Understanding Your Tax Obligations as an Employee

Employee tax compliance refers to meeting all federal, state, and local tax obligations as a worker. This includes proper filing, accurate reporting, and timely payment of taxes.

Here’s what employee tax compliance involves:

| Compliance Type | What It Means | Key Requirements |

|---|---|---|

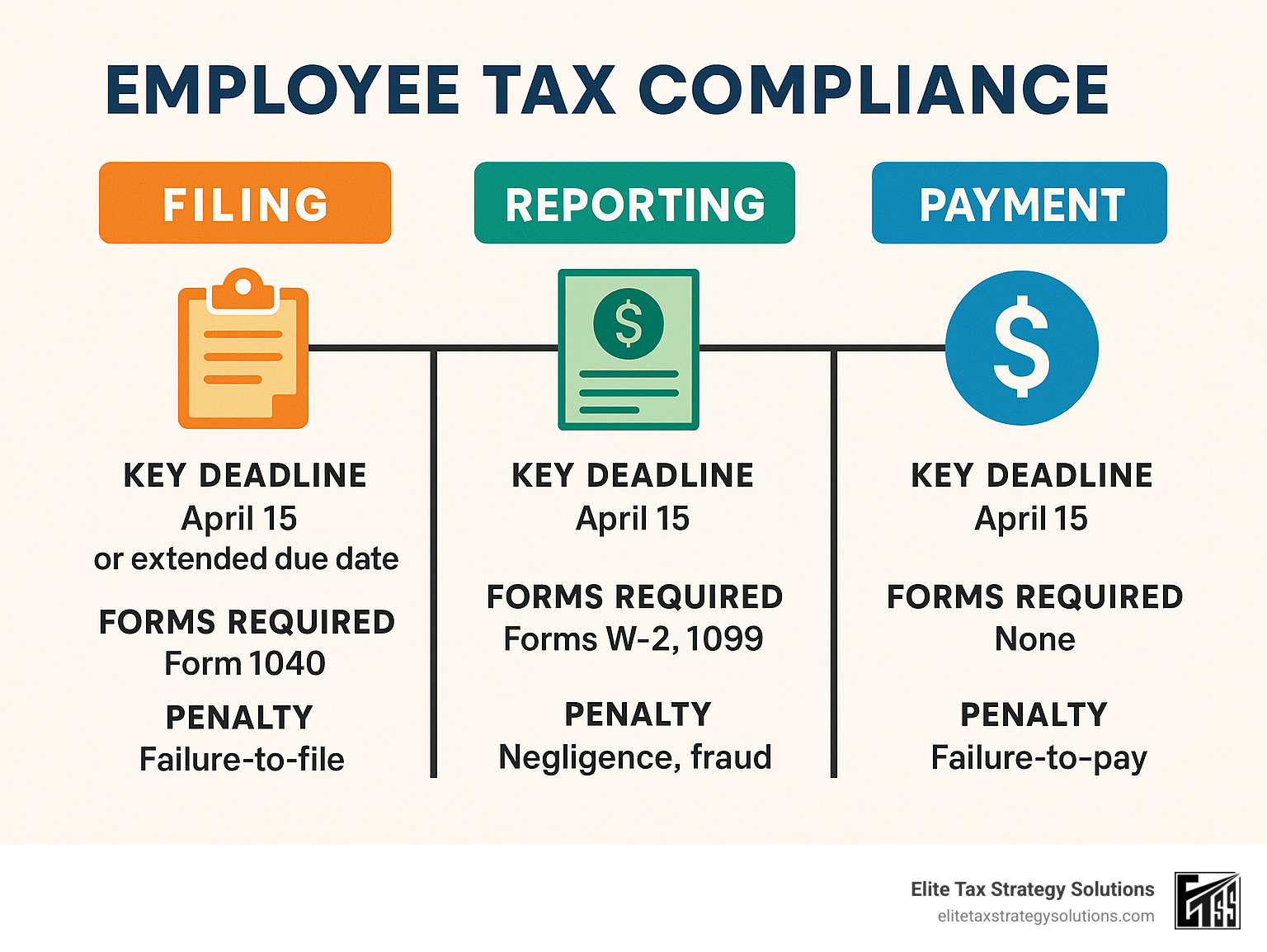

| Filing Compliance | Submitting returns on time | File by April deadline or request extension |

| Reporting Compliance | Declaring all income accurately | Include all income sources on return |

| Payment Compliance | Paying taxes when due | Pay through withholding or estimated payments |

Employee tax compliance is critical because it:

– Funds essential government programs and services

– Helps you avoid penalties, interest, and potential legal issues

– Maintains your professional reputation

– Is required by federal regulations (especially for federal employees)

Many employees find tax compliance confusing and stressful. According to research, common challenges include understanding withholding requirements, tracking multiple income sources, and keeping up with changing tax laws.

The good news? Tax compliance doesn’t have to be a headache. With proper knowledge and organization, you can confidently meet your obligations while minimizing stress.

I’m David Fritch, a CPA with over 40 years of experience helping individuals steer employee tax compliance requirements through my work at Elite Tax Strategy Solutions, where we specialize in providing clear guidance on complex tax matters.

Simple guide to employee tax compliance:

– multi state payroll tax compliance

– irs tax compliance

– tax compliance audit

Employee Tax Compliance Explained

Employee tax compliance is like a three-legged stool – it stands firmly on filing returns on time, accurately reporting all income, and paying the right amount of tax when due. If any one of these legs weakens, your entire tax situation could topple over!

Filing compliance simply means getting your tax returns in by the deadlines (usually April 15th for most of us). Reporting compliance goes beyond just your regular paycheck – it includes that side hustle money, rental income from your beach condo, or those investment dividends that trickle in throughout the year. Payment compliance ensures you’re paying the correct amount, typically through your employer’s withholding or through estimated tax payments if you have additional income.

The tax system might seem complicated, but understanding a few basics makes it much clearer:

Your paycheck includes FICA taxes – that’s 6.2% for Social Security (but only on wages up to $176,100 in 2025) and 1.45% for Medicare (on all your earnings). Your employer matches these exact amounts. If you’re earning the big bucks (over $200,000), you’ll chip in an extra 0.9% Medicare tax on those higher earnings.

Your Federal Income Tax uses marginal tax rates, which means different portions of your income get taxed at different rates, from 10% up to 37%. It’s like filling buckets – each bucket (tax bracket) gets filled at its own rate before overflowing to the next.

While FUTA (Federal Unemployment Tax Act) is mainly your employer’s headache (they pay 6% on your first $7,000 in wages, often reduced to 0.6% with state credits), it’s part of the overall employment tax structure that affects your workplace.

Don’t forget about state and local taxes – these vary dramatically depending on where you live and work, covering everything from income taxes to unemployment insurance.

Why Employee Tax Compliance Matters

Being tax compliant isn’t just about avoiding trouble – it’s about contributing to our shared society.

Your FICA taxes directly fund Social Security benefits for retirees and Medicare coverage for older Americans. Your income taxes support everything from our military to local schools, highways, and emergency services. Without these contributions, these essential services simply wouldn’t exist.

For those working in federal positions, employee tax compliance carries extra weight. Under Regulation 5 CFR § 2635.809, federal employees must “satisfy in good faith their obligations as citizens, including all just financial obligations, especially those such as Federal, State, and local taxes that are imposed by law.” It’s considered a fundamental ethical standard for public service.

The consequences of slipping up can be painful. The IRS can charge penalties starting at 0.5% monthly for unpaid taxes, plus interest that compounds daily. Employers who miss payroll tax deposits by more than 15 days might face penalties of 10% of the amount owed. In serious cases of deliberate non-compliance, criminal charges are possible.

As an IRS auditor once told me, “We’re not out to get people who make honest mistakes. We just expect everyone to make a good-faith effort to meet their tax obligations.”

Key Components of Employee Tax Compliance

The cornerstone of employee tax compliance is proper withholding. Your employer withholds taxes from each paycheck based on your Form W-4. Getting this form right is crucial – it determines whether you’ll be smiling at tax time or scrambling to find extra money.

If you’re earning significant income beyond your regular job – maybe from freelancing or rental property – you’ll likely need to make estimated tax payments quarterly. These payments help you stay current on taxes for income that doesn’t have automatic withholding.

There’s a hidden benefit in the system too – employer matching contributions. For every dollar you contribute to Social Security and Medicare taxes, your employer kicks in the same amount. This effectively doubles the funding without doubling your personal tax burden.

The Social Security wage base ($176,100 in 2025) puts a cap on how much of your income gets taxed for Social Security. Once you hit this threshold in a year, you stop paying Social Security tax on additional earnings. Medicare tax, however, applies to all your wages with no cap, plus that additional 0.9% for higher earners.

Employers rely on IRS Publication 15-T for guidance on calculating the correct withholding amounts from your paycheck. This document gets updated regularly to reflect current tax laws and rates.

For federal employees, Regulation 5 CFR § 2635.809 emphasizes that tax compliance isn’t just a legal requirement but an ethical obligation for those serving the public.

Understanding these fundamentals helps make employee tax compliance less mysterious and more manageable. With some basic knowledge and organization, you can steer the system confidently and avoid unnecessary headaches when tax season rolls around.

Responsibilities, Laws, Forms & Deadlines

Navigating the maze of employee tax compliance isn’t exactly anyone’s idea of a good time, but understanding the basics can save you a world of headaches down the road. Let’s break it down into manageable pieces.

The IRS provides a roadmap through publications like Circular E (Publication 15), which spells out everything employers need to know about withholding and reporting taxes. Think of it as the tax equivalent of an owner’s manual – not the most thrilling read, but essential for keeping things running smoothly.

Beyond the IRS guidelines, several laws shape your tax responsibilities. The Fair Labor Standards Act (FLSA) doesn’t just protect your right to fair wages and overtime; it also affects how those wages get taxed. When you earn time-and-a-half for working beyond 40 hours, that extra income is subject to withholding just like your regular pay.

State tax requirements can feel like visiting different countries – because they practically are! While Floridians, Texans, and Nevadans enjoy life without state income tax withholding, residents in states like California and New York steer complex progressive tax structures. And if you work remotely or cross state lines for your job, you’re in for an extra layer of complexity.

Then there are local taxes – the often-forgotten cousins in the tax family. Many cities and counties take their own slice of your paycheck, requiring separate withholding and reporting. It’s like paying rent to both your landlord and the building owner!

The Affordable Care Act added its own tax wrinkles, including potential credits for marketplace insurance and penalties for inadequate coverage. And while the Equal Pay Act’s primary goal is preventing wage discrimination, it indirectly supports tax compliance by ensuring proper wage reporting regardless of gender.

Employee Tax Compliance Duties at a Glance

As an employee, your tax responsibilities boil down to a handful of crucial tasks. First and foremost is completing your Form W-4 correctly. This little form packs a big punch – it’s what tells your employer how much tax to withhold from each paycheck. Since its 2020 makeover, it’s become more straightforward, asking for specific dollar amounts rather than the old “allowances” system that confused practically everyone.

Life changes? Update your W-4! Got married? Had a baby? Spouse started a new job? These events should trigger a W-4 review. As my colleague David likes to say, “Your W-4 should change when your life changes.”

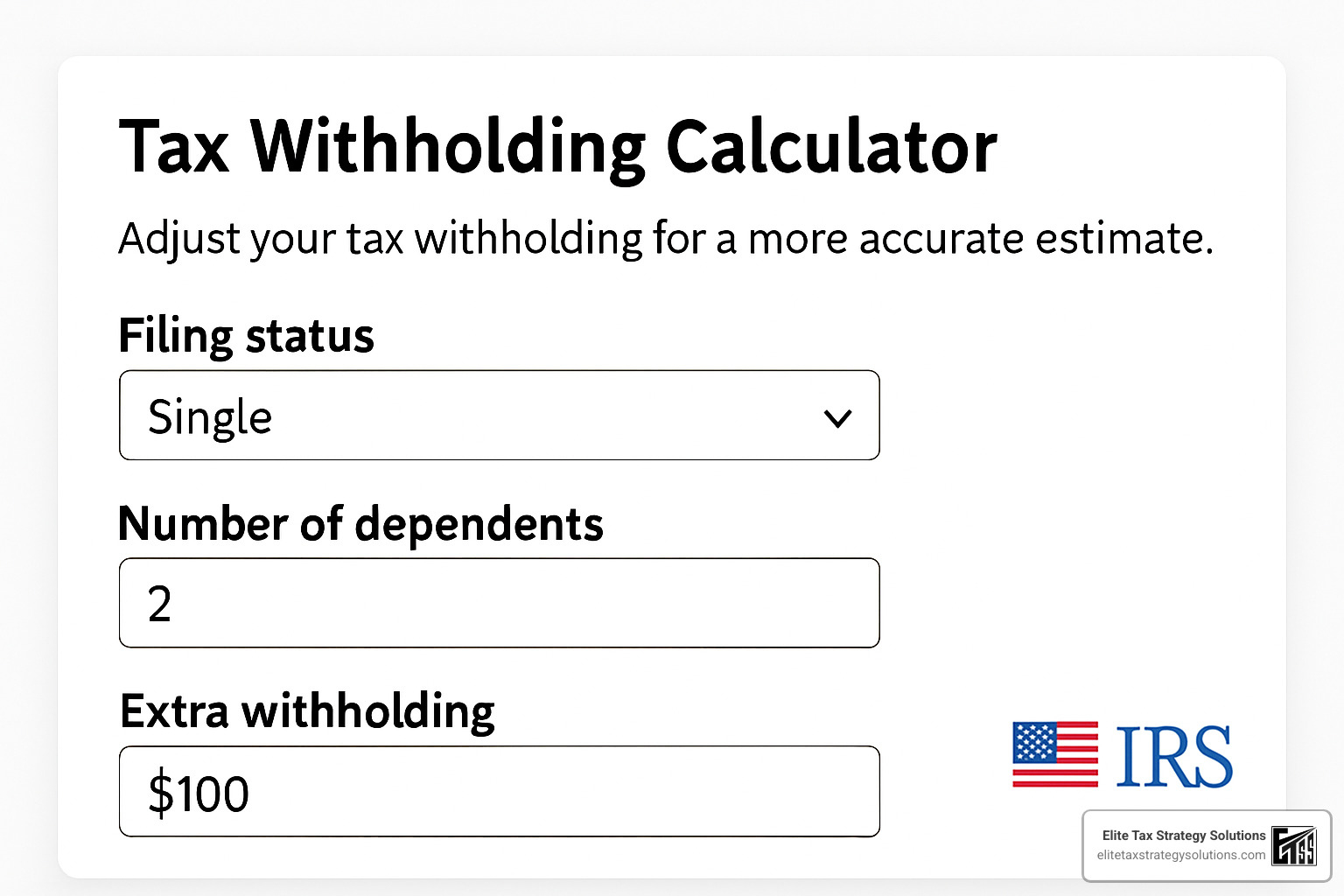

It’s also smart to periodically check your withholding using the IRS Tax Withholding Estimator. Ideally, you want your withholding to be like Goldilocks’ porridge – just right. Too little withholding and you might face an unexpected tax bill (plus possible penalties). Too much and you’re essentially giving the government an interest-free loan until refund time.

Of course, filing your return by the April deadline (typically the 15th) is non-negotiable. Need more time? You can request an extension to October, but remember – that only extends your filing deadline, not your payment deadline. The IRS still expects its money by April!

And those receipts and tax documents cluttering your desk? Keep them for at least three years. They’re your protection if the IRS ever has questions about your return.

Employer Oversight for Employee Tax Compliance

Employers shoulder significant responsibilities in the employee tax compliance ecosystem. They’re the frontline workers in our tax system, calculating and withholding the correct amounts from each paycheck – federal, state, and local income taxes, plus Social Security and Medicare contributions.

These withheld funds must be deposited through the Electronic Federal Tax Payment System (EFTPS) according to a schedule that depends on the employer’s tax liability. Some employers deposit monthly, others semi-weekly – missing these deadlines is one of the quickest ways to land in hot water with the IRS.

By January 31st each year, employers must provide each employee with Form W-2, documenting the previous year’s wages and withholdings. It’s like your annual tax report card – and the IRS gets a copy too.

The compliance responsibilities extend beyond taxes to employment verification. Form I-9 confirms that employees are legally authorized to work in the U.S., ensuring that only eligible workers are on payroll and participating in the tax system.

One of the trickiest areas is worker classification. Misclassifying employees as independent contractors can create serious tax headaches for everyone involved. In certain cases, Section 530 relief may protect employers who had reasonable grounds for classification decisions, but it’s always better to get it right from the start.

For deeper insights into employer tax responsibilities, check out our comprehensive guide to Tax Compliance for Companies.

Must-Have Forms & Documentation

The paperwork of employee tax compliance may not be exciting, but it’s essential. Form W-2 is the star of the show – your employer must provide this record of your annual wages and withholdings by January 31st. It’s the cornerstone document for filing your tax return.

The Employee’s Withholding Certificate (Form W-4) is equally important, telling your employer exactly how much tax to withhold. I always tell clients that your W-4 deserves a review whenever you experience a significant life or financial change.

Form I-9 verifies your eligibility to work in the United States – not directly tax-related, but a crucial part of legitimate employment documentation.

If you do freelance or contract work, expect Form 1099-NEC instead of (or in addition to) a W-2. This form reports non-employee compensation of $600 or more, and you’re responsible for paying self-employment tax on this income.

On the employer side, Forms 941 (quarterly), 940 (annual), and sometimes 944 (for small employers) report wages paid and taxes withheld to the IRS.

Accurate Social Security numbers are the glue that holds the system together. Even a single digit error can cause mismatches in IRS systems, potentially triggering notices or delaying refunds.

Critical Filing & Deposit Deadlines

When it comes to employee tax compliance, timing is everything. Missing deadlines can lead to penalties that add up quickly.

Employers file Form 941 quarterly to report wages and taxes, with deadlines falling on the last day of the month after each quarter ends (April 30, July 31, October 31, and January 31). Form 940, the annual unemployment tax return, is due by January 31 following the tax year.

Tax deposit schedules follow either monthly or semiweekly patterns based on the employer’s lookback period. Monthly depositors must submit taxes by the 15th of the following month, while semiweekly depositors follow a Wednesday/Friday schedule depending on when paydays fall.

State deadlines add another layer of complexity, with each state setting its own filing and deposit schedules. It’s like juggling while riding a unicycle – challenging but manageable with the right system.

For high earners, there’s the Additional Medicare Tax of 0.9% on wages exceeding $200,000. Employers must begin withholding this additional amount once an employee crosses that threshold in a calendar year.

As one of our clients, a payroll manager with 15 years of experience, shared: “Setting up automatic calendar reminders for all tax deadlines was a game-changer for our compliance efforts. We haven’t missed a deadline since implementing this simple system.”

The key to staying on top of these deadlines is organization and planning. At Elite Tax Strategy Solutions, we help clients build systems that make compliance nearly automatic, freeing them to focus on what they do best – running their businesses and living their lives.

Pitfalls, Penalties, Relief Options & Tech Tools

Navigating employee tax compliance is a bit like walking through a minefield – one wrong step and boom! Let’s explore the common pitfalls that can trip you up, what happens if you stumble, and how to recover your footing.

One of the biggest headaches in the tax world is worker misclassification. When you’re labeled as an independent contractor but should be an employee (or vice versa), it creates a tax mess for everyone involved. If you’re incorrectly classified as a contractor, you’re suddenly on the hook for the full 15.3% of self-employment taxes instead of sharing that burden with your employer. The IRS doesn’t take this lightly – they look at who controls what you do, who pays for your expenses, and the nature of your relationship with the company.

Late tax deposits are another common pitfall that can quickly drain your wallet. Miss a deposit deadline by more than 15 days, and you’re looking at a 10% penalty right off the bat. As one of my clients painfully finded, “Those penalties don’t just sting – they bite hard and hold on!”

Even simple math errors can create big problems. A transposed digit here or a decimal point in the wrong place there might seem minor, but they can trigger correspondence audits and delays in processing your return. I always tell my clients: “Double-check your math, then have someone else check it again.”

Under-withholding throughout the year feels great in your paycheck but feels terrible at tax time. The IRS expects you to pay as you earn, not in one lump sum in April. This is why proper W-4 completion is so crucial – it’s your roadmap to avoiding a surprise tax bill.

The Trust Fund Recovery Penalty is particularly nasty. If you’re responsible for a business’s finances and fail to remit employee withholding taxes, the IRS can come after your personal assets. I’ve seen this penalty devastate business owners who thought they could “borrow” from withholding taxes to cover cash flow problems.

Standard failure-to-deposit penalties start small but grow quickly: 2% for deposits 1-5 days late, 5% for 6-15 days late, and a whopping 10% for more than 15 days late. After the IRS sends you a notice, that jumps to 15%!

Can’t pay your tax bill? Don’t panic – you have options. Installment agreements let you pay over time, though interest and penalties continue to accrue. An Offer in Compromise might allow you to settle for less than you owe if you meet specific financial criteria. Neither is ideal, but both are better than ignoring the problem.

Modern payroll software with ISO and SOC certifications can dramatically reduce these headaches through automation. As one client told me after switching to an automated system, “It’s like having a tax compliance expert working for me 24/7!”

Common Mistakes that Trigger Audits

Nothing makes my heart sink faster than telling a client they’re being audited. Here are the slip-ups that tend to put you in the IRS’s crosshairs:

Using an incorrect Social Security number on tax documents is like waving a red flag at the IRS. This often happens due to innocent typos, but from the IRS perspective, it looks suspicious – like you might be trying to hide income.

Ignoring state tax nexus issues has become increasingly problematic with remote work becoming common. Working from your beachfront condo in Florida while employed by a New York company creates complex tax obligations in both states. Miss this, and you might find yourself facing state tax audits.

Overtime miscalculation leads to incorrect wage reporting and tax withholding. Overtime must be calculated at 1.5 times your regular rate for hours over 40 in a workweek – and yes, this affects your tax withholding too.

Missing signatures or incomplete forms might seem trivial, but they can delay processing and raise suspicions. I always remind clients: “A tax return without a signature is like a check without a signature – it’s not valid!”

After helping dozens of clients through audits, I can tell you that most IRS examinations stem from these types of preventable errors rather than deliberate tax evasion. A little attention to detail goes a long way toward keeping the tax authorities out of your life.

Consequences & How to Mitigate Them

The fallout from tax non-compliance can range from annoying to life-altering:

Interest charges accrue on unpaid taxes from the due date until you pay in full, regardless of extensions or payment plans. The IRS adjusts its interest rate quarterly, and it compounds daily – meaning your tax debt can grow surprisingly fast.

Civil penalties vary based on what went wrong. The failure-to-file penalty (5% of unpaid taxes per month, up to 25%) is steeper than the failure-to-pay penalty (0.5% per month, up to 25%) – which is why I always tell clients to file on time even if they can’t pay right away. Accuracy-related penalties add another 20% to your underpayment.

Criminal liability enters the picture in cases of willful evasion, fraud, or failure to file. These situations can lead to substantial fines and even jail time. While rare, these cases serve as a sobering reminder of how seriously the government takes tax compliance.

Section 1203 of the IRS Restructuring and Reform Act requires the IRS to terminate its own employees who willfully fail to file their returns or understate their tax liability. If they’re that tough on their own people, imagine how they treat everyone else!

If you find yourself unable to pay, follow these steps for an installment plan: file your return on time regardless of ability to pay, pay as much as possible upfront to reduce penalties, apply online through the IRS Failure-to-Deposit Penalty page, and stick to your payment schedule religiously.

A doctor client of mine faced a shocking tax bill after her most profitable year ever. She shared, “I was terrified when I saw how much I owed. Elite Tax Strategy Solutions helped me set up an installment plan that I could manage without destroying my finances. The relief was immediate.”

Leveraging Technology for Seamless Compliance

Technology has transformed employee tax compliance from a nightmare into something much more manageable:

Automated withholding calculators ensure the correct amount comes out of each paycheck based on your W-4 information and current tax rates. Many systems update these calculations automatically when tax laws change, saving you from unpleasant surprises at tax time.

E-filing provides built-in error checks, faster processing, and confirmation that your return was received. The IRS typically issues refunds within 21 days for e-filed returns, compared to 6-8 weeks for paper returns. That’s three times faster!

The Electronic Federal Tax Payment System (EFTPS) lets you schedule tax payments in advance and sends helpful reminders about upcoming due dates. This system is mandatory for most business tax deposits and available for individual estimated tax payments as well.

AI-powered expense tracking tools can automatically categorize and document deductible expenses throughout the year. No more shoebox full of receipts! These tools often integrate directly with tax preparation software, making tax season much less stressful.

Secure cloud storage provides safe, accessible record-keeping for all your tax documents. With proper encryption and access controls, cloud storage can be more secure than physical document storage while giving you access from anywhere with an internet connection.

For more information on how technology can support your tax compliance efforts, visit our page on Tax Support and Compliance.

As one client put it after we helped her implement these tech solutions: “I used to spend weekends sorting through tax paperwork. Now my system does the heavy lifting, and I spend my weekends with my family instead.”

Frequently Asked Questions about Employee Tax Compliance

Do I still have to file if I’m getting a refund?

Absolutely! Even when Uncle Sam owes you money, you still need to file your tax return by the April deadline. This requirement isn’t based on whether you’re owed money or owe money—it’s about your income level and filing status.

There are several important reasons to file on time even when a refund is coming your way:

First, there’s a three-year statute of limitations for claiming refunds. Wait too long, and that money becomes a permanent donation to the government. Second, the sooner you file, the sooner you’ll get your refund in hand. And third, certain valuable tax credits require timely filing to qualify.

I recently spoke with an IRS representative who put it plainly: “There is no distinction between a refund and a balance-due return; you must file on or before the deadline.”

What happens if I can’t pay my taxes on time?

Finding yourself short on cash when taxes are due can be stressful, but don’t let that stop you from filing! Always file your return on time, even if you can’t pay the full amount. This simple step will save you from the steep failure-to-file penalty of 5% per month, which is ten times higher than the failure-to-pay penalty of 0.5% per month.

The good news is the IRS offers several flexible payment options:

If you owe less than $50,000 and can pay within 72 months, the Online Payment Agreement is your fastest solution. For larger amounts or longer terms, a formal Installment Agreement might work better. Those facing genuine financial hardship may qualify for an Offer in Compromise to settle for less than the full amount. And if you’re truly unable to pay anything, you might qualify for a Temporary Delay while you get back on your feet.

Pay what you can by the deadline to minimize the penalties and interest that will continue accruing until your balance is paid in full.

How often should I review my Form W-4?

Think of your W-4 as your tax forecast—it needs regular updates to stay accurate. I recommend reviewing your withholding at least once annually, ideally in January when tax laws often change.

Beyond that annual check-up, certain life events should trigger an immediate W-4 review:

Major life changes like marriage, divorce, or welcoming a new child can dramatically shift your tax situation. Financial milestones such as buying a home, starting a side business, or retiring also warrant a fresh look at your withholding. Even significant income changes or shifts in your deduction strategy can throw your withholding out of balance.

The IRS Tax Withholding Estimator is a fantastic free tool to check if you’re on track. Taking fifteen minutes to update your W-4 can save you from an unwelcome surprise at tax time.

One of my clients learned this lesson the hard way: “I forgot to update my W-4 after our wedding. By tax time, we owed over $3,000 because both of us were claiming tax benefits as if we were single filers. Now I review my withholding every January and after any major life change.”

Staying on top of your withholding is one of the simplest ways to maintain employee tax compliance throughout the year, rather than scrambling at tax time.

Conclusion

Employee tax compliance doesn’t have to be overwhelming. Like learning to ride a bike, what seems daunting at first becomes second nature with a little practice and the right guidance.

Throughout this guide, we’ve explored the three pillars that form the foundation of tax compliance: filing your returns on time, reporting all income accurately, and paying the correct amount when due. These aren’t just bureaucratic requirements – they’re the framework that helps you maintain financial clarity and peace of mind.

I’ve seen countless clients transform their approach to taxes from reactive panic to confident control. The secret isn’t complicated – it’s about embracing a proactive mindset. Review your withholding whenever your life circumstances change. Keep your records organized year-round (a simple digital folder system works wonders). Stay informed about tax law changes that might affect your situation. And leverage technology tools that can automate the tedious parts of compliance.

Year-round tax planning beats last-minute scrambling every time. Consider setting a quarterly “tax check-in” on your calendar – just 30 minutes every three months can help you spot potential issues before they become problems. One of my clients, a teacher who had always dreaded tax season, told me: “Now that I’ve broken tax compliance into smaller, regular check-ins, it feels manageable for the first time in my life.”

At Elite Tax Strategy Solutions, we believe tax compliance should empower rather than intimidate you. Our team in Jasper, Indiana and surrounding areas specializes in translating complex tax requirements into clear, actionable strategies custom to your specific situation. We’ve helped clients from all walks of life steer multi-state employment challenges, prepare confidently for audits, and optimize their tax positions through thoughtful planning.

Effective employee tax compliance isn’t just about avoiding penalties—it’s about taking control of your financial future through informed decisions and proactive management. It’s about sleeping well at night knowing your tax affairs are in order.

For personalized guidance on your tax compliance journey, visit our page on tax support and compliance. We’re here to help transform tax compliance from a source of stress to a foundation for financial confidence.