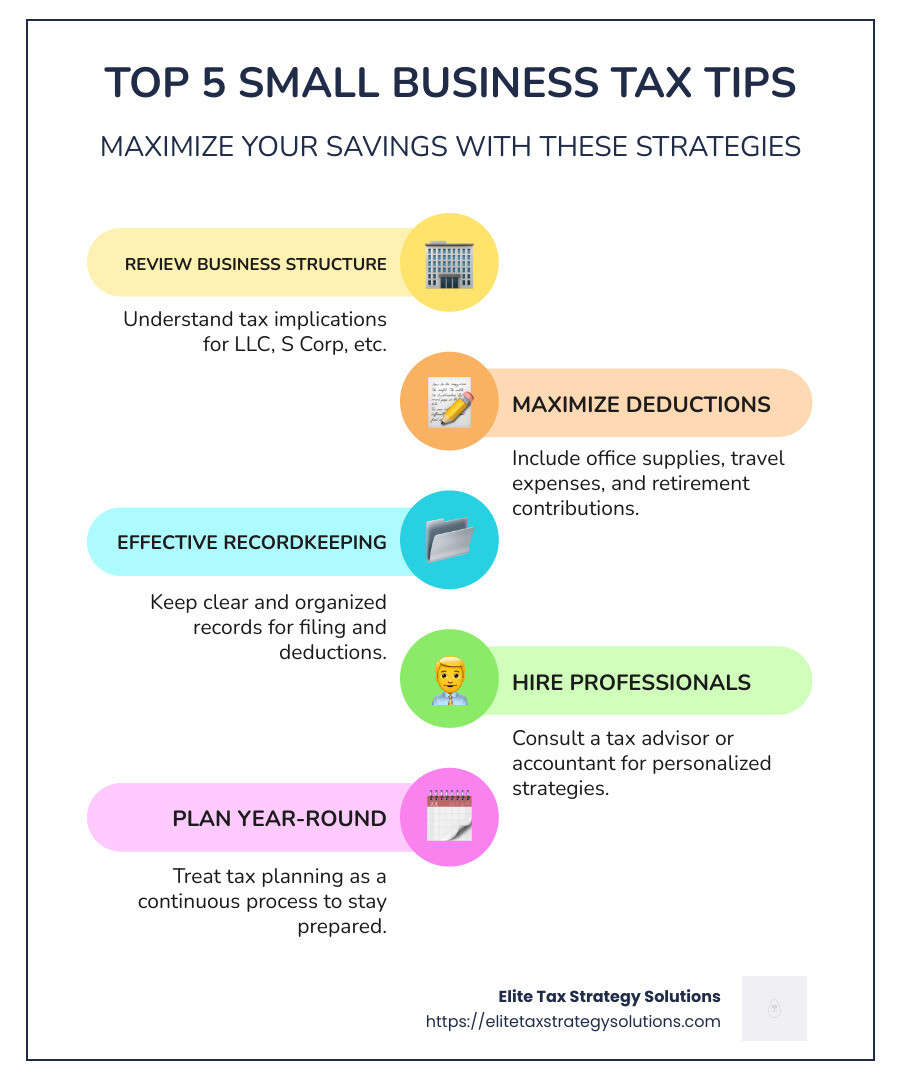

Small business tax tips can make a significant difference in your financial stability and overall business success. Whether you’re aiming to reduce your tax burden or steer through the complexities of tax regulations, these foundational tips can help:

- Review Your Business Structure: Understand the tax implications of your business classification, whether it’s an LLC, S Corp, or another form.

- Maximize Deductions: Don’t overlook eligible deductions such as office supplies, travel expenses, and retirement contributions.

- Implement Effective Recordkeeping: Maintain clear and organized records to streamline your tax filing and support any deductions.

- Consider Hiring Professionals: A tax advisor or accountant can provide personalized strategies to optimize your tax outcome.

- Plan Year-Round: Treat tax planning as a continuous process rather than a yearly task to ensure you’re always prepared.

My name is David Fritch. With 40 years of experience owning a law firm and CPA practice, I specialize in strategies designed to streamline tax processes for small businesses, offering expertise in maximizing tax savings and fostering financial stability.

Basic small business tax tips terms:

– business expense categories

– business expenses examples

– how can i save money on taxes

Essential Tax Deductions for Small Businesses

Navigating tax deductions can feel like exploring a dense jungle. But fear not! We’re here to guide you through the thicket of deductible expenses that can help your small business thrive.

Understanding Business Expenses

First things first, let’s break down what business expenses are. These are costs that are necessary and ordinary for your business operations. Think of things like office supplies, utilities, rent, and even wages. By deducting these expenses, you lower your taxable income, which reduces the amount you owe to Uncle Sam.

Common Tax Write-Offs

Here are some common tax write-offs you should be aware of:

- Office Supplies: Pens, paper, and printer ink might seem small, but they add up. Keep receipts for everything.

- Travel Expenses: If you travel for business, you can deduct costs like airfare, hotels, and even meals.

- Home Office Deduction: If you work from home, you might qualify for this deduction. You can simplify the process by using the $5 per square foot method or the standard method, where you track actual expenses.

The Power of Deductions

Let’s look at an example to see the impact of deductions. Imagine Joe, a self-employed writer, who finded $6,000 in contractor expenses he initially missed. By claiming these deductions, Joe reduced his taxable income from $60,000 to $54,000, saving over $1,500 in taxes!

“Adding the additional business expenses saved Joe over $1,500 in taxes!”

Maximize Your Deductions

To make the most of your deductions, keep these tips in mind:

- Stay Organized: Use bookkeeping software to track expenses throughout the year.

- Consult a Professional: A CPA or tax advisor can help you uncover deductions you might miss.

- Plan Ahead: Treat tax planning as a year-round task, not just something you scramble to do in April.

By understanding and utilizing these small business tax tips, you can significantly reduce your tax burden and keep more money in your pocket. Next, we’ll explore how maximizing retirement contributions can further improve your tax strategy.

Maximize Retirement Contributions

Saving for retirement is not just smart for your future—it’s also a savvy tax strategy. Small business owners can leverage retirement plans to reduce taxable income and secure their financial future. Let’s explore how small business tax tips related to retirement contributions can benefit you.

Retirement Plans: A Tax-Friendly Savings Tool

There are several retirement plans custom for small business owners. Each offers unique benefits and tax advantages:

-

SIMPLE IRA: Easy to set up and manage, the SIMPLE IRA allows both employer and employee contributions. Employers can match employee contributions up to 3% of their salary, or make a 2% non-elective contribution. Contributions are tax-deductible, reducing your taxable income.

-

SEP IRA: The SEP IRA is ideal for self-employed individuals and small business owners with few employees. You can contribute up to 25% of your income, up to $69,000 for 2024. Contributions are tax-deductible, and you can decide how much to contribute each year.

-

401(k) Plans: A traditional 401(k) allows employees to save pre-tax income, which lowers their taxable income. Employers can also contribute, with total contributions (employee and employer) capped at $69,000 for those under 50. For those 50 and older, there’s an additional catch-up contribution of $7,500. A one-participant 401(k), or solo 401(k), is a great option for business owners without employees, covering both the owner and their spouse.

Using Tax Credits

Starting a retirement plan can also bring tax credits. The IRS offers a credit of up to $5,000 for three years to offset the costs of setting up a SEP, SIMPLE IRA, or 401(k) plan. This credit can make establishing a retirement plan more affordable and attractive.

Real-Life Impact

Consider Susan, a small business owner in Indiana, who decided to set up a SEP IRA. By contributing $15,000 in 2023, she not only saved for her retirement but also reduced her taxable income by the same amount. This strategic move lowered her tax bill, allowing her to reinvest the savings back into her business.

“Contributing to a SEP IRA helped Susan cut her taxable income and invest in her future.”

Key Takeaways

- Choose the Right Plan: Evaluate your business needs to select the most suitable retirement plan.

- Contribute Regularly: Maximize contributions to reduce your taxable income.

- Leverage Tax Credits: Use available tax credits to lower the cost of starting a plan.

By maximizing retirement contributions, you not only prepare for the future but also optimize your current tax strategy. Next, we’ll dive into how equipment and green energy tax credits can further benefit your small business.

Equipment and Green Energy Tax Credits

Investing in equipment and green energy can be a win-win for your small business. Not only can you improve your operations, but you can also take advantage of valuable tax credits. Let’s explore how these small business tax tips can help you save money.

Equipment Deductions: Section 179 and Bonus Depreciation

Buying new or used equipment for your business can lead to significant tax savings. Under Section 179, you can expense up to $1,220,000 of equipment costs in 2024. However, this benefit starts to phase out if your total equipment purchases exceed $3.05 million.

If you’ve already hit the Section 179 limit, you can still benefit from bonus depreciation. For 2024, you can deduct 60% of the equipment’s cost basis. This means if you buy a $10,000 machine, you can write off $6,000 immediately.

Pro Tip: Timing is crucial. If your business had a tough year, consider delaying big purchases to maximize deductions in a more profitable year.

Green Energy Initiatives: Inflation Reduction Act

The federal Inflation Reduction Act, signed in 2022, offers nearly $400 billion in clean energy tax credits. These credits promote investment in eco-friendly technologies and can significantly reduce your tax bill.

- Electric and Hybrid Vehicles: Receive tax credits for purchasing new or used electric or hybrid vehicles for your business fleet.

- Clean Energy Installations: Installing solar panels or other renewable energy systems can qualify for federal income tax credits.

- State Incentives: Check if your state offers additional green energy incentives to further lower costs.

“Investing in green energy is not just good for the planet—it’s good for your business’s bottom line.”

Real-Life Impact

Imagine you own a small manufacturing company in Jasper, Indiana. You decide to invest in energy-efficient machinery and solar panels. By leveraging Section 179 for the equipment and the Inflation Reduction Act for solar installation, you significantly reduce your taxable income and operational costs.

Key Takeaways

- Plan Your Purchases: Use Section 179 and bonus depreciation to maximize tax savings on equipment.

- Go Green: Explore federal and state tax credits for investing in clean energy solutions.

- Consult a Professional: Tax incentives can be complex. A tax advisor can help identify all available credits.

By strategically investing in equipment and green energy, you not only improve your business operations but also enjoy substantial tax benefits. Next, we’ll cover best practices for record keeping and bookkeeping to ensure you capture all these savings.

Record Keeping and Bookkeeping Best Practices

Effective record keeping is the backbone of any successful small business. It helps you stay organized, track expenses, and maximize your tax deductions. Let’s explore some small business tax tips for managing your records and bookkeeping.

Organize Your Records

Keeping your records organized is crucial for smooth tax filing and financial management. Whether you prefer digital or physical files, consistency is key.

- Alphabetize or Code: Use a simple system like alphabetizing or client codes to make retrieval easy.

- Chronological Order: Sort documents by date to track expenses over time.

Pro Tip: Use folders or labels to keep everything in its place. This saves time when you need to find something quickly.

Use Bookkeeping Software

Technology can simplify your bookkeeping tasks. Accounting software can automate many processes, making it easier to maintain accurate records.

- Track Expenses: Sync your financial accounts to track transactions automatically.

- Generate Reports: Create financial statements with a few clicks.

- Ensure Accuracy: Double-check transactions to avoid mistakes.

“Investing in good bookkeeping software is like hiring a diligent assistant who never sleeps.”

Document Retention

Knowing how long to keep your business records is essential. Federal, state, and local laws vary, so research your region’s requirements.

- Receipts and Invoices: Keep these for at least three years, as they support your tax deductions.

- Employee Records: These may need to be retained longer, especially if they involve medical or legal matters.

Pro Tip: Scan paper documents to create digital backups. This not only saves space but also protects against loss or damage.

Secure Your Records

Security is vital, especially when dealing with sensitive information.

- Password Protection: Use passwords for digital files and folders.

- Physical Security: Lock up physical records in a secure location.

“Keeping your records secure is not just good practice; it’s a legal obligation for many types of business information.”

Real-Life Impact

Consider a small business owner in a suburban area near a major city. By implementing a robust record-keeping system and using bookkeeping software, they streamline their tax filing process and minimize errors. This organization leads to fewer headaches and potential savings during tax season.

Key Takeaways

- Stay Organized: Use simple systems to keep your records easy to access.

- Leverage Technology: Bookkeeping software can save you time and reduce errors.

- Know the Rules: Understand document retention requirements for your area.

- Protect Your Data: Ensure your records are secure from unauthorized access.

By following these best practices, you can simplify your bookkeeping and ensure you capture all potential tax savings. Next, we’ll explore small business tax tips for reducing taxable income.

Small Business Tax Tips for Reducing Taxable Income

Reducing taxable income is a smart strategy for small business owners. Let’s explore some small business tax tips to help you keep more of your hard-earned money.

Employ Family

Hiring family members can be a win-win situation. Not only do you provide income for your loved ones, but you also enjoy tax benefits.

- Hire Your Spouse: If your business is a sole proprietorship, hiring your spouse can save on Federal Unemployment Tax (FUTA) as their wages are exempt.

- Employ Your Children: Children under 18 are not subject to Social Security and Medicare taxes. Plus, earned income allows them to contribute to a retirement account like a Roth IRA, setting them up for future financial success.

“Employing family can create a supportive work environment while offering tax advantages.”

Travel Expenses

Business travel expenses can add up, but they are deductible if properly documented. Keep track of all travel-related costs, including:

- Transportation: Airfare, car rentals, and mileage for business trips.

- Lodging: Hotel stays and other accommodations while away for business.

- Meals: Meals are 50% deductible when traveling for business purposes.

Pro Tip: Always keep receipts and records of the business purpose for each trip to substantiate your deductions.

Business Losses

Experiencing a business loss isn’t ideal, but it can offer tax relief. You can often use these losses to offset other income, reducing your overall tax liability.

- Net Operating Loss (NOL): If your expenses exceed your income, you may be able to carry the loss forward to reduce future taxable income.

- Strategic Planning: Consult with a tax professional to explore how best to use business losses to your advantage.

“Understanding how to leverage business losses can be a powerful tool in managing your taxes.”

Real-Life Example

Imagine a small business owner in Jasper, Indiana, who hires their teenage children to help with seasonal work. By doing so, they save on payroll taxes while teaching valuable work skills. Additionally, they carefully track travel expenses for conferences and meetings, ensuring they capture all eligible deductions. In a challenging year, they use business losses to lower their taxable income, easing their financial burden.

Key Takeaways

- Hire Family: Employing family members can provide tax savings and support your household.

- Track Travel Costs: Keep detailed records to claim travel-related deductions.

- Use Losses: Use business losses strategically to reduce taxable income.

By implementing these strategies, small business owners can effectively manage their tax liabilities and keep more money in their pockets. Next, we’ll tackle some frequently asked questions about small business taxes.

Frequently Asked Questions about Small Business Taxes

How to pay less taxes for a small business?

Paying less in taxes is a common goal for small business owners. Here are some strategies to help you achieve that:

-

Qualified Business Income (QBI) Deduction: Thanks to the Tax Cuts and Jobs Act, eligible businesses can deduct up to 20% of their qualified business income. This deduction is available for sole proprietorships, partnerships, and S corporations. It’s a significant opportunity to lower your taxable income.

-

Maximize Deductions: Keep meticulous records of all business expenses. Deductions for items like office supplies, utilities, and travel can add up quickly and reduce your taxable income.

-

Hire a CPA: A Certified Public Accountant can help identify all possible deductions and credits. They can also provide guidance on tax strategies specific to your business structure.

How much should a small business put away for taxes?

Setting aside money for taxes is crucial to avoid surprises at tax time. Here’s a simple approach:

-

Estimate Your Tax Rate: Small businesses should generally set aside 25% to 30% of their income for federal taxes. This includes income tax, self-employment tax, and any applicable state taxes.

-

Quarterly Estimated Taxes: If you’re an LLC, sole proprietorship, or partnership, you may need to make estimated tax payments quarterly. This helps spread out the tax burden and avoids penalties.

-

Track Income and Expenses: Use bookkeeping software to help track your income and expenses throughout the year. This ensures you’re setting aside the right amount for taxes.

What are the best tax-saving strategies for small businesses?

Implementing effective tax-saving strategies can significantly impact your business’s bottom line:

-

LLC Taxation Options: An LLC can choose how it wants to be taxed—either as a sole proprietorship, partnership, or corporation. Each has different tax implications, so consider which structure offers the most tax benefits for your business.

-

Track Receipts: Maintain a detailed record of all receipts and business transactions. This documentation is crucial for claiming deductions and avoiding issues during an audit.

-

Use Tax Software: Consider using tax software to streamline the filing process. These tools can help ensure accuracy and uncover deductions you might miss.

By following these small business tax tips, you can minimize your tax liability and keep more of your profit. Next, we’ll dig into the conclusion, highlighting how Elite Tax Strategy Solutions can assist with proactive tax planning and personalized services.

Conclusion

Navigating small business taxes can feel overwhelming, but you don’t have to go it alone. At Elite Tax Strategy Solutions, we specialize in turning tax challenges into opportunities for savings and growth. Our proactive tax planning and personalized services are designed to help you keep more of your hard-earned money.

We understand that every business is unique. That’s why we tailor our tax strategies to fit your specific needs. Whether it’s maximizing deductions, optimizing your business structure, or planning for retirement contributions, our team of seasoned professionals is here to guide you every step of the way.

Imagine a future where tax season is stress-free, and your financial goals are within reach. With our expertise, you can focus on what you do best—running your business—while we handle the complexities of tax compliance and optimization.

Ready to take control of your tax strategy? Learn more about our tax planning for small businesses and find how we can help you achieve financial stability and success.

Let us be your partner in navigating the numbers, so you can focus on building your business.