High-income tax planning is crucial for those seeking to steer the complexities of tax laws while optimizing their financial outcomes. If managing your wealth efficiently and minimizing tax liabilities matter to you, here’s what you need to focus on:

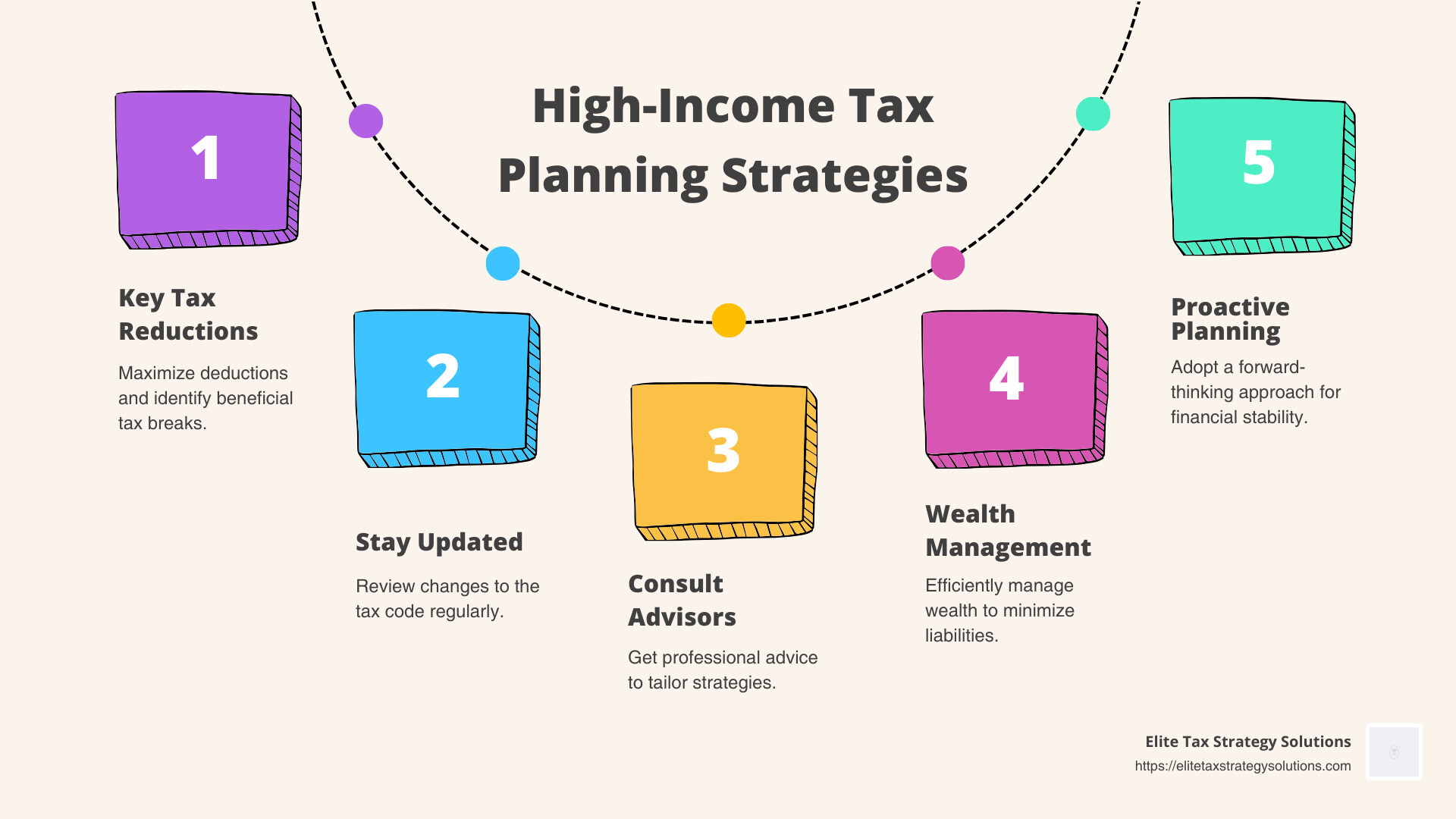

- Understanding Key Tax Reduction Strategies: Maximize deductions and identify the most beneficial tax breaks.

- Staying Updated on Latest Tax Laws: Regularly review changes to the tax code affecting high-income earners.

- Consulting a Financial Advisor: Leverage professional advice to tailor tax-saving strategies to your unique financial situation.

By incorporating these strategies, high-income earners can tackle their tax obligations more effectively.

My name is David Fritch. With over 40 years of experience in law and tax advisory services, I’ve dedicated my career to explaining high-income tax planning. My expertise lies in helping clients effectively manage their taxes and ensure financial stability.

Quick high-income tax planning definitions:

– business tax reduction

– tax planning for real estate investors

– tax planning for small businesses

Understanding High-Income Tax Planning

When it comes to high-income tax planning, understanding the intricacies of tax brackets, adjusted gross income (AGI), and taxable income is essential. Let’s break these concepts down to make them easier to grasp.

Tax Brackets

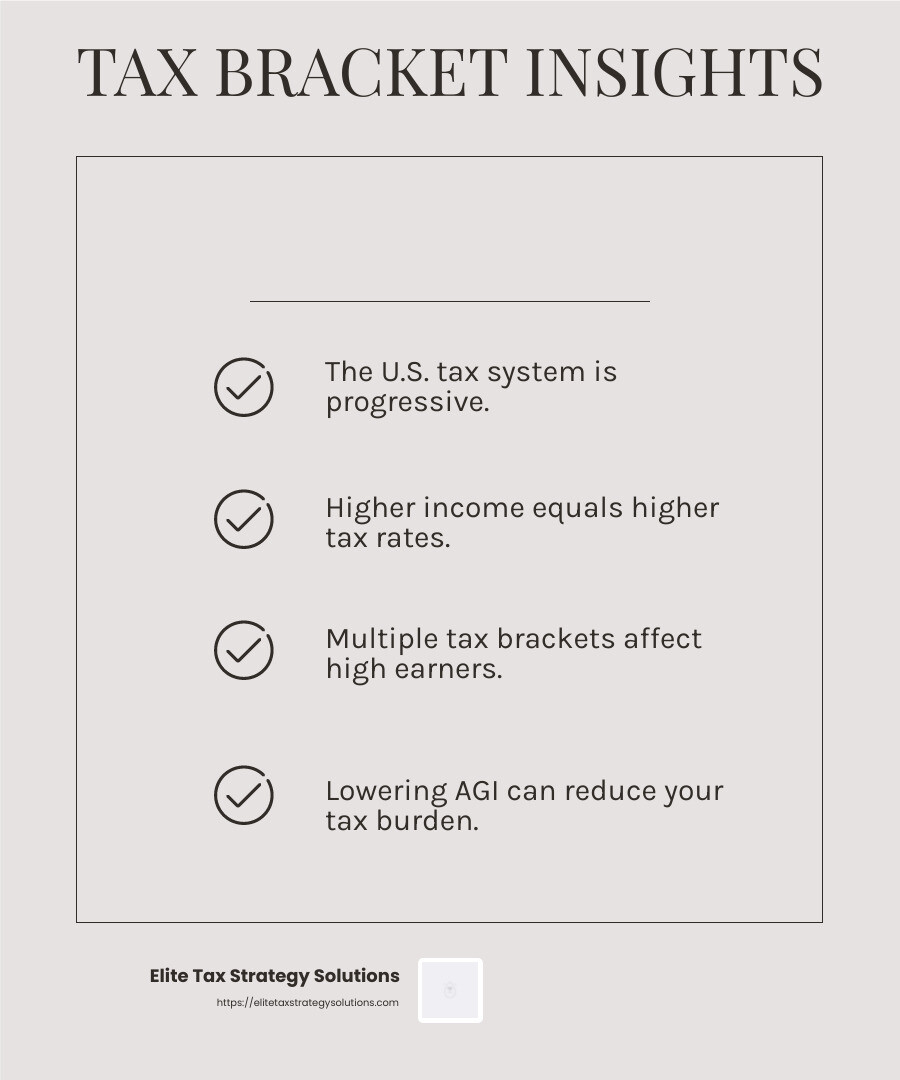

The U.S. tax system is progressive, meaning that as your income increases, so does your tax rate. This is organized into tax brackets, which determine the rate at which your income is taxed. For high-income earners, the top tax brackets can significantly impact how much you owe to the IRS. For example, if you’re a single filer with a taxable income over $191,951, you fall into one of the top three tax brackets.

Adjusted Gross Income (AGI)

Your Adjusted Gross Income is your total income minus specific deductions, such as retirement contributions or student loan interest. AGI is a critical figure because it’s used to determine your eligibility for various tax credits and deductions. Lowering your AGI can reduce your taxable income, potentially moving you into a lower tax bracket and reducing your tax bill.

Taxable Income

Taxable income is the portion of your income that is subject to taxes after all allowable deductions and exemptions. It’s the figure on which your tax liability is calculated. High-income earners often have complex financial situations, which can include multiple sources of income and various deductions. Understanding how to strategically manage these can lead to significant tax savings.

Here’s a quick breakdown of how these elements interact:

- Gross Income: Your total income from all sources.

- Deductions: Subtract deductions to find your AGI.

- Exemptions and Additional Deductions: Subtract these from your AGI to find your taxable income.

By understanding and managing these elements, high-income earners can effectively steer tax obligations and optimize their financial outcomes. This knowledge is a cornerstone of effective high-income tax planning and can lead to substantial tax savings when applied correctly.

Key Tax Reduction Strategies for High-Income Earners

When you’re a high-income earner, tax reduction strategies become essential tools in your financial toolkit. Let’s explore some effective methods to reduce your tax burden: retirement contributions, charitable contributions, and health savings accounts (HSAs).

Retirement Contributions

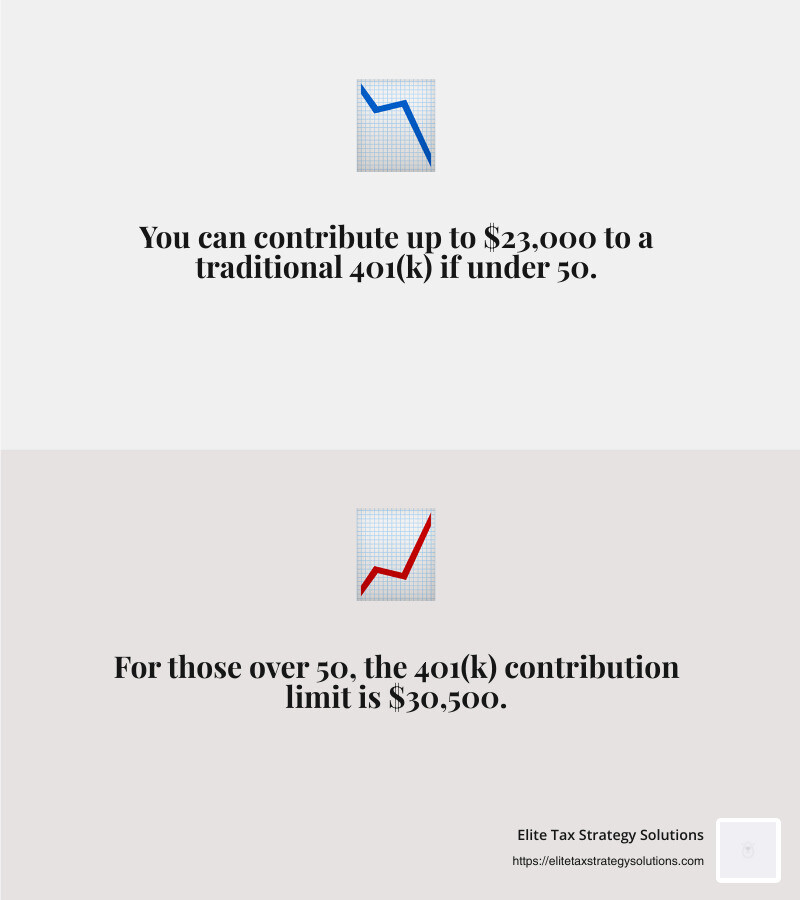

Maximizing contributions to retirement accounts is a smart move for high-income earners. By contributing to a traditional 401(k) or IRA, you reduce your taxable income. This means you pay less tax now while saving for the future.

In 2024, you can contribute up to $23,000 to a traditional 401(k) if you’re under 50, and $30,500 if you’re over 50. For a traditional IRA, the limit is $7,000, or $8,000 if you’re over 50.

Charitable Contributions

Giving to charity not only feels good but also offers tax benefits. When you donate to qualified charities, you may deduct the value of your gifts from your taxable income. This can help reduce your overall tax bill.

Remember to keep records of your donations and ensure the charity is IRS-approved. By strategically timing your gifts, you can maximize these deductions.

Health Savings Accounts (HSAs)

An HSA is a triple-tax-advantaged account: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free.

For 2024, you can contribute up to $4,150 for individuals or $8,300 for families. If you’re 55 or older, there’s an additional $1,000 catch-up contribution available.

To qualify for an HSA, you must have a high-deductible health plan. This account not only helps you save on taxes but also provides a cushion for future medical expenses.

By leveraging these key tax reduction strategies, you can effectively lower your taxable income and keep more of your hard-earned money. Next, we’ll dig into advanced strategies for high-income earners, such as income deferral and Roth IRA conversions.

Advanced Tax Strategies for High-Income Earners

For high-income earners, advanced tax strategies can make a significant difference in managing tax liabilities. Let’s dig into some effective techniques: income deferral, Roth IRA conversions, and municipal bonds.

Income Deferral

Income deferral is a powerful strategy that allows you to postpone receiving a portion of your income to a future year. This can be especially beneficial if you expect to be in a lower tax bracket later. By deferring income, you reduce your current taxable income, potentially lowering your tax rate.

Deferred compensation plans are a common tool for high-income earners to implement this strategy. These plans allow you to receive income, such as bonuses or salaries, at a later date, typically during retirement when your tax rate might be lower.

Roth IRA Conversions

Roth IRA conversions are another strategic tool for high-income earners. While you may not be eligible to contribute directly to a Roth IRA due to income limits, you can convert funds from a traditional IRA to a Roth IRA. This process involves paying taxes on the converted amount now, but it allows for tax-free growth and withdrawals in the future.

Timing is crucial with Roth conversions. Consider converting during years with lower income or when tax rates are favorable. Consulting with a tax advisor can help you steer the complexities and optimize the benefits of this strategy.

Municipal Bonds

Investing in municipal bonds can offer substantial tax advantages. The interest income from these bonds is generally exempt from federal taxes and may also be exempt from state and local taxes if you live in the issuing state.

For high-income earners, this tax-exempt status can make municipal bonds an attractive investment, especially if you reside in a state with high income tax rates. While munis typically offer lower interest rates compared to taxable bonds, their tax-equivalent yield can be quite competitive, particularly for those in higher tax brackets.

By incorporating these advanced tax strategies into your financial plan, you can effectively manage your tax burden and improve your overall financial well-being. Next, we’ll explore how changing the character of your income can further optimize your tax situation.

Changing the Character of Your Income

High-income earners can benefit significantly by changing the character of their income. Let’s explore how business structure, tax-exempt bonds, and index funds can play a role in this strategy.

Business Structure

Choosing the right business structure can transform your tax situation. For example, converting your business to a C-corporation might be beneficial. C-corps offer a lower top tax rate compared to S-corps or sole proprietorships. Plus, if your business is a pass-through entity, you might qualify for a deduction of up to 20% of your business income.

Restructuring your business can also provide opportunities to hire family members. By employing your minor children, you might avoid payroll taxes on their earnings, as children’s earnings are taxed at lower rates.

Tax-Exempt Bonds

Investing in tax-exempt bonds, like municipal bonds, is another way to change the character of your income. Interest from these bonds is generally not subject to federal income tax. If you buy bonds issued in your state, you could also avoid state and local taxes.

For high-income earners, this tax-free income can be a smart addition to your portfolio. While these bonds might offer lower interest rates compared to taxable bonds, the tax savings can make them more appealing, especially if you’re in a high tax bracket.

Index Funds

Index funds and exchange-traded funds (ETFs) are known for their tax efficiency. They typically have lower turnover rates compared to actively managed funds, which means fewer capital gains distributions.

For high-income earners, this can mean less taxable income each year. By investing in index funds or ETFs, you can manage your tax liabilities while still benefiting from market growth.

By strategically changing the character of your income, you can optimize your tax situation and potentially lower your tax burden. Next, we’ll address some frequently asked questions about high-income tax planning, providing more insights into how you can effectively manage your taxes.

Frequently Asked Questions about High-Income Tax Planning

How to reduce taxes as a high-income earner?

Reducing taxes as a high-income earner involves smart planning and strategic use of various tax-saving tools. Retirement contributions are one of the most powerful ways to lower taxable income. By contributing to a Traditional 401(k) or IRA, you can deduct contributions from your total income, reducing the amount subject to tax. For 2024, high-income earners can contribute up to $23,000 to a Traditional 401(k) and $7,000 to a Traditional IRA, with higher limits for those over 50.

Charitable contributions also offer a way to decrease taxable income. Donations to qualified charities can be deducted, which lowers your taxable income. This not only benefits you by reducing taxes but also supports causes you care about.

What is considered a high-income taxpayer?

The IRS defines a high-income earner as someone who reports $200,000 or more in total income on their tax return. Total income includes all sources, from wages to dividends. Understanding where you stand in terms of tax brackets is crucial for planning. In 2024, the federal income tax brackets range from 10% to 37%, depending on your income level and filing status.

How to avoid the 32% tax bracket?

Avoiding the 32% tax bracket requires careful income timing and planning. If you anticipate being close to this bracket, consider deferring some income to the following year. This can be achieved through deferred compensation plans, which allow you to delay receiving part of your income until retirement, potentially lowering your taxable income for the year.

Additionally, maximizing deductible expenses can help keep you below the 32% bracket. Expenses like mortgage interest, state and local taxes, and medical expenses can be deducted, reducing your taxable income.

By leveraging these strategies, high-income earners can effectively manage their tax obligations and potentially keep more of their hard-earned money.

Conclusion

Navigating the complexities of high-income tax planning can feel like solving a puzzle. However, with the right strategies, it’s possible to minimize your tax burden and improve your financial stability. At Elite Tax Strategy Solutions, we specialize in crafting personalized tax plans that align with your financial goals and help you keep more of what you earn.

Proactive tax planning is not just about reducing taxes today; it’s about securing your financial future. By taking advantage of strategies like income deferral, Roth IRA conversions, and investing in municipal bonds, you can effectively manage your tax liabilities. Our team of experts is dedicated to staying ahead of tax law changes, ensuring that your plan is always optimized for your unique situation.

As high-income earners, it’s crucial to understand the impact of tax brackets and taxable income on your financial health. By working with us, you gain access to a wealth of knowledge and resources that can help you steer the tax maze with confidence. Our comprehensive approach ensures that every aspect of your tax situation is addressed, from maximizing deductions to strategically timing income.

The goal isn’t to avoid taxes altogether—it’s about making smart decisions that align with your long-term financial objectives. Whether you’re planning for retirement, considering charitable contributions, or exploring new investment opportunities, our team is here to guide you every step of the way.

For those ready to take control of their financial future, contact Elite Tax Strategy Solutions today. Let us help you develop a tax plan that not only saves you money but also supports your broader financial aspirations.