Navigating the Extra Medicare Tax: A Guide for High Income Earners

Extra medicare tax for high earners is an additional tax on top of the standard Medicare tax, affecting those with significant earnings. Here’s a quick breakdown for those in a hurry:

Key Points:

– Standard Medicare Tax Rate: 2.9% (1.45% each from employee and employer).

– Additional Medicare Tax Rate: 0.9% for high earners.

– Thresholds: $200,000 for single filers, $250,000 for married filing jointly, $125,000 for married filing separately.

If you surpass these income thresholds, you’ll be subject to this extra tax. Staying informed can save you a lot in the long run.

I’m David Fritch, an expert in helping high-income earners steer complex tax regulations, focusing on financial optimization. With over 40 years of tax planning experience, I’ve guided numerous clients in minimizing their tax liabilities through personalized strategies.

Understanding the Extra Medicare Tax

What is the Extra Medicare Tax?

The Extra Medicare Tax is a 0.9% surtax on top of the standard Medicare tax, introduced by the Affordable Care Act (ACA) in 2013. This additional tax applies to high-income earners and helps fund ACA provisions, such as premium tax credits for lower-income Americans.

Key Points:

– Standard Medicare Tax Rate: 2.9% (split between employee and employer).

– Additional Medicare Tax Rate: 0.9% for earnings above certain thresholds.

While the standard Medicare tax funds Medicare Part A, which covers hospital insurance for seniors and people with disabilities, the Extra Medicare Tax specifically supports ACA initiatives.

Who Pays the Extra Medicare Tax?

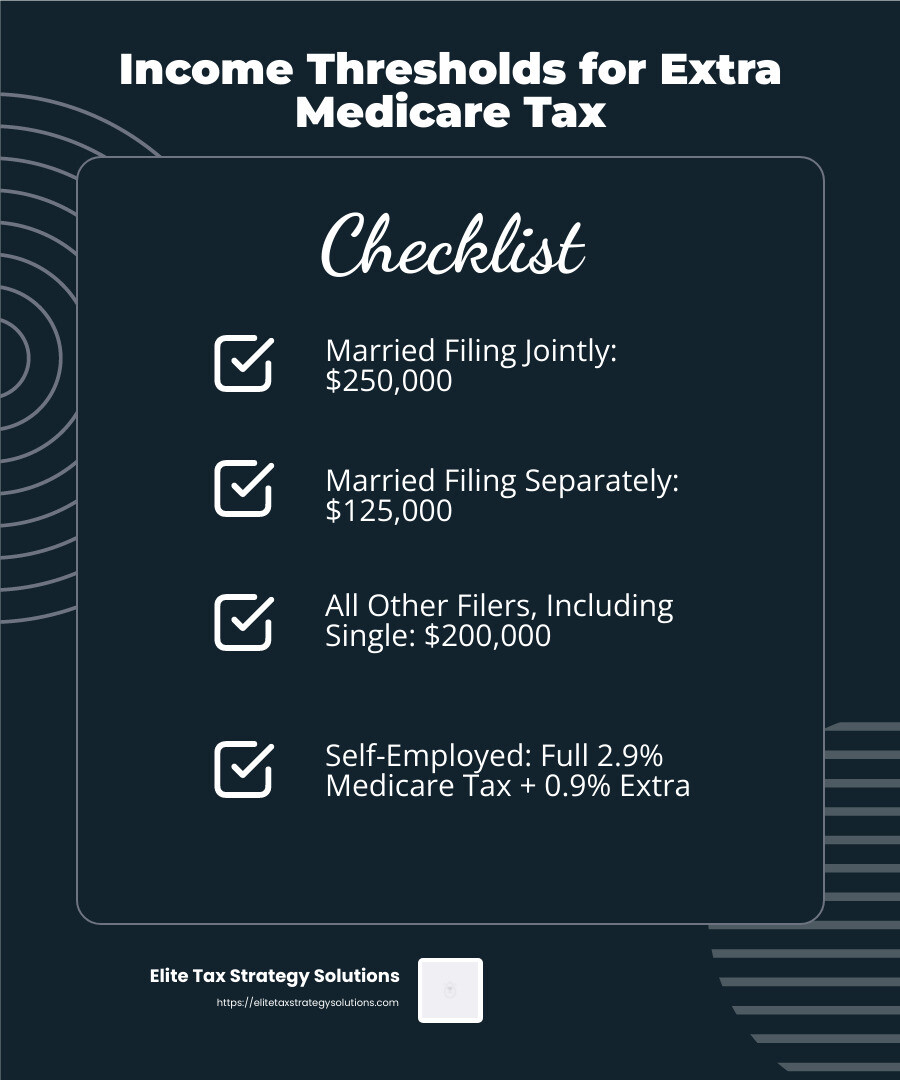

High-income earners are required to pay this additional 0.9% tax if their earnings exceed specific thresholds. These thresholds differ based on filing status:

| Filing Status | Annual Income Threshold |

|---|---|

| Married filing jointly | $250,000 |

| Married filing separately | $125,000 |

| All other filers (including single) | $200,000 |

For example, if a single filer earns $250,000 in a year, they will pay the standard 2.9% Medicare tax on the first $200,000 and an additional 0.9% on the remaining $50,000.

Important Notes:

– Self-employed individuals pay the full 2.9% Medicare tax and the additional 0.9% on income above the thresholds.

– There is no employer match for the Extra Medicare Tax.

– The IRS requires employers to withhold the additional 0.9% once an employee’s wages exceed $200,000, regardless of the employee’s filing status.

Understanding these thresholds and how the tax is applied can help high-income earners better manage their tax liabilities. In the next section, we’ll dive into how to calculate the Extra Medicare Tax and ensure you’re prepared come tax season.

Calculating the Extra Medicare Tax

Income Thresholds for the Extra Medicare Tax

The Extra Medicare Tax kicks in when your income surpasses certain thresholds, which vary by filing status:

- Married filing jointly: $250,000

- Married filing separately: $125,000

- All other filers (including single): $200,000

Example: If you’re a single filer with a salary of $250,000, the first $200,000 is subject to the standard Medicare tax (1.45% for the employee and 1.45% for the employer). The remaining $50,000 is subject to an extra 0.9% tax, resulting in a total Medicare tax rate of 2.35% on that portion.

How to Compute the Extra Medicare Tax

To compute the Extra Medicare Tax, you’ll need to consider three main types of income: Medicare wages, self-employment income, and Railroad Retirement Tax Act (RRTA) compensation. Here’s how to break it down:

1. Medicare Wages

First, calculate the additional tax on any Medicare wages exceeding the threshold for your filing status.

Example: If you are a single filer with $225,000 in wages, the first $200,000 is taxed at the standard rate. The extra $25,000 is taxed at an additional 0.9%.

2. Self-Employment Income

Next, reduce the applicable threshold by the total Medicare wages received (but not below zero). Calculate the additional tax on any self-employment income exceeding this reduced threshold.

Example: If you’re married filing jointly with $150,000 in wages and $175,000 in self-employment income:

– The threshold is reduced from $250,000 to $100,000 ($250,000 – $150,000).

– Additional Medicare Tax applies to $75,000 of self-employment income ($175,000 – $100,000).

3. RRTA Compensation

RRTA compensation is treated separately from Medicare wages and self-employment income. Apply the threshold to RRTA compensation independently.

Example: If one spouse earns $190,000 in wages and the other earns $150,000 in RRTA compensation, neither exceeds the $250,000 threshold for married filing jointly, so no additional tax is due.

IRS Guidelines and Form 8959

To report and compute the Extra Medicare Tax, use Form 8959, Additional Medicare Tax. Follow these steps:

- Calculate Wages: Identify wages exceeding the threshold.

- Adjust Threshold: Reduce the threshold by total Medicare wages.

- Calculate Self-Employment Income: Apply the reduced threshold to self-employment income.

- Complete Form 8959: Report the additional tax on your tax return.

Important: The IRS requires employers to withhold the Extra Medicare Tax once an employee’s wages exceed $200,000, regardless of filing status. This ensures compliance but may lead to over-withholding, which can be adjusted when filing your tax return.

By understanding these steps and thresholds, high-income earners can accurately calculate their Extra Medicare Tax and avoid surprises during tax season. Up next, we’ll explore the impact on employers and their responsibilities in withholding this tax.

Impact on Employers

Employer Withholding Requirements

Employers play a crucial role in managing the Extra Medicare Tax for high-income earners. While employers are not liable for the tax itself, they are responsible for withholding it from employees’ wages that exceed the $200,000 threshold in a calendar year.

Key Points:

– $200,000 Threshold: Employers must start withholding an additional 0.9% once an employee’s wages exceed $200,000, regardless of the employee’s filing status.

– Payroll Period: This withholding must begin in the payroll period when the employee’s wages exceed $200,000.

– No Employer Match: Unlike the standard Medicare tax, there is no employer match for the Extra Medicare Tax. Only the employee’s share is subject to the additional 0.9%.

Employers are required to withhold this tax even if an employee’s combined income with a spouse (or other sources) does not meet the threshold for the additional tax. This can lead to scenarios where employees may be over-withheld or under-withheld, which we will address next.

Correcting Withholding Errors

Errors in withholding the Extra Medicare Tax can occur, and it is crucial for employers to correct these promptly to avoid penalties from the IRS.

Under-Withholding:

If an employer realizes they have under-withheld the Extra Medicare Tax, they should correct this by deducting the correct amount from the employee’s wages by the end of the year. If the error is not caught within the same year, the employer may be liable for the amount not withheld, unless the employee pays the tax when filing their tax return.

Example: An employer fails to withhold the additional 0.9% for an employee who earns $250,000. The employer should adjust the withholding from subsequent wages within the same year to correct this. If not corrected, the employer may face liability.

Over-Withholding:

If an employer over-withholds the Extra Medicare Tax, they should reimburse the employee before the end of the year. Employers must also make an interest-free adjustment on the appropriate corrected form (e.g., Form 941-X).

Example: An employer starts withholding the additional 0.9% before the employee’s wages actually exceed $200,000. The employer should refund the over-withheld amount and adjust the reported wages.

IRS Penalties:

Employers who fail to meet their withholding, deposit, reporting, and payment responsibilities for the Extra Medicare Tax may be subject to penalties. It is essential to stay compliant to avoid these additional costs.

Important: If errors are finded in a subsequent year, employers cannot make interest-free adjustments. Instead, they should report the correct amount on the appropriate “X” form (e.g., Form 941-X) and ensure that the employee’s Form W-2 accurately reflects the withheld amount.

By understanding these responsibilities and correcting any errors promptly, employers can ensure compliance with IRS requirements and avoid potential penalties.

Next, we will dig into strategies to minimize the impact of the Extra Medicare Tax for high-income earners.

Strategies to Minimize the Extra Medicare Tax

Tax Planning Tips

Navigating the extra Medicare tax for high earners can be challenging, but with proactive tax planning, you can minimize its impact. Here are some effective strategies:

Income Deferral

One way to reduce your exposure to the extra Medicare tax is by deferring income. This means delaying the receipt of income to a future year when your overall earnings might be lower. For example, you could negotiate with your employer to receive bonuses in the next tax year. This could help keep your current year’s income below the $200,000 (single) or $250,000 (married) threshold.

Roth IRA Conversions

Converting a traditional IRA to a Roth IRA can be a smart move. While you will pay taxes on the converted amount now, the future distributions from the Roth IRA will be tax-free if certain conditions are met. This can help you avoid pushing your adjusted gross income (AGI) over the threshold in retirement, reducing your exposure to the extra Medicare tax.

Note: It’s generally better to pay the conversion taxes from another account to avoid additional penalties and taxes.

Investment Strategies

Managing your investments wisely can also help. Consider tax-efficient investment strategies such as:

- Tax-Loss Harvesting: This involves selling investments at a loss to offset gains and reduce your taxable income.

- Municipal Bonds: Income from municipal bonds is generally exempt from federal taxes and can help keep your AGI below the threshold.

Managing Investment Income

Investment income is a significant factor in the extra Medicare tax for high earners. Here’s how you can manage it effectively:

Net Investment Income

The 3.8% Medicare tax applies to net investment income, which includes taxable interest, dividends, capital gains, rental income, and more. To reduce this tax:

- Allocate Investments Wisely: Place high-yield investments in tax-advantaged accounts like IRAs and 401(k)s.

- Monitor Distributions: Be mindful of distributions from mutual funds and other investments that could push your income over the threshold.

Modified Adjusted Gross Income (MAGI)

The extra Medicare tax is calculated based on your MAGI. To manage your MAGI:

- Charitable Contributions: Making charitable contributions can reduce your taxable income.

- Retirement Contributions: Increase contributions to retirement accounts like 401(k)s and IRAs to lower your AGI.

Capital Gains

Capital gains can significantly impact your exposure to the extra Medicare tax. Consider these tips:

- Timing: Plan the timing of your capital gains. For instance, if you anticipate a large gain, you might spread it over multiple years to stay below the threshold.

- Installment Sales: If selling a large asset, consider an installment sale to spread the gain over several years.

By implementing these strategies, you can effectively manage your income and investments to minimize the impact of the extra Medicare tax.

Next, we will address some frequently asked questions about the extra Medicare tax.

Frequently Asked Questions about the Extra Medicare Tax

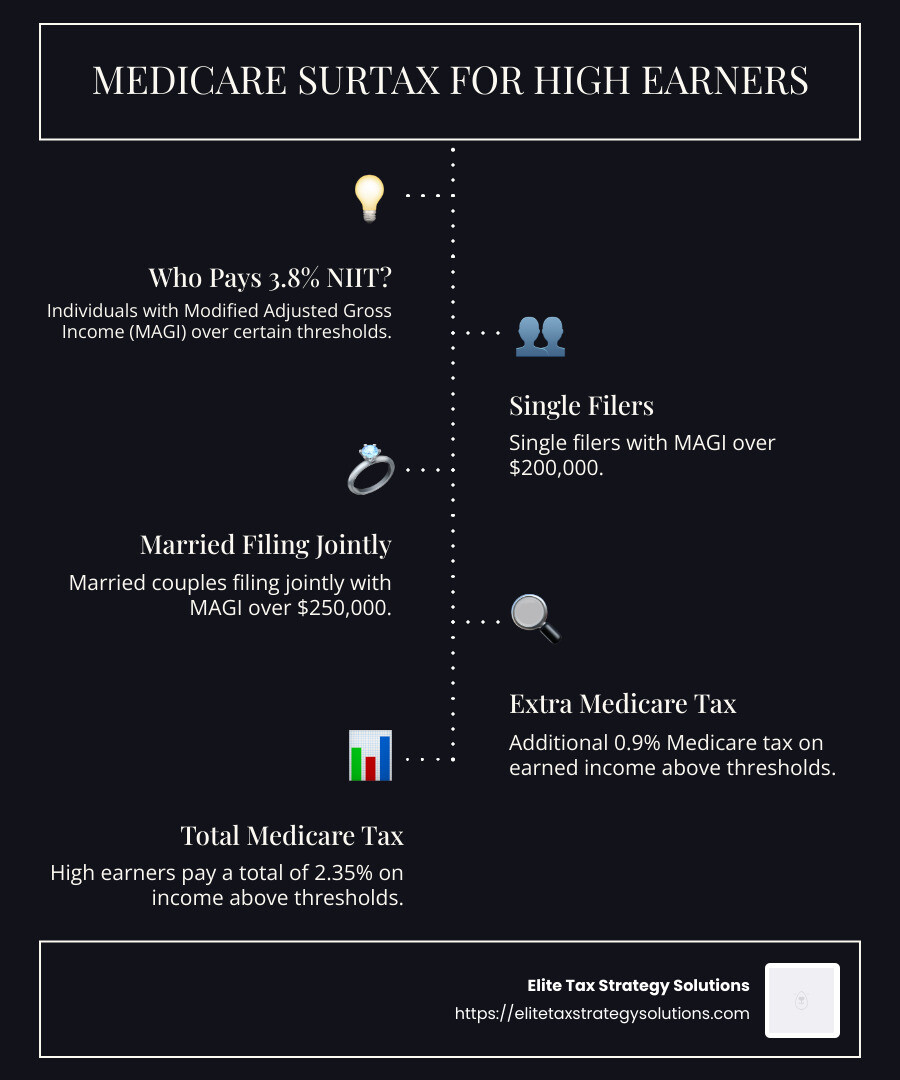

Who pays the 3.8% Medicare surtax?

The 3.8% Medicare surtax, also known as the Net Investment Income Tax, applies to individuals, estates, and trusts with income above certain thresholds. Specifically, it affects:

- Single filers with a Modified Adjusted Gross Income (MAGI) over $200,000.

- Married couples filing jointly with a MAGI over $250,000.

- Married individuals filing separately with a MAGI over $125,000.

The surtax is applied to the lesser of your net investment income or the excess of your MAGI over the applicable threshold.

Do high income earners pay more for Medicare tax?

Yes, high-income earners do pay more for Medicare tax. In addition to the standard 1.45% Medicare tax on all earned income, individuals with earnings above specific thresholds are subject to an additional 0.9% Medicare tax on the excess income. The thresholds are:

- $200,000 for single filers

- $250,000 for married couples filing jointly

- $125,000 for married individuals filing separately

This means that high earners will pay a total of 2.35% (1.45% + 0.9%) on income above these thresholds.

What is the Medicare surcharge for high income earners?

The Medicare surcharge for high-income earners consists of two parts:

- Additional Medicare Tax: A 0.9% tax on earned income above the thresholds mentioned above.

- Net Investment Income Tax (NIIT): A 3.8% tax on the lesser of your net investment income or the excess of your MAGI over the applicable threshold.

These surtaxes were introduced under the Affordable Care Act to help fund Medicare and are specific to high-income individuals. This means if you have significant investment income or your earnings exceed the thresholds, you will incur these additional taxes.

By understanding these rules, you can better manage your finances and plan for the extra Medicare tax. Stay tuned for more insights on how to steer these taxes effectively.

Conclusion

Understanding the extra Medicare tax for high earners is crucial for effective tax planning. High-income earners face additional taxes due to the Affordable Care Act, which includes a 0.9% tax on earned income above certain thresholds and a 3.8% Net Investment Income Tax (NIIT).

Proactive Tax Planning

Proactive tax planning can help minimize the impact of these additional taxes. Here are some strategies to consider:

- Income Management: Adjusting the timing of income and deductions can help manage your Modified Adjusted Gross Income (MAGI) to stay below the thresholds.

- Investment Strategies: Consider tax-efficient investments that generate less taxable income. For example, municipal bonds are generally exempt from federal taxes and the NIIT.

- Roth IRA Conversions: Converting traditional IRAs to Roth IRAs can help manage future taxable income since Roth IRA distributions are tax-free.

At Elite Tax Strategy Solutions, we specialize in helping high-income earners steer the complexities of tax regulations. Our custom tax-saving strategies are designed to optimize your financial outcomes and ensure compliance.

By integrating tax planning with your broader financial goals, you can better manage your tax liabilities and achieve long-term financial stability. Contact us to learn more about how we can help you steer the extra Medicare tax and other tax challenges.

Stay informed, plan ahead, and let us guide you through the maze of tax regulations.

For more details on how we can assist you, visit our Innovative Tax Planning page.