Small business tax saving strategies are essential for entrepreneurs aiming to minimize tax liabilities and boost long-term profitability. In today’s dynamic business landscape, having a proactive tax plan can significantly reduce financial stress and improve overall financial stability. Here are some quick methods to mitigate tax burdens:

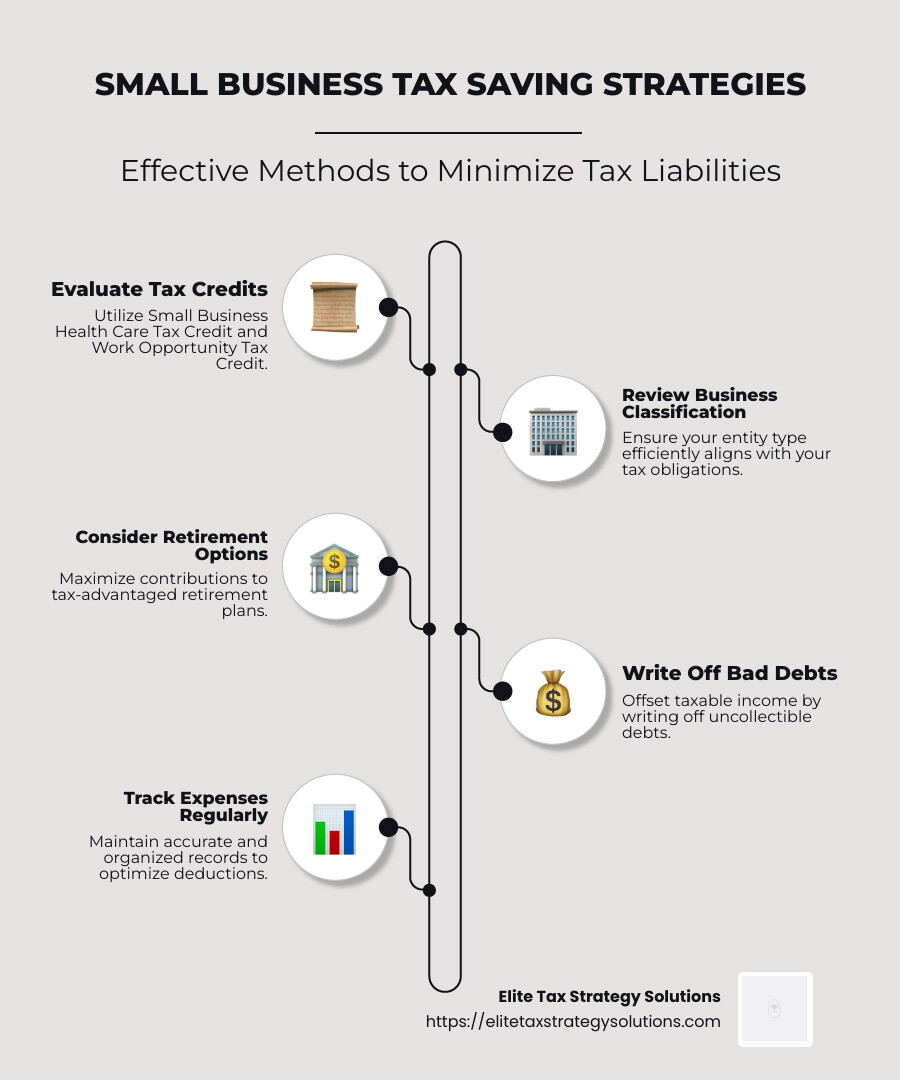

- Evaluate Tax Credits: Use credits like the Small Business Health Care Tax Credit and Work Opportunity Tax Credit.

- Review Your Business Classification: Ensure your entity type efficiently aligns with your tax obligations.

- Consider Retirement Options: Maximize contributions to tax-advantaged retirement plans.

- Write Off Bad Debts: Offset taxable income by writing off uncollectible debts.

As a small business owner, mastering these strategies is crucial for navigating your tax obligations while concurrently planning for financial stability. This guide will equip you with actionable insights to manage taxes effectively throughout the year.

My name is David Fritch, and I bring over 40 years of experience in tax planning, focusing on helping small business owners manage taxes and optimize profits. Let’s explore these small business tax saving strategies in detail to set your business on a path toward financial success.

Small business tax saving strategies terminology:

– small business tax strategies

– how can i save money on taxes

– business expense categories

Employ Family Members

One effective way to save on taxes is to hire family members. It’s a strategy that not only benefits your business but also your family.

Payroll Benefits

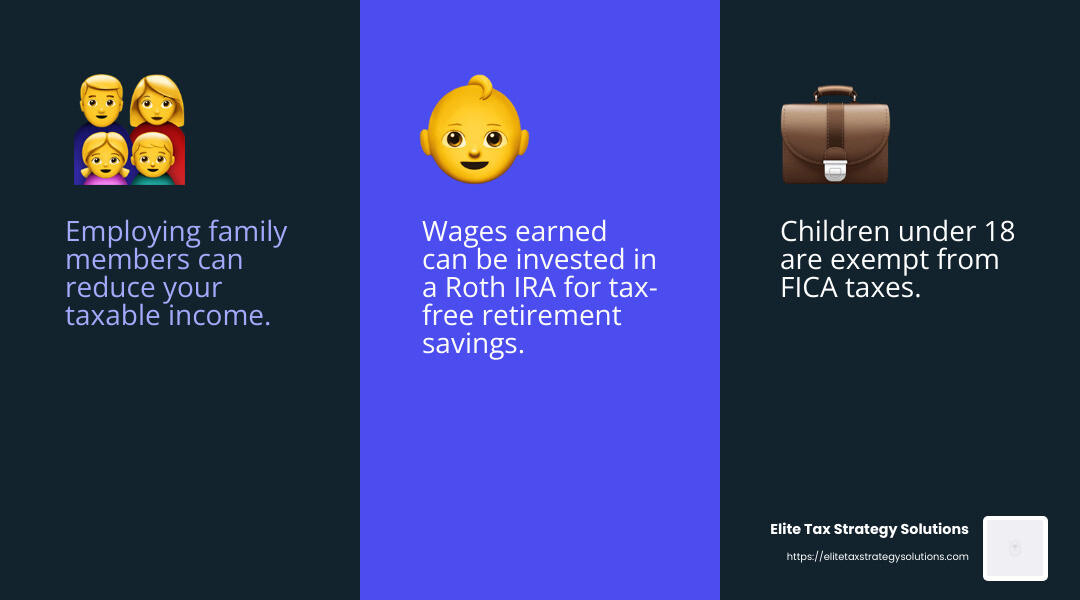

When you put family members on the payroll, you can reduce your taxable income. For instance, hiring your spouse as an employee can save on certain taxes. Their wages are subject to federal income tax and FICA taxes, but not FUTA, as long as they are not a business partner. This can be a smart move, especially for sole proprietorships.

Tax-Free Income for Children

Hiring your children can be even more beneficial. Children under 18 are exempt from FICA taxes, and those under 21 don’t pay FUTA taxes. This means that employing your kids not only helps them gain work experience but also provides tax savings for your business.

Moreover, the income they earn can be invested in a Roth IRA, setting them up for a tax-free retirement. Starting early with retirement savings can have a huge impact on their future financial stability.

Real-Life Example

Consider a small business owner in Jasper, Indiana, who hired his teenage daughter to manage social media accounts. By doing so, he saved on payroll taxes and taught her valuable skills. The income was used to fund her Roth IRA, providing her with a head start on retirement savings.

By employing family members, you can reduce payroll costs and provide your loved ones with valuable work experience and financial benefits. It’s a win-win strategy for your business and family.

Next, we’ll dig into how funding a retirement plan can offer significant tax advantages for your small business.

Fund a Retirement Plan

Saving for retirement isn’t just about securing your future. It’s also a smart way to reduce your tax burden today. By setting up a retirement plan for your small business, you can make tax-deductible contributions and lower your taxable income.

SEP IRA

A Simplified Employee Pension (SEP) IRA is a popular choice for small business owners due to its simplicity and high contribution limits. In 2024, you can contribute up to $69,000 or 25% of your compensation, whichever is less. This plan is easy to set up and administer, making it ideal for busy entrepreneurs. Plus, contributions are tax-deductible, providing immediate tax savings.

SIMPLE IRA

The Savings Incentive Match Plan for Employees (SIMPLE) IRA is another great option. It allows both employers and employees to contribute, with a maximum contribution limit of $17,500 in 2024. Employers can match employee contributions, up to 3% of their salary, or make a 2% non-elective contribution. SIMPLE IRAs are easy to maintain and also offer tax-deductible contributions.

One-Participant 401(k)

For those running a solo business or a business with only a spouse as an employee, a one-participant 401(k), often called a “solo 401(k),” can be a powerful tool. In 2024, you can defer up to $69,000 in income if you’re under 50, with an additional $7,500 catch-up contribution if you’re 50 or older. This plan allows for substantial contributions, which are tax-deductible, and can cover both you and your spouse.

Real-Life Example

Consider a small business owner in a suburban area near a major city. By setting up a SEP IRA, she was able to significantly reduce her taxable income while saving for retirement. The tax savings allowed her to reinvest in her business, fueling further growth.

Funding a retirement plan is a crucial part of small business tax saving strategies. Not only does it help secure your future, but it also provides immediate tax benefits. Next, we’ll explore how optimizing your business structure can lead to even more tax savings.

Optimize Business Structure

Choosing the right business structure can have a big impact on your taxes. For small businesses, pass-through entities like LLCs and S corporations offer unique tax advantages that can save you money.

Pass-Through Entities

Pass-through entities are business structures where the income “passes through” to the owners’ personal tax returns. This means the business itself doesn’t pay income tax. Instead, the owners do, based on their personal tax rates. LLCs and S corporations are popular pass-through entities.

LLC (Limited Liability Company)

An LLC is a flexible and simple structure. It combines the liability protection of a corporation with the tax benefits of a partnership. LLC owners report business income on their personal tax returns, avoiding double taxation. This structure is ideal for small business owners who want to keep things straightforward while enjoying tax savings.

S Corporation

An S corporation offers similar benefits to an LLC but with some differences. It allows income, deductions, and credits to pass through to shareholders, avoiding corporate taxes. However, S corporations have stricter regulations, like limits on the number and type of shareholders. They can be a great option for businesses looking to minimize self-employment taxes, as only salaries (not distributions) are subject to these taxes.

Real-Life Example

Consider a family-owned bakery in Jasper, Indiana. By switching from a sole proprietorship to an LLC, they saved thousands in taxes. The owners could reinvest these savings into expanding their product line, boosting their business growth.

Optimizing your business structure is a key part of small business tax saving strategies. By choosing the right entity, you can reduce your tax burden and keep more money in your pocket.

Next, we’ll dive into maximizing equipment deductions and green energy credits to further improve your tax savings.

Maximize Equipment Deductions and Green Energy Credits

Investing in new equipment or going green can significantly reduce your tax bill. Let’s explore how Section 179, bonus depreciation, and clean energy incentives can help you save.

Section 179 Deduction

Section 179 allows you to deduct the full cost of qualifying equipment purchased or financed during the tax year. For 2024, the deduction limit is $1,220,000. This means if you buy a new oven for your bakery, you can write off the entire cost, reducing your taxable income.

However, be mindful of the spending cap. The deduction begins to phase out once your total equipment purchases exceed $3.05 million. Timing your purchases wisely can help you maximize this deduction.

Bonus Depreciation

If you’ve hit the Section 179 limit, bonus depreciation is another way to lower your tax bill. For 2024, you can deduct 60% of the cost basis for eligible property. Unlike Section 179, there’s no spending cap, making it a great option for larger investments.

For example, if your business invests in a fleet of delivery vehicles, you can take advantage of bonus depreciation to claim a significant deduction. This can be particularly beneficial if you expect higher profits next year, as it reduces your taxable income now.

Clean Energy Incentives

The federal government offers incentives to encourage businesses to invest in clean energy. Thanks to the Inflation Reduction Act, you can claim tax credits for buying electric vehicles or installing solar panels. These credits directly reduce the amount of tax you owe, making them even more valuable than deductions.

For instance, if your suburban office near a major city installs solar panels, you could qualify for a substantial tax credit. This not only lowers your tax bill but also reduces your energy costs, providing long-term savings.

Maximizing equipment deductions and taking advantage of green energy credits are vital components of small business tax saving strategies. By leveraging these opportunities, you can keep more money in your business and invest in its growth.

Next, we’ll explore various small business tax saving strategies to further improve your financial success.

Small Business Tax Saving Strategies

When it comes to small business tax saving strategies, you have a wealth of options to consider. Let’s explore deductions, credits, and smart tax planning to save you money.

Deductions: Reduce Your Taxable Income

Deductions lower your taxable income, which means you pay less in taxes. Common deductions for small businesses include:

-

Business Expenses: You can deduct costs like rent, utilities, and office supplies. If you use your personal vehicle for business, don’t forget to claim mileage expenses.

-

Home Office Deduction: If you work from home, you might qualify for this deduction. Calculate the percentage of your home used for business to determine your deduction.

-

Depreciation: Instead of deducting the full cost of certain assets in one year, spread it out over time. This is useful for items like office furniture and equipment.

Credits: Dollar-for-Dollar Tax Savings

Credits are even better than deductions because they reduce your tax bill directly. Here are some to consider:

-

Work Opportunity Tax Credit: Hire from certain groups and get a tax credit. This includes veterans and individuals on public assistance.

-

Small Business Health Care Tax Credit: If you provide health insurance, you could qualify for a credit covering a portion of the premiums.

-

Clean Energy Credits: Invest in solar panels or electric vehicles and earn credits that cut your taxes.

Tax Planning: A Year-Round Strategy

Tax planning isn’t just for tax season. It’s a year-round effort to optimize your financial situation. Here’s how:

-

Evaluate Your Business Structure: Consider whether changing your business type could save you money. For instance, S corporations can offer tax advantages over C corporations.

-

Defer Income: If you expect to be in the same or lower tax bracket next year, defer income to reduce this year’s tax burden.

-

Carryover Deductions: If you can’t use all your deductions this year, carry them over to the next. This is common with capital losses and charitable contributions.

Elite Tax Strategy Solutions: Your Partner in Tax Savings

At Elite Tax Strategy Solutions, we specialize in helping small businesses steer complex tax regulations. Our experts provide custom strategies to maximize your deductions and credits. With our guidance, you can align tax planning with your broader financial goals.

By leveraging these small business tax saving strategies, you can optimize your tax position and keep more money in your business. Next, we’ll tackle frequently asked questions about small business taxes to clear up any lingering doubts.

Frequently Asked Questions about Small Business Taxes

How to pay less taxes as a small business?

Paying less in taxes starts with smart tax-saving strategies. Here are some tips:

-

Hire a CPA: A Certified Public Accountant can help you find deductions and credits you might miss. They keep you updated on tax law changes and ensure you file correctly.

-

Track Expenses: Keep detailed records of all business expenses. This includes receipts, invoices, and utility bills. Organized records make it easier to claim deductions.

-

Take Advantage of Deductions and Credits: As covered earlier, use all available deductions and credits. This includes business expenses, home office deductions, and more.

How do LLC owners avoid taxes?

LLC owners can benefit from pass-through taxation. Here’s what that means:

-

Pass-Through Taxation: Income from the LLC “passes through” to your personal tax return, avoiding corporate taxes. This means you only pay taxes at your personal income tax rate.

-

Personal Income Tax: Since your LLC income is part of your personal income, you can use personal deductions and credits to reduce your tax bill.

-

Consider an S Corporation Election: LLCs can elect to be taxed as S corporations. This might offer additional tax benefits, like reducing self-employment taxes.

How much should I save for taxes as a small business owner?

The amount you should save depends on your net income and tax bracket. Here’s a simple guide:

-

Estimate Your Tax Bracket: Use last year’s income to estimate your tax bracket. This helps you predict your tax rate.

-

Save a Percentage of Income: A common rule is to save 25-30% of your net income for taxes. This covers federal, state, and self-employment taxes.

-

Adjust for Changes: If your income changes, adjust your savings rate. Keep an eye on tax law changes that might affect your tax bracket.

By understanding these key areas, you can better manage your tax obligations and keep more money in your pocket. Next, we’ll wrap up with some final thoughts on tax optimization and how Elite Tax Strategy Solutions can support your small business.

Conclusion

In small business, tax optimization is not just an annual task—it’s a year-round commitment. By taking a proactive approach, you can significantly improve your financial stability and ensure you’re not paying more than necessary.

At Elite Tax Strategy Solutions, we specialize in crafting personalized tax strategies that align with your unique business goals. Our team of experts is dedicated to helping you steer the complexities of tax regulations and uncover opportunities for savings. Whether it’s maximizing deductions, choosing the right business structure, or planning for retirement, we’re here to support you every step of the way.

Why choose Elite Tax Strategy Solutions?

-

Custom Strategies: We understand that every business is different. Our solutions are customized to meet your specific needs and financial objectives.

-

Expert Guidance: With our seasoned professionals by your side, you’ll have access to the latest tax-saving strategies and insights.

-

Long-Term Focus: We integrate tax planning with your broader financial goals, ensuring that you’re not only saving money today but also setting up for future success.

Don’t leave your tax savings to chance. Partner with us to take control of your financial future and optimize your tax strategy for the best results.

Find how our custom tax planning services can benefit your small business by visiting our Tax Planning for Small Businesses page. Let’s work together to make tax season less stressful and more rewarding.