Financial planning for high income earners is not just about growing your wealth—it’s about protecting it. Here are immediate steps to ensure your financial stability and optimize your taxes:

1. Establish an emergency fund: Aim to save three to six months of expenses.

2. Maximize employer-sponsored retirement plans: Contribute enough to get full employer matches.

3. Address high-interest debt: Pay off credit cards and loans with high-interest rates.

4. Explore diverse investment avenues: Consider real estate, taxable accounts, and more.

Managing finances proactively is key to maintaining long-term wealth. By leveraging tax-saving strategies and planning for the future, high-income earners can minimize liabilities and boost their financial health. In this guide, we’ll cover everything you need to create a robust financial plan custom to your needs.

I’m David Fritch, with over 40 years of experience in financial planning and tax strategy, having served high-income earners and small business owners. My aim is to simplify complex tax regulations and provide proven strategies for financial success.

Financial planning for high income earners word guide:

– extra medicare tax for high earners

– high net worth tax strategies

Establishing a Financial Safety Net

Financial planning for high income earners starts with establishing a strong safety net. One of the most critical components of this safety net is an emergency fund.

The Importance of an Emergency Fund

Life is unpredictable. Even with a high income, unexpected expenses can arise. Whether it’s a sudden medical emergency, a major car repair, or a job loss, having an emergency fund can make these situations manageable.

Financial experts recommend saving between three to six months’ worth of living expenses. This fund acts as a financial buffer, giving you peace of mind and reducing stress during tough times.

Why three to six months? This range provides a cushion that can cover most unforeseen expenses without causing a significant financial strain. For high-income earners, this fund is essential because it ensures that your financial plan remains intact, even when unexpected costs arise.

Building Your Emergency Fund

-

Calculate Your Monthly Expenses: Include rent/mortgage, utilities, groceries, insurance, and other essentials. Multiply this by three to six to determine your emergency fund goal.

-

Automate Your Savings: Set up automatic transfers from your checking account to a dedicated savings account. This way, you consistently save without having to think about it.

-

Prioritize Your Fund: Before investing in other areas, ensure your emergency fund is fully funded. This step is foundational to any robust financial plan.

Real-Life Example

Consider Jane, a high-income earner in the healthcare sector. She diligently saved six months’ worth of expenses. When she faced an unexpected medical bill, she didn’t have to dip into her retirement savings or take on debt. Her emergency fund covered the costs, and her long-term financial plan stayed on track.

The Psychological Comfort

Having an emergency fund isn’t just about the money—it’s about the peace of mind it brings. Knowing you have a financial cushion allows you to make better decisions without the pressure of immediate financial stress.

Key Takeaways

- Save three to six months’ worth of expenses: This provides a solid financial buffer.

- Automate your savings: Make it easy and consistent.

- Prioritize building this fund: It’s the foundation of your financial safety net.

Next, we’ll explore how to maximize employer-sponsored retirement plans to further secure your financial future.

Maximizing Employer-Sponsored Retirement Plans

Employer-sponsored retirement plans are a cornerstone of financial planning for high income earners. These plans, such as 401(k) and 403(b), offer significant tax benefits and the potential for employer matching, which can substantially boost your retirement savings.

Understanding 401(k) and 403(b) Plans

401(k) plans are common in the private sector, while 403(b) plans are typically offered to employees of public schools and certain non-profit organizations. Both plans allow you to contribute a portion of your salary on a pre-tax basis, reducing your taxable income for the year.

In 2023, the maximum contribution limit for a 401(k) is $22,500. If you’re 50 or older, you can make an additional “catch-up” contribution of $7,500, bringing the total to $30,000. These contributions grow tax-free until you withdraw them in retirement.

The Power of Employer Match

One of the most attractive features of employer-sponsored retirement plans is the employer match. Many employers will match your contributions up to a certain percentage of your salary. This is essentially free money that can significantly improve your retirement savings.

For example, if your employer matches 50% of your contributions up to 6% of your salary, and you earn $200,000 annually, contributing 6% ($12,000) would result in an additional $6,000 from your employer. That’s a 50% return on your investment before any market gains.

Tax Benefits of 401(k) and 403(b) Plans

Contributing to a 401(k) or 403(b) plan offers immediate tax benefits by reducing your taxable income. For high-income earners, this can mean substantial tax savings each year. The money in these accounts grows tax-deferred, meaning you won’t pay taxes on the gains until you withdraw the funds in retirement.

Exploring Roth 401(k) Options

Many employers now offer Roth 401(k) options, which combine the benefits of a Roth IRA with the higher contribution limits of a 401(k). Contributions to a Roth 401(k) are made with after-tax dollars, but withdrawals in retirement are tax-free.

For high-income earners, splitting contributions between a traditional 401(k) and a Roth 401(k) can provide a balanced approach to tax planning. This strategy allows you to benefit from immediate tax deductions while also building a source of tax-free income for retirement.

Case Study: Maximizing Retirement Savings

Consider a successful executive earning $250,000 annually. By maxing out 401(k) contributions at $22,500 and taking advantage of an employer’s 50% match up to 6% of the salary, an additional $7,500 can be added to retirement savings each year. Over a 20-year period, assuming a modest annual growth rate of 6%, the account could grow to over $1.3 million, thanks in large part to the employer match and tax-deferred growth.

Key Takeaways

- Max out your contributions: Aim to contribute the maximum allowed each year to take full advantage of tax benefits and employer matching.

- Understand your employer’s match: Contribute at least enough to get the full match—it’s free money.

- Consider a Roth 401(k): Diversifying between traditional and Roth contributions can provide tax benefits now and in retirement.

Next, we’ll discuss how to address high-interest debt to improve your overall financial health.

Addressing High-Interest Debt

High-interest debt can be a significant drain on your financial health. As a high-income earner, it’s crucial to tackle this type of debt head-on to free up more of your income for savings and investments. Let’s dig into the key areas to focus on: credit card debt and car loans.

Credit Card Debt

Credit card debt often carries some of the highest interest rates, sometimes exceeding 20% annually. This can quickly snowball, making it difficult to pay off the principal amount.

Steps to Manage Credit Card Debt:

-

List All Debts: Start by listing all your credit card debts, including the outstanding balance, interest rate, and minimum monthly payment.

-

Prioritize High-Interest Cards: Focus on paying off the card with the highest interest rate first. This is known as the avalanche method and helps minimize the total interest paid over time.

-

Consider Balance Transfers: If you have a good credit score, look into balance transfer offers. These can provide a temporary reprieve with lower or even 0% interest rates for a set period.

-

Automate Payments: Set up automatic payments to ensure you never miss a due date, which can lead to additional fees and higher interest rates.

Car Loans

Car loans can also carry relatively high-interest rates, especially if your credit score was lower at the time of purchase. Paying off your car loan early can save you a substantial amount in interest.

Tips for Managing Car Loans:

-

Refinance: If your credit score has improved, consider refinancing your car loan to secure a lower interest rate.

-

Make Extra Payments: Whenever possible, make extra payments towards the principal. This reduces the overall amount on which interest is calculated.

-

Bi-Weekly Payments: Switching to bi-weekly payments instead of monthly can help you pay off the loan faster and reduce interest.

Financial Health

Addressing high-interest debt is a critical step in improving your overall financial health. By eliminating these debts, you can redirect your income towards more productive investments and savings.

Benefits of Paying Off High-Interest Debt:

- Increased Cash Flow: Freeing up money that was previously going towards interest payments.

- Better Credit Score: Reducing your debt-to-income ratio can improve your credit score.

- Lower Stress: Financial stability leads to reduced stress and better mental health.

By prioritizing high-interest debt, you set a solid foundation for achieving long-term financial goals. Once these debts are under control, you can focus on maximizing your savings and investments.

Next, we’ll explore how to broaden your retirement savings for even greater financial security.

Broadening Your Retirement Savings

Maximizing your retirement savings is a crucial step in financial planning for high-income earners. By fully utilizing your retirement accounts, you can significantly reduce your taxable income and build a robust financial future. Let’s explore the key strategies for broadening your retirement savings.

Max Out Contributions

One of the most effective ways to boost your retirement savings is to max out your contributions to employer-sponsored retirement plans like the 401(k) or 403(b).

For 2024, the contribution limit for these plans is $23,000 for individuals under 50, and $30,500 for those 50 or older.

Why max out?

-

Tax Benefits: Contributions to these plans are typically tax-deferred, meaning you won’t pay taxes on the money until you withdraw it in retirement. This can lower your taxable income now, potentially placing you in a lower tax bracket.

-

Employer Matching: Many employers offer matching contributions. Not taking full advantage of this is like leaving free money on the table. Always aim to contribute at least enough to get the full match.

Tax Benefits

Maximizing your retirement contributions offers substantial tax benefits. Here’s how:

-

Tax-Deferred Growth: Investments within a 401(k) or 403(b) grow tax-free until you withdraw the money. This allows your investments to compound more efficiently.

-

Lower Tax Bracket: By reducing your taxable income through contributions, you might fall into a lower tax bracket, reducing your overall tax liability.

Retirement Funds

Building a substantial retirement fund is essential for long-term financial security. By maximizing contributions and taking advantage of tax benefits, you can ensure a comfortable retirement.

Strategies to Improve Your Retirement Funds:

-

Diversify Investments: Within your retirement accounts, diversify your investments to balance risk and reward. Consider a mix of stocks, bonds, and other assets.

-

Automatic Increases: Some retirement plans allow you to automatically increase your contributions annually. This can be a painless way to boost your savings over time.

-

Regular Reviews: Periodically review your retirement accounts to ensure they align with your financial goals. Adjust contributions and investments as needed.

Real-Life Example

Consider Jane, a high-income earner in her early 40s. She maximizes her 401(k) contributions, taking full advantage of her employer’s 5% match. By doing so, she reduces her taxable income significantly and benefits from tax-deferred growth. Over 20 years, Jane’s diligent contributions and smart investment choices allow her to amass a substantial retirement fund, providing financial security and peace of mind.

By focusing on maxing out contributions, leveraging tax benefits, and strategically growing your retirement funds, you can set yourself up for a financially secure future.

Next, we’ll discuss the benefits of leveraging Roth IRAs through backdoor conversions to further improve your retirement strategy.

Leveraging Roth IRAs Through Backdoor Conversions

For high-income earners, traditional Roth IRA contributions are often off-limits due to income restrictions. But don’t worry, there’s a perfectly legal workaround known as the backdoor Roth IRA. This strategy allows you to enjoy the benefits of a Roth IRA regardless of your income level.

What is a Backdoor Roth IRA?

A backdoor Roth IRA involves a two-step process:

- Contribute to a Traditional IRA: Even high earners can contribute to a traditional IRA. For 2024, you can contribute up to $7,000 (or $8,000 if you’re 50 or older) to a traditional IRA.

- Convert to a Roth IRA: Once your contribution posts, you convert the traditional IRA to a Roth IRA. You’ll pay taxes on the amount converted, but future growth and withdrawals in retirement will be tax-free.

The Benefits of a Backdoor Roth IRA

1. Tax-Free Growth:

When you convert your traditional IRA to a Roth IRA, the money inside the account grows tax-free. This means you won’t pay taxes on the investment gains, allowing your money to compound more efficiently over time.

2. Financial Flexibility:

Roth IRAs offer more flexibility compared to traditional IRAs. You can withdraw your contributions (not earnings) at any time, tax-free and penalty-free. This can be a valuable feature if you need access to funds before retirement.

3. No Required Minimum Distributions (RMDs):

Roth IRAs are not subject to RMDs during the account holder’s lifetime. This allows your investments to continue growing tax-free for as long as you live, giving you more control over your retirement funds.

Example: How a Backdoor Roth IRA Works

Let’s look at a high-income earner who wants to leverage a backdoor Roth IRA. Here’s how it works:

- Step 1: They contribute $7,000 to their traditional IRA.

- Step 2: They immediately convert the traditional IRA to a Roth IRA.

- Step 3: They pay taxes on the $7,000 contribution, but now their money can grow tax-free in the Roth IRA.

Important Considerations

- Tax Implications: When you convert to a Roth IRA, you’ll pay taxes on the converted amount. Make sure you have the cash on hand to cover this tax bill.

- Existing IRAs: If you already have traditional IRAs with pre-tax contributions, the tax calculation for the conversion can get complicated. Consult a tax professional to understand the implications.

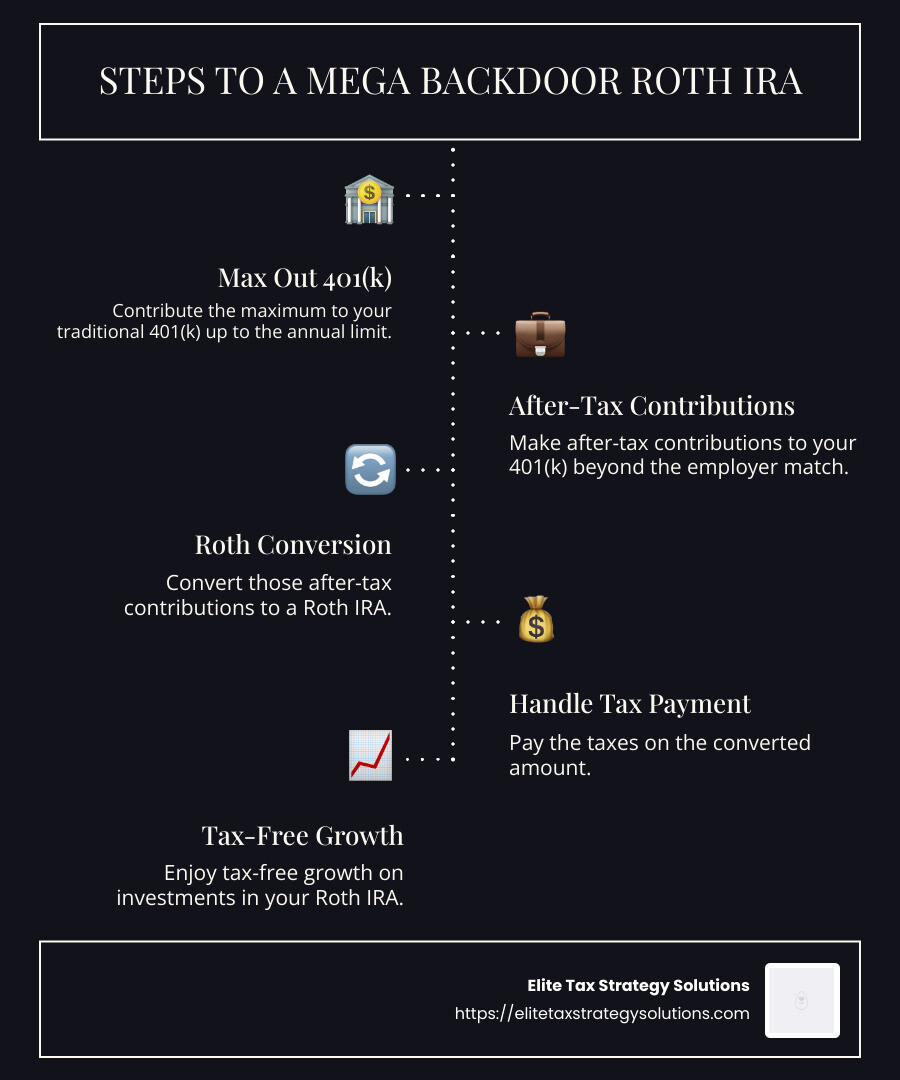

Mega Backdoor Roth IRA

For those who want to contribute even more, some employers offer a Mega Backdoor Roth option. This allows after-tax contributions to a 401(k) that can be rolled over to a Roth IRA, potentially increasing your annual Roth contributions up to $66,000.

Real-Life Case Study

Consider a high-income earner who uses the backdoor Roth IRA strategy every year, contributing $7,000 annually. Over 20 years, assuming a 6% annual return, their Roth IRA grows to nearly $275,000. And because it’s a Roth IRA, they can withdraw this money tax-free in retirement, providing significant financial security.

By leveraging the backdoor Roth IRA, high-income earners can enjoy tax-free growth and financial flexibility, ensuring a robust retirement strategy.

Next, we’ll explore the triple tax advantages of Health Savings Accounts (HSAs) and how they can further improve your financial planning.

Health Savings Accounts (HSAs): Triple Tax Advantages

Health Savings Accounts (HSAs) are a powerful tool for high-income earners. They offer triple tax advantages: tax-deductible contributions, tax-deferred growth, and tax-free withdrawals for qualified medical expenses.

Tax-Deductible Contributions

Contributions to an HSA are made with pre-tax dollars. This reduces your taxable income for the year, providing immediate tax savings. For 2024, the IRS has set the individual contribution limit at $4,150 and the family contribution limit at $8,300.

Example: If you contribute the maximum $8,300 to your HSA and you’re in the 35% tax bracket, you could save $2,905 in taxes that year.

Tax-Deferred Growth

The money in your HSA grows tax-deferred. This means you don’t pay taxes on the interest, dividends, or capital gains as long as the money remains in the account. Over time, this can result in significant growth, especially if you invest the funds.

Fact: Unlike Flexible Spending Accounts (FSAs), HSAs do not have a “use it or lose it” rule. Your funds roll over year after year, allowing your savings to compound.

Tax-Free Withdrawals

Withdrawals from an HSA are tax-free if used for qualified medical expenses. This includes a wide range of expenses such as doctor visits, prescriptions, and even some over-the-counter medications.

Pro Tip: Keep receipts for all medical expenses paid out of pocket. You can reimburse yourself from your HSA at any time, even years later, as long as the expenses were incurred after the HSA was established.

Real-Life Case Study

Meet Alex, a high-income earner who contributes the family maximum of $8,300 to his HSA annually. Over 20 years, assuming a 6% annual return, Alex’s HSA grows to about $315,000. He uses this money tax-free to cover medical expenses during retirement, significantly reducing his out-of-pocket costs.

Important Considerations

- Medicare Enrollment: Once you enroll in Medicare, you can no longer contribute to an HSA. However, you can still use the funds for qualified medical expenses.

- Contribution Limits: Be aware of the annual contribution limits to avoid penalties.

Maximizing HSA Benefits

To fully leverage an HSA, consider the following strategies:

- Max Out Contributions: Aim to contribute the maximum allowed amount each year.

- Invest Wisely: If your HSA provider offers investment options, consider investing in mutual funds or ETFs to grow your savings.

- Keep Detailed Records: Maintain records of all medical expenses to ensure you can reimburse yourself tax-free in the future.

By utilizing HSAs, high-income earners can enjoy significant tax savings and prepare for future medical expenses. Next, we’ll dive into additional pre-tax savings opportunities that can further improve your financial planning.

Additional Pre-Tax Savings Opportunities

When it comes to financial planning for high income earners, maximizing pre-tax savings is crucial. Beyond traditional retirement accounts and HSAs, there are other valuable pre-tax savings options to consider, such as 457(b) plans, especially for those in academic medicine or public sector roles.

457(b) Plans

457(b) plans are retirement savings plans offered to employees of state and local governments and certain non-profit organizations. These plans allow you to defer a portion of your salary pre-tax, reducing your taxable income for the year.

Key Benefits:

- Deferred Taxation: Contributions grow tax-deferred, meaning you don’t pay taxes on the earnings until you withdraw the funds.

- High Contribution Limits: For 2024, you can contribute up to $22,500 annually, or $30,000 if you’re over 50.

- Catch-Up Contributions: In the last three years before retirement age, you may be eligible to contribute even more, potentially doubling your annual contribution limit.

Example: A high-income earner in a state university contributes the maximum of $22,500 to their 457(b) plan. This reduces their taxable income and allows their investments to grow tax-deferred, providing a significant boost to their retirement savings.

Academic Medicine

For those in academic medicine, 457(b) plans are often a key part of their financial strategy. Academic institutions frequently offer these plans as a complement to other retirement accounts, such as 403(b) plans.

Advantages for Academic Professionals:

- Dual Contributions: You can contribute to both a 403(b) and a 457(b) plan, maximizing your pre-tax savings.

- Flexible Withdrawals: Unlike other retirement accounts, 457(b) plans do not impose a 10% early withdrawal penalty if you leave your job before age 59½. This can be a significant advantage if you plan to retire early or change careers.

Case Study: A professor at a medical school contributes to both their 403(b) and their 457(b) plans. By doing so, they defer a significant portion of their income, reducing their current tax liability while building a substantial retirement nest egg.

Deferred Taxation

Deferred taxation is a powerful concept in financial planning. It allows your investments to grow without being taxed annually, which can lead to substantial growth over time.

How It Works:

- Tax-Deferred Accounts: Contributions to accounts like 457(b) plans grow tax-deferred. You only pay taxes when you withdraw the funds in retirement, ideally when you are in a lower tax bracket.

- Compounding Growth: By avoiding annual taxes on earnings, your investments can compound more effectively, leading to greater wealth accumulation.

Pro Tip: Regularly review your tax-deferred accounts and adjust your contributions to maximize your tax benefits. This proactive approach can significantly improve your long-term financial health.

Maximizing Pre-Tax Savings

To fully leverage these pre-tax savings opportunities, consider the following strategies:

- Max Out Contributions: Aim to contribute the maximum allowed amount to your 457(b) plan each year.

- Dual Plan Participation: If eligible, contribute to both 403(b) and 457(b) plans to maximize your pre-tax savings.

- Plan for Withdrawals: Understand the rules and penalties associated with withdrawals to avoid unnecessary taxes and fees.

By incorporating 457(b) plans and understanding the benefits of deferred taxation, high-income earners can significantly improve their financial planning strategy. Next, we’ll explore how to save for education expenses using 529 plans.

Educational Savings: The 529 Plans

Saving for your child’s college education can be daunting, but 529 plans make it easier. These plans offer tax-free growth and withdrawals for qualified educational expenses, making them an attractive option for high-income earners.

What is a 529 Plan?

A 529 plan is a tax-advantaged savings plan designed to encourage saving for future education costs. These plans are sponsored by states, state agencies, or educational institutions.

Key Features:

- Tax-Free Growth: Investments in a 529 plan grow tax-free, meaning you don’t pay taxes on earnings as long as the withdrawals are used for qualified educational expenses.

- Qualified Expenses: These include tuition, fees, books, supplies, and even room and board at eligible institutions.

- State Tax Benefits: Many states offer tax deductions or credits for contributions to a 529 plan, providing additional savings.

Benefits of 529 Plans

1. Tax-Free Growth and Withdrawals

One of the biggest advantages of a 529 plan is the tax treatment of earnings. As long as the funds are used for qualified educational expenses, the growth is tax-free.

Example: If you invest $10,000 in a 529 plan and it grows to $20,000, you can withdraw the entire $20,000 for educational expenses without paying any taxes on the $10,000 gain.

2. High Contribution Limits

529 plans have high contribution limits, often exceeding $300,000 per beneficiary. This makes them suitable for high-income earners who want to save substantial amounts for education.

3. Estate Planning Benefits

Contributing to a 529 plan can also help with estate planning. You can contribute up to five times the annual gift tax exclusion limit at once, removing those contributions from your gross taxable estate.

Example: In 2023, the annual gift tax exclusion is $17,000. You can contribute up to $85,000 per beneficiary in a single year without incurring gift taxes.

How to Get Started with a 529 Plan

1. Choose a Plan

Research and select a 529 plan that fits your needs. Many states offer their own plans, but you are not limited to your home state’s plan.

2. Open an Account

Opening a 529 account is straightforward. Most plans allow you to open an account online with minimal paperwork.

3. Set Up Contributions

Decide how much you want to contribute regularly. You can set up automatic contributions to make saving easier.

4. Invest Wisely

529 plans offer various investment options, including age-based portfolios that adjust the asset allocation as the beneficiary gets closer to college age.

Case Study: Jane and Mark, high-income earners, started a 529 plan for their daughter when she was born. By contributing $500 per month, they accumulated over $100,000 by the time she turned 18, all of which can be used tax-free for her college expenses.

Maximizing Your 529 Plan

1. Start Early: The earlier you start, the more time your investments have to grow tax-free.

2. Take Advantage of State Tax Benefits: If your state offers tax deductions or credits, make sure to take full advantage.

3. Monitor and Adjust: Regularly review your investment choices and adjust as needed to ensure you’re on track to meet your education savings goals.

Conclusion

By leveraging the benefits of 529 plans, high-income earners can effectively save for their children’s education while enjoying significant tax advantages. Next, we’ll discuss how to build flexibility through taxable investment accounts.

Building Flexibility Through Taxable Investment Accounts

Taxable investment accounts offer a unique blend of flexibility and accessibility that can be highly beneficial for high-income earners. Unlike retirement accounts, these accounts have no contribution limits and allow you to withdraw funds at any time without penalties.

Key Features of Taxable Investment Accounts

1. No Contribution Limits

One of the biggest advantages of taxable investment accounts is the absence of contribution limits. Whether you want to invest $1,000 or $100,000, you can do so without any restrictions.

Example: If you receive a large bonus at work, you can invest the entire amount in a taxable account without worrying about hitting any caps.

2. Accessibility

Funds in taxable accounts can be withdrawn at any time for any purpose without incurring early withdrawal penalties. This makes them ideal for mid-term goals or unexpected expenses.

Example: If you need to make a down payment on a new home, you can easily liquidate some of your investments.

3. No Required Minimum Distributions (RMDs)

Unlike certain retirement accounts, taxable investment accounts do not have RMDs. You decide when and how much to withdraw, giving you complete control over your money.

Pros of Investing in Taxable Accounts

Flexibility: Withdraw funds anytime for any reason without penalties.

Investment Choices: Wide range of investment options, including stocks, bonds, ETFs, and mutual funds.

No Contribution Limits: Invest as much as you want each year.

Cons of Investing in Taxable Accounts

No Tax Breaks: Investments are made with after-tax money, and you’ll pay capital gains taxes upon selling investments. Dividends and interest are also taxable.

Liability: Investments in taxable accounts are not protected from lawsuits, unlike certain retirement accounts. It’s wise to consider umbrella insurance for added protection.

Strategies for Tax-Efficient Investing

Even though taxable accounts don’t offer the same tax advantages as retirement accounts, you can still invest tax-efficiently:

1. Use Tax-Efficient Funds

Consider investing in exchange-traded funds (ETFs), which generally generate fewer taxable events compared to mutual funds.

2. Consider Municipal Bonds

For the fixed-income portion of your portfolio, municipal bonds can be a smart choice. These bonds often generate tax-free interest payments, depending on the issuer.

3. Tax-Loss Harvesting

Offset gains by selling investments at a loss. This strategy can help reduce your taxable income and lower your tax bill.

Case Study: Sarah’s Early Retirement Fund

Sarah, a high-income earner, wanted to retire early. She maxed out her retirement accounts but needed more savings. By investing in a taxable account, she was able to save an additional $200,000 over ten years. This fund provided her with the flexibility to retire at 55, using the money without worrying about penalties or RMDs.

Conclusion

Taxable investment accounts offer high-income earners a flexible and accessible way to grow their wealth. By understanding the pros and cons and employing tax-efficient strategies, you can make the most of these accounts. Next, we’ll explore other investment avenues, such as real estate and small businesses, to further diversify your portfolio.

Exploring Other Investment Avenues

When you’re a high-income earner, maximizing your wealth often means looking beyond traditional investments. Real estate and small businesses offer unique opportunities but come with higher risks and demands. Let’s break down these options.

Real Estate

Real estate is a popular choice for those looking to diversify. It can provide steady income and appreciate over time. However, it’s not without challenges.

Types of Real Estate Investments:

- Residential Properties: Buying homes or apartments to rent out.

- Commercial Properties: Investing in office buildings, shopping centers, or warehouses.

- Land: Purchasing land in developing areas.

Example: Suppose you buy a rental property. You could earn monthly rent, and the property value might increase. But you’ll also need to manage tenants and maintenance.

Pros:

- Income Stream: Rental properties can provide regular income.

- Appreciation: Real estate often increases in value over time.

- Tax Benefits: Deductions for mortgage interest, property taxes, and depreciation.

Cons:

- Time-Consuming: Managing properties requires effort.

- Risk: Property values can fluctuate, and vacancies can affect income.

- High Initial Investment: Requires significant upfront capital.

Small Businesses

Investing in small businesses can be rewarding but is also risky. Whether you’re starting your own business or investing in someone else’s, it’s crucial to do your homework.

Example: Imagine investing in a local coffee shop. If the shop thrives, you could see significant returns. But if it fails, you could lose your investment.

Pros:

- Potential High Returns: Successful businesses can yield substantial profits.

- Control: If you start your own business, you control its direction.

- Diversification: Adds another layer to your investment portfolio.

Cons:

- High Risk: Many small businesses fail within the first few years.

- Time and Effort: Running or managing a business requires dedication.

- Financial Commitment: Starting or investing in a business often requires a large upfront investment.

Higher Risks

Both real estate and small business investments come with higher risks compared to traditional investments like stocks and bonds. It’s essential to weigh these risks against the potential rewards.

Key Considerations:

- Market Research: Understand the market and potential pitfalls.

- Financial Planning: Ensure you have the financial stability to handle potential losses.

- Professional Advice: Consult with financial advisors to make informed decisions.

Case Study: Real Estate Portfolio

A high-income earner diversified their investments by purchasing three rental properties. Over five years, they earned a steady rental income and saw their property values increase by 20%. However, they also faced challenges like tenant turnover and unexpected repairs. By balancing these risks with other investments, they successfully grew their wealth.

Conclusion

Exploring other investment avenues like real estate and small businesses can offer high-income earners significant returns. However, these options come with higher risks and require careful planning and management. Next, we’ll address some frequently asked questions about financial planning for high-income earners.

Frequently Asked Questions about Financial Planning for High Income Earners

What is the 401(k) strategy for high earners?

For high-income earners, a 401(k) can be a powerful tool for retirement savings. Here’s how to maximize it:

1. Maximize Contributions: In 2023, you can contribute up to $22,500 to your 401(k). If you’re 50 or older, you can make an additional catch-up contribution of $7,500.

2. Consider a Roth 401(k): Unlike traditional 401(k) contributions, which are tax-deferred, Roth 401(k) contributions are made with after-tax dollars. This means your withdrawals in retirement will be tax-free. Splitting your contributions between a traditional and Roth 401(k) can provide tax benefits now and in the future.

3. Employer Match: Don’t leave free money on the table. Many employers match a portion of your contributions. Ensure you contribute enough to get the full match.

4. Brokerage Link: Some 401(k) plans offer a brokerage link, allowing you to invest in a broader range of options, including individual stocks and ETFs, giving you greater growth potential.

5. Catch-Up Contributions: Starting in 2024, if your W-2 income exceeds $145,000, any catch-up contributions must be made to a Roth 401(k). If your employer doesn’t offer a Roth 401(k), you won’t be able to make catch-up contributions.

Example: Imagine Jane, a high-income earner, splits her contributions between a traditional and Roth 401(k). She benefits from immediate tax deductions and enjoys tax-free withdrawals in retirement.

What is considered a high income earner?

High income earners are typically defined by their annual income. Here’s a quick breakdown:

1. Top 1%: Earning approximately $540,000 or more annually places you in the top 1% of earners in the U.S.

2. Top 5%: An annual income of around $225,000 qualifies you as part of the top 5%.

Being a high-income earner means you have unique financial planning needs and opportunities. It’s crucial to leverage tax-advantaged accounts and strategies to preserve your wealth.

How to invest with a $150K salary?

Earning $150,000 annually puts you in a strong position to build wealth. Here are some strategies:

1. Diversify Your Portfolio: Invest in a mix of stocks, ETFs, and index funds. This approach spreads risk and can provide steady growth.

2. Real Estate: Consider investing in real estate for rental income and potential appreciation. This could include residential properties, commercial properties, or REITs (Real Estate Investment Trusts).

3. Max Out Retirement Accounts: Fully fund your 401(k) and consider a backdoor Roth IRA conversion to take advantage of tax-free growth.

4. Taxable Investment Accounts: These accounts offer flexibility with no contribution limits or early withdrawal penalties. They’re ideal for mid-term goals or early retirement.

Example: Mark, earning $150K, invests in a mix of index funds and real estate. He maxes out his 401(k) and uses a taxable investment account for additional savings. This diversified approach helps him grow his wealth while managing risk.

5. Professional Advice: Consult with a financial advisor to tailor your investment strategy to your specific goals and risk tolerance.

By following these strategies, high-income earners can effectively manage their wealth, minimize taxes, and prepare for a comfortable retirement.

Conclusion

At Elite Tax Strategy Solutions, we understand the unique challenges that high-income earners face. Our mission is to provide personalized tax planning services that help you maximize your tax savings and achieve financial stability.

Personalized Tax Planning

We believe in a proactive approach to tax optimization. Our team of seasoned professionals works closely with you to understand your financial situation and long-term goals. We then craft custom strategies to minimize your tax liabilities and improve your financial well-being.

Maximizing Tax Savings

High-income earners have numerous opportunities to save on taxes, but navigating the complex tax code can be daunting. That’s where we come in. Our experts stay updated on the latest tax laws and regulations, ensuring that you benefit from every available tax-saving strategy.

For example:

– Maximizing Retirement Contributions: We help you take full advantage of 401(k) and Roth IRA contributions, ensuring you benefit from tax-deferred or tax-free growth.

– Deferring Income: We guide you on deferring bonuses or other income to manage your tax brackets effectively.

– Utilizing Tax Credits and Deductions: We identify all eligible credits and deductions to reduce your taxable income.

Comprehensive Financial Planning

Financial planning for high-income earners isn’t just about taxes. It’s about creating a holistic strategy that includes retirement planning, debt reduction, investment diversification, and more. Our integrated approach ensures that all aspects of your financial life work together seamlessly.

Case Study:

Imagine Sarah, a high-income earner, who came to us with a complex financial situation. By implementing a combination of tax deferral strategies, maximizing her retirement contributions, and diversifying her investments, we helped her reduce her tax burden and set a clear path toward her financial goals.

Start Your Journey Today

Ready to take control of your financial future? Contact Elite Tax Strategy Solutions today to schedule a consultation. Our expert team is here to help you steer the complexities of tax planning and achieve your financial aspirations.

Remember: Effective financial planning is not a one-time event but an ongoing process. Regular reviews and adjustments are crucial to staying on track and maximizing your financial success.

By partnering with Elite Tax Strategy Solutions, you can be confident that you are making informed decisions that will benefit you now and in the future. Let’s work together to build a secure and prosperous financial future.

For more detailed information on our services, visit our Innovative Tax Planning page.