entities account for more than 95% of U.S. businesses, highlighting their popularity among business owners.

Choosing the Right Structure

Selecting the right business structure is a strategic decision. It can impact your tax liabilities, personal liability, and even your ability to raise capital. Consulting with a tax professional can help tailor your business setup to maximize tax savings and align with your financial goals.

In the next section, we’ll answer frequently asked questions about tax savings strategies for high earners.

Frequently Asked Questions about Tax Savings for High Earners

How do high wage earners reduce taxes?

High wage earners have several strategies at their disposal to reduce taxes. The most common approach is maximizing retirement plan contributions. By contributing to plans like 401(k)s, you reduce your pre-tax income, effectively lowering the amount of income subject to taxation. For 2024, you can contribute up to $23,000 to a Traditional 401(k), and even more if you’re over 50.

Another tactic is utilizing Health Savings Accounts (HSAs). Contributions to HSAs are tax-deductible, and withdrawals for qualified medical expenses are tax-free. This dual benefit can significantly reduce taxable income.

How to avoid 32% tax bracket?

Avoiding a higher tax bracket, like the 32% bracket, requires careful income management. One method is to strategically time your income. For instance, if you’re close to the 32% threshold, consider deferring bonuses or income to the following year.

Strategic asset sales can also help. If you have investments, consider selling assets that have decreased in value to offset gains, a practice known as tax-loss harvesting. This can help manage your capital gains and keep you in a lower tax bracket.

What is the extra tax for high-income earners?

High-income earners face an additional Medicare tax of 0.9% on wages and self-employment income above certain thresholds. For single filers, this kicks in at $200,000, while for married couples filing jointly, it starts at $250,000.

Understanding income thresholds is crucial. By keeping your income below these thresholds through strategic planning, you can avoid additional taxes. For example, contributing more to your retirement accounts or utilizing deferred compensation plans can help keep your taxable income below these limits.

These strategies not only reduce the amount you owe but also align with long-term financial goals. In the next section, we will explore charitable contributions and donor-advised funds as additional tax-saving strategies.

Conclusion

Navigating the complex world of taxes can be daunting, especially for high earners. But with the right strategies, you can achieve significant tax savings for high earners while securing your financial future.

At Elite Tax Strategy Solutions, we specialize in proactive tax planning custom to your unique financial situation. Our approach focuses not just on minimizing your current tax burden but also on ensuring long-term financial stability. We understand the intricacies of tax codes and leverage them to your advantage, whether through maximizing retirement contributions, optimizing investment strategies, or strategic tax residency planning.

Our team of seasoned professionals in Jasper, Indiana, and suburban areas near major cities, is dedicated to providing personalized guidance. We aim to align your tax strategy with your broader financial goals, ensuring a seamless integration that supports your aspirations.

With Elite Tax Strategy Solutions, you’re not just getting a service—you’re gaining a partner committed to your financial success. For more information on how we can help you steer the complexities of tax planning and maximize your savings, visit our Innovative Tax Planning page.

Let us help you take control of your taxes and secure a brighter financial future.