The Importance of Tax Planning for Real Estate Investors

Tax planning for real estate investors is crucial for maximizing returns and minimizing liabilities. Whether you’re flipping houses, renting properties, or investing in commercial real estate, understanding effective tax strategies can significantly boost your financial outcomes. Here are a few key reasons why tax planning is indispensable:

- Tax Deductions and Depreciation: Taking advantage of deductions and depreciation can lower taxable income.

- Deferred Taxation: Strategies like 1031 exchanges allow you to defer capital gains taxes.

- Maximized Returns: Efficient tax planning translates to higher net profits.

Real estate investments offer numerous tax benefits, making them attractive to high-income earners and small business owners looking to grow their wealth. However, navigating complex tax regulations requires a thorough understanding and often, the guidance of seasoned tax professionals.

I’m David Fritch, with over 40 years of experience in tax law and accounting, specializing in tax planning for real estate investors. My aim is to help you optimize your tax strategy to achieve long-term financial success.

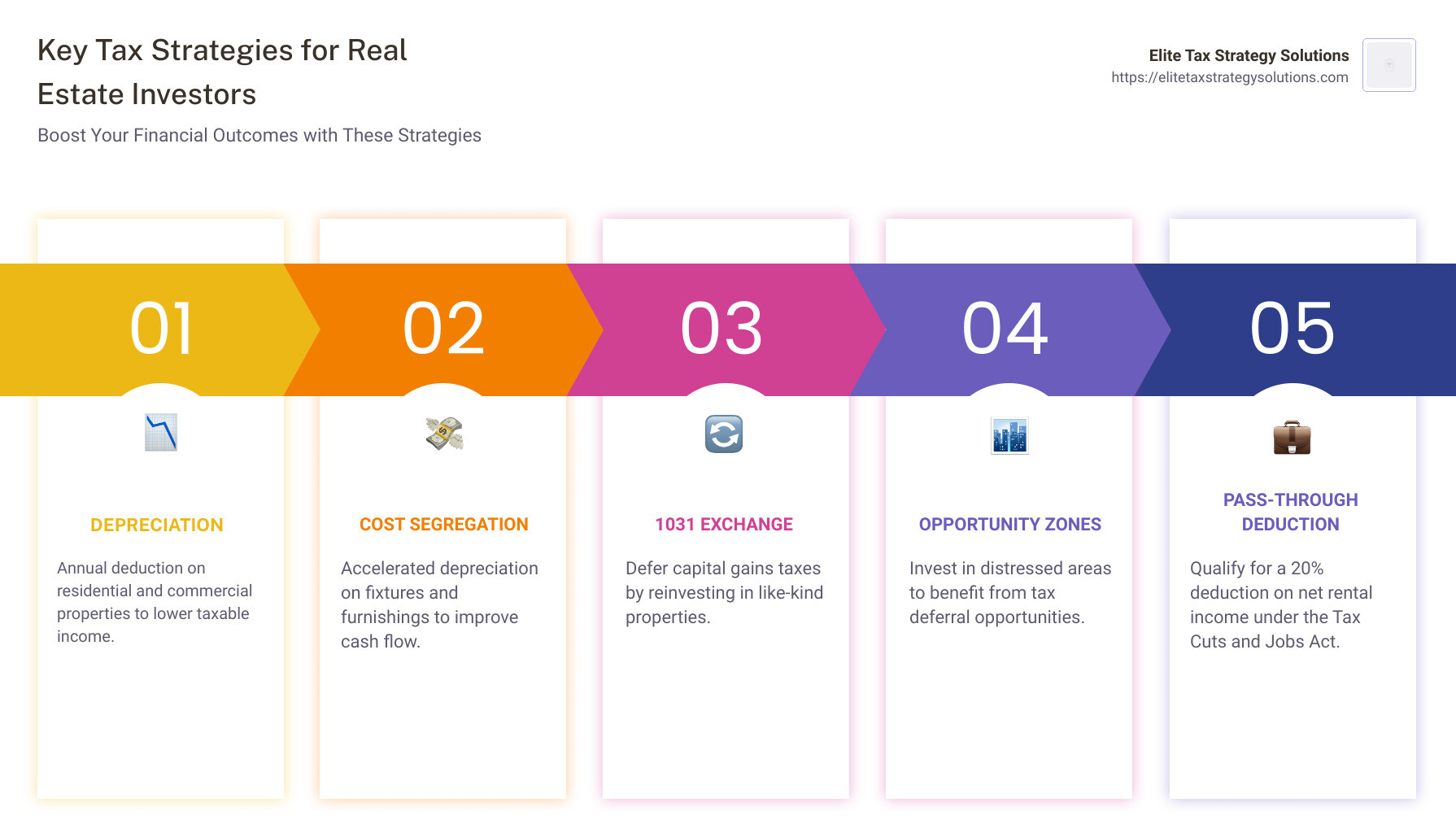

Key Tax Strategies for Real Estate Investors

Depreciation

Depreciation is a powerful tax strategy for real estate investors. It allows you to recover the cost of income-producing rental property through annual tax deductions. The IRS considers residential property to have a useful life of 27.5 years and commercial property to have a useful life of 39 years.

For example, if you purchase a residential rental property for $350,000 and the land is valued at $75,000, you can deduct $10,000 a year in depreciation for 27.5 years. This deduction can significantly reduce your taxable income each year.

Cost Segregation

Cost segregation is an advanced tax strategy that accelerates depreciation deductions. By performing a cost segregation study, you can identify and separate personal property assets that depreciate faster than the building itself. This includes fixtures, furnishings, and equipment.

For instance, if you own a commercial property, a cost segregation study might allow you to depreciate certain assets over 5, 7, or 15 years instead of the standard 39 years. This accelerated depreciation increases your cash flow by reducing taxable income in the early years of ownership.

1031 Exchange

A 1031 exchange, named after Section 1031 of the Internal Revenue Code, allows you to defer capital gains taxes when you sell one investment property and reinvest the proceeds in another like-kind property of equal or greater value. This strategy is valuable for growing your real estate portfolio without the immediate tax burden.

To qualify, the exchange must meet specific criteria:

- The replacement property must be of like-kind.

- The total value of the replacement property must be equal to or greater than the relinquished property.

- Both properties must be held for investment or business purposes.

Opportunity Zones

Opportunity Zones, created by the Tax Cuts and Jobs Act, are economically-distressed areas designated for investment. Investing in these zones through Qualified Opportunity Funds offers several tax benefits, including deferral of capital gains taxes.

When you invest in an Opportunity Zone, you can defer taxes on prior gains until the investment is sold or until December 31, 2026, whichever comes first. Additionally, if you hold the investment for at least 10 years, you may qualify for a permanent exclusion from capital gains tax on the new investment.

Pass-Through Deduction

The Tax Cuts and Jobs Act introduced the pass-through deduction, allowing real estate investors to deduct up to 20% of their net rental income. This deduction applies to income from pass-through entities like LLCs, partnerships, and S-corporations.

For example, if your rental properties generate $100,000 in net income, you can potentially deduct $20,000, reducing your taxable income significantly. This deduction is subject to various limitations and qualifications, so consulting with a tax professional is essential.

Next, we will explore strategies for maximizing deductions in your real estate investments.

Maximizing Deductions

Operating Expenses

Operating expenses are the ongoing costs necessary to manage and maintain your rental property. These expenses are deductible and can significantly reduce your taxable income. Common operating expenses include:

- Management fees: Costs paid to property managers for overseeing the property.

- Repairs and maintenance: Routine expenses to keep the property in good condition.

- Insurance: Premiums for property insurance policies.

For example, if you spend $5,000 on management fees, $2,000 on repairs, and $1,500 on insurance annually, that’s $8,500 you can deduct from your rental income, lowering your overall tax bill.

Mortgage Interest

Mortgage interest is one of the largest deductions available to real estate investors. You can deduct the interest paid on loans used to acquire or improve your rental property. According to the IRS, you can deduct home mortgage interest on the first $750,000 of indebtedness.

For instance, if your annual mortgage interest payment is $10,000, you can deduct this amount from your taxable income, providing substantial tax savings.

Property Taxes

Property taxes are another significant deductible expense. These are the annual taxes assessed by local governments based on the value of your property. You can deduct the full amount of property taxes paid each year.

For example, if you pay $3,000 in property taxes annually, you can deduct this amount from your rental income, reducing your taxable income accordingly.

Repairs and Maintenance

Understanding the difference between repairs and capital improvements is crucial for maximizing deductions. Repairs are expenses that keep the property in good working condition and are fully deductible in the year they are incurred. Capital improvements are expenses that add value to the property and must be depreciated over time.

IRS guidelines help distinguish between the two. Words like “patch,” “temporary,” and “minor” often indicate repairs, while “replace,” “upgrade,” and “new” suggest capital improvements.

For example, if you spend $1,200 to repaint a rental unit, this is considered a repair and is fully deductible. However, installing a new roof for $10,000 is a capital improvement and must be depreciated over the useful life of the roof.

Next, we will dig into advanced tax planning techniques for real estate investors.

Advanced Tax Planning Techniques

Entity Structure

Choosing the right entity structure is crucial for real estate investors. Most investors opt for an LLC (Limited Liability Company) due to its benefits in asset protection and tax flexibility. An LLC can protect your personal assets from lawsuits and debts related to your rental properties.

Moreover, operating under an LLC allows for more aggressive deductions. For example, you can deduct expenses like auto, meals, and travel, which might be harder to justify as a sole proprietor.

Case in point: Suppose you own a rental property under an LLC and spend $3,000 on business travel to inspect the property. With proper documentation, this expense can be deducted, reducing your taxable income.

Audit-Proofing

No one wants to be audited by the IRS, but there are ways to audit-proof your tax return. Here are two effective strategies:

-

Filing Extensions: File your tax return as late as legally allowed. The IRS tends to audit early filers more frequently. Use IRS forms 4868 for individuals and 7004 for entities like LLCs. While you still need to pay your taxes on time, this reduces your audit risk.

-

Written Explanations and Tax Law Citations: For items that may raise red flags, include written explanations and cite relevant tax laws. For instance, if you have significant travel expenses, cite IRS regulation 1.274-5T(c). Attach related bills and receipts with notarized statements for added credibility.

Avoiding Dealer Status

Being classified as a “dealer” by the IRS can be disastrous. Dealers are subject to the highest ordinary income tax rates, self-employment taxes, and alternative minimum taxes. To avoid this, you must demonstrate investment intent rather than a quick-sale motive.

One effective strategy is to hold properties for longer periods and document your intent to generate rental income. For example, maintaining detailed records of rental activities and improvements can help prove your intent to invest rather than flip properties quickly.

Self-Directed IRA

A Self-Directed IRA allows you to invest in real estate within your retirement account, offering tax-free gains. This is particularly useful for flipping properties or other short-term investments that generate immediate income.

Example: Suppose you flip a property within your Self-Directed IRA and make a $50,000 profit. Since the gains are within the IRA, they are not subject to immediate taxation, allowing the profits to grow tax-free until retirement.

By leveraging the right entity structure, audit-proofing your returns, avoiding dealer status, and using a Self-Directed IRA, you can significantly improve your tax planning strategies.

Next, we will explore frequently asked questions about tax planning for real estate investors.

Frequently Asked Questions about Tax Planning for Real Estate Investors

How to save tax by investing in real estate?

Saving on taxes as a real estate investor involves several key strategies:

-

Tax Write-Offs: You can deduct a wide range of expenses related to your rental property. This includes management fees, repairs, maintenance, and insurance.

-

Depreciation: Depreciation allows you to deduct the cost of the property over its useful life. For residential properties, this is typically 27.5 years, and for commercial properties, it’s 39 years. This can substantially reduce your taxable income.

-

Pass-Through Deduction: Thanks to the Tax Cuts and Jobs Act, you can deduct up to 20% of your net rental income if you qualify as a pass-through entity.

-

Capital Gains: Holding onto a property for more than a year can qualify you for long-term capital gains tax rates, which are lower than short-term rates.

-

Incentive Programs: Programs like Opportunity Zones can offer tax deferrals and even tax-free gains if you invest in designated distressed areas.

What is a simple trick for avoiding capital gains tax on real estate investments?

One effective way to avoid capital gains tax is through a 1031 Exchange. This allows you to defer paying taxes by reinvesting the proceeds from the sale of one investment property into a “like-kind” property. The key is to follow IRS rules and timelines closely.

Another trick is to use a retirement account like a Self-Directed IRA. By holding real estate within your IRA, you can defer taxes on gains until you withdraw the money in retirement.

How to pay no taxes with real estate investing?

While paying no taxes might sound too good to be true, there are legal ways to significantly minimize your tax burden:

-

Depreciation Recapture: When you sell a property, depreciation recapture can lead to taxes, but using a 1031 Exchange can defer these taxes indefinitely.

-

1031 Exchange: As mentioned, this allows you to defer capital gains taxes by reinvesting in a like-kind property. The new property must be of equal or greater value to fully defer the gains.

-

Equal or Greater Value Property: Ensure the replacement property in a 1031 Exchange is of equal or greater value to defer all capital gains taxes.

-

Primary Residence: If you live in the property for at least two out of the last five years, you can exclude up to $250,000 ($500,000 for married couples) of capital gains from your taxable income.

By leveraging these strategies, you can effectively manage and even eliminate your tax liabilities, maximizing your investment returns.

Conclusion

In summary, tax planning for real estate investors is essential for maximizing your investment returns and minimizing your tax liabilities. By utilizing strategies like depreciation, cost segregation, 1031 exchanges, and investing in Opportunity Zones, you can significantly reduce your taxable income and defer taxes on gains.

Elite Tax Strategy Solutions

At Elite Tax Strategy Solutions, we specialize in providing personalized tax planning services custom to your unique circumstances. Our team of seasoned tax professionals is dedicated to helping you steer the complexities of tax regulations and optimize your financial outcomes.

Personalized Tax Planning

Every investor’s situation is unique, and a one-size-fits-all approach doesn’t work. Our experts analyze your financial portfolio, considering factors such as your property investments, income sources, and deductions. This personalized approach ensures that every available tax-saving avenue is explored, maximizing your financial benefits.

Maximizing Savings

Our goal is to help you achieve sustained financial success by minimizing your tax liabilities. We stay abreast of the latest tax laws and regulations, ensuring compliance and proactive risk management. By collaborating with us, you gain insights into optimizing your tax strategy and safeguarding your financial interests.

To learn more about our innovative tax planning services and how we can help you maximize your savings, click here to get started.

Take control of your financial future with Elite Tax Strategy Solutions.