Mastering Retirement Savings: Tax Strategies for High Earners

Retirement tax strategies for high income earners can help you significantly reduce your taxable income and grow your wealth for the future. Let’s cut to the chase – here are some effective strategies:

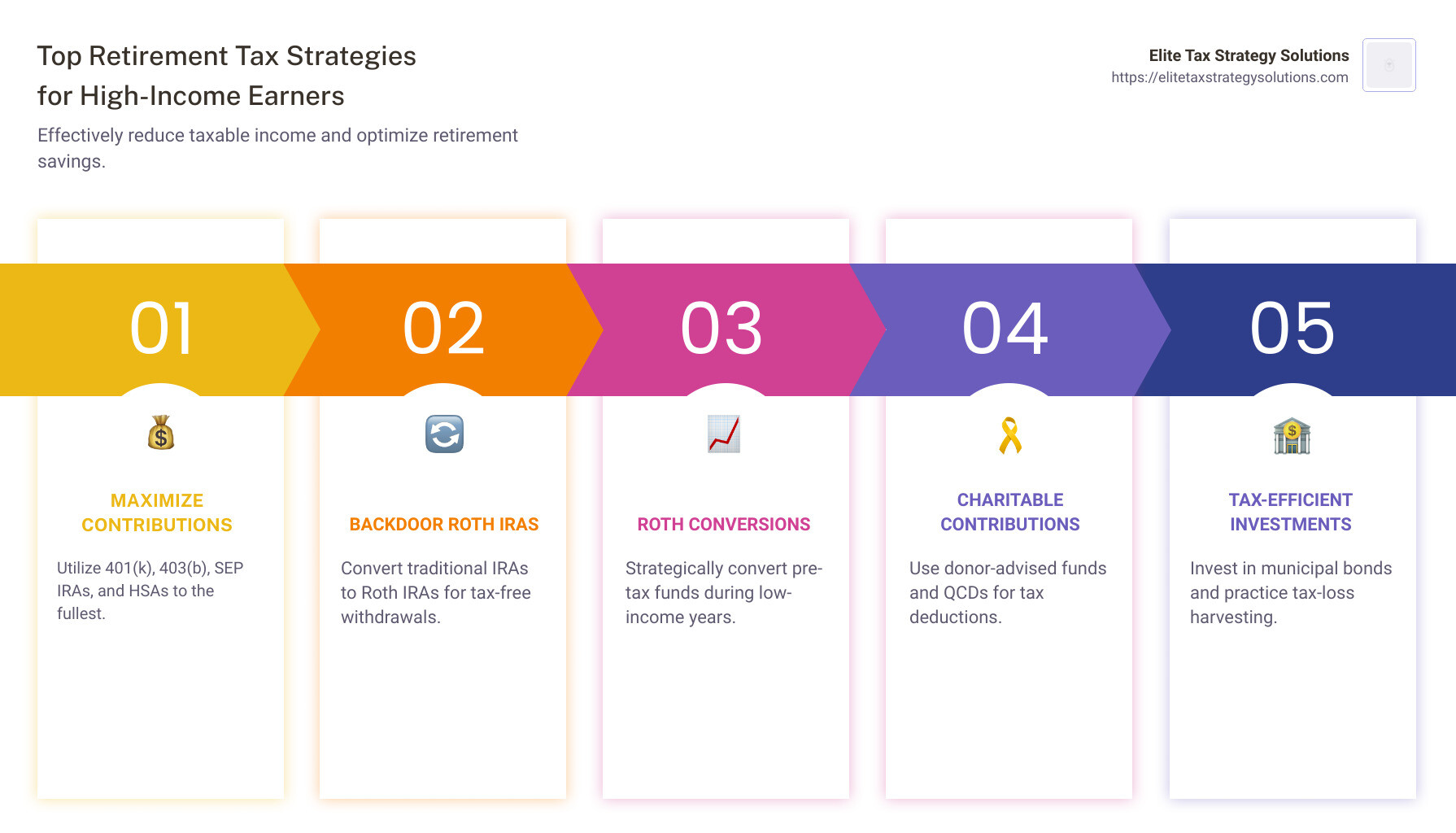

- Maximize Contributions to Tax-Advantaged Accounts: Use 401(k), 403(b), SEP IRAs, and HSAs.

- Explore Backdoor Roth IRAs: Convert traditional IRAs to Roth IRAs for tax-free withdrawals.

- Leverage Roth Conversions: Strategically convert pre-tax retirement funds to Roth IRAs during low-income years.

- Make Charitable Contributions: Benefit from tax deductions using donor-advised funds and qualified charitable distributions.

High-income earners face unique challenges when it comes to tax planning, yet it’s crucial to steer these complexities to ensure financial stability. Sound tax strategies not only minimize the amount owed to Uncle Sam but also optimize your retirement savings.

I’m David Fritch, with 40 years of experience in tax planning and financial advising. I’ve dedicated my career to helping high-income earners like yourself make the most of their retirement savings through well-planned, effective tax strategies.

Quick retirement tax strategies for high income earners definitions:

– extra medicare tax for high earners

– financial planning for high income earners

– high income individual tax planning

Understanding High-Income Earners

To master retirement tax strategies for high income earners, it’s essential to first understand what qualifies someone as a high-income earner and how the IRS views their income.

IRS Definition of High-Income Earners

The IRS defines high-income earners as individuals who fall into the top three tax brackets. This means:

- Single filers: Taxable income over $191,951

- Married filing jointly: Taxable income over $383,901

- Head of household: Taxable income over $191,951

These income levels place individuals in brackets where they face higher tax rates, making tax planning crucial.

Tax Brackets

Tax brackets determine the percentage of tax owed on each portion of taxable income. For 2023, the tax brackets for high-income earners are:

- Bracket 5: $191,951 – $243,725; add 32% of amount over $191,951

- Bracket 6: $243,726 – $609,350; add 34% of amount over $243,726

- Bracket 7: Over $609,350; add 37% of amount over $609,350

Understanding these brackets helps in planning how to minimize taxes through strategic actions like income deferral and contributions to tax-advantaged accounts.

Taxable Income vs. Adjusted Gross Income

Taxable income is the amount of income subject to federal income tax after deductions and exemptions. It’s calculated as:

Taxable Income = Adjusted Gross Income (AGI) – Deductions

Adjusted Gross Income (AGI) is your gross income minus certain adjustments, such as:

- Contributions to traditional IRAs

- Student loan interest

- Alimony payments (for agreements made before 2019)

AGI serves as a baseline for calculating taxable income and for determining eligibility for various tax credits and deductions.

Impact on Tax Strategies

High-income earners need to carefully manage both AGI and taxable income to optimize their tax situation. Some strategies include:

- Converting traditional IRAs to Roth IRAs to take advantage of tax-free withdrawals later.

- Deferring income to control when it’s taxed, such as delaying a bonus to a lower-income year.

- Investing in tax-exempt bonds to reduce taxable interest income.

By understanding these fundamental concepts, high-income earners can better steer tax brackets and make informed decisions to reduce their tax burden and maximize retirement savings.

Next, we’ll explore how to fully fund tax-advantaged accounts to lower your taxable income and grow your retirement savings.

Tax-Advantaged Accounts

Fully Fund Tax-Advantaged Accounts

Maxing out contributions to tax-advantaged accounts is a powerful strategy to reduce taxable income and grow your retirement savings. For high-income earners, accounts like 401(k)s, 403(b)s, SEP IRAs, and Solo 401(k)s are essential tools.

401(k) and 403(b) Plans: Contributions to these employer-based plans are made pre-tax, which lowers your taxable income for the year. For 2024, the maximum contribution is $23,000. If you’re over 50, you can add an extra $7,500 in catch-up contributions. This means you can defer taxes on up to $30,500 annually.

SEP IRA and Solo 401(k): Ideal for self-employed individuals and small business owners. These accounts allow for significant contributions, with the SEP IRA permitting up to 25% of your net earnings or $66,000 (whichever is less) in 2024. Solo 401(k)s follow similar limits and also allow for catch-up contributions if you’re over 50.

Example: Consider a dual-physician household earning $700,000 annually. By each maxing out their 401(k) contributions, they can reduce their taxable income by $46,000. At a 35% tax rate, this saves them $16,100 in federal taxes alone.

Health Savings Accounts (HSAs)

Health Savings Accounts (HSAs) offer a triple tax advantage: contributions are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free.

Contribution Limits: For 2024, you can contribute up to $4,150 for individual coverage and $8,300 for family coverage. If you’re 55 or older, you can add an extra $1,000 in catch-up contributions.

Tax-Free Growth: Unlike Flexible Spending Accounts (FSAs), the money in your HSA rolls over year to year and can be invested, allowing it to grow tax-free. This makes HSAs not just a tool for current medical expenses but also a long-term investment vehicle.

Example: If you contribute the maximum $8,300 to your family HSA annually and invest it, the account can grow significantly over time. Assuming a 7% annual return, your HSA could grow to over $200,000 in 20 years, all tax-free if used for medical expenses.

Medical Expenses: HSAs can cover a wide range of medical and dental expenses, including over-the-counter medications and first aid supplies. Withdrawals for non-qualified expenses are subject to taxes and a 20% penalty, but after age 65, withdrawals for any purpose are only subject to regular income tax, making it a versatile retirement savings tool.

Next, we’ll explore Roth IRA Strategies to further maximize your retirement savings and manage your tax burden effectively.

Roth IRA Strategies

Backdoor Roth IRA

A Backdoor Roth IRA is a clever strategy for high-income earners who exceed the income limits for direct Roth IRA contributions. This involves making non-deductible contributions to a traditional IRA and then converting that amount to a Roth IRA.

Income Limits: For 2024, the IRS sets income limits that prevent high earners from contributing directly to a Roth IRA. However, the backdoor method circumvents these limits.

Conversion Process:

1. Contribute: Make a non-deductible contribution to a traditional IRA. The contribution limit for 2024 is $7,000 (or $8,000 if you’re over 50).

2. Convert: Convert the traditional IRA to a Roth IRA. Since the initial contribution was non-deductible, you generally won’t owe taxes on the conversion.

Example: A couple earning $400,000 annually can each contribute $7,000 to a traditional IRA and then convert it to a Roth IRA. Over time, with a 7% annual return, these contributions can grow significantly, providing a robust tax-free income stream in retirement.

Roth Conversions

Roth Conversions involve moving funds from a traditional IRA or 401(k) to a Roth IRA. Unlike the backdoor method, these conversions can be done with pre-tax funds, which means you’ll owe taxes on the converted amount.

Timing Conversions: The best time to perform Roth conversions is when your income is lower, such as during early retirement years before Required Minimum Distributions (RMDs) begin at age 73. This allows you to fill up lower tax brackets and minimize the tax impact.

Tax Bracket Management: By converting smaller amounts over several years, you can manage your tax brackets effectively. This can significantly reduce your overall tax liability.

Example: Suppose you retire at 60 with a sizeable traditional IRA. By converting $50,000 annually to a Roth IRA over several years, you can spread out the tax burden. If you’re in a 22% tax bracket, this strategy could save you hundreds of thousands in taxes over time.

Required Minimum Distributions (RMDs): Traditional IRAs require you to start taking distributions at age 73, which are taxable. Roth IRAs, however, do not have RMDs, allowing your investments to grow tax-free for as long as you live.

By utilizing Roth IRA strategies like backdoor contributions and strategic Roth conversions, high-income earners can maximize their tax-free retirement savings.

Next, we’ll explore Charitable Contributions to further optimize your tax strategy and support your philanthropic goals.

Charitable Contributions

Donor-Advised Funds

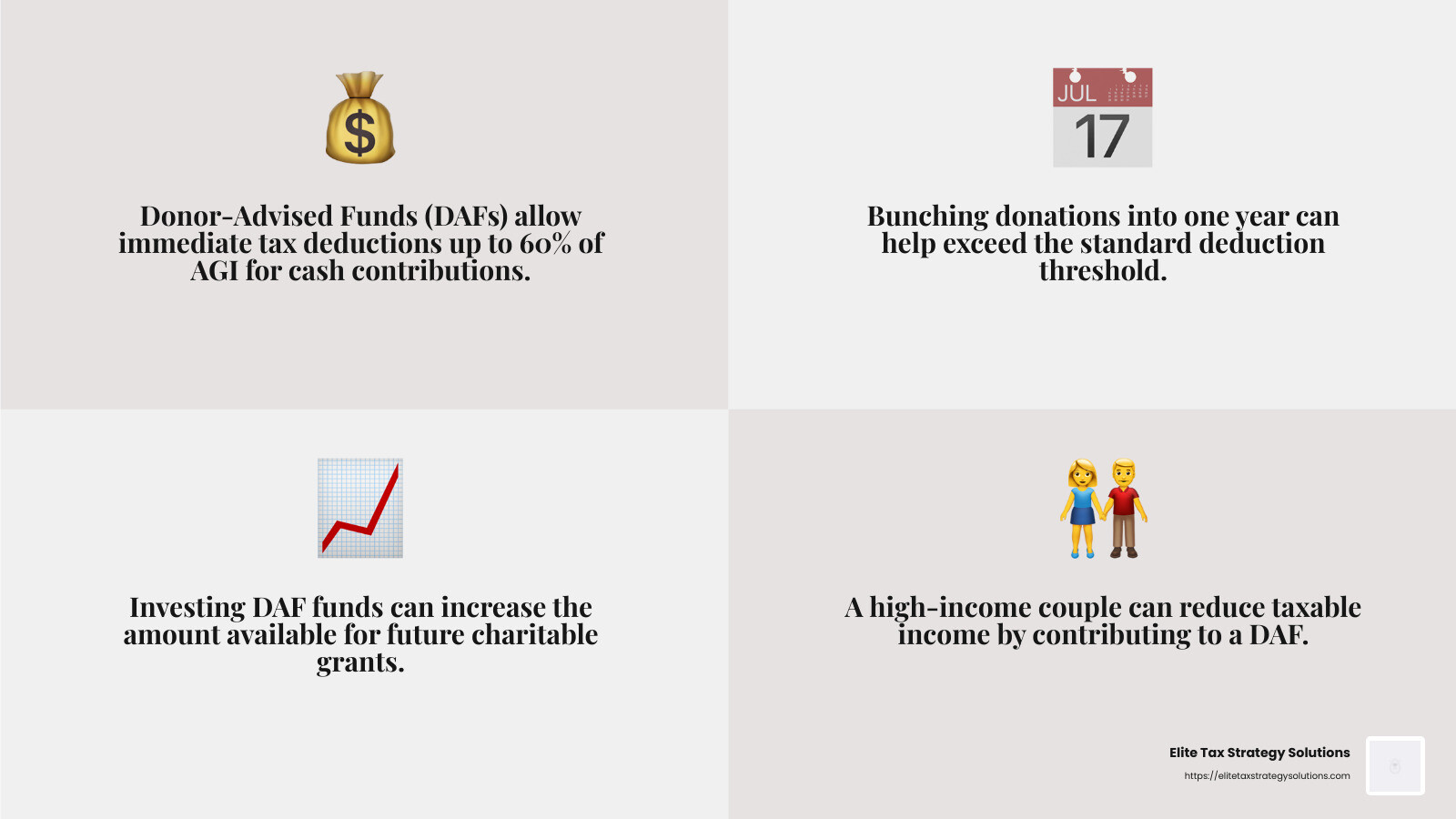

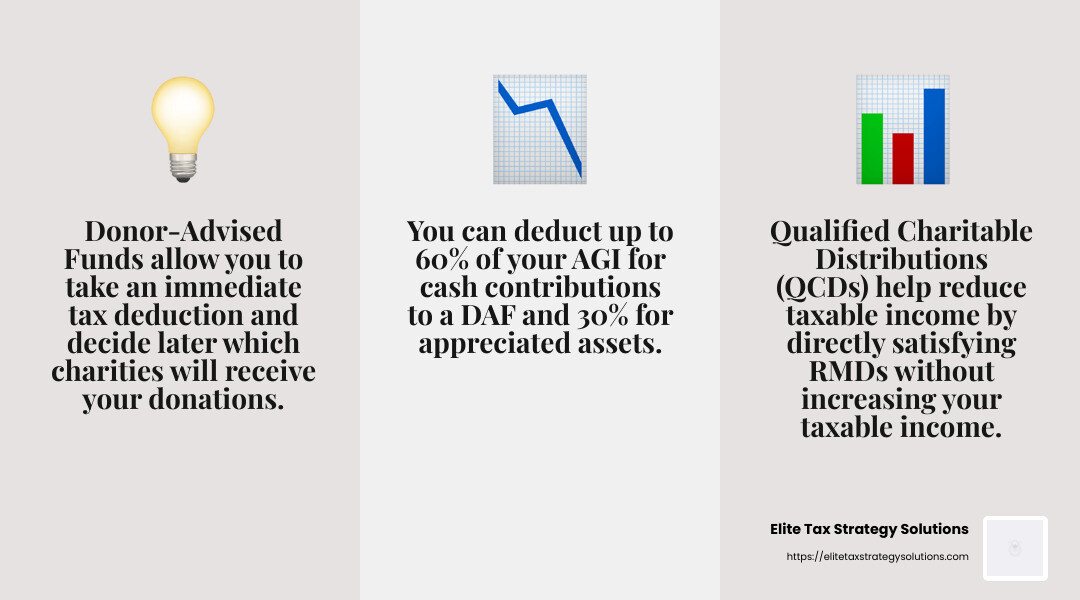

A Donor-Advised Fund (DAF) is a powerful tool for high-income earners looking to maximize their charitable impact while gaining significant tax benefits. By contributing to a DAF, you can take an immediate tax deduction and decide later which charities will receive your donations.

Tax Deductions: When you contribute to a DAF, you can deduct up to 60% of your adjusted gross income (AGI) for cash contributions and 30% for appreciated assets. This can be particularly beneficial in years with higher-than-normal income due to bonuses or windfalls.

Multi-Year Contributions: One strategy is to “bunch” multiple years’ worth of charitable donations into a single year. This helps you exceed the standard deduction threshold, allowing for itemized deductions and greater tax savings.

Charitable Planning: With a DAF, you have the flexibility to support your favorite causes over time. You can invest the funds for potential growth, increasing the amount available for future grants to charities.

Example: Imagine a high-income couple with a combined income of $500,000. They can contribute $50,000 to a DAF, take an immediate tax deduction, and then distribute the funds to various charities over the next several years. This not only supports their philanthropic goals but also reduces their taxable income for the year.

Qualified Charitable Distributions (QCDs)

For those aged 70.5 and older, Qualified Charitable Distributions (QCDs) offer another tax-efficient way to support charities. A QCD allows you to donate up to $100,000 directly from your IRA to a qualified charity, satisfying your Required Minimum Distributions (RMDs) without increasing your taxable income.

IRA Distributions: Normally, RMDs from a traditional IRA are taxable. However, a QCD counts toward your RMD but is excluded from your taxable income, providing a double benefit.

Tax Benefits: By reducing your taxable income, QCDs can help you stay in a lower tax bracket and potentially avoid higher Medicare premiums or the net investment income tax.

Age Requirements: You must be at least 70.5 years old to make a QCD. This strategy is particularly useful for retirees who are required to take RMDs but do not need the extra income.

Example: Suppose you’re 72 and have an RMD of $20,000. By directing this amount to a qualified charity through a QCD, you fulfill your RMD requirement and reduce your taxable income by $20,000, potentially saving thousands in taxes.

By incorporating Donor-Advised Funds and Qualified Charitable Distributions into your retirement tax strategy, you can achieve substantial tax savings while making a meaningful impact on the causes you care about.

Next, we’ll explore Investment Strategies to further optimize your tax strategy and grow your wealth.

Investment Strategies

Municipal Bonds

Municipal bonds are a fantastic option for high-income earners seeking tax-exempt income. These bonds, issued by state and local governments, offer interest payments that are generally not subject to federal income tax. If you live in the state where the bond is issued, you might also avoid state and local taxes.

Federal and State Tax Benefits: Because the interest is tax-free, municipal bonds often provide a higher after-tax return compared to taxable bonds, especially for those in higher tax brackets.

Investment Strategy: Municipal bonds can be a stable addition to your portfolio, providing steady income while reducing your tax liability. They are particularly beneficial if you are in a high tax bracket and looking for tax-efficient investments.

Example: Suppose you are in the 35% tax bracket and invest in a municipal bond with a 3% interest rate. Because the interest is tax-free, your equivalent taxable yield would be around 4.62%. This makes municipal bonds an attractive option compared to taxable bonds offering similar interest rates.

Tax-Loss Harvesting

Tax-loss harvesting is a strategy to offset capital gains by selling investments at a loss. This can reduce your taxable income and help you manage your investment portfolio more effectively.

Offset Capital Gains: If you have realized capital gains, you can sell underperforming investments to offset these gains. The IRS allows taxpayers to deduct up to $3,000 in losses against regular income each year, with any unused losses carried forward to future years.

Carry Forward Losses: Losses not used in the current year can be carried forward indefinitely, providing a cushion against future gains.

Investment Portfolio Management: By actively managing your portfolio and strategically harvesting losses, you can improve your after-tax returns. This approach is particularly useful during market downturns when many investments may be at a loss.

Example: Imagine you have $10,000 in capital gains from selling stocks but also have a stock that has lost $4,000. By selling the losing stock, you can offset the gains, reducing your taxable capital gain to $6,000. If you don’t have enough gains to offset, you can use $3,000 to reduce your ordinary income and carry the remaining $1,000 loss to the next year.

Tax-Efficient Funds

Investing in tax-efficient funds like index mutual funds and exchange-traded funds (ETFs) can help reduce the taxes you pay on your investments year-to-year.

Tax-Efficient Funds: These funds typically have lower turnover rates, meaning they buy and sell securities less frequently. This results in fewer taxable events and lower capital gains distributions.

Example: Suppose you invest in an actively managed mutual fund with a turnover rate of 100%. This fund could generate significant short-term capital gains, taxed at your ordinary income rate. In contrast, an index fund with a turnover rate of 5% would likely generate fewer taxable events, resulting in lower taxes.

Opportunity Zones

Qualified Opportunity Funds (QOFs) offer another way to defer and potentially reduce taxes on capital gains. Created by the Tax Cuts and Jobs Act, these funds encourage investment in economically distressed areas.

Tax Deferral: By investing in a QOF within 180 days of the sale, you can defer taxes on your capital gains until 2026. If you hold the investment for at least five years, you can reduce the deferred gain by 10%.

Investment Strategy: Opportunity Zones provide a way to support community development while benefiting from tax incentives. They can be a strategic addition to a diversified portfolio.

Example: If you sell an asset for a $100,000 gain and invest that gain in a QOF, you can defer paying taxes on it until 2026. If you hold the investment for more than five years, you can exclude 10% of the original gain, reducing your taxable gain to $90,000.

By incorporating municipal bonds, tax-loss harvesting, tax-efficient funds, and Opportunity Zones into your investment strategy, you can optimize your tax position and grow your wealth more effectively.

Next, we’ll dig into Real Estate and Property Tax Strategies to further improve your retirement tax planning.

Real Estate and Property Tax Strategies

Selling Inherited Real Estate

When you inherit real estate, you get a significant tax benefit called the stepped-up basis. This means the property’s value is “stepped up” to its fair market value at the time of the original owner’s death. This adjustment can drastically reduce the capital gains tax when you sell the property.

Example: Suppose you inherit a house that was originally purchased for $100,000 but is worth $500,000 at the time of inheritance. Your new basis is $500,000. If you sell the house for $510,000, you only pay capital gains tax on the $10,000 increase, not the $410,000.

1031 Exchanges

A 1031 exchange allows you to defer capital gains tax by reinvesting the proceeds from a sold property into another like-kind property. This strategy is highly beneficial for real estate investors looking to upgrade or diversify their holdings without immediate tax consequences.

Example: If you sell a rental property for $300,000 and use a 1031 exchange to buy a new rental property for $350,000, you can defer paying capital gains tax on the $300,000.

Paying Property Taxes Early

Paying your property taxes early can be a smart move, especially if you haven’t hit the $10,000 limit for state and local tax (SALT) deductions. Some states and counties even offer discounts for early payments, providing additional savings.

Tax Deductions: The IRS allows you to deduct up to $10,000 in state and local taxes, including property taxes. This deduction can reduce your federal taxable income.

Example: If your property taxes are $8,000 a year, paying them early ensures you can take full advantage of the SALT deduction, reducing your overall tax bill.

Real Estate Investment

Investing in real estate can offer multiple tax benefits, including mortgage interest deductions and depreciation deductions.

Mortgage Interest Deduction: You can deduct the interest paid on mortgages for your primary and secondary residences, up to certain limits.

Depreciation Deduction: The IRS allows you to depreciate the cost of income-producing property over its useful life, even if the property appreciates in value.

Example: If you own a rental property worth $500,000, you can deduct a portion of its cost each year as depreciation. This can significantly reduce your taxable rental income.

State and Local Tax Benefits

State Tax Credits: Some states offer tax credits or deductions for specific activities, such as investing in renewable energy or contributing to a 529 plan.

Example: If you contribute to a 529 plan for your child’s education, some states allow you to deduct these contributions from your state taxable income, providing a double benefit of saving for education and reducing your tax bill.

By leveraging these real estate and property tax strategies, you can optimize your tax position and improve your long-term financial stability.

Frequently Asked Questions about Retirement Tax Strategies for High Income Earners

How can high-income earners save for retirement?

High-income earners have several options to save for retirement effectively:

-

Tax-Advantaged Accounts: Max out contributions to accounts like 401(k)s, 403(b)s, and HSAs. These accounts allow you to defer taxes on contributions and growth until retirement.

-

Roth IRA and Roth 401(k): While direct contributions to a Roth IRA might be limited due to income caps, you can use a Backdoor Roth IRA strategy. This involves making non-deductible contributions to a traditional IRA and then converting it to a Roth IRA.

-

Real Estate: Investing in real estate can provide rental income and significant tax benefits, such as mortgage interest and depreciation deductions.

-

Charitable Donations: Use strategies like Donor-Advised Funds (DAFs) to make charitable contributions. These funds allow you to donate appreciated assets, get an immediate tax deduction, and distribute the funds to charities over time.

How to reduce taxes as a high-income earner?

Reducing taxes requires a multifaceted approach:

-

Maximize Tax-Advantaged Accounts: Fully fund your 401(k), HSA, and other retirement accounts to lower your taxable income.

-

Roth Conversions: Convert traditional IRA assets to a Roth IRA during years when your income is lower. This can help you manage your tax bracket and reduce future tax liabilities.

-

Charitable Contributions: Donate appreciated stocks or other assets to charities. This not only helps you avoid capital gains tax but also provides a tax deduction for the full market value of the donation.

-

Investment Losses: Use tax-loss harvesting to offset capital gains. Selling investments at a loss can help reduce your taxable income.

What are the best tax strategies for high-income earners?

Here are some top strategies:

-

Roth Conversions: Converting traditional IRA funds to a Roth IRA can provide tax-free withdrawals in retirement and reduce required minimum distributions (RMDs).

-

Donor-Advised Funds (DAFs): These funds allow you to make a charitable donation, take an immediate tax deduction, and then recommend grants to charities over time.

-

Municipal Bonds: Invest in municipal bonds to earn tax-exempt interest income. These bonds can provide federal and state tax benefits.

-

1031 Exchanges: For real estate investors, a 1031 exchange allows you to defer capital gains taxes by reinvesting proceeds into a new property.

By understanding and utilizing these retirement tax strategies for high income earners, you can optimize your savings and reduce your tax burden effectively.

Conclusion

Tax planning is essential for high-income earners who want to maximize their retirement savings and minimize their tax burden. It’s not just about filing your taxes annually; it’s about taking a proactive approach to tax optimization.

Why Work with a Financial Advisor?

A financial advisor can provide you with personalized strategies that align with your long-term financial goals. They help you steer the complexities of tax laws and identify opportunities that you might miss on your own.

Elite Tax Strategy Solutions: Your Partner in Tax Optimization

At Elite Tax Strategy Solutions, we specialize in helping high-income earners and closely held businesses maximize their tax savings. Our thorough, proactive approach ensures that you stay ahead of ever-changing tax regulations.

We offer over 100 custom tax-saving strategies to help you achieve financial stability and optimize your tax position. Whether it’s maximizing contributions to tax-advantaged accounts, utilizing Roth IRA strategies, or planning charitable contributions, we have the expertise to guide you.

Take Action Now

Don’t let taxes take a big bite out of your hard-earned money. By integrating tax planning with your overall financial strategy, you can achieve your financial aspirations while minimizing your tax liabilities.

Ready to take the next step? Explore our innovative tax planning services and see how we can help you optimize your retirement savings.

By understanding and utilizing these retirement tax strategies for high income earners, you can optimize your savings and reduce your tax burden effectively.