Why Proactive Tax Planning Makes Or Breaks Entrepreneurial Success

Tax planning for entrepreneurs is a strategic approach to legally minimizing tax liability while ensuring compliance with regulations. When done properly, it can significantly impact your bottom line and contribute to long-term business growth.

Key Components of Effective Tax Planning for Entrepreneurs:

- Business Structure Selection – Choose between LLC, S-Corp, C-Corp, or sole proprietorship based on your specific situation

- Income Timing Strategies – Defer income or accelerate expenses to manage tax brackets

- Qualified Business Income Deduction – Potentially deduct up to 20% of business income

- Retirement Plan Contributions – Reduce taxable income while building wealth

- State Tax Planning – Use pass-through entity elections to work around SALT caps

- Tax Credits Maximization – Identify and claim all available credits for hiring, research, and energy efficiency

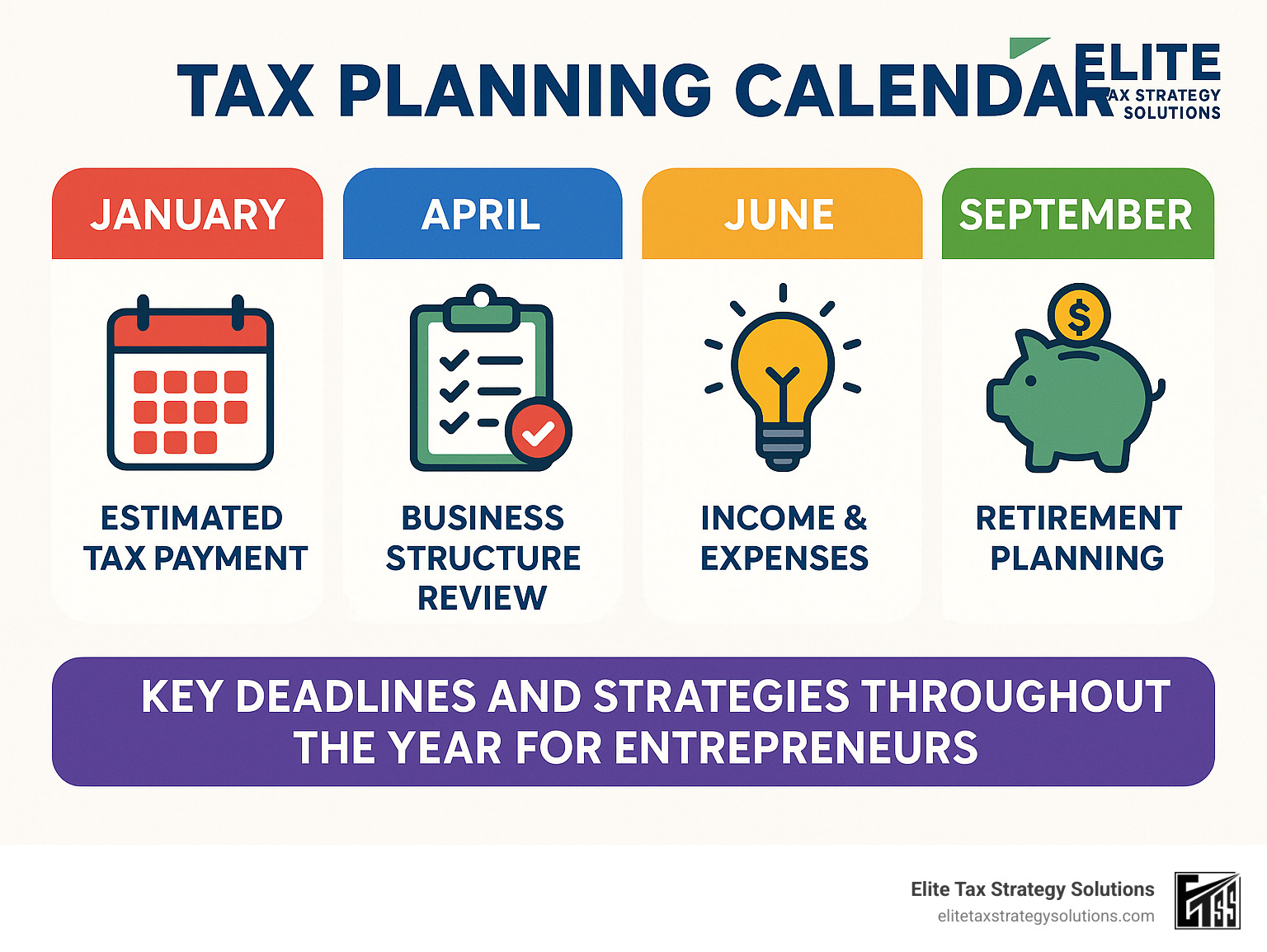

Tax planning isn’t a once-a-year activity but an ongoing process that requires attention throughout the year. Unlike tax preparation, which focuses on filing past-year returns, tax planning for entrepreneurs looks forward to create strategies that align with your business goals.

The difference between entrepreneurs who struggle with taxes and those who thrive often comes down to timing. According to research, 45% of small businesses spend over 40 hours annually dealing with federal taxes—that’s a full week of productivity lost! With proper planning, you can redirect that time toward growing your business instead.

I’m David Fritch, a CPA with over 40 years of experience providing tax planning for entrepreneurs through my firm Elite Tax Strategy Solutions, where I’ve helped hundreds of small business owners legally minimize their tax burden while ensuring compliance with ever-changing regulations. My background includes working at Arthur Andersen and maintaining my own successful tax practice focused specifically on helping entrepreneurs keep more of what they earn.

Tax planning for entrepreneurs vocab to learn:

– Business expense categories

– Tax risk management

– Comprehensive tax planning

Strategy 1: Pick the Optimal Business Structure First

The foundation of effective tax planning for entrepreneurs begins with selecting the right business structure. This decision isn’t just paperwork—it’s the cornerstone that shapes everything from your personal liability protection to the size of your tax bill each year.

I’ve seen this with hundreds of clients over my career. As one of our senior advisors often tells business owners: “Your business isn’t just your largest asset—it’s likely the one growing fastest in value each year. Getting the structure right can put tens of thousands back in your pocket annually.”

Let me walk you through your main options:

| Entity Type | Tax Treatment | Self-Employment Tax | Personal Liability | Complexity |

|---|---|---|---|---|

| Sole Proprietorship | Pass-through to personal return | Applies to all profits | Unlimited | Low |

| LLC | Pass-through (default) | Applies to all profits | Limited | Medium |

| S Corporation | Pass-through with salary/distribution split | Only on salary portion | Limited | Medium-High |

| C Corporation | Corporate tax + dividend tax | None (but double taxation) | Limited | High |

| Partnership | Pass-through to partners | Applies to all profits for general partners | Varies by partner type | Medium-High |

The biggest tax-saving opportunity I see most entrepreneurs miss? Transitioning from a sole proprietorship or standard LLC to an S Corporation. Here’s why this matters: with an S Corp, you only pay that hefty 15.3% self-employment tax (covering Social Security and Medicare) on your reasonable salary—not on your entire profit.

Let me make this real for you. Say your business nets $150,000 annually. As a sole proprietor, you’d pay self-employment tax on the full amount. But as an S Corp, if you pay yourself a reasonable salary of $80,000, you’d only pay self-employment tax on that portion—saving about $10,700 each year. That’s a family vacation, retirement savings, or reinvestment in your business!

When does making this switch make sense? In my experience, once your business consistently earns more than $80,000 in profit, the tax savings usually outweigh the additional compliance costs of running an S Corp.

Ready to make the change? You’ll need to file Form 8832 with the IRS. But don’t procrastinate—miss the deadline and you’ll be waiting until next year to implement this strategy.

For more personalized guidance on choosing the right structure for your specific situation, check out our detailed Business Tax Planning resources.

Avoid the Double-Tax Trap

One mistake I see smart entrepreneurs make repeatedly is defaulting to a C Corporation because it sounds more established or because that 21% corporate tax rate looks attractive compared to individual rates that can reach 37%.

Here’s the trap: C Corporations face what tax pros call “double taxation.” Your profits get taxed once at the corporate level, then you get taxed again when those profits come to you as dividends. It’s like paying toll at both ends of the bridge!

Pass-through entities (S Corps, LLCs, partnerships, sole proprietorships) avoid this trap because business income “passes through” to your personal tax return and is only taxed once.

That said, a C Corp isn’t always wrong. It might make sense if:

– You plan to plow most profits back into growing the business

– You need to retain significant earnings for future projects

– You’re courting venture capital funding

– Your business qualifies for special credits only available to C Corps

Let me share a real success story. A software developer client in Jasper, Indiana was operating as a sole proprietorship, making about $200,000 annually. After we helped him switch to an S Corporation, he took a reasonable salary of $90,000 while receiving the remaining $110,000 as distributions—completely exempt from self-employment tax. First-year tax savings? Over $22,000. That’s the power of choosing the right structure from the start.

Strategy 2: Maximize the 20% Qualified Business Income Deduction

Let me tell you about one of the best tax breaks small business owners have seen in decades. The Tax Cuts and Jobs Act of 2017 gave us the Qualified Business Income (QBI) deduction, and it’s a game-changer for your bottom line. This provision could put up to 20% of your business income back in your pocket—money that would otherwise go straight to the IRS.

“Confused? You’re not alone,” a tax professional colleague admitted to me recently. The QBI rules make even seasoned accountants scratch their heads, but I promise the potential savings make it worth untangling this web.

Here’s the straightforward version: if you run a business as a sole proprietor, partnership, S corporation, or certain LLCs, you might qualify to deduct up to one-fifth of your business income. For 2024, if your taxable income falls below $191,950 (filing single) or $383,900 (married filing jointly), you can likely claim the full deduction without jumping through too many hoops.

Once you cross those thresholds, though, things get trickier. The deduction starts phasing out, with complete elimination at $241,950 (single) or $483,900 (joint). And if you’re in what the IRS calls a Specified Service Trade or Business (think doctors, lawyers, consultants, performers, financial advisors), you’ll face stricter limitations.

For entrepreneurs with higher incomes, the calculation gets more complex, factoring in:

1. The W-2 wages your business pays employees

2. The original cost of your business assets (what the IRS calls “unadjusted basis of qualified property”)

If you’d like a deeper dive into strategies custom to your industry, check out our Small Business Tax Planning Strategies page.

Tax planning for entrepreneurs: Calculating Your 20% QBI Safely

When tax season rolls around, you’ll claim this deduction using either Form 8995 (the simplified version) or Form 8995-A (for more complex situations). Let me walk you through a basic example:

Imagine your business earned $200,000 in qualified income this year. Multiply that by 20%, and you’re looking at a potential $40,000 deduction. Of course, you’ll need to check those income thresholds I mentioned, apply any necessary limitations, and then claim your final deduction amount on your personal tax return.

One strategy many of my clients overlook is aggregation. If you own multiple businesses, combining them for QBI purposes might maximize your deduction by optimizing those W-2 wage and property tests.

Just last year, I worked with a real estate investor who owned several rental properties plus a property management company. By properly aggregating his businesses rather than treating each entity separately, he saved an additional $12,300 on his taxes. That’s a family vacation or a nice boost to his retirement account!

I should mention that the QBI deduction is currently set to expire after 2025 unless Congress extends it. This makes it especially important to maximize this benefit while it’s still available. Tax planning for entrepreneurs isn’t just about this year—it’s about looking ahead and capturing every legitimate deduction while you can.

Good record-keeping is essential for claiming this deduction. As a cash-basis business owner, make sure you’re tracking all qualifying income and related expenses carefully. This documentation will be your best friend if the IRS ever has questions.

Strategy 3: Timing Is Everything—Tax planning for entrepreneurs Through Income & Expenses

The art of timing your financial moves might be the most powerful tool in your tax planning for entrepreneurs toolkit. Yet surprisingly, many business owners don’t take full advantage of this strategy. By thoughtfully controlling when you recognize income and when you pay expenses, you can potentially drop into a lower tax bracket or push taxes into future years when they might impact you less.

“Think of your business finances like a river you can partially dam up or release as needed,” I often tell my clients. “The IRS calls this concept ‘constructive receipt,’ and mastering it can mean thousands in your pocket rather than Uncle Sam’s.”

Here’s when you might want to hold back that revenue stream until next year:

– You expect to earn less next year, putting you in a lower tax bracket

– Tax experts are predicting rate decreases

– Your cash flow is healthy enough to handle the delay

On the flip side, you might want to pull income forward into this year when:

– You anticipate jumping to a higher bracket next year

– Tax increases are on the horizon (like when TCJA provisions sunset in 2025)

– You have losses or credits that will disappear if not used now

Most small businesses operate on a cash basis for tax purposes, which gives you wonderful flexibility as year-end approaches. You can delay sending December invoices until January, prepay certain expenses in December, or purchase needed equipment before the ball drops on New Year’s Eve.

I remember working with a web developer from just outside Indianapolis who strategically delayed billing $45,000 of December projects until January 1st. This simple move kept him in a lower tax bracket and saved him about $6,700 in taxes that year—money he used to hire his first employee the following spring.

For more clever approaches to timing your income and expenses, check out our Business Tax Reduction page.

Year-End Moves to Shift Your Tax Bracket

The final quarter is where tax planning for entrepreneurs really shines. Here are some of my favorite year-end tax moves:

Invoice scheduling becomes critical in December. Take a hard look at your projected income and consider whether delaying those final invoices until January might keep you in a lower bracket. Just be sure your clients won’t be upset by the timing shift.

Prepaid expenses offer another opportunity. You can deduct up to 12 months of prepaid costs in the current year, including insurance premiums, rent payments, service contracts, and professional subscriptions. One restaurant owner I work with prepays her liability insurance every December, keeping $4,800 of income in her pocket rather than sending it to the IRS.

Business equipment purchases can dramatically reduce your taxable income. Section 179 allows deducting up to $1,220,000 in 2024 for qualifying equipment, with phase-out beginning at $3.05 million. Meanwhile, bonus depreciation permits writing off 60% of qualified property costs in 2024 (down from 100% in previous years).

Net Operating Loss management matters too. If you have NOL carryforwards, you might consider accelerating income to use them before they expire or become limited.

I always remind my clients in Jasper and throughout southern Indiana: “Don’t let the tax tail wag the business dog.” Only defer income if it makes sense from both cash flow and business perspectives. The goal isn’t just to save on taxes—it’s to build a stronger, more profitable business that happens to pay only its fair share in taxes.

Strategy 4: Turbo-Charge Savings With Retirement Plans

When it comes to tax planning for entrepreneurs, retirement plans are like finding money in both pockets of your jacket – they reduce what you owe Uncle Sam today while building your nest egg for tomorrow. The trick is picking the right plan for your unique situation.

Let me walk you through your main options for 2024, so you can see which fits your business best:

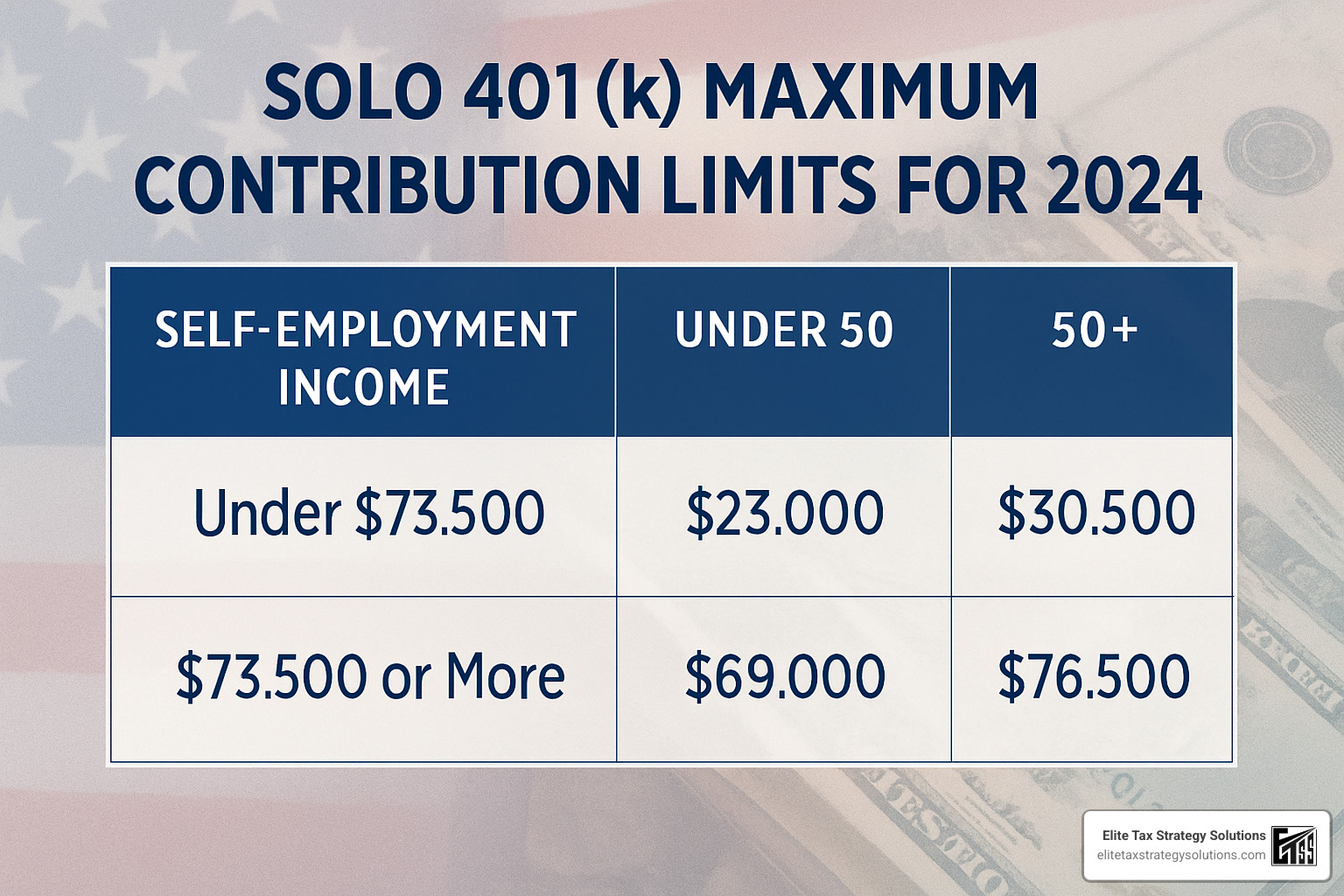

A SEP IRA lets you contribute up to $69,000 (or 25% of compensation, whichever is less). The paperwork is minimal, and you can set it up as late as your tax filing deadline plus extensions. This makes it perfect if you’re flying solo or have just a small team. Many of our Jasper clients love the simplicity.

The Solo 401(k) is my personal favorite for high-earning solo entrepreneurs. You can sock away up to $69,000, plus an extra $7,500 if you’re 50 or older. The catch? You need to establish it by December 31st. The paperwork is a bit more involved, but the tax savings are well worth it.

For businesses with employees, a SIMPLE IRA might be your sweet spot. You can contribute $16,000 (plus $3,500 more if you’re over 50). Just remember to set it up by October 1st. It’s a nice middle ground between simplicity and decent contribution limits.

If you’re a high-income professional looking to maximize tax deferral, a Cash Balance Plan could be your best friend. These age-based plans can allow contributions exceeding $300,000 annually for older entrepreneurs. Yes, they’re complex and require an actuary, but the tax savings can be enormous.

To see the power of these plans in action, consider John, a 55-year-old S-Corp owner earning $300,000 in profit. By implementing both a Solo 401(k) and a Cash Balance Plan, he contributes over $200,000 annually to retirement while saving approximately $74,000 in taxes each year. That’s like giving yourself a $74,000 bonus just for being smart about retirement planning!

“Most independent workers focus so much on making more that they forget about keeping more,” one retirement specialist told me recently. It’s a common mistake I see with new clients.

Thanks to the SECURE Act and SECURE 2.0, small businesses now have extra incentives to start retirement plans. You could qualify for a tax credit of up to $5,000 per year for the first three years when starting a new plan. Add another $500 credit if you implement auto-enrollment features. That’s the government essentially paying you to save for retirement!

For more details on setting up the perfect retirement plan for your business, check out our Tax Advice for Startups page.

Avoid Self-Employment Drag with Smart Tax planning for entrepreneurs

The 15.3% self-employment tax feels like a ball and chain for many entrepreneurs. It’s that extra tax covering Social Security and Medicare that employees split with their employers, but self-employed folks pay in full.

Here’s where smart tax planning for entrepreneurs creates magic: With an S Corporation structure, only your salary (not distributions) gets hit with self-employment tax. When you contribute to retirement plans from that salary, you’re essentially triple-dipping:

First, you’re slashing your income tax bill. Second, you’re building your retirement wealth. And third, you’re squeezing more value from dollars that were already subject to self-employment tax anyway.

Let me show you how powerful this can be: A solo entrepreneur earning $150,000 could save approximately $5,600 in income taxes by maxing out a Solo 401(k) contribution. That’s money that stays in your pocket while simultaneously growing your retirement account.

One of my favorite success stories comes from a marketing consultant in suburban Chicago. By combining an S Corporation election with a maximized Solo 401(k), she dropped her effective tax rate by 9 percentage points – saving over $27,000 in her first year implementing these strategies. That paid for a family vacation to Europe and still left plenty to reinvest in her business.

The best retirement plan isn’t just about maximum contributions – it’s about finding the perfect fit for your business size, income level, and long-term goals. That’s where personalized tax planning for entrepreneurs really shines.

Strategy 5: Elect Pass-Through Entity Taxes to Beat the $10k SALT Cap

If you’re an entrepreneur in a high-tax state, you’ve likely felt the sting of the $10,000 cap on state and local tax (SALT) deductions that came with the Tax Cuts and Jobs Act. This limitation has hit business owners particularly hard, especially those in states with higher income tax rates.

But here’s some good news – there’s a powerful workaround that savvy business owners are using: Pass-Through Entity Tax (PTET) elections.

This strategy allows your pass-through business (like your S Corporation, partnership, or certain LLCs) to pay state taxes at the entity level instead of passing those taxes through to your personal return. Why does this matter? Because when your business pays these taxes, they’re fully deductible as business expenses – effectively sidestepping that frustrating $10,000 SALT cap.

“This is one of the most significant tax-saving opportunities for business owners in high-tax states that we’ve seen in years,” says one of our senior tax advisors. “It’s like finding money that was previously locked away.”

As of 2024, this opportunity is available in 36 states plus New York City. If you operate in California, New York, New Jersey, Illinois, Connecticut, Massachusetts, or any of the other states with PTET regimes, you could be leaving serious money on the table by not exploring this option.

Here’s a simplified breakdown of how it works:

- Your business makes an election to pay state income tax directly at the entity level

- These taxes get deducted as a business expense, reducing your federal taxable income

- You receive a credit on your personal state tax return for the taxes already paid by your business

The savings can be substantial. For a business owner in a high-tax state with $500,000 in income, this strategy could put $15,000 or more back in your pocket annually through federal tax savings.

For more detailed guidance on implementing this strategy for your specific situation, check out our Business Tax Advisory Services page.

Checklist Before Filing Your PTET Election

Before jumping into a PTET election, there are several important factors to consider. Let’s walk through the key points to ensure this strategy is right for your business:

State-specific rules matter tremendously. Each state has different requirements, rates, and deadlines for PTET elections. For example, if you’re operating in New York, you’ll need to make your election by March 15, 2025, for the 2025 tax year. Missing these deadlines means missing out on the savings.

Owner consent is typically required. Most states won’t let you make this election unless all owners agree to it. This can become complicated with multiple partners or shareholders who may have different tax situations.

Cash flow impact deserves careful consideration. Entity-level taxes must be paid during the year, which might affect your business’s available cash. You’ll need to plan for these payments, which often come due before the tax benefit is realized.

Your entity structure may limit eligibility, as some states only allow certain types of entities to make PTET elections. Similarly, if you have multi-state operations, you’ll need to analyze each state’s specific PTET rules.

Don’t forget about quarterly vouchers – many states require quarterly estimated tax payments for PTET, just like other business taxes. And always consider the interaction with other tax benefits to ensure you’re maximizing your overall tax position.

I recently worked with a client based in Indiana who had substantial operations in Illinois. By electing Illinois’ PTET option, we converted what would have been non-deductible personal state taxes into fully deductible business expenses, saving over $18,000 in federal taxes. That’s real money that went back into growing their business instead of paying Uncle Sam.

Tax planning for entrepreneurs requires looking at these state-level strategies alongside your federal tax planning. With SALT cap workarounds like PTET elections, the state-federal tax interaction becomes an opportunity rather than just a compliance burden.

Strategy 6: Capture Every Credit & Incentive Available

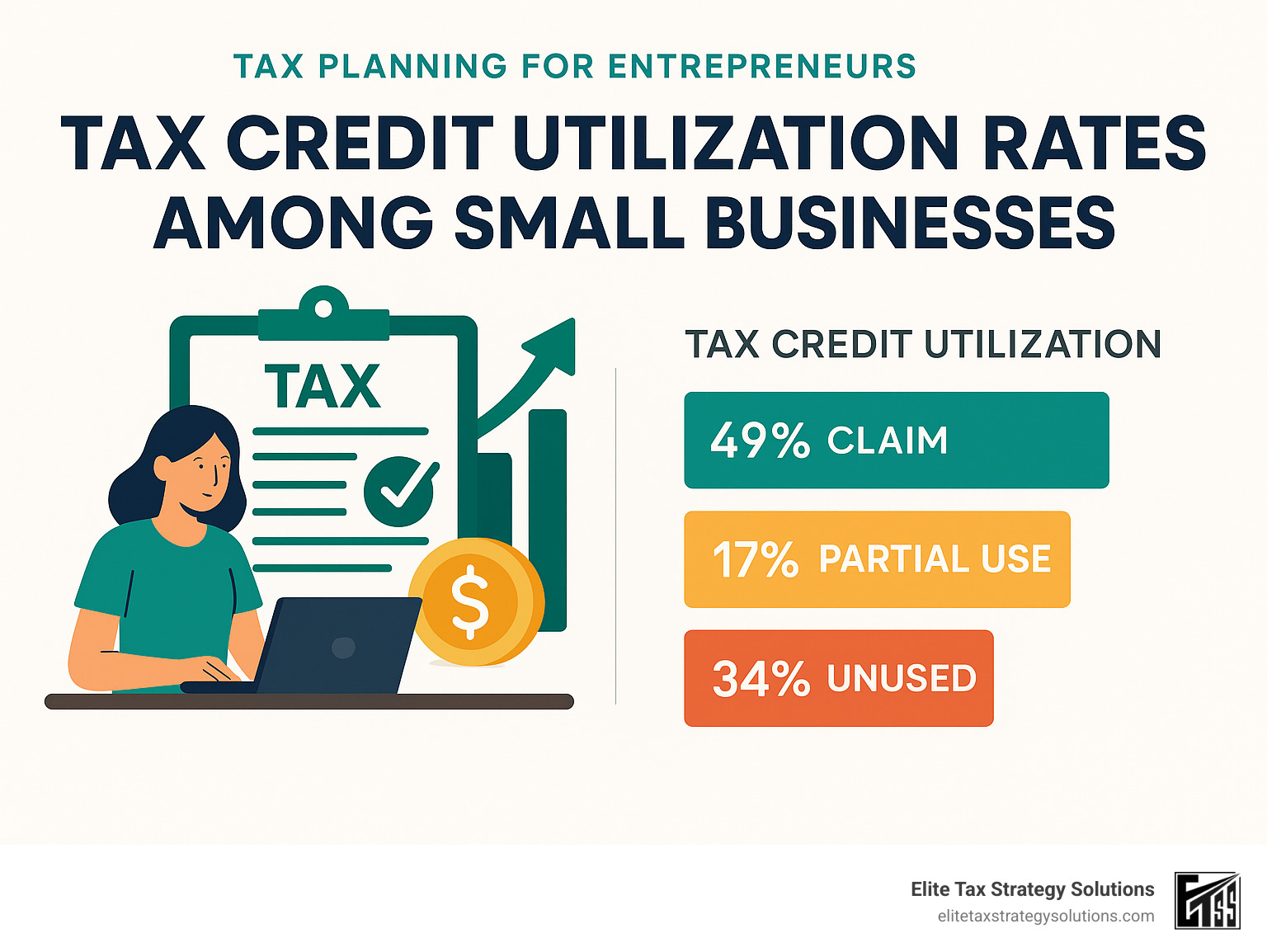

I tell my clients there’s a big difference between deductions and credits—and it’s a difference that can save you thousands. While deductions merely reduce your taxable income, tax credits cut your tax bill dollar-for-dollar. That’s like finding money in your pocket!

Yet I’m constantly surprised by how many entrepreneurs leave these valuable credits on the table. Let me share some of the most powerful ones that could be yours for the taking.

The Research & Development (R&D) Credit is a hidden gem for many businesses. You don’t need to be running a laboratory—if you’re developing new products, improving processes, or creating software, you might qualify for a credit worth up to 14% of your qualifying expenses. This includes wages paid to employees working on innovation, supplies used in the process, and even some contract research costs.

Are you hiring? The Work Opportunity Tax Credit can put up to $9,600 back in your pocket for each eligible employee you bring on board from certain groups. These include veterans, long-term unemployed individuals, and SNAP benefit recipients. One of my clients in Evansville hired three eligible veterans last year and received over $25,000 in credits—money that would have otherwise gone to Uncle Sam.

For those providing health insurance to your team, the Small Business Health Insurance Credit can cover up to 50% of the premiums you pay. Meanwhile, the Disabled Access Credit offers a 50% credit (up to $5,000) for making your facilities more accessible—a win for both your business and the community.

If you’ve made your building more energy-efficient, don’t miss the Section 179D deduction, which allows up to $1.88 per square foot. And speaking of energy, the Clean Vehicle Credit can provide up to $7,500 for qualifying electric vehicles used in your business operations.

Starting a retirement plan? The Retirement Plan Startup Credit can refund up to $5,000 per year for your first three years—essentially subsidizing the cost of helping your employees save for their future.

Tech startups should pay special attention to the Qualified small business payroll tax credit for R&D activities. This gem allows you to offset up to $500,000 in payroll taxes, which can be a lifeline for pre-profit companies.

Of course, don’t forget about all the available deductible expenses that can lower your taxable income. For a deeper dive into maximizing these opportunities, check out our Small Business Tax Saving Strategies page.

Simple Workflow to Document Credits

The IRS loves documentation—and so should you if you’re claiming tax credits. Here’s how to keep things simple and audit-proof:

When claiming the Work Opportunity Tax Credit, complete IRS Form 8850 within 28 days of your eligible employee’s first day. This timing is crucial—I’ve seen business owners miss out simply because they filed a day late. Submit this form to your state workforce agency, keep those time-stamped payroll records showing hours worked, and you’ll be ready to claim your credit at tax time.

For the R&D Credit, documentation is everything. Keep contemporaneous notes about your qualifying activities—”contemporaneous” is tax-speak for “written at the time you did the work.” Track time spent by your team on qualified research and save all related invoices. For larger claims (generally over $50,000), consider investing in a formal R&D study to strengthen your position.

If you’re pursuing energy credits, get certification letters from manufacturers, document your improvements with before-and-after photos, and track energy usage changes. For substantial projects, having a qualified engineer’s certification can provide valuable peace of mind.

I’ll never forget helping a manufacturing client in southern Indiana find over $42,000 in R&D credits for developing new production processes. The look on the owner’s face when we uncovered this “free money” was priceless. With proper tax planning for entrepreneurs, these credits aren’t just for big corporations—they’re for businesses just like yours.

Frequently Asked Questions about Entrepreneurial Tax Strategy

What’s the difference between a deduction and a credit?

When I’m sitting with clients in my office, this is often the first question that comes up. The answer makes a real difference to your bottom line: a tax deduction reduces your taxable income, while a tax credit directly reduces your tax bill dollar-for-dollar.

Let me put that in real terms. If you’re in the 30% tax bracket, a $1,000 deduction might save you about $300. But a $1,000 credit? That’s a full $1,000 back in your pocket, regardless of your tax bracket. This simple distinction is why I always encourage my entrepreneurial clients to hunt for credits first when we’re crafting their tax strategy.

“David,” a client recently told me, “I had no idea the difference was so significant. I’ve been focusing on the wrong things for years!”

How often should I review my entity structure?

Think of your business structure like your wardrobe – what fit perfectly when you started might feel a bit tight as you grow. I recommend my clients review their entity structure at least annually, especially when:

- Your business income takes a significant jump (or drop)

- You bring on new partners or say goodbye to existing ones

- Your business expands into new states or international markets

- Retirement or succession planning appears on your horizon

- Major tax law changes occur (like the upcoming TCJA provision expirations in 2025)

I’ll never forget working with a manufacturing client in Jasper who had operated as a sole proprietorship for five years without reviewing his structure. When we finally sat down together, we finded he had overpaid nearly $47,000 in taxes during that period! A simple switch to an S Corporation structure would have saved him enough to purchase new equipment and hire another employee.

Timing these reviews is important too – don’t wait until tax season when you’re already overwhelmed. Mid-year reviews give you time to implement changes that can affect the current tax year.

Can international expansion increase my U.S. tax bill?

“Going global is exciting, but it can create tax headaches if you’re not careful,” I often tell my clients considering international expansion. Yes, international operations can complicate your tax situation considerably.

As a U.S. citizen or resident, you’re taxed on your worldwide income – a concept that surprises many entrepreneurs. Fortunately, several mechanisms exist to prevent you from paying taxes twice on the same income:

The Foreign Tax Credit allows you to offset your U.S. tax liability with taxes you’ve already paid to foreign governments. One client who expanded to Canada was relieved to learn this would prevent double taxation on her growing business.

The Foreign Earned Income Exclusion can exclude up to $126,500 (2024) of foreign earnings if you meet certain residency requirements abroad.

Tax Treaties between the U.S. and other countries may provide special provisions that reduce taxation in certain scenarios.

Beyond these basics, international tax planning for entrepreneurs requires attention to complex filing requirements like Foreign Bank Account Reports (FBARs) and Form 8938 for foreign assets. The penalties for non-compliance can be severe – I’ve seen penalties exceed $10,000 for simple filing oversights.

A client who operates manufacturing facilities in both Indiana and Mexico told me recently, “Your guidance on structuring our international operations saved us more in taxes than we spent on equipment last year.” With proper planning, international expansion can be both profitable and tax-efficient.

Conclusion

Effective tax planning for entrepreneurs isn’t just about minimizing your current tax bill—it’s about creating a comprehensive strategy that supports your long-term business goals while ensuring full compliance with tax laws.

The strategies we’ve covered—from selecting the optimal business structure to maximizing available credits and deductions—work best when implemented as part of a coordinated plan rather than as isolated tactics.

As the tax landscape continues to evolve, with significant changes on the horizon when many TCJA provisions expire after 2025, working with experienced tax professionals becomes increasingly valuable.

At Elite Tax Strategy Solutions, we specialize in helping entrepreneurs in Jasper, Indiana and surrounding areas develop and implement comprehensive tax strategies custom to their unique situations. Our proactive approach focuses on year-round planning rather than just year-end scrambling, helping our clients legally minimize their tax burdens while avoiding costly mistakes.

The best time to start tax planning is now, not during tax season when options are limited. By implementing these strategies throughout the year, you can significantly reduce your tax liability while positioning your business for long-term success.

For more information about how we can help with comprehensive Tax Planning for Small Businesses, contact us today for a consultation.