Why High Net Worth Tax Planning Can’t Wait

High net worth tax planning becomes critical when your wealth reaches $1 million or more in investable assets – but most successful individuals wait too long to start. The tax code isn’t built for the wealthy. It’s designed to extract maximum revenue from your success through income taxes, capital gains taxes, and estate taxes that can consume 40% or more of your wealth without proper planning.

Quick Answer: Essential High Net Worth Tax Strategies

- Maximize tax-advantaged accounts – 401(k) contributions up to $23,000 ($30,500 if 50+), backdoor Roth IRAs, HSAs

- Use trusts strategically – Spousal Lifetime Access Trusts (SLATs), Grantor Retained Annuity Trusts (GRATs)

- Leverage annual gifting – $18,000 per recipient annually ($36,000 for couples) to reduce estate size

- Implement tax-loss harvesting – Offset gains with losses, carry forward excess losses

- Optimize charitable giving – Donor-advised funds, Qualified Charitable Distributions from IRAs

- Plan for estate taxes – Use $13.61 million lifetime exemption before it potentially drops in 2026

The stakes are higher when you’re wealthy. A single mistake can cost tens of thousands. The good news? Proactive planning can save you more in taxes than most people earn in a year.

Time matters more than you think. The Tax Cuts and Jobs Act provisions expire at the end of 2025, potentially cutting estate tax exemptions in half. High-income earners face the highest tax brackets (37% federal), plus state taxes that can push total rates above 50%.

As someone who has spent 40 years helping high-income earners and business owners steer complex tax strategies, I’ve seen how proper high net worth tax planning can preserve millions for families. The most successful wealthy individuals treat tax planning as an ongoing strategy, not a once-a-year event.

Easy high net worth tax planning word list:

– tax-efficient estate planning

– advanced tax strategies

– tax-efficient investments

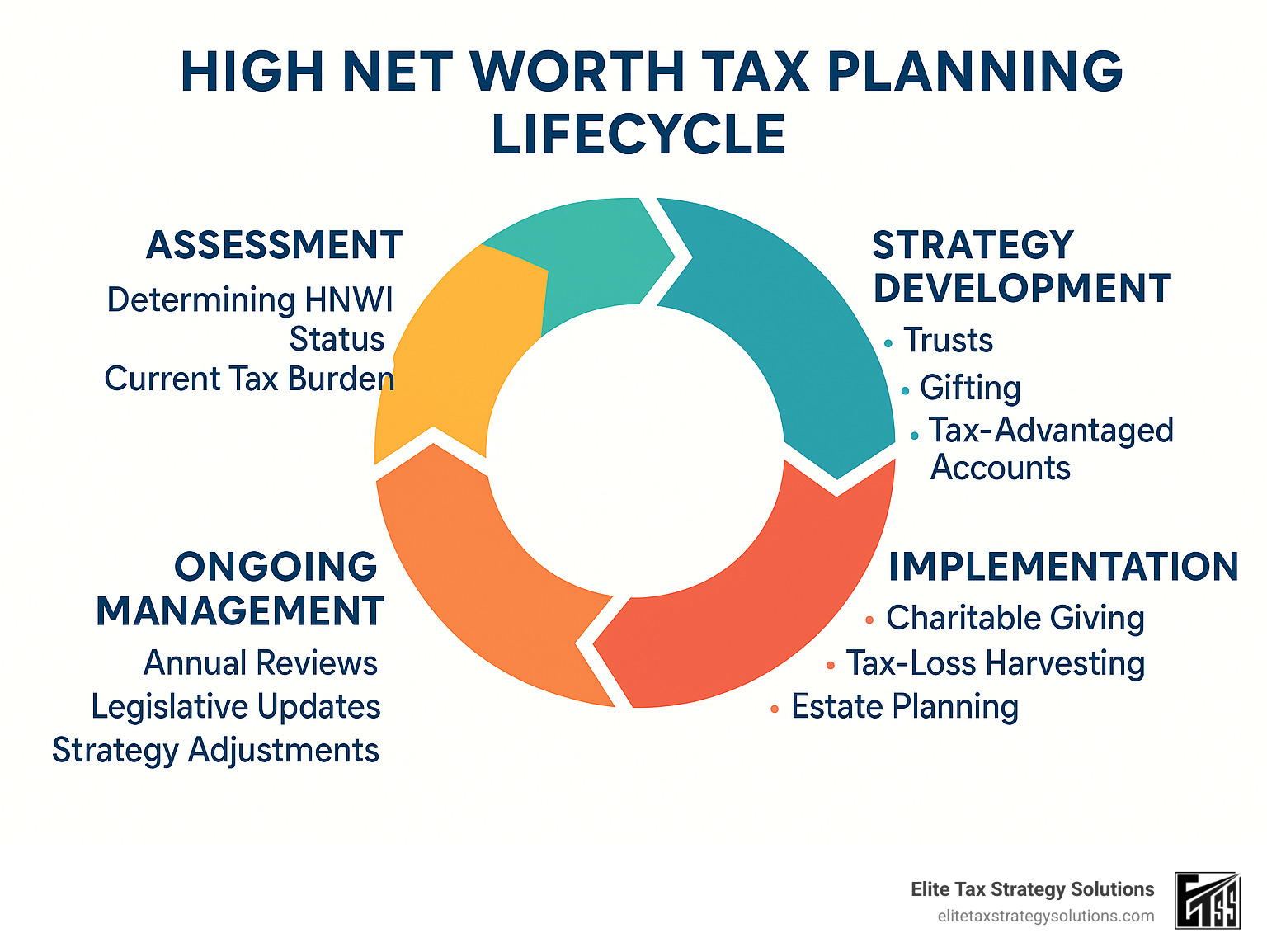

Mapping Your Tax Landscape

Think of high net worth tax planning like navigating with a GPS – you need to know exactly where you are before you can plot the best route to your destination. Your wealth level determines which tax strategies are available to you, and more importantly, which ones will actually move the needle.

What Makes You “High-Net-Worth”?

You officially join the high-net-worth individual (HNWI) club when you have at least $1 million in investable assets. Notice I said investable – this doesn’t include your primary home or that classic car collection. We’re talking about stocks, bonds, cash, and investment real estate.

Once you hit $30 million or more in investable assets, you graduate to ultra-high-net-worth individual (UHNWI) status. At this level, you’re dealing with challenges that most financial advisors have never encountered.

Here’s what makes your tax situation fundamentally different: You face higher tax brackets with taxable incomes over $609,350 ($731,200 for married couples filing jointly), putting you in the highest federal bracket at 37%. The Alternative Minimum Tax (AMT) becomes a real concern. Your investment income gets complicated quickly with diverse streams from stocks, bonds, real estate, and possibly business interests. And estate tax exposure becomes a major concern – without proper planning, estates over $13.61 million face a 40% federal estate tax.

Three Taxes That Matter Most

Income tax hits your earned income hard – salary, bonuses, and ordinary investment income. At the highest brackets, federal rates reach 37%, and when you add state taxes, total rates can push above 50% in high-tax states.

Capital gains tax offers some relief, but not as much as you might hope. Long-term capital gains get preferential treatment at 0%, 15%, or 20% depending on your income level. However, high earners also face the 3.8% Net Investment Income Tax, bringing the top effective rate to 23.8%.

Estate tax can be the most devastating without proper planning. The federal estate tax rate hits 40% on amounts exceeding the $13.61 million exemption ($27.22 million for married couples). Some states add their own estate taxes with even lower exemptions.

The key insight is that each tax requires different strategies. That’s why effective high net worth tax planning requires a coordinated approach that addresses all three simultaneously.

Core High Net Worth Tax Planning Strategies

When you’re managing significant wealth, every tax dollar you save is a dollar that can continue growing for your family. The most successful wealthy families understand that high net worth tax planning isn’t about one big strategy – it’s about layering multiple approaches that work together.

High Net Worth Tax Planning With Accounts

Even if you’re earning seven figures, don’t overlook the basics. Tax-advantaged retirement accounts are still your best friends – they’re just more powerful when you have the income to maximize them.

Your 401(k) lets you defer $23,000 in 2024 ($30,500 if you’re 50 or older). That might seem small compared to your total income, but it’s still a guaranteed tax reduction.

The Mega Backdoor Roth is where things get exciting. If your employer’s 401(k) plan allows after-tax contributions and in-plan conversions, you can potentially contribute up to $69,000 annually. This includes your regular contribution, employer match, and additional after-tax dollars that convert to Roth.

Health Savings Accounts are criminally underused by wealthy families. The triple tax benefit is unbeatable. Contributions reduce current taxes, growth is tax-free, and withdrawals for medical expenses are tax-free. In 2024, you can contribute $4,150 individually or $8,300 for families, plus an extra $1,000 if you’re 55 or older.

The Backdoor Roth IRA keeps you in the Roth game even when your income is too high for direct contributions. You contribute $7,000 to a non-deductible traditional IRA ($8,000 if 50+), then immediately convert it to a Roth.

For more detailed guidance on maximizing these opportunities, explore our proactive tax strategies.

Harvesting Losses & Gains

Tax-loss harvesting is like getting paid to clean up your portfolio. When investments lose value, you can sell them to create tax losses that offset gains elsewhere. You can deduct up to $3,000 of net losses against ordinary income each year, and any excess carries forward indefinitely.

The wash-sale rule is the main gotcha here. You can’t buy back the same security within 30 days of selling it for a loss, or the IRS disallows your deduction. But you can buy something similar to maintain your market exposure.

Direct indexing takes this strategy to the next level. Instead of owning an index fund, you own the individual stocks that make up the index. This lets you harvest losses on specific companies even when the overall index is rising.

Charitable Power Plays

Charitable giving offers some of the most powerful tax strategies available, especially when you’re in high tax brackets.

Donor-Advised Funds are like charitable checking accounts. You contribute cash or appreciated securities, get an immediate tax deduction, and then recommend grants to charities over time. You avoid capital gains on donated securities and can “bunch” multiple years of giving into one tax year.

Qualified Charitable Distributions are perfect for retirees. If you’re 70½ or older, you can send up to $100,000 annually directly from your IRA to charity. The distribution doesn’t count as taxable income and can satisfy your Required Minimum Distribution. Learn more about QCDs from the IRS.

Bunching your charitable giving can dramatically increase your tax benefits. Instead of giving $20,000 annually, consider giving $40,000 every other year. This pushes your itemized deductions above the standard deduction in the giving year while you take the standard deduction in the off year.

Trusts, Gifting & Estate Shields

When your wealth approaches the federal estate tax exemption of $13.61 million, estate planning transforms from optional to essential. Without proper planning, your family could lose 40% of everything above this threshold to estate taxes. High net worth tax planning through strategic trusts and gifting can preserve millions for your heirs.

Using Trusts for High Net Worth Tax Planning

Trusts aren’t just legal documents gathering dust in a filing cabinet. They’re powerful wealth preservation tools that serve two critical functions: minimizing taxes and protecting assets from creditors.

Spousal Lifetime Access Trusts (SLATs) offer an neat solution for married couples. You create an irrevocable trust for your spouse, removing assets from your estate while your spouse retains access to the trust funds. Each spouse can create a SLAT for the other, effectively doubling the benefit while maintaining some access to your wealth.

Intentionally Defective Grantor Trusts (IDGTs) sound complicated, but the concept is straightforward. You sell appreciating assets to the trust in exchange for a promissory note. The trust pays you back with interest, but because you’re treated as the owner for income tax purposes, no income is recognized on those interest payments. This strategy freezes the asset’s value in your estate while transferring all future appreciation to your heirs tax-free.

Grantor Retained Annuity Trusts (GRATs) work beautifully for assets you expect to appreciate significantly. You transfer the assets to the trust but retain an annuity payment for a specified period. Any appreciation above the IRS assumed interest rate passes to your beneficiaries without using your gift tax exemption.

Strategic Gifting in Action

The annual gift tax exclusion might seem small at $18,000 per recipient in 2024 ($36,000 for married couples), but it adds up quickly. A married couple with four adult children and their spouses can gift $288,000 annually without touching their lifetime exemption.

529 Plan Superfunding boosts your gifting strategy. You can front-load five years’ worth of annual exclusion gifts into a 529 plan at once – that’s $90,000 per beneficiary in 2024, or $180,000 for married couples. This immediately removes the funds from your estate while providing tax-free growth for education expenses.

Valuation discounts provide additional leverage when gifting interests in family businesses or limited partnerships. These gifts often qualify for discounts of 20-40% due to lack of marketability and minority interest restrictions.

Life Insurance & Liquidity

Irrevocable Life Insurance Trusts (ILITs) keep life insurance death benefits out of your taxable estate. The trust owns the policy and receives the death benefit, providing your heirs with estate-tax-free liquidity. This is particularly valuable when your estate consists largely of illiquid assets like real estate or family businesses.

Life insurance also serves as an estate tax bridge, providing immediate cash to pay estate taxes without forcing your heirs to sell inherited assets at fire-sale prices. Learn more about charitable remainder trusts for additional estate planning strategies.

Investment & Withdrawal Optimization

Your investment structure and withdrawal strategy can make or break your high net worth tax planning efforts. Many wealthy investors lose hundreds of thousands in unnecessary taxes simply because they don’t understand asset location – the art of putting the right investments in the right types of accounts.

Building a Tax-Smart Portfolio

Municipal bonds deserve serious consideration when you’re in the highest tax brackets. Yes, they typically offer lower yields than corporate bonds, but if you’re paying 37% federal taxes plus state taxes (potentially over 50% total), a 4% tax-free municipal bond can be equivalent to an 8% taxable bond.

Tax-efficient ETFs and index funds minimize capital gains distributions through their structure. Unlike actively managed funds that generate taxable distributions through frequent trading, these funds use in-kind redemptions to minimize capital gains distributions. Clients often reduce their annual tax drag by 1-2% simply by switching from active funds to tax-efficient alternatives.

Private equity and alternative investments offer unique tax advantages through carried interest treatment and depreciation benefits. However, they require meticulous record-keeping and often generate complex K-1 forms that can delay your tax filing.

Cryptocurrency basis tracking is critical. Every single transaction – even trading Bitcoin for Ethereum – creates a taxable event. The IRS expects detailed records, and penalties for non-compliance are severe.

For deeper insights into structuring your portfolio for maximum tax efficiency, explore our comprehensive guide on tax-efficient investments.

Retirement Distribution Playbook

Roth conversion ladders represent one of the most powerful strategies for long-term tax optimization. Convert traditional IRA assets to Roth IRAs during years when your income is lower, paying taxes at reduced rates to secure tax-free growth forever. This strategy works particularly well during market downturns when account values are temporarily depressed.

Required Minimum Distribution management becomes critical once you hit age 73. The IRS forces you to withdraw specific amounts from traditional retirement accounts, whether you need the money or not. Smart planning involves coordinating these mandatory withdrawals with charitable giving, tax-loss harvesting, and other income sources.

Withdrawal sequencing follows a general rule: taxable accounts first, tax-deferred accounts second, and tax-free Roth accounts last. But exceptions abound based on your specific circumstances.

| Account Type | Tax Treatment | Withdrawal Strategy |

|---|---|---|

| Taxable | Gains taxed at capital gains rates | First priority – most flexible |

| Tax-Deferred (401k, Traditional IRA) | Withdrawals taxed as ordinary income | Second priority – manage brackets |

| Tax-Free (Roth IRA) | No taxes on qualified withdrawals | Last priority – preserve tax-free growth |

Navigating Compliance, Residency & Alternative Assets

The tax landscape for wealthy individuals changes constantly. New regulations, expiring provisions, and evolving investment structures mean that what worked last year might not work today. Staying ahead of these changes isn’t just about compliance – it’s about protecting your wealth from unnecessary taxation.

Stay Ahead of Changing Rules

The clock is ticking on some major tax benefits. The Tax Cuts and Jobs Act provisions expire at the end of 2025, and the changes could be dramatic. The lifetime gift and estate tax exemption, currently sitting at $13.61 million, is scheduled to drop to approximately $7 million (adjusted for inflation) in 2026.

This creates a massive planning opportunity for 2024 and 2025. If you’ve been considering significant gifts to family members or charitable organizations, these next two years offer a window that may not come again for decades.

The State and Local Tax (SALT) cap is another sunset provision worth watching. The current $10,000 limit on state and local tax deductions has been particularly painful for high earners in states like California, New York, and New Jersey. This limitation is also set to expire after 2025.

Don’t forget about the Alternative Minimum Tax (AMT). While the TCJA raised AMT exemption amounts, high earners can still get caught by this parallel tax system. The AMT essentially says “we don’t care how many deductions you have – you’re going to pay at least this much in taxes.”

Alternative Assets & Real Estate

Real estate and alternative investments offer unique tax advantages, but they also come with complex rules.

1031 Like-Kind Exchanges remain one of the most powerful tools for real estate investors. You can defer capital gains taxes indefinitely by exchanging investment properties for similar properties. The timing requirements are strict and unforgiving. You have exactly 45 days to identify potential replacement properties and 180 days to complete the exchange.

Qualified Opportunity Zone (QOZ) Funds offer an interesting twist on capital gains deferral. You can defer capital gains taxes by investing those gains in designated economically distressed areas. Hold the investment for 10 years, and any appreciation in the QOZ investment becomes completely tax-free.

Private equity professionals often benefit from carried interest treatment, where their share of investment profits gets taxed as capital gains rather than ordinary income. Recent legislation added a three-year holding period requirement for this preferential treatment.

Cryptocurrency continues to evolve as an asset class, but the tax rules are becoming clearer. Every transaction – including trading one cryptocurrency for another – creates a taxable event that must be reported. Maintaining accurate basis records is essential as the IRS increases enforcement.

The complexity of high net worth tax planning with alternative assets requires careful coordination between your tax advisor, investment manager, and estate planning attorney.

Frequently Asked Questions about High Net Worth Tax Planning

When you’re managing significant wealth, certain questions come up repeatedly in our planning sessions. These are the ones that keep high-net-worth individuals up at night – and rightfully so, given the tax implications involved.

How do trusts reduce estate taxes?

Think of trusts as a way to have your cake and eat it too – well, sort of. The magic happens because trusts remove assets from your taxable estate while still allowing you to retain some benefits or control.

Take a Grantor Retained Annuity Trust (GRAT), for example. You transfer appreciating assets into the trust but keep receiving annuity payments for a set period. Any appreciation above the IRS assumed interest rate passes to your beneficiaries completely gift-tax-free.

Spousal Lifetime Access Trusts (SLATs) work differently but just as effectively. These irrevocable trusts permanently remove assets from your estate, reducing future estate tax liability. Your spouse can still access the trust assets if needed, so you’re not completely cutting yourself off from the wealth.

The key is proper structuring. The IRS has specific rules about what makes a trust truly independent from your estate. Get it wrong, and those assets come right back into your taxable estate.

What is the difference between a donor-advised fund and a private foundation?

Donor-advised funds are the simpler, more flexible option for most charitable giving. You contribute assets, receive an immediate tax deduction, and then recommend grants to qualified charities over time. There’s no minimum distribution requirement, administrative costs typically run under 1%, and you can start with relatively modest amounts.

Private foundations are the heavyweight option – think of them as your family’s personal charity. They require more than $1 million to be cost-effective and come with serious responsibilities. You must distribute at least 5% of assets annually, pay excise taxes, and deal with complex reporting requirements.

But here’s why some families choose foundations despite the complexity: they offer complete control and can exist forever. Your great-grandchildren could still be running your family foundation, carrying on your charitable legacy.

For more sophisticated charitable strategies, you might also consider charitable remainder trusts, which provide income to you or your family while ultimately benefiting charity. The IRS provides detailed guidance on charitable remainder trusts for those interested in this powerful planning tool.

How often should I update my tax plan?

Most wealthy families don’t review their tax plans nearly often enough. They set up their strategies and then forget about them until something major happens – usually something that could have been planned for.

We recommend comprehensive annual reviews as your baseline. Think of it like an annual physical for your wealth. The tax code changes, your life changes, and your financial situation evolves.

But don’t wait for your annual review if significant life events occur. Major income changes like selling a business or receiving an inheritance can completely alter your tax landscape. Family changes such as marriage, divorce, births, or deaths often require immediate strategy adjustments.

Legislative changes are particularly critical right now. The upcoming TCJA sunset in 2025 will dramatically impact estate planning strategies. Market volatility can also trigger the need for portfolio rebalancing and tax-loss harvesting opportunities.

The most successful high-net-worth families treat high net worth tax planning as an ongoing conversation, not an annual event. Regular monitoring allows us to spot opportunities and threats before they become expensive problems.

Conclusion

Effective high net worth tax planning requires a comprehensive, proactive approach that evolves with your wealth and changing tax laws. The strategies we’ve outlined – from maximizing tax-advantaged accounts to implementing sophisticated trust structures – can save high-net-worth families hundreds of thousands or even millions in taxes over time.

The key is starting early and maintaining consistency. The families who achieve the best results treat tax planning as an integral part of their wealth management strategy, not an afterthought during tax season.

At Elite Tax Strategy Solutions, we’ve spent decades helping high-income earners and business owners in Indiana and suburban areas near major cities steer these complex strategies. Our thorough, proactive approach to tax optimization ensures you’re not leaving money on the table while maintaining full compliance with evolving tax laws.

The Tax Cuts and Jobs Act provisions expire at the end of 2025, creating both challenges and opportunities. The time to act is now, whether you’re implementing gifting strategies to use your lifetime exemption or restructuring investments for maximum tax efficiency.

The complexity of high-net-worth tax planning demands specialized expertise. Working with professionals who understand the intricacies of trust law, estate planning, and advanced tax strategies is essential for achieving optimal results while avoiding costly mistakes.

Your wealth represents years of hard work and smart decisions. Protecting it from unnecessary taxation through strategic planning isn’t just about saving money – it’s about preserving your legacy for future generations and maximizing your ability to support the causes and people you care about most.

For comprehensive guidance custom to your specific situation, explore our comprehensive financial planning services. The investment in proper planning today will pay dividends for generations to come.