Explaining the Tax Planning Process

The tax planning process is a systematic approach to reducing your tax liability legally by making strategic financial decisions throughout the year. Here’s a simple breakdown:

- Define your financial goals – Short and long-term objectives

- Gather and organize tax information – Income, expenses, investments

- Analyze your current tax position – Understand your bracket and liability

- Identify potential strategies – Deductions, credits, timing opportunities

- Implement chosen actions – Make financial moves before deadlines

- Review and update regularly – Quarterly checks and annual reassessment

Tax planning isn’t a once-a-year scramble before filing deadlines—it’s an ongoing process that can significantly impact your financial health. When done properly, it helps you keep more of what you earn while staying fully compliant with tax laws.

The key distinction between tax planning and just filing taxes is timing and intention. While tax filing looks backward at what already happened, tax planning looks forward, creating opportunities to legally minimize your tax burden before financial decisions are locked in.

As Benjamin Franklin famously noted, “Nothing can be said to be certain, except death and taxes.” While we can’t help with the former, a structured tax planning process puts you in control of the latter.

I’m David Fritch, with over 40 years of experience helping small business owners and high-income earners steer the tax planning process through my CPA practice and law firm, now bringing this expertise to Elite Tax Strategy Solutions where we specialize in innovative tax planning for clients with substantial tax burdens.

Tax planning process terms made easy:

– taxes and financial planning

– business tax advisory services

– how to defer taxes

Tax Planning 101: Definitions, Objectives, and Types

Think of tax planning as looking at your financial puzzle from above, seeing how all the pieces fit together to create the smallest tax bill possible. It’s not about looking at just one transaction or decision in isolation—it’s about seeing the whole picture of your finances.

The heart of the tax planning process focuses on several key objectives that work together:

You want to keep more of what you earn by reducing your tax bill. You want to avoid those frustrating penalties that come from missing deadlines or making mistakes. You’re thinking about your family’s future and how to minimize taxes across generations. And of course, you want to do all this while staying on the right side of tax laws.

Our tax system works like a staircase—the more you earn, the higher the steps (and tax rates) you climb. In 2024, if you’re filing as single, you’ll pay 10% on your first $11,000, then 12% on earnings up to $44,725, and so on up to 37% for income over $609,350. Understanding these brackets is crucial to effective planning.

As we often tell our clients at Elite Tax Strategy Solutions, “You worked hard for your money—let’s make sure you keep as much of it as legally possible.”

Why Tax Planning Is Important

Tax planning does far more than just save you money at filing time:

First, it gives your cash flow a significant boost. When you reduce your tax liability through careful planning, you free up money that can work for you—whether that’s investing, paying down debt, or funding other priorities. Our clients typically see their effective tax rate drop by 2-5% through year-round planning.

Second, it helps you fly under the audit radar. With proper documentation and consistent reporting patterns, you’re less likely to trigger IRS scrutiny. Did you know the average American leaves about $1,200 in tax credits on the table each year by rushing through their taxes without proper planning?

Third, it helps grow your family legacy. With the 2024 federal lifetime estate tax exemption at $13.61 million per person ($27.22 million for married couples), strategic planning can help preserve substantial wealth for future generations.

Finally, it dramatically reduces stress. As one client recently told me, “Tax planning transformed April from a month of dread to just another month on the calendar.” That peace of mind is invaluable.

Four Main Types of Tax Planning

The tax planning process comes in four main flavors, each with its own approach:

Permissive tax planning works within the existing framework without seeking special provisions. It’s like following a recipe exactly as written—taking the standard deduction or claiming the child tax credit that’s explicitly spelled out in tax code.

Purposive tax planning takes advantage of tax incentives designed to encourage certain behaviors. This might include contributing to retirement accounts, investing in opportunity zones, or installing those energy-efficient windows that come with tax credits.

Short-term tax planning focuses on the current tax year. It’s about timing—like a small retailer client of ours who restructured in Q1 and cut their self-employment tax liability by 15% through timely entity changes.

Long-term tax planning takes the marathon view, not the sprint. It addresses multi-year or lifetime considerations like retirement accounts, estate planning, and business succession. This might include Roth conversion strategies, establishing trusts, or implementing family limited partnerships.

At Elite Tax Strategy Solutions, we believe the most effective approach blends all four types, customized to your specific situation. As one client put it, “I used to think tax planning was just about finding deductions. Now I see it’s about building a comprehensive financial strategy where taxes are just one piece of the puzzle.”

More info about Tax and Financial Planning

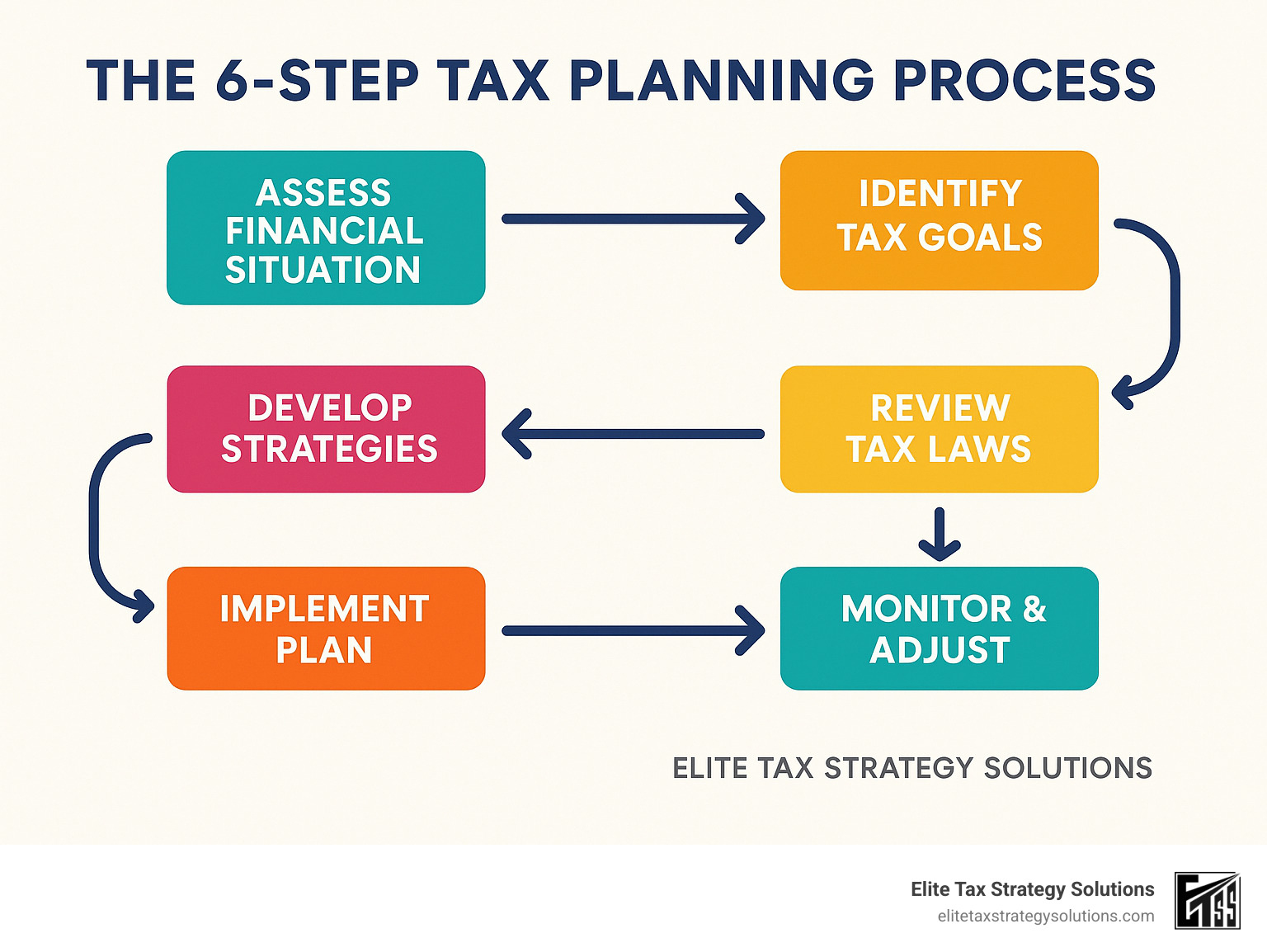

The 6-Step Tax Planning Process

A good tax plan doesn’t happen by accident. At Elite Tax Strategy Solutions, we’ve refined the tax planning process into six essential steps that provide structure while remaining flexible enough to adapt to your unique situation.

Think of tax planning as a team sport. The most successful outcomes happen when we coordinate between all your financial partners – you (of course!), your CPA, financial advisors, estate planning attorneys, and insurance professionals. This collaborative approach ensures we’re looking at your complete financial picture, not just isolated pieces of the puzzle.

Want to dive deeper? Check out our Comprehensive Tax Planning services.

Step 1: Define Goals in the Tax Planning Process

Before we talk deductions and credits, we need to understand what matters most to you. Your tax plan should support your broader life goals, not the other way around.

Maybe you’re focused on reducing this year’s tax bill. Or perhaps you’re more concerned with building retirement savings tax-efficiently. Many clients come to us during major life transitions – getting married, having a baby, changing careers, approaching retirement, or selling a business.

During our initial conversations, we’ll also discuss your comfort level with different approaches. Some tax strategies are straightforward with predictable outcomes, while others might be more complex or nuanced. As one client put it, “I never realized how much my risk tolerance would influence my tax decisions.”

“The biggest mistake we see is people jumping to tax strategies before they’ve clarified their goals,” explains our senior tax strategist. “When you know exactly what you’re trying to accomplish, the right tax moves become much clearer.”

Step 2: Gather & Organize Tax Data

Now comes the part many people dread – paperwork! But don’t worry, we’ll make this as painless as possible.

We’ll need to collect your financial information – income documents like W-2s and 1099s, investment statements, prior tax returns, business financials, real estate documents, retirement account information, charitable receipts, and medical expense records.

The IRS can typically look back three years for audits (sometimes longer), so good recordkeeping isn’t just convenient – it’s essential protection. We recommend creating a digital vault for tax documents with consistent file naming and regular backups. Many of our clients appreciate our secure client portal that eliminates the traditional “shoebox of receipts” approach.

“A little planning goes a long way in reducing your tax bill,” notes the IRS in their guidance. This is particularly true when it comes to organization – having the right documents at your fingertips makes everything else flow more smoothly.

Step 3: Analyze Current Tax Position

With your goals defined and data gathered, we’ll analyze where you stand today. This creates the baseline from which all planning decisions will flow.

We’ll look closely at your Adjusted Gross Income (AGI), which influences everything from your tax rates to deduction eligibility. We’ll calculate both your marginal tax rate (the rate on your last dollar earned) and your effective tax rate (the average rate across all your income). For higher earners, we’ll assess potential exposure to the Alternative Minimum Tax (AMT), which in 2024 has an exemption of $85,700 for single filers with a top rate of 28%.

For business owners, we’ll evaluate whether your current entity structure (sole proprietorship, S-corporation, C-corporation) still makes sense for your situation.

This analysis often reveals immediate opportunities. One client finded they were just $5,000 over a key threshold that increased their capital gains rate from 15% to 20%. With a few strategic adjustments to income timing, they saved over $10,000 in taxes.

For scientific research on how tax brackets work, check out Investopedia’s guide.

Step 4: Identify & Model Strategies

Now for the creative part – identifying potential strategies and modeling their impact on your tax situation.

We’ll evaluate available deductions and credits, analyze timing opportunities for income and expenses, optimize retirement contributions, review investment strategies, and assess business structure options. The most powerful insights often come from creating multiple scenarios and comparing their outcomes.

For example, we might model the impact of:

– Taking the standard deduction versus itemizing

– Converting traditional IRA assets to Roth

– Accelerating or deferring business income

– Implementing tax-loss harvesting in your portfolio

– Adjusting how you compensate yourself as a business owner

Our sophisticated modeling tools allow us to project multi-year tax impacts and compare different approaches side by side. As our lead strategist often says, “Tax planning isn’t about finding a single magic bullet. It’s about identifying the combination of strategies that work together to achieve your goals.”

For more ideas, visit our guide to Tax Planning Strategies.

Step 5: Implement Chosen Actions

After we’ve identified the most beneficial strategies, it’s time to put them into action. This might include adjusting your W-4 withholding, making retirement contributions, opening HSAs or FSAs, executing Roth conversions, making strategic charitable donations, purchasing business equipment, implementing estate planning documents, or making Qualified Charitable Distributions from IRAs.

Timing is critical in tax planning. For example, 401(k) contributions for 2024 must be made by December 31, 2024, while IRA contributions can be made until April 15, 2025. SEP IRA contributions can be made until your business tax filing deadline, including extensions.

“The best tax strategy in the world is worthless if you miss the implementation deadline,” our implementation specialist reminds clients. That’s why we provide a detailed action plan with clear deadlines and responsibilities.

Step 6: Review & Update the Tax Planning Process

Tax planning isn’t something you do once and forget about. It requires regular attention as tax laws change and your life evolves.

We recommend quarterly check-ins to review your year-to-date income, recent tax law changes, and progress on implementation steps. We’ll also help you monitor your position relative to key tax thresholds. For example, if you’re approaching the $200,000 (single) or $250,000 (married) threshold for the Net Investment Income Tax, we might recommend deferring certain investment income.

Beyond these regular reviews, we’ll also conduct an annual comprehensive assessment of your entire tax situation and revisit your plan after any major life events like marriages, divorces, births, job changes, or business transactions.

“Tax planning is a dynamic process that requires ongoing attention,” explains our client relationship manager. “The most successful clients view it as a regular part of their financial routine, not an annual event.”

Learn more about our approach to Proactive Tax Planning.

Top Tax Planning Strategies for Individuals

Let’s face it – nobody enjoys paying more taxes than necessary. The good news? With smart planning, you don’t have to. Here are some of the most powerful strategies I’ve seen work wonders for our clients during the tax planning process:

Retirement accounts remain one of your strongest tax-saving tools. For 2024, you can contribute up to $23,000 to your 401(k), with an extra $7,500 if you’re 50+. IRA contribution limits sit at $7,000 with a $1,000 catch-up provision. As one client told me, “It feels like getting paid twice – once when my tax bill shrinks, and again when I retire.”

Capital gains management can dramatically reduce your tax burden. Assets held longer than a year qualify for preferential long-term rates of 0%, 15%, or 20% (depending on your income). This creates opportunities for strategic timing of your investment sales.

When investments underperform, tax-loss harvesting turns lemons into lemonade. You can offset gains with losses and deduct up to $3,000 against ordinary income each year. Any excess losses roll forward indefinitely – like storing tax savings for a rainy day.

Health Savings Accounts offer what I call the “triple crown” of tax benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. In 2024, individuals can contribute $4,150 and families $8,300, with an additional $1,000 for those 55+.

Flexible Spending Accounts let you set aside pre-tax dollars for healthcare ($3,200 limit in 2024) or dependent care. Remember though – unlike HSAs, FSA funds typically need to be used within the plan year.

The “bunching” strategy has saved many of our clients thousands. By grouping deductible expenses (especially charitable contributions and medical expenses) into alternate years, you can exceed the standard deduction threshold when it otherwise wouldn’t be possible.

For charitable-minded folks, donor-advised funds provide immediate deductions for contributions while allowing you to distribute the money to charities over time. It’s like banking your tax savings while spreading your giving.

Maximizing Deductions & Credits

Understanding the difference between deductions and credits can significantly impact your bottom line:

| Tax Deductions | Tax Credits |

|---|---|

| Reduce taxable income | Reduce tax liability dollar-for-dollar |

| Value depends on tax bracket | Same value regardless of income |

| Examples: mortgage interest, charitable donations | Examples: Child Tax Credit, EITC |

For 2024, the standard deduction is $14,600 for single filers and $29,200 for married couples filing jointly. Itemizing makes sense when your eligible deductions exceed these thresholds.

Common itemized deductions include mortgage interest (limited to the first $750,000 of debt), state and local taxes (capped at $10,000), charitable contributions (up to 60% of AGI for cash donations), and medical expenses exceeding 7.5% of your AGI.

Tax credits are even more valuable since they directly reduce your tax bill dollar-for-dollar. The Child Tax Credit offers up to $2,000 per qualifying child, while the Earned Income Tax Credit can provide up to $7,430 for low to moderate-income workers. Education credits like the American Opportunity Credit (up to $2,500) and Lifetime Learning Credit (up to $2,000) help offset the rising cost of education.

As I often tell clients during our tax planning process, “If deductions are good, credits are great!” Their direct impact on your tax bill makes them particularly powerful.

Investment Moves & Tax Liability

Your investment decisions and tax situation are more connected than most people realize:

Long-term holding might seem boring, but patience pays off. Assets held over a year qualify for those lower long-term capital gains rates I mentioned earlier. Sometimes the most sophisticated tax strategy is simply sitting tight.

Municipal bonds generate interest that’s generally exempt from federal income tax (and sometimes state and local taxes too). To compare them with taxable investments, calculate the tax-equivalent yield by dividing the municipal bond yield by (1 – your marginal tax rate).

Cost basis planning lets you specify which shares to sell when liquidating partial positions. By choosing high-cost-basis shares, you can generate smaller gains or larger losses. This control can be invaluable during the tax planning process.

Be careful with the wash-sale rule – if you sell a security at a loss and buy the same or a “substantially identical” security within 30 days before or after, the IRS disallows the loss. As one client learned the hard way, “The tax code has more traps than an Indiana Jones movie.”

Tax-managed funds and ETFs are designed to minimize taxable distributions, making them excellent choices for non-retirement accounts. Their tax-efficient structure can save you thousands over time.

At Elite Tax Strategy Solutions, we coordinate closely with your investment advisors to ensure tax considerations are baked into your investment strategy. This teamwork maximizes what really matters – your after-tax returns.

For more specialized guidance on managing your investments with taxes in mind, check out our Tax Management Services page or review external research on retirement limits from the IRS.

Effective Tax Planning Strategies for Businesses

Business owners face unique tax challenges—and opportunities. At Elite Tax Strategy Solutions, we’ve seen how strategic planning can transform a business’s bottom line through the tax planning process.

One manufacturing client told us, “I used to think taxes were just a cost of doing business. Now I see they’re actually a business strategy.” This mindset shift helped them save over $37,000 last year alone.

The entity you choose sets the foundation for all your business tax planning. A self-employed consultant client of ours saved over $15,000 in self-employment taxes simply by switching from a sole proprietorship to an S-corporation and implementing a reasonable salary strategy. The right structure depends on your specific situation, growth plans, and exit strategy.

Depreciation deductions represent another powerful opportunity. In 2024, Section 179 expensing allows businesses to deduct up to $1,220,000 of qualified property placed in service. Meanwhile, bonus depreciation sits at 60% for 2024 (down from 80% in 2023). One restaurant owner client used these provisions to completely renovate their kitchen equipment while dramatically reducing their tax bill.

“People often think the R&D Credit is only for scientists in lab coats,” our lead business strategist often jokes. In reality, this valuable credit applies to many activities aimed at developing or improving products, processes, or software—even for small businesses innovating in traditional industries.

Family businesses have additional planning opportunities. Paying reasonable salaries to family members who provide legitimate services can shift income to potentially lower tax brackets. As one client put it, “My daughter was going to work somewhere during college anyway—having her work in our business helped her gain experience while helping our family’s overall tax situation.”

For businesses with international operations, the tax planning process becomes even more complex—but so do the opportunities. Transfer pricing, tax treaties, and foreign tax credits require careful navigation, but can yield significant savings when handled properly.

With the $10,000 SALT (state and local tax) deduction cap still in place, business owners need creative strategies to manage state and local tax exposure. This might include reconsidering where business activities occur or how they’re structured.

Small & Pass-Through Entities

Small businesses and pass-through entities deserve special attention in the tax planning process. These structures—including sole proprietorships, partnerships, S-corporations, and many LLCs—offer unique planning opportunities.

S-corporation salary optimization remains one of the most powerful strategies for many business owners. While S-corporation owners must take a “reasonable” salary, finding the right balance between salary and distributions can save thousands in self-employment taxes. As one client said after our planning session, “I had no idea I was overpaying myself—in terms of taxes, anyway!”

The Qualified Business Income (QBI) deduction under Section 199A allows eligible pass-through business owners to deduct up to 20% of their qualified business income. Though this deduction phases out for certain service businesses at higher income levels, proper planning can help maximize its benefits. A real estate investor client restructured their holdings to qualify for this deduction, saving nearly $22,000 annually.

IRS safe harbors provide valuable certainty in an uncertain tax landscape. For example, the Section 199A rental real estate safe harbor clarifies when rental activities qualify for the QBI deduction. These provisions can simplify compliance while providing peace of mind during the tax planning process.

The choice between cash and accrual accounting methods can significantly impact when income is recognized and expenses are deducted. One construction company client deferred over $50,000 in taxable income by switching from accrual to cash accounting, giving them breathing room during a challenging year.

Retirement plan selection represents another powerful opportunity. In 2024, a self-employed individual can contribute up to $69,000 to a Solo 401(k)—or $76,500 if age 50 or older. Compared to simpler options like SEP IRAs, SIMPLE IRAs, or defined benefit plans, the right retirement plan can dramatically reduce current tax liability while building long-term wealth.

Corporations & Cross-Border Operations

Larger businesses and those with international operations face additional layers in the tax planning process. These complexities require specialized expertise, but also create opportunities for significant savings.

Transfer pricing compliance has become increasingly important as tax authorities worldwide scrutinize cross-border transactions. When related entities in different countries conduct business, these transactions must reflect “arm’s length” prices—what unrelated parties would charge each other. Proper documentation isn’t just about compliance; it’s about avoiding costly penalties and double taxation.

“The global tax landscape is shifting under our feet,” notes our international tax specialist. Many countries are adopting OECD Base Erosion and Profit Shifting (BEPS) regulations to combat perceived tax avoidance strategies. Staying ahead of these changes requires both global perspective and local expertise.

Foreign tax credit planning helps clients avoid paying tax twice on the same income. One technology company client saved over $120,000 by properly structuring their operations to maximize available credits while maintaining business flexibility.

Global Intangible Low-Taxed Income (GILTI) provisions have complicated international tax planning since their introduction in 2017. We help clients steer these complex rules with strategies that align with their broader business objectives rather than letting tax considerations drive business decisions.

Repatriation planning—structuring the movement of funds from foreign subsidiaries to U.S. parent companies—requires careful consideration of both tax and business needs. As one client told us, “I never realized how many options we had for bringing profits home until we worked through the tax planning process together.”

At Elite Tax Strategy Solutions, we maintain relationships with tax professionals worldwide to provide truly comprehensive cross-border planning. Learn more about our approach to Tax Planning for Small Businesses or explore Investopedia’s corporate tax basics for additional background.

Recordkeeping, Compliance & Mistakes to Avoid

The backbone of successful tax planning isn’t just smart strategy—it’s meticulous recordkeeping. Those organized files (whether digital or physical) aren’t just for peace of mind; they’re your protection and proof when deductions are questioned or an audit letter arrives in your mailbox.

“The difference between tax avoidance and tax evasion is the thickness of a prison wall,” goes the old joke among tax professionals. The key to staying on the right side of that wall? Proper documentation.

The IRS typically has three years to audit your return, but this window extends to six years if they suspect substantial income underreporting—and there’s no time limit whatsoever for fraudulent returns. This is why we recommend a prudent approach to recordkeeping:

- Keep basic tax records for at least seven years

- Hold onto property records for as long as you own the asset, plus seven years afterward

- Maintain retirement account documentation indefinitely

- Store estate planning documents permanently

At Elite Tax Strategy Solutions, we’ve seen the relief on clients’ faces when they can quickly produce the exact document needed during an IRS inquiry. As one client told us after surviving an audit: “Moving from a shoebox of receipts to a digital system saved me hours of stress when I was audited. I found everything the auditor requested within minutes.”

Organizing Tax Records Year-Round

The tax planning process works best when recordkeeping becomes a habit rather than a seasonal panic. Here’s how to make it painless:

Create a secure digital vault for your tax documents using encrypted cloud storage or specialized tax organization software. This approach not only protects sensitive information but makes retrieval almost instant when needed.

Modern receipt-capturing apps like Expensify, Receipt Bank, or QuickBooks have transformed expense tracking. Simply snap a photo of receipts as you receive them, and the app handles categorization and storage. One business owner client shared: “I used to lose 20% of my deductible expenses simply because the receipts disappeared. Now I capture everything in real-time, and my tax deductions have increased significantly.”

Whether your system is physical or digital, consistent labeling makes all the difference. Develop a naming convention that works for you and stick with it. Remember to establish backup protocols too—redundant copies of critical tax information can save you if technology fails.

Perhaps most importantly, schedule regular monthly or quarterly review dates to keep your records current. These check-ins often reveal potential tax issues while there’s still time to address them.

As the IRS itself advises, “Organize tax records in software or labeled folders as you receive them.” This ongoing approach transforms tax preparation from a dreaded marathon into a simple review of already-organized information.

Pitfalls in the Tax Planning Process & Prevention

Even sophisticated taxpayers can stumble into common tax traps. Here are the pitfalls we most frequently help clients avoid:

Procrastination tops the list of tax planning mistakes. When you wait until December—or worse, April—your options narrow dramatically. As our tax director often reminds clients, “The best time to start tax planning for 2024 was January 1, 2024. The second best time is now.”

Life-event blindness catches many taxpayers off guard. Major life changes like marriage, divorce, birth, death, or job changes trigger tax implications that are easily overlooked without proactive planning. One client who failed to adjust withholding after divorce faced an unexpected $7,000 tax bill that could have been avoided with timely planning.

Worker misclassification remains a serious risk for business owners. Incorrectly treating employees as independent contractors can lead to substantial penalties, back taxes, and interest. The IRS looks at behavioral control, financial control, and relationship factors—not just what’s written in a contract.

Wash-sale violations trip up even sophisticated investors. When you sell securities at a loss and repurchase “substantially identical” securities within 30 days before or after the sale, you can’t claim the tax loss. We’ve seen clients inadvertently trigger this rule through automated investing platforms or by repurchasing in a different account.

Required Minimum Distribution (RMD) penalties can be particularly costly. Once you reach age 73, you must begin taking distributions from retirement accounts by April 1 following that year. Miss an RMD, and you’ll face a penalty of 25% of the amount not taken (though this can be reduced to 10% if corrected promptly).

Excess contribution penalties affect those who inadvertently contribute more than allowed to retirement accounts. This triggers a 6% excise tax on the excess amount for each year it remains in the account—a penalty that compounds over time if not addressed.

At Elite Tax Strategy Solutions, we’ve built proactive reminders and checkpoints into our client service model specifically to prevent these common mistakes. As one grateful client told us, “Having a professional team watching my back has saved me from countless tax headaches. The peace of mind alone is worth the investment.”

Learn more about maintaining proper compliance through our Tax Compliance Audit service, which helps identify potential issues before they become problems.

Frequently Asked Questions about the Tax Planning Process

What is the difference between a tax deduction and a tax credit?

When clients first come to us at Elite Tax Strategy Solutions, one of the most common questions involves understanding the difference between deductions and credits. The distinction is crucial for effective tax planning process decisions.

Think of tax deductions as reducing the income you’re taxed on, while tax credits directly reduce your tax bill dollar-for-dollar. If you’re in the 24% tax bracket, a $1,000 deduction lowers your tax bill by $240. But a $1,000 tax credit? That puts a full $1,000 back in your pocket, regardless of your tax bracket.

“If I had to choose between a $1,000 deduction or a $500 credit, I’d take the credit every time,” our senior tax specialist often tells clients. Credits simply pack more punch per dollar.

Common deductions include mortgage interest, charitable gifts, and state and local taxes (though these are capped at $10,000). On the credit side, you might benefit from the Child Tax Credit, Earned Income Tax Credit, or education credits that directly reduce what you owe the IRS.

Should I take the standard deduction or itemize?

This question comes down to simple math, but with significant implications for your tax planning process. For 2024, the standard deduction amounts are quite substantial:

- $14,600 for single filers and married filing separately

- $29,200 for married filing jointly

- $21,900 for heads of household

Itemizing only makes financial sense when your eligible deductions exceed these amounts. We find that many clients who previously itemized now take the standard deduction following recent tax law changes that nearly doubled these amounts.

One creative strategy we implement with our clients is “bunching” deductions. This involves concentrating deductible expenses into alternate years. For example, making two years’ worth of charitable contributions in December and January (of different tax years) might push you over the standard deduction threshold in one year, while allowing you to claim the standard deduction the next.

“Taking the standard deduction makes tax prep go a lot faster,” as one client happily finded, “but itemizing could save you thousands if you have significant deductible expenses.” The right choice depends entirely on your personal financial situation.

How often should I review my tax plan?

Tax planning isn’t a once-a-year event—it’s an ongoing process that requires regular attention. At Elite Tax Strategy Solutions, we’ve found that the most successful clients follow a rhythm of regular reviews:

Quarterly check-ins help you assess your year-to-date income and expenses, evaluate progress on implementation steps, and adjust withholding if needed. These brief reviews catch potential issues before they become problems.

A more comprehensive mid-year check-in around June or July gives you time to update projections and identify new planning opportunities while there’s still plenty of time to implement them.

Year-end planning in November and December focuses on last-minute strategies that must be completed before December 31, such as tax-loss harvesting, charitable contributions, or maximizing retirement contributions.

After filing your return, a post-filing review helps analyze the results and refine your strategy for the coming year. This is when we often identify the biggest opportunities for the next cycle.

“Tax planning is like navigation,” as our lead strategist often explains. “You set your course at the beginning of the year, but you need to check your position regularly and make adjustments as conditions change.”

Beyond these scheduled reviews, significant life events should trigger an immediate review of your tax plan. Marriage, divorce, the birth of a child, a new job, selling a business—all these milestones create both challenges and opportunities in the tax planning process.

At Elite Tax Strategy Solutions, we’ve built our reputation on staying proactive rather than reactive. When tax laws change (as they frequently do), we notify our clients immediately about how these changes might affect their specific situation and what adjustments might be needed to their tax strategy.

Conclusion

The tax planning process isn’t just about saving money—it’s about taking control of your financial future. Throughout this guide, we’ve walked through the six steps that can transform your approach to taxes from reactive to proactive, from stressful to strategic.

At Elite Tax Strategy Solutions, we see the difference this change makes in our clients’ lives every day. One business owner recently told me, “I used to see taxes as this unavoidable storm that hit every April. Now I steer with confidence, knowing exactly where I’m headed and how to get there.”

That’s the real power of effective tax planning—it gives you clarity and control.

What makes our approach at Elite Tax Strategy Solutions different is that we believe tax planning should be:

Proactive, not just reactive. We’re looking ahead at what might happen, not just dealing with what already did. This forward-thinking approach opens up opportunities that disappear if you wait until tax season.

Ongoing throughout the year. Your life doesn’t operate on tax deadlines, and neither should your tax strategy. We check in quarterly, making adjustments as your situation evolves.

Integrated with everything else in your financial life. Your retirement goals, business plans, and family needs all connect to your tax situation. When these elements work together, the results can be powerful.

Personalized to your unique circumstances. Those one-size-fits-all tax tips you read online? They’re just the starting point. Your tax strategy should be as individual as you are.

Compliant with all tax laws. We find every legitimate opportunity to reduce your tax burden while ensuring you stay well within the boundaries of the law.

I remember a client who came to us frustrated after years of last-minute tax preparation. After implementing our systematic approach, she called me in mid-December saying, “For the first time ever, I’m actually looking forward to tax season. I know exactly what to expect, and it’s so much better than I thought possible.”

That’s the peace of mind that comes from having a plan.

The best part? You don’t have to wait for a new year or a new tax season to begin. The best time to start the tax planning process is right now, wherever you are in your financial journey.

Ready to transform your relationship with taxes? Contact Elite Tax Strategy Solutions today and take the first step toward greater tax efficiency and financial confidence.