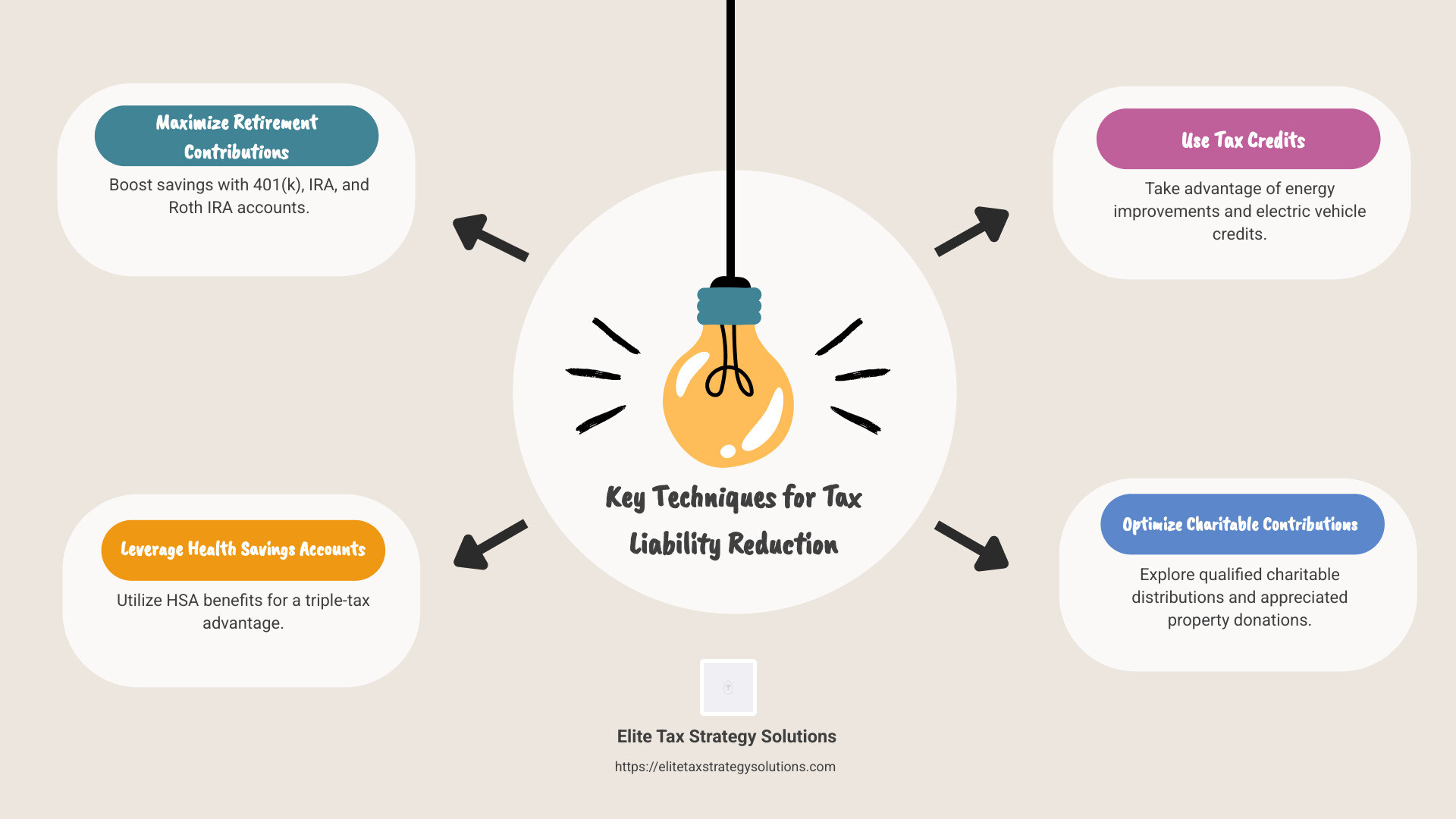

Tax liability reduction is about planning smart strategies to keep more of your hard-earned money. The key is proactive tax planning, which involves taking early steps throughout the year to minimize your tax bill. Here are a few effective techniques:

- Maximize retirement contributions.

- Take advantage of tax credits and deductions.

- Use Health Savings Accounts (HSA).

- Engage in tax-loss harvesting.

- Consider charitable contributions.

These strategies can help individuals and businesses significantly reduce the amounts they owe, leading to greater financial stability and peace of mind.

I’m David Fritch. With over 40 years in law and tax advisories, I’ve mastered the art of tax liability reduction. I help individuals and businesses steer complex tax laws to maximize savings and achieve financial goals. Let’s dive deeper into successful tax strategies.

Common Tax liability reduction vocab:

– small business tax saving strategies

– tax management services

– how can i save money on taxes

Understanding Tax Liability

Let’s break down tax liability in simple terms. It’s the total amount of money you owe to the government in taxes. This can include income taxes, sales taxes, property taxes, and more. Essentially, it’s your tax bill.

How is Tax Liability Calculated?

Calculating your tax liability involves several steps:

-

Determine Your Gross Income: This includes all the money you earn, such as wages, dividends, and rental income.

-

Apply Deductions and Exemptions: Subtract any deductions or exemptions you’re eligible for. This could include the standard deduction or itemized deductions like mortgage interest or charitable donations.

-

Calculate Taxable Income: The result after applying deductions is your taxable income.

-

Use IRS Tax Brackets: The IRS uses a progressive tax system. This means your income is taxed at different rates as it rises through the brackets. For example, in 2024, single filers have a standard deduction of $14,600. After subtracting this from your income, the remaining amount is taxed according to the appropriate bracket.

Why Understanding Tax Brackets Matters

Knowing how tax brackets work helps you plan better. If you’re on the edge of a bracket, certain strategies can help you stay in a lower one. This could involve timing income or deductions strategically.

For instance, if you’re nearing the next bracket, you might consider deferring some income or increasing retirement contributions to lower your taxable income.

Tax liability reduction isn’t just about paying less tax. It’s about understanding how taxes work and planning accordingly to keep more of your money.

This knowledge is crucial for both individuals and businesses aiming to achieve financial stability.

Top Strategies for Tax Liability Reduction

Reducing your tax liability isn’t just about saving money—it’s about smart planning. Here are some top strategies to help you keep more of what you earn.

Boost Retirement Contributions

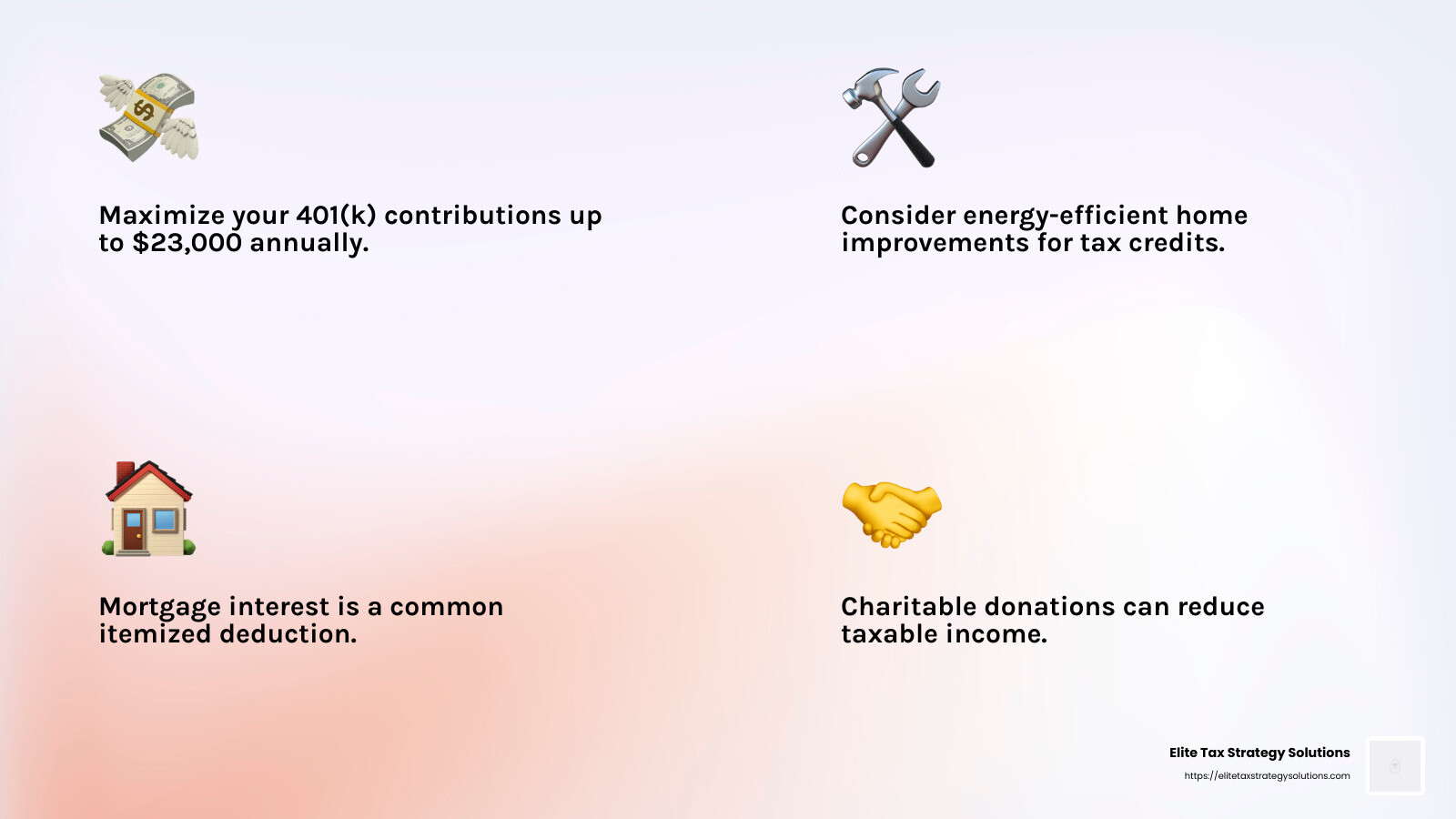

One of the easiest ways to reduce your taxable income is by maximizing retirement contributions. By contributing to employer-sponsored retirement plans like 401(k) or 403(b), you can lower your taxable income directly. In 2024, you can contribute up to $23,000, with an additional $7,500 if you’re 50 or older. These contributions are made with pre-tax dollars, which means they reduce your total taxable income right off the bat.

For those without access to employer-sponsored plans, consider an Individual Retirement Account (IRA). Traditional IRAs allow you to contribute up to $7,000 (or $8,000 if you’re over 50) annually, which can also reduce your taxable income.

Take Advantage of Tax Credits

Tax credits are often more valuable than deductions because they reduce your tax bill dollar-for-dollar. There are various tax credits available, such as those for energy-efficient home improvements or electric vehicle purchases. For instance, installing solar panels can qualify you for a federal tax credit, significantly slashing your tax bill.

Maximize Deductions

Deductions reduce the amount of your income that’s subject to tax. You can choose between a standard deduction or itemizing your deductions, depending on which saves you more. For 2024, the standard deduction for single filers is $14,600. However, if your itemized deductions exceed this amount, itemizing could be more beneficial.

Common itemized deductions include mortgage interest, state and local taxes, and charitable donations. Speaking of donations, giving to charity can not only help others but also decrease your tax bill if you itemize deductions.

Strategic Planning Is Key

Understanding these strategies and how they apply to your situation can make a big difference in your tax bill. By planning ahead and knowing which credits and deductions you qualify for, you can significantly reduce your tax liability.

Next, we’ll explore how leveraging Health Savings Accounts (HSAs) can provide a triple-tax advantage, further enhancing your tax-saving strategies.

Maximize Retirement Contributions

When it comes to tax liability reduction, maximizing your retirement contributions is a powerful strategy. Let’s break down how you can use different retirement accounts to your advantage.

401(k) Plans

A 401(k) is an employer-sponsored retirement plan that allows you to contribute pre-tax dollars, directly reducing your taxable income. For 2024, you can contribute up to $23,000, and if you’re 50 or older, you can add an extra $7,500 as a catch-up contribution. This means more money saved for retirement and less income subject to taxes now.

Example: If you earn $80,000 a year and contribute $23,000 to your 401(k), your taxable income drops to $57,000. This can significantly reduce your tax bill.

Individual Retirement Accounts (IRAs)

An IRA is another excellent way to save for retirement while cutting down on taxes. Traditional IRAs allow contributions with pre-tax dollars, reducing your taxable income for the year. You can contribute up to $7,000 annually (or $8,000 if you’re over 50).

Example: Suppose you contribute $7,000 to a traditional IRA. This amount is deducted from your taxable income, providing immediate tax benefits.

Roth IRAs

While Roth IRAs don’t offer an upfront tax deduction, they have a unique advantage: tax-free withdrawals in retirement. Contributions are made with after-tax dollars, but your money grows tax-free, and you won’t pay taxes on withdrawals if you follow the rules.

Why consider a Roth IRA? If you expect to be in a higher tax bracket in retirement, a Roth IRA can be a smart choice. It provides tax-free income when you might need it the most.

Balancing Contributions

Choosing between a traditional or Roth IRA often depends on your current tax situation and future expectations. Some people even split their contributions between both types to enjoy a mix of immediate tax benefits and future tax-free income.

In summary, maximizing your retirement contributions not only prepares you for a comfortable future but also offers immediate tax advantages. By using 401(k)s and IRAs effectively, you can significantly reduce your taxable income today while building wealth for tomorrow.

Next, we’ll explore how leveraging Health Savings Accounts (HSAs) can provide a triple-tax advantage, further enhancing your tax-saving strategies.

Leverage Health Savings Accounts

Health Savings Accounts, or HSAs, offer a unique triple-tax advantage that can significantly aid in tax liability reduction. Let’s explore how these accounts work and why they are a smart choice for those with high-deductible health plans.

What is an HSA?

An HSA is a special savings account designed to help you save for medical expenses. It’s available to individuals enrolled in high-deductible health plans. The best part? It offers three levels of tax benefits that can help you save money both now and in the future.

The Triple-Tax Advantage

- Pre-Tax Contributions: Money you contribute to an HSA is tax-deductible, meaning it reduces your taxable income for the year. This is similar to the way contributions to a traditional 401(k) or IRA work.

Example: If you contribute $3,000 to your HSA, that amount is deducted from your taxable income, lowering your overall tax bill.

-

Tax-Free Growth: The money in your HSA grows tax-free. Any interest or investment earnings within the account are not subject to taxes, allowing your savings to accumulate more quickly over time.

-

Tax-Free Withdrawals: Withdrawals from your HSA are tax-free when used for qualified medical expenses. This means you’re not taxed on the money when you use it for healthcare costs, providing a significant advantage over other savings options.

Why Use an HSA?

An HSA is not just a short-term tax-saving tool; it’s also a powerful long-term strategy. Funds in an HSA roll over year after year, so you don’t lose your savings at the end of the year. Plus, once you reach age 65, you can use the funds for non-medical expenses without penalty, though they will be taxed as ordinary income.

Maximize Your Contributions

For 2024, you can contribute up to $4,150 for individual coverage and $8,300 for family coverage. If you’re 55 or older, you can add an extra $1,000 as a catch-up contribution.

Pro Tip: Try to maximize your HSA contributions each year to take full advantage of the tax benefits and prepare for future medical expenses.

By leveraging an HSA, you can enjoy immediate tax savings, grow your healthcare nest egg tax-free, and ensure a financially secure future. It’s a strategic move that aligns with both your health and financial goals.

Next, we’ll look at how utilizing tax credits can further reduce your tax burden and improve your overall savings strategy.

Use Tax Credits

Tax credits are a powerful tool for tax liability reduction. They offer a direct reduction in the amount of tax you owe, unlike deductions that only reduce your taxable income. Let’s explore two effective ways to use tax credits: energy improvements and electric vehicle credits.

Energy Improvements

Making energy-efficient upgrades to your home can qualify you for valuable tax credits. These credits are designed to encourage homeowners to adopt eco-friendly practices that benefit both the environment and their wallets.

What qualifies?

- Solar Panels: Installing solar panels can earn you a sizable tax credit. This not only helps reduce your carbon footprint but also slashes your energy bills.

- Energy-Efficient Windows and Doors: Upgrading to energy-efficient windows and doors can also qualify for credits. These improvements help keep your home insulated, reducing heating and cooling costs.

Electric Vehicle Credits

Thinking about going electric? The government offers tax credits to encourage the purchase of electric vehicles (EVs), which are cleaner and more sustainable than traditional gas-powered cars.

How does it work?

- Qualified Electric Vehicles: If you buy a qualified electric vehicle, you can receive a tax credit. The amount varies based on the vehicle’s battery capacity and other factors.

- Inflation Reduction Act: Recent legislation, like the Inflation Reduction Act, has expanded these credits, making it even more appealing to switch to an electric vehicle.

Example: If you purchase an EV with a large battery capacity, you might qualify for a credit of up to several thousand dollars. This can significantly lower the initial cost of the vehicle.

Why Use Tax Credits?

Using tax credits for energy improvements and electric vehicles not only lowers your tax bill but also supports sustainable living. These credits are a win-win, promoting green practices while providing financial benefits.

By taking advantage of these tax credits, you can play a part in protecting the environment and enjoy substantial savings. Next, we’ll dive into optimizing charitable contributions to further improve your tax strategy.

Optimize Charitable Contributions

Charitable contributions can be a smart way to reduce your tax liability while supporting causes you care about. Let’s explore two effective strategies: qualified charitable distributions and appreciated property donations.

Qualified Charitable Distributions (QCDs)

If you’re 70½ or older, you can make a Qualified Charitable Distribution (QCD) from your IRA. This allows you to donate up to $100,000 per year directly to a charity without counting it as taxable income. It’s a great way to meet your Required Minimum Distribution (RMD) while supporting a good cause.

Benefits of QCDs:

- Reduces Taxable Income: Since the distribution goes directly to charity, it doesn’t increase your taxable income.

- Fulfills RMDs: You can satisfy your RMD without the usual tax implications.

Example: Jane, aged 72, donates $5,000 from her IRA to a qualified charity. This amount counts towards her RMD but isn’t included in her taxable income, effectively lowering her tax bill.

Appreciated Property Donations

Donating appreciated property, like stocks or real estate, can be another savvy move. Instead of selling the asset and donating the cash, you can donate the asset directly to a charity. This strategy allows you to avoid capital gains tax and claim a deduction for the full market value.

Why consider this?

- Avoid Capital Gains Tax: By donating the asset directly, you bypass the capital gains tax you’d owe if you sold it first.

- Larger Deduction: You can deduct the fair market value of the donated asset, potentially leading to a larger deduction than if you sold it and donated the proceeds.

Example: John owns shares worth $10,000 that he bought for $5,000. By donating the shares directly, he avoids paying capital gains tax on the $5,000 profit and can deduct the full $10,000 from his taxable income.

Making the Most of Charitable Contributions

Optimizing your charitable contributions through QCDs and appreciated property donations can significantly reduce your tax liability while supporting meaningful causes. It’s a win-win for your finances and the charities you love.

Next, we’ll explore tax-loss harvesting and capital gains strategies to further improve your tax planning efforts.

Tax-Loss Harvesting and Capital Gains

Tax-loss harvesting and capital gains strategies can be powerful tools for tax liability reduction. Let’s break down how these methods work and how they can benefit you.

Tax-Loss Harvesting

What is Tax-Loss Harvesting?

Tax-loss harvesting involves selling investments at a loss to offset gains you’ve made elsewhere. This strategy can help reduce the taxes you owe on capital gains, effectively lowering your overall tax bill.

How it Works:

- Identify Losses: Review your investment portfolio to find assets that are underperforming.

- Sell at a Loss: Sell these assets to realize a loss, which can then be used to offset any capital gains.

- Offset Gains: Use the loss to offset capital gains from other investments, reducing the amount of tax you owe.

Example: Suppose you have a $3,000 gain from selling Stock A. You also have a $2,000 loss from Stock B. By selling Stock B, you can offset $2,000 of your gain, reducing your taxable gain to $1,000.

Benefits of Tax-Loss Harvesting:

- Reduces Taxable Income: Offsets capital gains, lowering your taxable income.

- Carries Forward: If your losses exceed your gains, you can carry the loss forward to future tax years.

Capital Gains Strategy

Understanding Capital Gains

Capital gains are the profits you make from selling an asset for more than its purchase price. The tax rate on these gains depends on how long you’ve held the asset.

Short-Term vs. Long-Term:

- Short-Term Capital Gains: Assets held for less than a year. Taxed at your ordinary income tax rate.

- Long-Term Capital Gains: Assets held for more than a year. Taxed at a lower rate, typically 0%, 15%, or 20%, depending on your income.

Strategic Tips:

- Hold for the Long Term: Whenever possible, aim to hold investments for over a year to benefit from lower long-term capital gains rates.

- Review Tax Brackets: Consider selling assets when your income is lower to take advantage of more favorable tax brackets.

- Harvest Gains: In years with lower tax rates, you might choose to sell assets to lock in gains at a reduced tax rate.

Example: If you sell a stock for a $10,000 gain after holding it for over a year, and your taxable income falls within the 15% capital gains bracket, you’d owe $1,500 in taxes. If you held it for less than a year, you might owe more, depending on your income tax rate.

Optimizing Your Strategy

By combining tax-loss harvesting with a thoughtful approach to capital gains, you can effectively manage your tax liability. This strategic planning can help you keep more of your investment returns.

Next, we’ll dive into frequently asked questions about tax liability reduction to address common concerns and provide clarity.

Frequently Asked Questions about Tax Liability Reduction

What is the tax liability deduction?

Taxable Income and Standard Deduction

Your taxable income is the portion of your income that is subject to taxes after accounting for deductions and exemptions. The standard deduction is a fixed amount that reduces your taxable income, simplifying the tax filing process for many individuals. This deduction varies based on your filing status, such as single, married, or head of household. For example, if your taxable income is $50,000 and the standard deduction for your filing status is $12,000, you only pay taxes on $38,000.

How can I reduce my LLC tax liability?

Retirement Accounts and QBI Deduction

For LLC owners, there are specific strategies to reduce tax liability:

-

Retirement Accounts: Contributing to retirement accounts like a SEP IRA or a SIMPLE IRA can lower your taxable income. These contributions are often tax-deductible, reducing your immediate tax burden.

-

Qualified Business Income (QBI) Deduction: This deduction allows eligible LLCs to deduct up to 20% of their qualified business income. It’s a significant tax-saving opportunity for many small business owners. However, the deduction has specific rules and income thresholds, so consulting with a tax professional is advisable.

How can I reduce my tax owed?

Municipal Bonds and Long-Term Capital Gains

-

Municipal Bonds: Investing in municipal bonds can be a smart way to reduce your tax liability. The interest earned on these bonds is often exempt from federal taxes and, in some cases, state and local taxes as well. This tax-free income can be particularly beneficial for those in higher tax brackets.

-

Long-Term Capital Gains: Holding investments for more than a year can qualify you for lower long-term capital gains tax rates. These rates are generally more favorable than short-term capital gains rates, which align with your ordinary income tax rate. By strategically timing your asset sales, you can minimize taxes owed on investment profits.

These FAQs highlight some of the most effective ways to achieve tax liability reduction. By understanding and utilizing these strategies, you can significantly lower your tax bill and improve your financial health.

Next, we’ll explore how to leverage these strategies with personalized tax planning to ensure financial stability.

Conclusion

At Elite Tax Strategy Solutions, we understand that navigating the complexities of tax liability can be overwhelming. But with the right strategies and guidance, you can achieve significant tax savings and improve your financial well-being.

Our approach is all about personalized tax planning. We tailor strategies to fit your unique financial situation, whether you’re a high-income earner or a small business owner. Our proactive methods ensure that you’re not just reacting to tax season, but planning ahead to maximize your savings.

By integrating tax planning with your broader financial goals, we help you achieve financial stability. Whether it’s through optimizing retirement contributions, leveraging health savings accounts, or employing tax-loss harvesting, we aim to minimize your tax burden while aligning with your long-term objectives.

Our team of seasoned professionals stays on top of the latest tax law changes, ensuring that our clients benefit from the most current and effective strategies available. We believe that tax planning is not just about compliance, but about creating opportunities for growth and security.

If you’re ready to take control of your tax situation and work towards financial stability, we invite you to explore our tax planning services for small businesses. Let us help you slash your taxes and secure your financial future.