Tax saving techniques can be a powerful way for high-income earners and small business owners to keep more of their hard-earned money. If you’re looking for strategies to reduce your tax bill, consider these key techniques:

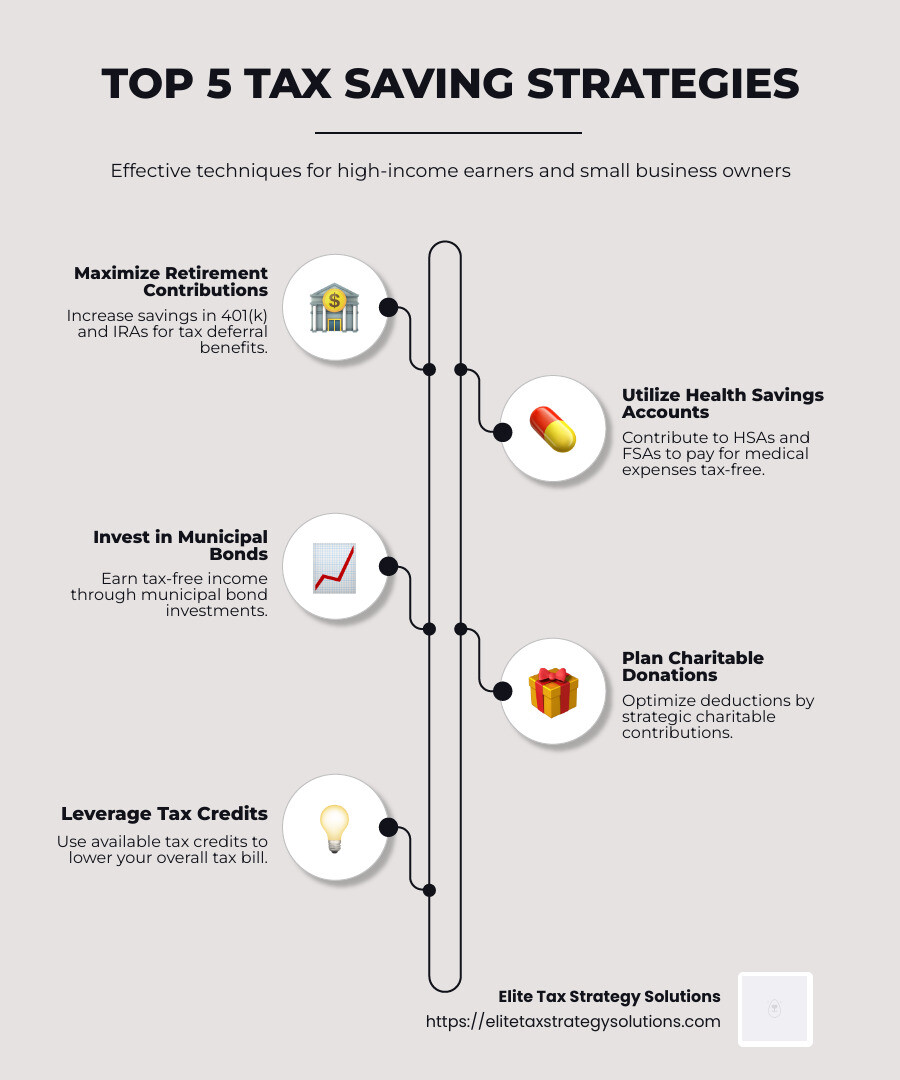

- Maximize contributions to retirement accounts

- Take advantage of health savings and flexible spending accounts

- Consider municipal bonds for tax-free income

- Plan charitable contributions to optimize deductions

- Use tax credits effectively

A wealth of strategies exists, each offering different benefits. The right approach depends on your financial situation and goals.

Now, allow me to introduce myself. I’m David Fritch, with over four decades of experience as a CPA and in handling tax saving techniques for high earners and small business owners. I believe tax planning is more than just filing returns; it’s about a proactive strategy to improve your financial well-being.

Tax saving techniques basics:

– deduction optimization

– tax liability reduction

– tax planning for businesses

Maximize Retirement Contributions

Saving for retirement isn’t just about securing your future; it’s also a smart tax saving technique. By maximizing contributions to retirement accounts, you can significantly reduce your taxable income today.

401(k) and Catch-Up Contributions

401(k) plans are a popular way to save for retirement because they offer tax advantages. Contributions are made with pre-tax dollars, which lowers your taxable income for the year. In 2024, you can contribute up to $23,000 to your 401(k). If you’re 50 or older, take advantage of catch-up contributions by adding an extra $7,500. This means you can contribute a total of $30,500, helping you save more and reduce your tax bill.

Roth IRA for Future Tax Benefits

While a Roth IRA doesn’t offer an immediate tax break, it provides tax-free withdrawals in retirement. This can be beneficial if you expect to be in a higher tax bracket later. If your income is too high to contribute directly to a Roth IRA, consider a Roth conversion. This involves converting a traditional IRA to a Roth IRA, allowing you to enjoy those tax-free benefits in retirement.

Self-Employed Retirement Plans

If you’re self-employed or a small business owner, you have even more options. Consider setting up a SEP IRA or a SIMPLE IRA. These plans allow you to contribute a significant portion of your income, reducing your taxable income while building your retirement savings.

Employer Matching Contributions

Don’t leave free money on the table! If your employer offers a matching contribution, make sure to contribute enough to get the full match. This not only boosts your retirement savings but also maximizes the tax advantages of your 401(k).

Maximizing your retirement contributions is a win-win strategy. You lower your taxable income now and build a solid financial foundation for your future. Next, let’s explore how optimizing health savings can further improve your tax strategy.

Optimize Health Savings

When it comes to tax saving techniques, optimizing your health savings can be a game-changer. Both Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) offer ways to save on taxes while managing medical expenses.

Health Savings Accounts (HSAs)

HSAs are a powerful tool for those with high-deductible health plans. They allow you to contribute pre-tax dollars, reducing your taxable income. In 2025, individuals can contribute up to $4,300, while families can contribute up to $8,550. One of the biggest advantages of an HSA is that the funds roll over year to year—you won’t lose what you don’t use.

Moreover, HSAs can earn interest, and you can even invest these funds, making them an additional source of retirement savings. Plus, you can use HSA funds for qualified medical expenses tax-free.

Flexible Spending Accounts (FSAs)

FSAs are another way to save on medical expenses, although they come with different rules. FSAs must be sponsored by an employer, and you need to decide how much to contribute at the start of the year. Unlike HSAs, FSAs generally require you to use the funds within the plan year, or you risk losing them.

However, some employers offer options to roll over up to $640 or provide a grace period of 2½ months to spend the remaining funds. FSAs can cover both healthcare and childcare expenses, giving you flexibility in how you use the funds.

Strategic Use of Medical Expenses

Both HSAs and FSAs allow you to pay for out-of-pocket medical expenses with pre-tax money. This can convert nondeductible expenses into deductible ones, effectively lowering your taxable income. If you expect significant medical expenses, consider maximizing your contributions to these accounts.

In summary, optimizing health savings not only helps you manage medical costs but also provides substantial tax benefits. Whether you choose an HSA or FSA, these accounts are integral to a savvy tax-saving strategy. Now, let’s dig into how you can apply tax saving techniques to your investments.

Tax Saving Techniques for Investments

Investments are a powerful avenue for saving on taxes. By choosing the right strategies, you can keep more of your money working for you. Let’s explore three key tax saving techniques for investments: municipal bonds, long-term capital gains, and tax-loss harvesting.

Municipal Bonds

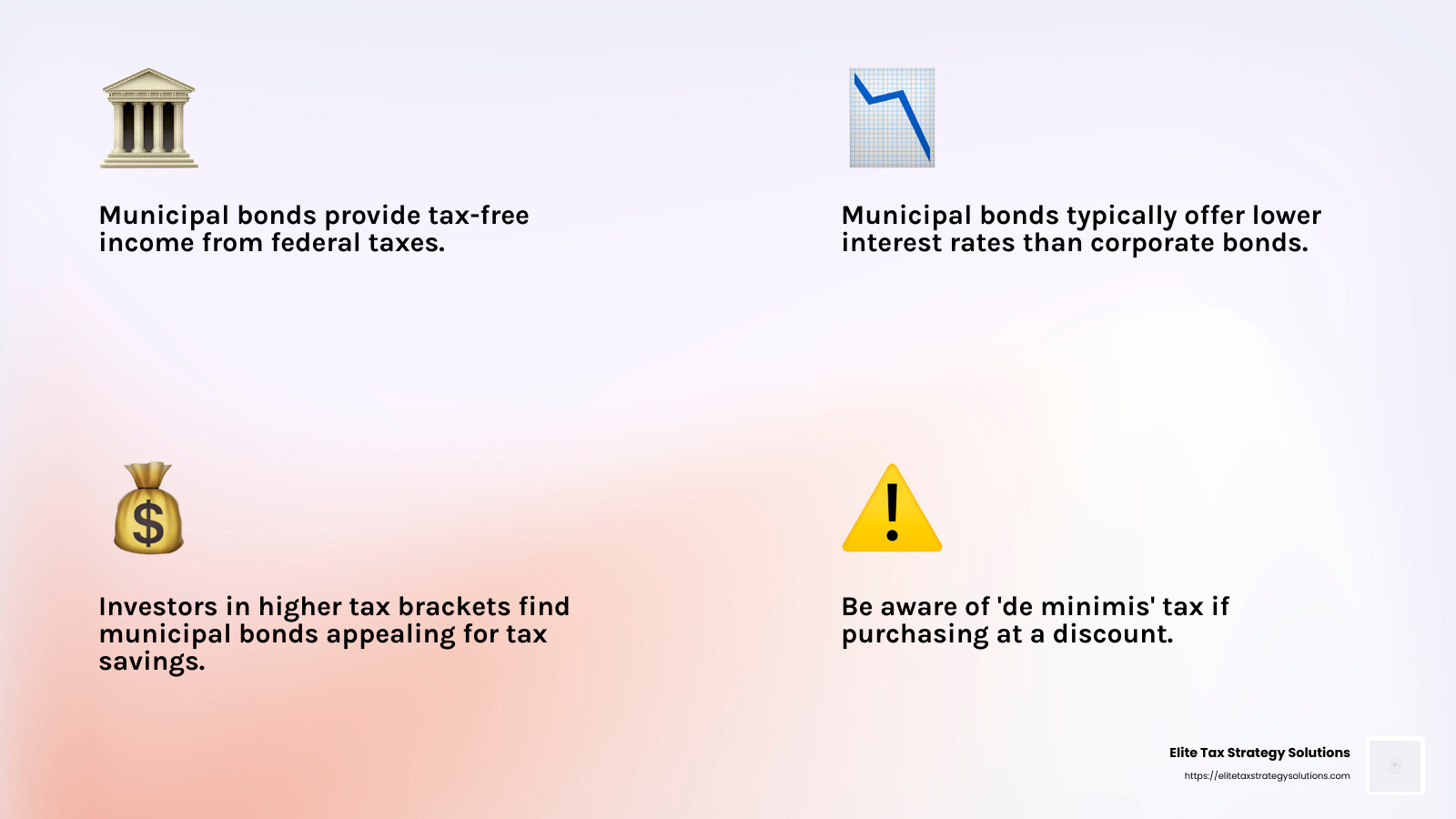

Municipal bonds, or “munis,” are debt securities issued by local governments to fund public projects. The standout feature of these bonds is that the interest income they generate is generally exempt from federal taxes. If you live in the state or locality where the bond is issued, you might also avoid state and local taxes.

This tax-free income makes municipal bonds particularly attractive to investors in higher tax brackets. While they typically offer lower interest rates compared to corporate bonds, their tax-equivalent yield can be quite appealing when you factor in the tax savings.

However, be aware of exceptions. If you purchase a muni bond at a discount, a “de minimis” tax may apply, taxing the interest and gains from the discounted amount as regular income.

Long-Term Capital Gains

Holding investments for more than a year can lead to significant tax savings due to the favorable tax rates on long-term capital gains. Depending on your income level, these gains are taxed at 0%, 15%, or 20%, which is usually lower than the rates for short-term gains.

For example, in 2024, married couples filing jointly can enjoy a 0% tax rate on long-term capital gains if their taxable income is up to $94,050. This threshold increases to $96,700 in 2025. Understanding these brackets can help you plan when to sell your investments to maximize your tax savings.

Tax-Loss Harvesting

Tax-loss harvesting is a strategy that involves selling securities at a loss to offset capital gains tax liabilities. If your capital losses exceed your capital gains, you can use up to $3,000 of the excess loss to reduce other taxable income. Any losses beyond this can be carried forward to future tax years.

This technique is particularly useful in taxable accounts, as it helps mitigate the tax impact of capital gains. However, be careful of the wash-sale rule, which disallows the tax deduction if you buy the same or a “substantially identical” security within 30 days before or after the sale.

In summary, leveraging these tax saving techniques can make a significant difference in your investment returns. By investing in municipal bonds, focusing on long-term capital gains, and employing tax-loss harvesting, you can effectively reduce your tax burden and improve your financial growth. Next, we’ll explore how charitable contributions and gifting can further optimize your tax savings strategy.

Charitable Contributions and Gifting

Charitable contributions and gifting are not just acts of kindness—they’re smart tax saving techniques that can reduce your tax bill while supporting causes you care about.

Charitable Donations

When you donate to qualified charities, you can deduct cash contributions up to 60% of your adjusted gross income (AGI). But here’s a savvy tip: donate appreciated long-term investments instead. Why? You avoid paying capital gains tax on the appreciation and still get a deduction for the full market value of the donation, up to 30% of your AGI.

Imagine you bought stock for $1,000, and now it’s worth $5,000. If you donate the stock, you skip the $4,000 capital gain and deduct $5,000 from your taxes. Nice, right?

Qualified Charitable Distribution (QCD)

For those aged 70½ or older, a Qualified Charitable Distribution (QCD) is another powerful tool. You can donate up to $105,000 directly from your IRA to a charity. This counts towards your required minimum distribution (RMD) but isn’t taxed as income. It’s a win-win: you meet your RMD requirement and lower your taxable income, all while helping your favorite charity.

Tax-Free Gifts

In 2024, you can gift up to $18,000 per person, tax-free, without affecting your lifetime estate and gift tax exemption. If you’re married, that amount doubles to $36,000. This is a strategic way to transfer wealth to family or friends without worrying about taxes.

While these gifts won’t reduce your taxable income, they help manage your estate tax exposure and offer a way to support loved ones financially.

Incorporating charitable donations, QCDs, and tax-free gifts into your financial strategy not only supports your community and loved ones but also optimizes your tax savings. These techniques can be custom to fit your unique situation and help achieve your long-term financial goals.

Next, let’s dig into tax planning for future changes to ensure you stay ahead of potential tax law shifts.

Tax Planning for Future Changes

As tax laws evolve, staying informed can save you big bucks. Let’s explore some key areas where future changes might affect your tax strategy.

Tax Cuts and Jobs Act (TCJA)

The TCJA, enacted in 2017, brought significant changes to tax rates and deductions. While these adjustments have provided benefits, many provisions are set to expire after 2025. This means that tax brackets, standard deductions, and other benefits might revert to pre-2017 levels. Planning for these potential changes now can help you avoid surprises later.

Consider maximizing your use of current deductions and credits. For instance, the increased standard deduction has made itemizing less common, but if you anticipate the old rules returning, bunching deductions might become advantageous again.

Estate Tax

Estate tax, often dubbed the “death tax,” affects the transfer of wealth upon someone’s passing. Under the TCJA, the estate tax exemption was significantly increased, meaning fewer estates are subject to this tax. However, this higher exemption is also set to expire after 2025, potentially lowering the threshold and impacting more families.

To prepare, consider gifting strategies or setting up trusts. These methods can help manage estate size and ensure your wealth is passed on according to your wishes, without incurring hefty taxes.

Alternative Minimum Tax (AMT)

The AMT was designed to ensure that high-income individuals pay a minimum amount of tax, regardless of deductions and credits. The TCJA raised the AMT exemption and phase-out thresholds, reducing its reach. But, as with other provisions, these changes are temporary.

Monitoring your income and deductions is crucial to avoid unexpected AMT liability. Strategies such as timing income and deductions can help manage your exposure.

Incorporating these tax saving techniques into your planning can shield you from future tax hikes and ensure your financial plan remains robust. Stay proactive and consult with a tax professional to adapt your strategy as laws evolve.

Next, let’s address some frequently asked questions about tax saving techniques to clear up common concerns and help you make informed decisions.

Frequently Asked Questions about Tax Saving Techniques

How do I reduce my taxable income?

Reducing your taxable income can be achieved through several tax saving techniques. Here are some effective methods:

-

Retirement Savings: Contributing to retirement accounts like a 401(k) or a traditional IRA can lower your taxable income. These contributions are often tax-deductible, which means they reduce your taxable income for the year.

-

Tax Credits: Unlike deductions, tax credits directly reduce the amount of tax you owe. Look for credits like the Earned Income Tax Credit or Child and Dependent Care Credit to lower your tax bill.

-

Charitable Contributions: Donations to qualified charities can be deducted from your taxable income if you itemize. Consider bunching donations into one year to maximize your tax benefit.

What reduces your tax bill the most?

Reducing your tax bill effectively requires a mix of strategies:

-

Pass-Through Entity: If you own a business, consider structuring it as an S Corporation or LLC. These entities allow income to “pass through” to the owner’s personal tax return, often resulting in lower overall taxes.

-

Harvest Gains and Losses: Use tax-loss harvesting to offset capital gains. Selling investments at a loss can balance out gains, reducing your taxable income.

-

Financial Gifts: Giving financial gifts can reduce your taxable estate. Under current laws, you can give up to a certain amount per year to individuals without incurring gift taxes.

How do LLC owners avoid taxes?

LLC owners have unique opportunities to manage and potentially reduce their taxes:

-

LLC Taxation: Choose how your LLC is taxed. As a default, an LLC is a pass-through entity, meaning profits are taxed on the owner’s personal tax return. This can be advantageous compared to corporate tax rates.

-

Retirement Savings: Contributing to a self-employed retirement plan, like a SEP IRA, can reduce taxable income for LLC owners.

-

S Corporation Election: LLCs can elect to be taxed as an S Corporation. This allows owners to pay themselves a reasonable salary and take additional profits as dividends, which may be taxed at a lower rate.

Implementing these tax saving techniques can significantly impact your financial health. Always consult with a tax professional to ensure you’re making the most of available opportunities while staying compliant with tax laws.

Conclusion

At Elite Tax Strategy Solutions, we believe that personalized tax planning is not just about saving money today; it’s about building a stable financial future. Our proactive approach to tax optimization and compliance ensures that high earners and closely held businesses can steer the complexities of tax regulations with confidence.

We serve clients in Jasper, Indiana, and suburban areas near major cities, providing custom strategies that align with both immediate needs and long-term goals. Whether it’s maximizing retirement contributions, optimizing health savings, or exploring investment strategies like municipal bonds and tax-loss harvesting, our expert team is here to guide you every step of the way.

Tax laws are always changing, but with our comprehensive and forward-thinking planning, you can stay ahead of the curve. By integrating tax planning with your overall financial strategy, we help you make informed decisions that contribute to your financial well-being.

If you’re ready to take control of your taxes and work towards financial stability, explore our high-income individual tax planning services. Let us help you open up the full potential of your financial resources with our expertly crafted tax-saving techniques.