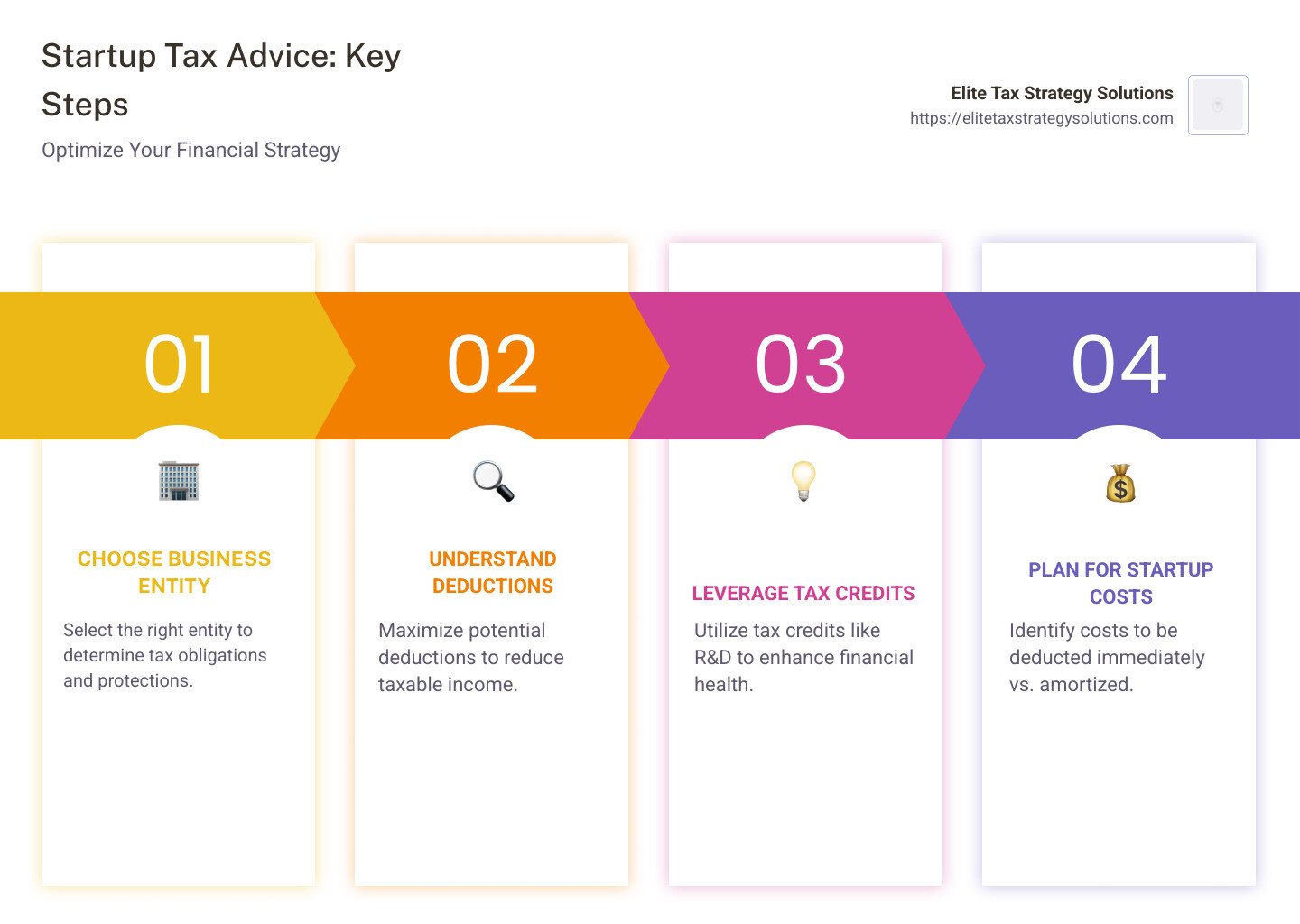

Tax advice for startups matters now more than ever. Starting a new business can be a thrilling ride full of potential and dreams, but it also comes with its own set of problems. Among the biggest of these are understanding tax implications and developing a solid financial strategy. Here are some key points to keep in mind:

- Selecting the right business entity: This decision plays a crucial role in determining your tax obligations and liability protections.

- Understanding deductions and credits: Make sure you’re aware of potential deductions and tax credits like the R&D credit to boost your bottom line.

- Planning for startup costs: Know which costs can be deducted immediately and which need to be amortized over time.

As your business grows, these considerations will help you steer the financial and regulatory landscape more effectively.

I’m David Fritch, and with 40 years of experience in tax and financial strategy, I understand the challenges founders face in ensuring tax compliance while nurturing a startup. My expertise lies in offering comprehensive tax advice for startups, helping them optimize tax savings and achieve their long-term financial goals.

Essential Tax advice for startups terms:

– small business tax planning strategies

– business tax planning services

– how can i save money on taxes

Choosing the Right Business Entity

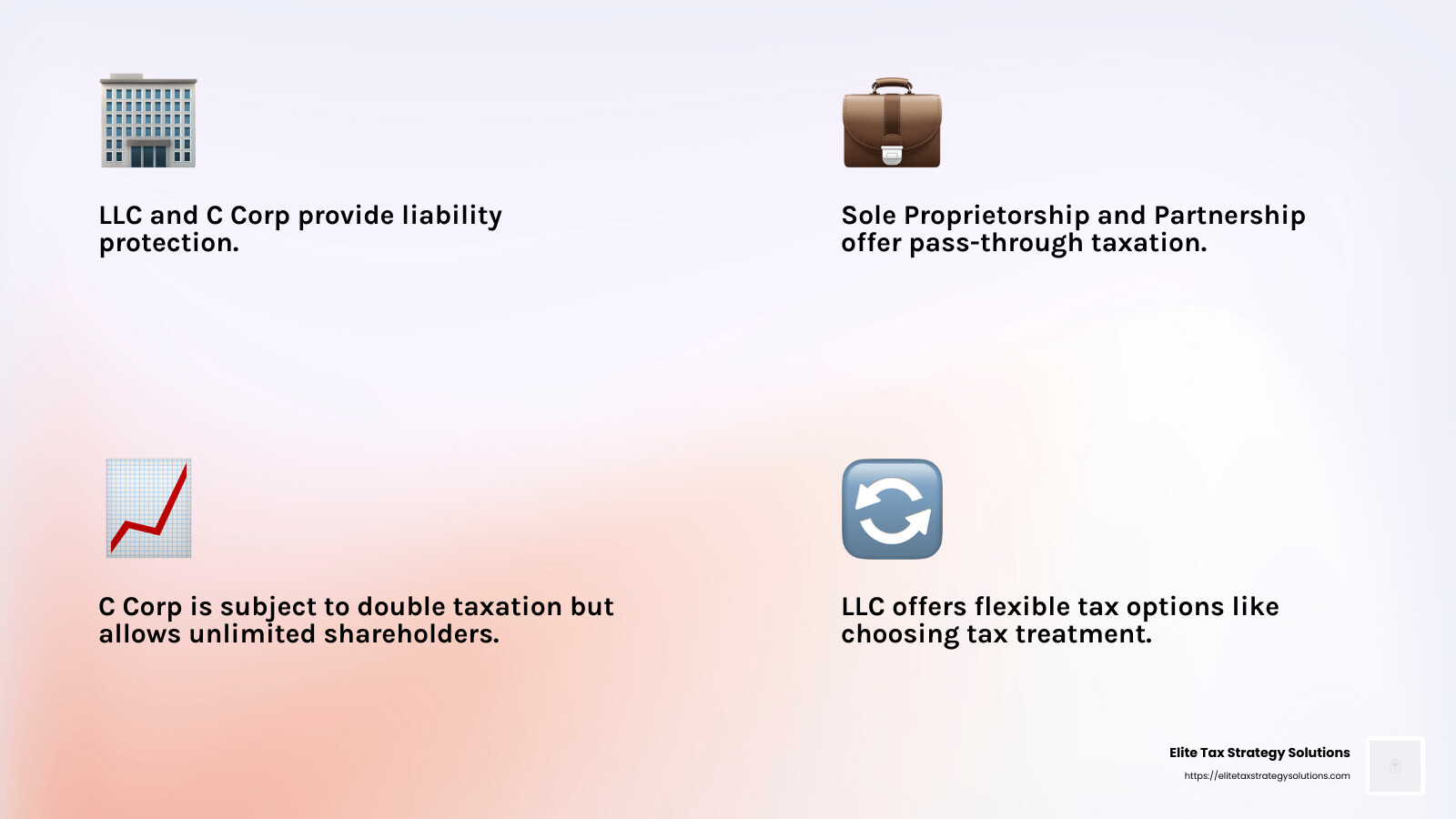

Choosing the right business entity is a pivotal decision for any startup. It lays the foundation for your tax obligations and influences your liability protections. Let’s break down the main options: Sole Proprietorship, Partnership, LLC, S Corporation, and C Corporation.

Sole Proprietorship

A Sole Proprietorship is the simplest form. It’s just you running the show. You report income and expenses on your personal tax return, making tax filing straightforward. However, there’s a catch: you have no liability protection. If the business incurs debt or legal issues, your personal assets are at risk.

Partnership

Partnerships are for two or more people sharing ownership. This entity allows for shared responsibility and resources, but it also means shared liability. Like sole proprietorships, partnerships offer pass-through taxation, meaning the business itself doesn’t pay taxes. Instead, profits and losses are reported on the partners’ individual tax returns.

Limited Liability Company (LLC)

An LLC combines the simplicity of a partnership with the liability protection of a corporation. It offers flexible tax options, allowing you to choose how you want to be taxed—either as a sole proprietorship, partnership, or corporation. This flexibility makes LLCs a popular choice for startups.

S Corporation

S Corporations provide tax advantages by allowing profits to pass through to shareholders without incurring corporate tax. However, there are limitations. For instance, you can have no more than 100 shareholders, and they must be U.S. citizens or residents. S Corporations also require more formalities, like holding regular meetings and maintaining records.

C Corporation

C Corporations are typically for larger businesses. They offer the most robust liability protection and have no restrictions on the number of shareholders. The downside? Double taxation. The corporation pays taxes on its income, and then shareholders pay taxes on dividends. Yet, the flat corporate tax rate and potential for growth can make this option attractive.

Making the Choice

Choosing the right entity depends on your business goals, the level of liability protection you need, and how you want to handle taxes. Consulting with a tax professional can help you weigh the pros and cons of each option.

In the next section, we’ll explore tax deductions and credits that can benefit your startup.

Tax Advice for Startups: Essential Considerations

Navigating taxes can be daunting for startups. Understanding tax deductions and how to handle startup expenses is crucial. Here’s a simplified guide to help you get started.

Startup Expenses and Tax Deductions

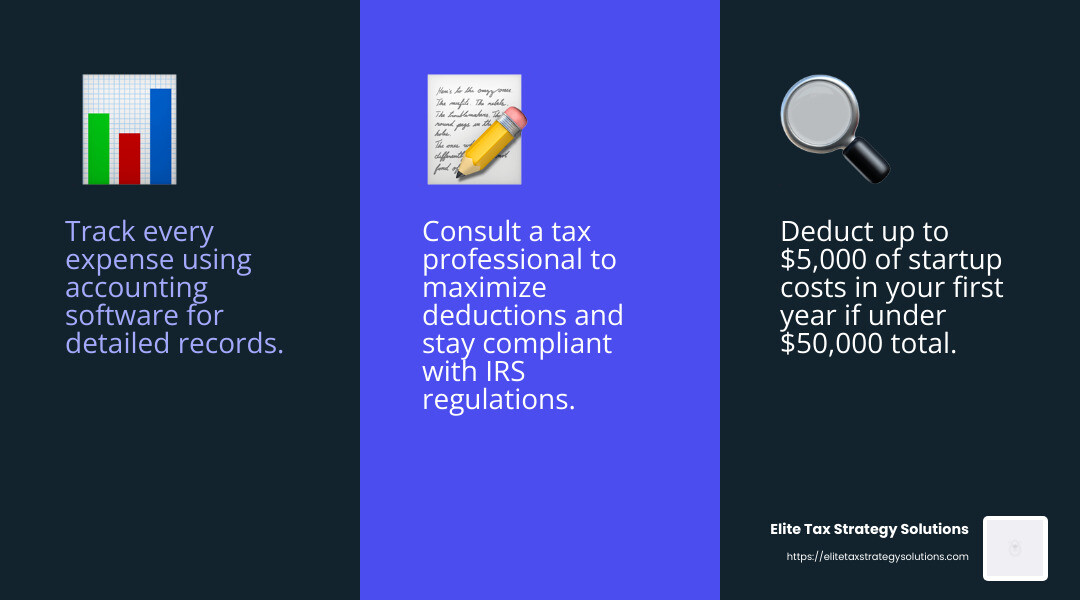

When you’re getting your startup off the ground, you’ll incur numerous expenses. The good news? Many of these can be deducted from your taxes. Startup expenses might include costs for market research, legal fees, and employee training. The IRS allows you to deduct up to $5,000 of startup costs in your first year if your total startup costs are under $50,000. If your expenses exceed this amount, you can amortize them over 15 years.

Amortization vs. Depreciation

Understanding the difference between amortization and depreciation is key. Both are methods of spreading out the cost of an asset over time, but they apply to different types of expenses:

-

Amortization is used for intangible assets like patents and startup costs. It allows you to write off these expenses gradually, which can be beneficial if your startup isn’t profitable right away.

-

Depreciation applies to tangible assets, such as computers and office furniture. This process spreads the cost of these items over their useful life, helping to reduce taxable income.

IRS Regulations

Staying compliant with IRS regulations is essential. Make sure to keep detailed records of all expenses and consult with a tax professional to ensure you’re maximizing your deductions. The tax code can change, so staying informed is crucial. For example, recent changes to Section 174 impact how research and development expenses are capitalized and amortized.

Practical Steps

-

Track Every Expense: Use accounting software to log every cost associated with starting your business.

-

Consult with a Tax Professional: They can help you steer deductions, amortization, and IRS regulations.

-

Plan for the Long Term: Consider how amortizing expenses might benefit you in future profitable years.

By understanding these essential tax considerations, you’ll be better equipped to manage your startup’s finances and keep more money in your pocket.

Next, we’ll dive into exploring tax credits and incentives that can provide additional benefits for your startup.

Exploring Tax Credits and Incentives

Tax credits and incentives can be a game-changer for startups. They can save you money and help your business grow. Let’s break down some of the key opportunities available to you.

R&D Credit

The Research and Development (R&D) tax credit is a valuable tool for startups engaged in innovation. This credit encourages businesses to invest in developing new products, processes, or technologies. Even if your startup is not profitable yet, you might still benefit. For instance, startups can use the R&D credit to offset up to $500,000 in payroll taxes, which can significantly reduce your burn rate.

Innovation Incentives

Many states offer additional innovation incentives to attract tech companies and foster economic growth. These incentives can vary widely, from tax credits for hiring new employees to grants for developing green technologies. Be sure to check your state’s specific offerings to maximize your benefits.

Federal and State Credits

Beyond the R&D credit, there are numerous federal and state credits that your startup might qualify for. These can include credits for energy efficiency, hiring veterans, or even providing childcare for employees. Each credit has its own set of requirements, so research and understand which ones apply to your business.

Tax Benefits

Taking advantage of these tax credits and incentives can provide significant tax benefits. They can lower your taxable income, which means paying less in taxes and having more capital to reinvest in your business. Startups that strategically leverage these benefits can improve their financial stability and accelerate growth.

Practical Steps

-

Research Available Credits: Use online resources or consult with a tax professional to identify all the credits your startup may qualify for.

-

Document Your Activities: Keep detailed records of your R&D activities and other qualifying expenses. This documentation is crucial for claiming credits.

-

Stay Informed: Tax laws and available incentives can change. Regularly check for updates to ensure you’re maximizing your benefits.

By understanding and utilizing these tax credits and incentives, your startup can reduce its tax burden and free up resources to fuel growth. In the next section, we’ll discuss managing startup expenses to further optimize your financial strategy.

Managing Startup Expenses

Managing startup expenses is crucial for keeping your business financially healthy. Let’s explore some key areas like deductible expenses, capital costs, and financial planning, and see how they impact your cash flow.

Deductible Expenses

When you’re starting a business, every dollar counts. Fortunately, the IRS allows you to deduct certain startup expenses, which can lower your taxable income. Deductible expenses include costs like office supplies, legal fees, and marketing efforts. However, you can only deduct these expenses if your business actually launches.

Capital Costs

Startups often incur significant capital costs, such as purchasing equipment or software. These are considered long-term investments in your business. For tax purposes, you can’t deduct the full cost in the year of purchase. Instead, you must spread the deduction over several years through depreciation. This helps you match the expense with the revenue it generates.

Financial Planning

Effective financial planning is vital for managing your startup expenses. It’s important to create a budget that forecasts your income and expenses. This helps you understand your cash flow and ensure you have enough funds to cover your costs. Consider working with a financial advisor or accountant who can help you set realistic financial goals and track your progress.

Cash Flow Impact

Your cash flow is the lifeblood of your startup. It’s essential to monitor it closely, as cash flow issues can lead to serious problems. By carefully managing your deductible expenses and capital costs, you can improve your cash flow. This means having more money available to reinvest in growth opportunities or to cushion against unexpected expenses.

Practical Steps

-

Track Your Expenses: Keep a detailed record of all your business expenses. This will not only help you at tax time but also give you a clear picture of where your money is going.

-

Create a Budget: Develop a budget that outlines your expected income and expenses. Regularly review and adjust it as needed to stay on track.

-

Plan for Depreciation: Understand which of your capital costs need to be depreciated and plan accordingly. This will help you manage your tax deductions effectively.

-

Consult a Professional: Consider hiring a CPA or financial advisor to help you steer the complexities of startup expenses and ensure you’re maximizing your financial resources.

By managing your startup expenses wisely, you can strengthen your financial foundation and set your business up for long-term success. In the next section, we’ll explore equity compensation and its tax implications.

Equity Compensation and Tax Implications

Equity compensation can be a powerful tool for startups. It helps attract and retain talented employees without the immediate cash outlay. But it’s important to understand the tax implications.

Equity Options

Startups often offer equity options to employees as part of their compensation package. This gives employees the right to buy company stock at a set price in the future. There are two main types: Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NSOs).

Incentive Stock Options (ISOs)

ISOs offer tax advantages for employees but come with strict rules. If employees hold the stock for at least two years from the grant date and one year from the exercise date, they might qualify for favorable tax treatment. This means they could pay long-term capital gains tax instead of ordinary income tax on the profits.

However, the company must meet eligibility requirements, and ISOs can’t be granted to non-employees. For startups, offering ISOs can be appealing, but it’s important to ensure compliance with these rules.

Non-Qualified Stock Options (NSOs)

NSOs are more flexible and can be offered to employees, consultants, and directors. They don’t have the same tax benefits as ISOs. When employees exercise NSOs, they pay ordinary income tax on the difference between the exercise price and the fair market value. This can lead to a higher tax bill, but the flexibility makes NSOs a popular choice for startups.

Employee Retention

Using equity compensation is not just about saving cash. It’s also a strategy to align employees’ interests with the company’s success. When employees own a piece of the company, they’re more likely to stay and work towards its growth. This is especially important for startups that rely heavily on their teams to drive innovation and progress.

Practical Steps

-

Understand the Types: Learn the differences between ISOs and NSOs. Decide which is best for your company and employees.

-

Consult with Experts: Work with tax professionals to ensure compliance with tax laws and to structure your equity plans effectively.

-

Communicate Clearly: Make sure your employees understand the terms and tax implications of their equity compensation. This transparency can foster trust and commitment.

-

Plan for Taxes: Consider the tax impact on both the company and employees. Proper planning can help avoid unexpected tax liabilities.

By carefully considering equity compensation and its tax implications, startups can create incentives that benefit both the company and its employees. In the next section, we’ll dive into international and state tax considerations that startups need to keep in mind.

International and State Tax Considerations

As startups grow, they often expand beyond their initial markets, which brings new tax considerations. Understanding both international and state tax obligations is crucial to avoid surprises and maintain compliance.

International Tax

For startups with global aspirations, international tax considerations are key. The U.S. has a quasi-worldwide tax system for corporations, meaning U.S. companies may owe taxes on foreign income. This can get complicated with rules like GILTI (Global Intangible Low-Taxed Income), which taxes foreign earnings to discourage profit shifting to low-tax countries.

To steer these complexities:

-

Plan Ahead: Structure your international operations thoughtfully to minimize tax burdens. Consider where you locate intellectual property and R&D activities.

-

Stay Compliant: Ensure you comply with both U.S. and foreign tax laws. This includes filing necessary forms, like Form 5471, to report ownership in foreign corporations.

-

Use Tax Credits: Take advantage of foreign tax credits to reduce double taxation on international profits.

State and Local Taxes

In the U.S., startups must also consider state and local taxes. These can include corporate income taxes, franchise taxes, and sales taxes. Each state has different rules, so it’s important to:

-

Know Your Nexus: Determine where your business has a tax “nexus” or connection. This could be where you have employees, property, or significant sales.

-

Stay Updated: Tax laws change frequently. For example, the South Dakota v. Wayfair decision allows states to collect sales tax from remote sellers, even without physical presence.

-

Plan for Sales Tax: If you sell software or digital products, many states now require sales tax collection. Approximately 25 states tax SaaS models, and this landscape is evolving.

Compliance

Compliance with tax laws is not just about avoiding penalties. It’s about building a solid foundation for growth. Here are some tips:

-

Keep Accurate Records: Good record-keeping is essential. It helps in audits and when claiming deductions or credits.

-

Consult Professionals: Work with tax experts to steer complex tax landscapes. They can provide insights and strategies to optimize your tax position.

-

Regular Reviews: Revisit your tax strategy regularly to adapt to changing laws and business circumstances.

By understanding and planning for international and state tax obligations, startups can avoid pitfalls and position themselves for success. Next, we’ll tackle some frequently asked questions about startup taxes.

Frequently Asked Questions about Startup Taxes

Can you write off startup costs on taxes?

Yes, you can write off certain startup costs on your taxes. The IRS allows startups to deduct expenses related to creating and launching a business. These costs are typically categorized into three main areas:

-

Creating the Business: Costs for market research, feasibility studies, and travel for site selection.

-

Launching the Business: Expenses for licenses, hiring, and training employees, as well as initial marketing efforts.

-

Organizational Costs: Fees for setting up a legal entity like an LLC or corporation.

However, you can’t deduct these costs if your business doesn’t actually launch. For startups beginning operations, you can generally deduct up to $5,000 in startup costs and another $5,000 in organizational costs in the first year, as long as total startup costs are under $50,000. If your costs exceed this, the deduction decreases.

What are the tax rules for start-ups?

Startups need to steer various tax rules, including franchise tax and corporate income tax:

-

Franchise Tax: Some states impose a franchise tax on businesses for the privilege of operating within the state. It’s not based on income, so even if you’re not making money yet, you might owe this tax.

-

Corporate Income Tax: If you’ve structured your startup as a corporation, you’ll need to pay corporate income tax on profits. This applies to C corporations, which face double taxation on earnings and dividends. S corporations, on the other hand, pass income to shareholders to be taxed at individual rates, avoiding double taxation.

To ensure compliance, startups should:

-

Understand State Requirements: Each state has different rules. Know where your business has a tax obligation.

-

File Correctly: Keep track of deadlines and necessary forms to avoid penalties.

Do I get a tax break for starting a business?

Starting a business does come with potential tax breaks:

-

Deductions: As mentioned, you can deduct certain startup and organizational costs. Additionally, regular business expenses like rent, salaries, and office supplies are deductible.

-

Amortization: Some costs, like those for establishing a corporation, can be amortized over time, spreading the deduction across several years. This can be beneficial if your startup isn’t immediately profitable.

It’s crucial to maintain good records and consult with a tax professional to maximize these benefits. By understanding these tax rules and opportunities, startups can optimize their financial strategy and reduce their tax burden.

Next, we’ll explore how equity compensation and its tax implications can play a role in attracting and retaining top talent for your startup.

Conclusion

Navigating the tax landscape is crucial for any startup aiming to thrive. Tax compliance isn’t just about avoiding penalties—it’s about setting a solid foundation for growth. At Elite Tax Strategy Solutions, we understand the unique challenges startups face. Our proactive approach to tax planning aims to maximize your tax savings while ensuring financial stability.

By staying ahead of tax regulations, you can avoid costly mistakes and focus on what matters most: growing your business. We offer custom strategies that align with your business model, ensuring that you’re not only compliant but also optimized for success.

Taxes are not just a yearly chore. They are an integral part of your startup’s financial strategy. With the right guidance, you can leverage tax rules to your advantage, securing a stronger financial footing and paving the way for future growth.

For startups ready to take control of their financial destiny, partnering with a knowledgeable tax advisor is a wise move. At Elite Tax Strategy Solutions, we’re here to help you turn your idea into income with confidence.

Explore more about how we can assist your startup on our Tax Planning for Small Businesses page. Let us be your guide on the path to financial success.