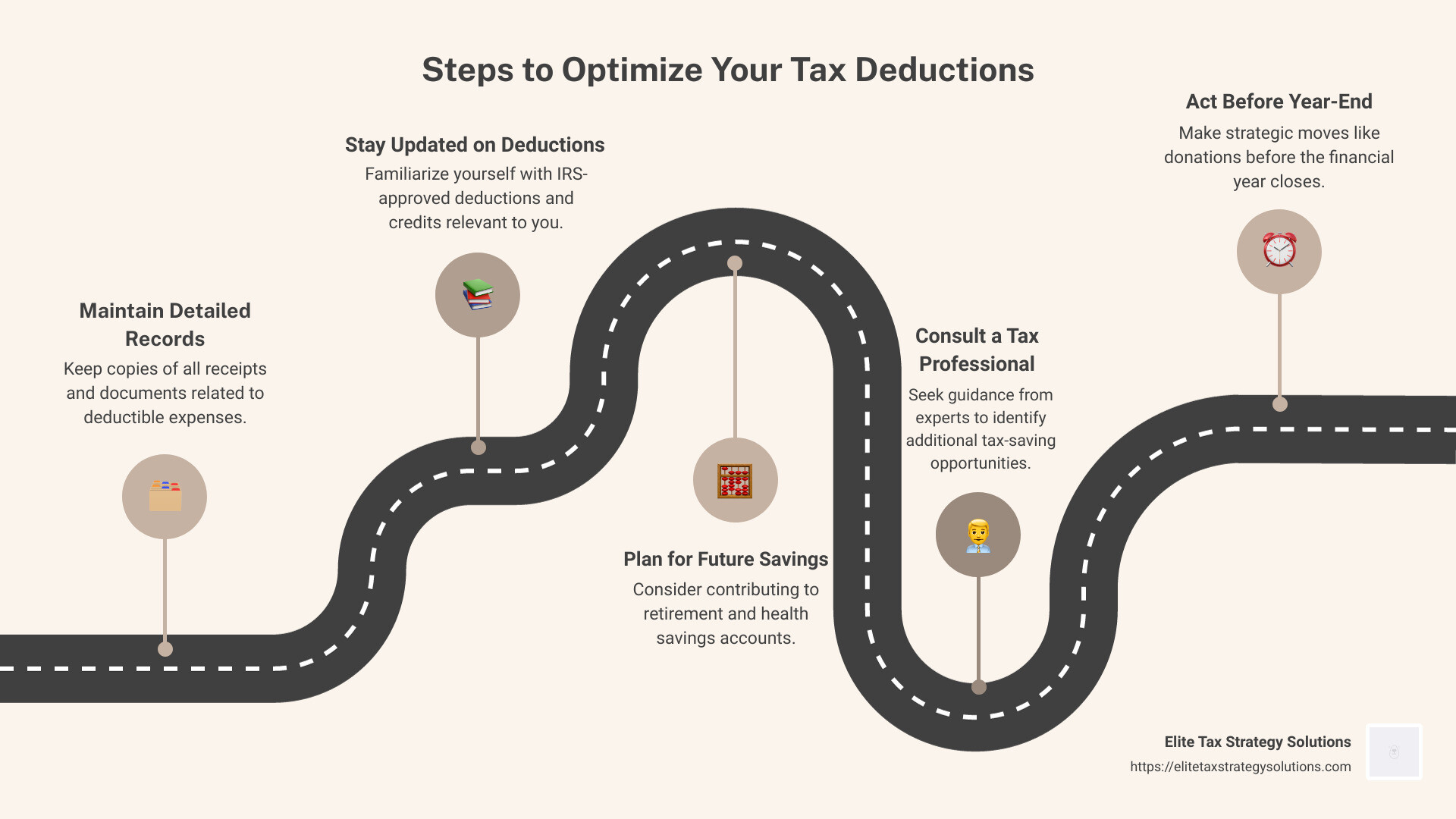

How to optimize tax deductions is a pressing question for those navigating the intricate world of taxes. Here’s a quick breakdown to simplify your strategy:

- Keep meticulous records: Collect all receipts and documentation for deductible expenses.

- Stay informed: Understand IRS-approved deductions and credits applicable to you.

- Plan for the future: Consider retirement and health savings accounts.

- Seek professional guidance: Consult with a tax expert to uncover potential tax savings.

- Act timely: Make strategic moves before the financial year ends to improve deductions.

Tax planning can feel like a bewildering maze, but you’re not alone on this journey. The tax code holds many opportunities to alleviate financial strain through tax deductions and credits. Leveraging these tools can drastically reduce taxable income and even increase your refund.

I’m David Fritch, with over four decades of experience in navigating tax complexities. My expertise lies in helping people like you optimize tax deductions for better financial health. Let’s explore how you can take control of your tax outcomes.

Understanding Tax Deductions

When it comes to taxes, understanding tax deductions can make a big difference in your financial life. There are two main types of deductions: itemized deductions and the standard deduction. Let’s break these down.

Itemized Deductions

Itemizing your deductions means listing out specific expenses that the IRS allows you to deduct from your taxable income. This option is beneficial when your deductible expenses are higher than the standard deduction amount.

Common Itemized Deductions:

- Medical and Dental Expenses: You can deduct these if they exceed a certain percentage of your adjusted gross income.

- State and Local Taxes: This includes property taxes and either sales or income taxes.

- Home Mortgage Interest: If you own a home, you can deduct the interest on your mortgage.

- Charitable Contributions: Donations to qualified organizations can be deducted.

- Casualty and Theft Losses: If you’ve experienced a significant loss, you might be able to deduct it.

However, not all expenses qualify, and some deductions, like unreimbursed job expenses, were eliminated by the Tax Cuts and Jobs Act of 2017.

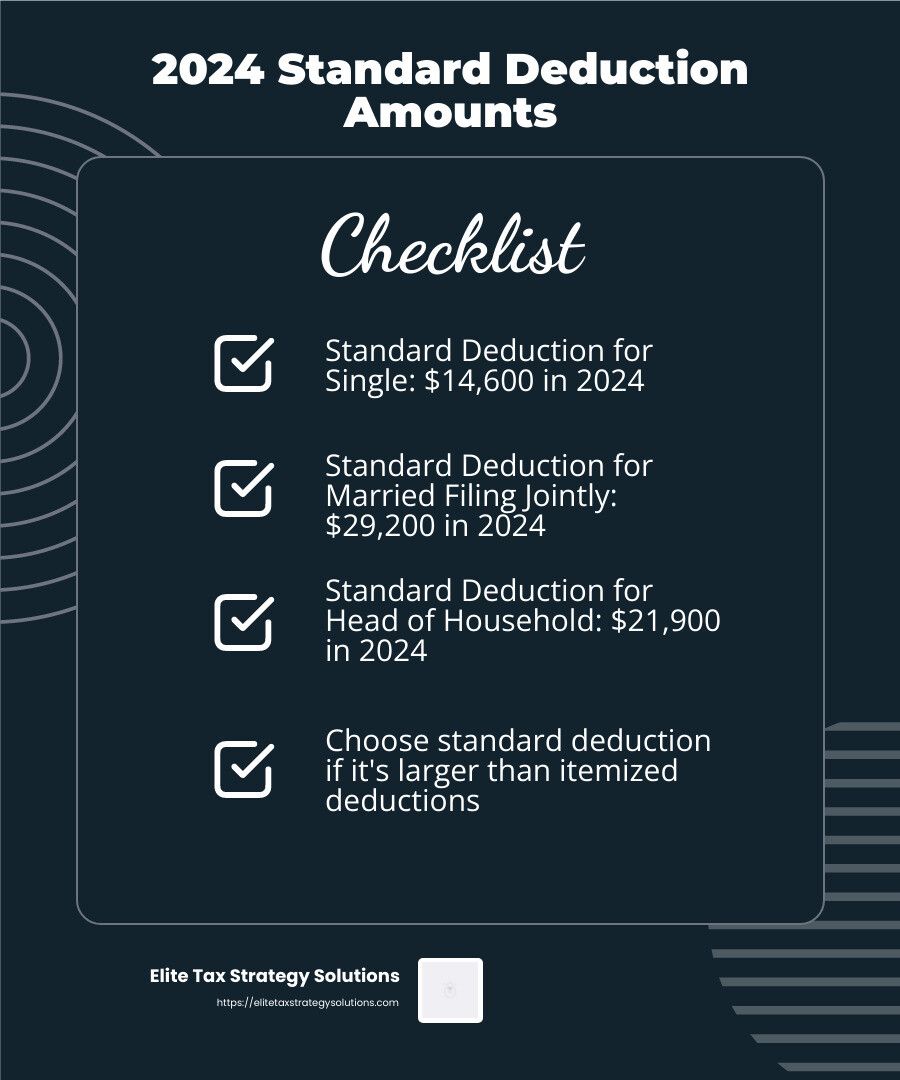

Standard Deduction

The standard deduction is a fixed dollar amount that reduces the income you’re taxed on. It’s available to everyone and is often simpler and quicker than itemizing. The amount varies based on your filing status:

- Single: $14,600 in 2024

- Married Filing Jointly: $29,200 in 2024

- Head of Household: $21,900 in 2024

IRS-Approved Categories

When itemizing, it’s crucial to categorize your expenses correctly. The IRS has specific categories for deductions, and you need to ensure your expenses fit these categories to qualify.

Key Categories Include:

- Medical and Dental Expenses

- Taxes Paid

- Interest Paid

- Charitable Gifts

- Casualty and Theft Losses

Understanding these categories and keeping accurate records can help you decide whether to itemize or take the standard deduction.

Choosing between itemized deductions and the standard deduction depends on your personal financial situation. Each year, evaluate your expenses and choose the option that maximizes your deductions. This decision can significantly impact your taxable income and overall tax liability.

In the next section, we’ll explore how to optimize tax deductions by focusing on various strategies, including retirement contributions and charitable donations.

How to Optimize Tax Deductions

Optimizing tax deductions is all about making smart financial moves throughout the year. Here are some key areas to focus on:

Retirement Contributions

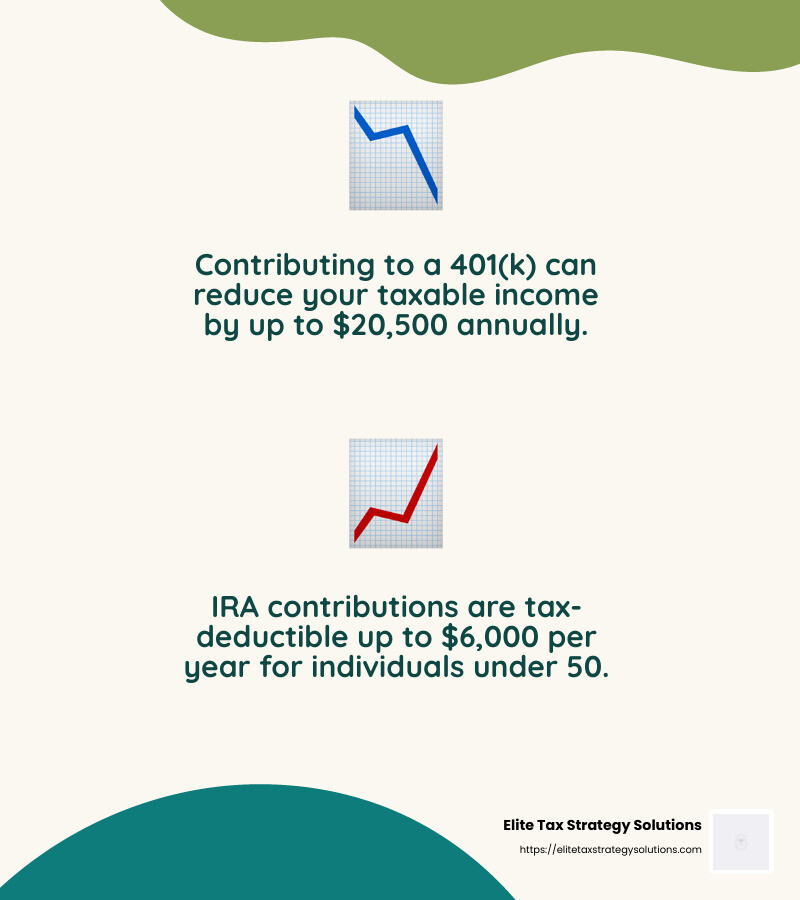

Contributing to retirement accounts like 401(k)s and IRAs can significantly reduce your taxable income. The IRS allows you to contribute up to $23,000 to a 401(k) in 2024, with an additional $7,500 if you’re 50 or older. For IRAs, the contribution limit is $7,000, increasing to $8,000 for those over 50.

These contributions not only lower your taxable income but also prepare you for a secure financial future. If your employer offers a match on your 401(k) contributions, make sure to take full advantage of it—it’s essentially free money.

Health Savings Accounts (HSAs)

HSAs are a triple tax-advantaged way to save for medical expenses. Contributions are tax-deductible, the account grows tax-free, and withdrawals for qualified medical expenses are also tax-free.

For 2024, you can contribute up to $4,150 for an individual and $8,300 for a family. If you’re 55 or older, you can add an extra $1,000 as a catch-up contribution. This not only helps with current medical costs but also serves as a nest egg for future health expenses.

Charitable Donations

Donating to qualified charities can also help reduce your taxable income. Whether you’re giving cash, goods, or even volunteering your time (mileage counts too), these contributions can be deducted.

It’s essential to keep detailed records of your donations, including receipts and any acknowledgment letters from the charities. This documentation is crucial for substantiating your deductions if the IRS comes knocking.

By focusing on these areas, you can effectively optimize your tax deductions and keep more of your hard-earned money. In the following section, we’ll dive into top strategies for maximizing deductions, exploring options like municipal bonds and tax-loss harvesting.

Top Strategies for Maximizing Deductions

When it comes to maximizing your tax deductions, leveraging the right strategies can make a significant difference. Let’s explore some key tactics that can help you keep more money in your pocket.

Municipal Bonds

Investing in municipal bonds is a smart way to earn interest income that is generally exempt from federal taxes. If you reside in the state or locality where the bond is issued, you might also avoid state and local taxes. This makes municipal bonds particularly attractive for those in higher tax brackets.

However, it’s crucial to be aware of exceptions. Some municipal bonds, when purchased at a discount, may incur a “de minimis” tax. Always verify the tax status of a bond before investing to ensure you’re making the most of this tax advantage.

Long-Term Capital Gains

Holding onto investments for more than a year can lead to favorable tax treatment. Long-term capital gains are taxed at lower rates compared to short-term gains, which are taxed as ordinary income. For 2024, the long-term capital gains tax rate can be as low as 0% for those within certain income thresholds, making it a powerful tool for tax savings.

Consider tax-loss harvesting to further optimize your tax position. This involves selling underperforming investments to offset gains, allowing you to reduce your taxable income. Losses can offset up to $3,000 of other income, with any excess carried forward to future tax years.

Business Expenses

If you’re a business owner, maximizing deductions through business expenses is essential. Typical deductible expenses include office supplies, travel, and even some home office costs. Properly categorizing and documenting these expenses can lead to substantial tax savings.

To maximize deductions, keep detailed records and consider consulting a tax professional to ensure you’re not missing out on any potential deductions. Even small business expenses can add up to significant tax savings over time.

By incorporating these strategies, you can effectively maximize your tax deductions and improve your financial well-being. In the next section, we’ll address frequently asked questions about tax deductions, providing clarity on common concerns and offering practical advice.

Frequently Asked Questions about Tax Deductions

Tax deductions can be a bit confusing, but understanding them is crucial for saving money. Here, we’ll answer some common questions and provide clear strategies to help you optimize your tax deductions.

How do I maximize my tax deductions?

Maximizing your tax deductions starts with strategic planning. Here are a few key tactics:

-

Retirement Accounts: Contributing to retirement accounts like a 401(k) or an IRA can significantly reduce your taxable income. For example, maximizing contributions to a 401(k) can lower your tax bill by reducing your taxable income.

-

Health Savings Accounts (HSAs): These accounts allow you to save pre-tax dollars for medical expenses, further reducing your taxable income. For 2024, you can contribute up to $4,150 for an individual or $8,300 for a family.

-

Charitable Donations: Donating to qualified charities not only supports good causes but also provides tax benefits. You can deduct donations up to a certain percentage of your adjusted gross income.

-

Tax-Loss Harvesting: Selling investments at a loss to offset gains can help reduce your taxable income. This strategy is particularly useful if you have significant capital gains.

How can I get less taxes deducted?

Reducing the amount of tax withheld from your paycheck can increase your take-home pay. Consider these options:

-

Filing Status: Choosing the right filing status can impact your tax bracket and deductions. For instance, filing jointly may offer more benefits for married couples.

-

Tax Credits: Unlike deductions, credits directly reduce the tax you owe. Make sure to claim any available credits, such as the Saver’s Credit, which benefits moderate and lower-income individuals saving for retirement.

-

Year-End Tax Moves: Making contributions to retirement accounts or paying deductible expenses before the end of the year can decrease your taxable income for that tax year.

What can I write off on my taxes?

Understanding what you can write off is key to optimizing your deductions. Here are some common deductions:

-

Business Use: If you’re self-employed, you can deduct expenses related to the business use of your home or vehicle.

-

Health Savings: Contributions to HSAs or FSAs can be deducted from your taxable income.

-

Charitable Contributions: As mentioned earlier, donations to eligible charities are deductible.

Keeping accurate records and receipts is essential for claiming these deductions. If you’re unsure about what qualifies, consulting with a tax professional can provide clarity and ensure you’re maximizing your deductions.

In the next section, we will explore more in-depth strategies and address common concerns about tax deductions. Stay tuned to learn how to make the most out of your tax situation.

Conclusion

In finance, tax planning is not just about compliance; it’s about crafting a strategy that aligns with your financial goals. At Elite Tax Strategy Solutions, we focus on turning complex tax challenges into opportunities for growth and financial stability.

Our approach is straightforward yet thorough. By understanding your unique financial situation, we help you optimize your tax deductions and ensure you keep more of your hard-earned money. Whether it’s through maximizing contributions to retirement accounts or utilizing Health Savings Accounts, we tailor strategies that fit your needs.

Financial stability is not just a destination but a journey. With proactive planning and expert guidance, we pave the way for a secure financial future. Our team is dedicated to staying ahead of tax law changes, ensuring that your tax plan evolves with your life and goals.

If you’re ready to take control of your financial future and maximize your tax savings, explore our personalized tax planning services. Let’s work together to achieve your financial aspirations and make tax season a time of opportunity, not stress.