Comprehensive tax planning is your dynamic roadmap to achieve financial success. It aligns your tax strategies with your long-term financial goals, ensuring that every dollar works harder for you. Here’s a quick glance at what it entails:

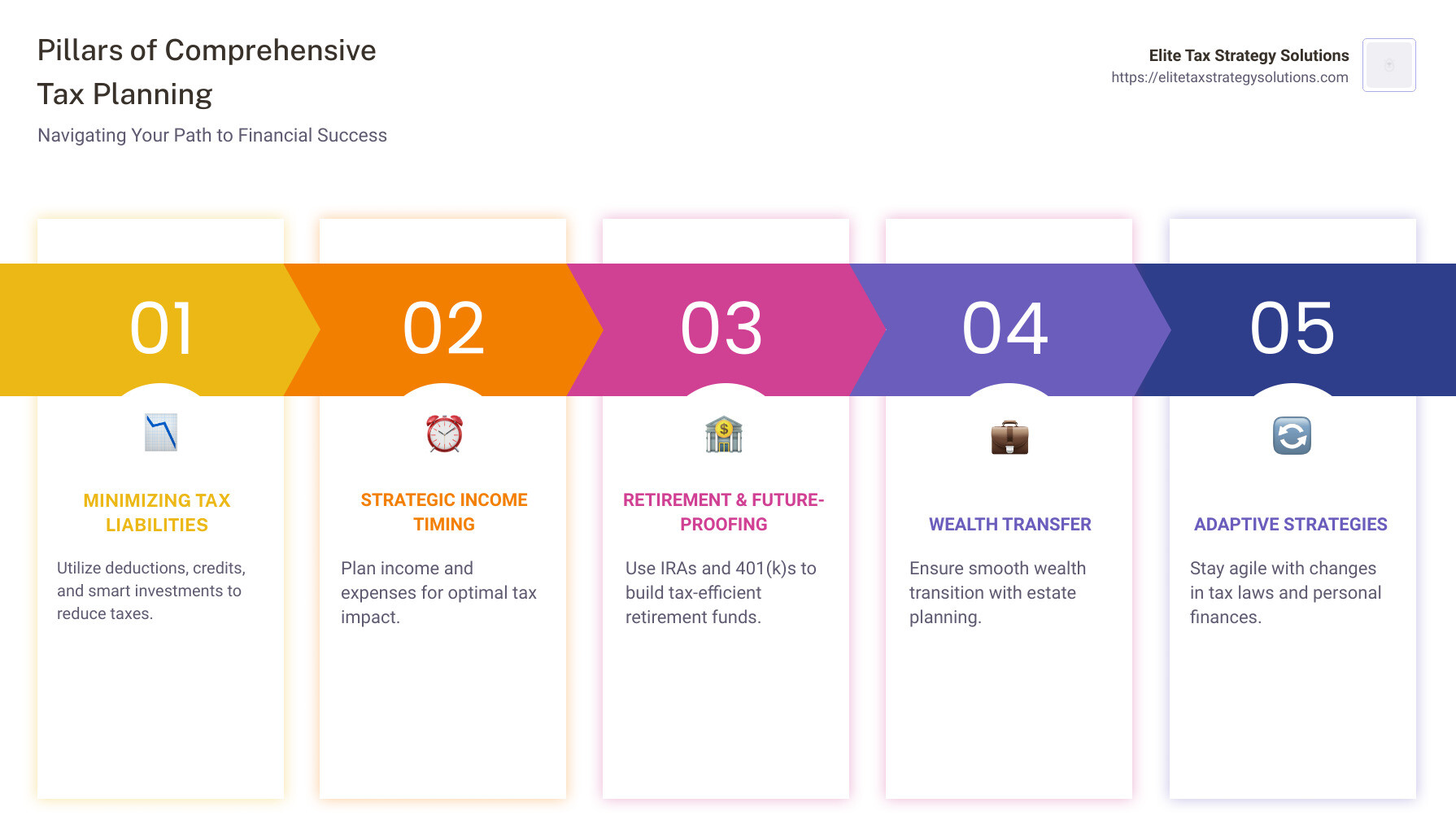

- Minimizing Tax Liabilities: Use deductions, credits, and smart investments to lower what you owe.

- Strategic Income Timing: Plan when to receive income and make purchases for optimal tax results.

- Retirement and Future-Proofing: Leverage IRAs, 401(k)s, and other accounts to shelter income and grow funds tax-efficiently.

- Wealth Transfer: Ensure a smooth transition of wealth with estate planning strategies.

- Adaptive Strategies: Stay agile with evolving tax laws and personal financial situations.

Now, let me introduce myself. I’m David Fritch, with over 40 years of experience in navigating the intricate world of taxes. My journey with comprehensive tax planning began at Fritch Law Office, followed by my tenure at Arthur Andersen, and has continued with my dedication to Elite Tax Strategy Solutions. Here, I guide high-income earners and small business owners to master their tax challenges with confidence.

Understanding Comprehensive Tax Planning

Comprehensive tax planning is more than just a yearly ritual. It’s a strategic approach to managing your finances to ensure you’re not overpaying taxes and that your money is working for you. Let’s break it down.

What is Tax Planning?

At its core, tax planning is about understanding your financial situation and making decisions that minimize your tax liability. This means paying the least amount of tax legally possible while maximizing your income and investments. It’s not just about filing your returns; it’s about strategic foresight.

The Importance of Being Tax-Efficient

Being tax-efficient means making financial decisions that consider their tax implications. For example, investing in a Roth IRA can be more tax-efficient than a traditional IRA, depending on your situation. The goal is to keep more of your earnings in your pocket.

A Key Component of Your Financial Strategy

Tax planning should be an integral part of your overall financial strategy. It’s not just about saving money today; it’s about planning for the future. Whether you’re saving for retirement, buying a home, or planning your estate, tax planning can help you reach those goals more effectively.

Consider This: If you’re planning to retire, contributing to a 401(k) or IRA can reduce your taxable income now while providing tax-deferred growth for the future. This strategy aligns with both your tax and retirement goals.

Adaptability is Crucial

Tax laws change, and so does your financial situation. Your tax plan should be flexible enough to adapt to these changes. Regularly reviewing and updating your strategy ensures you remain on track toward your financial goals.

The Role of Professional Expertise

While some individuals can handle basic tax strategies, complex situations often require professional help. Tax professionals can steer the complexities of the tax code and tailor strategies to your unique needs.

By integrating tax planning into your financial strategy, you can improve your financial well-being and work towards long-term success. Up next, we’ll dive into key strategies for comprehensive tax planning that you can start implementing today.

Key Strategies for Comprehensive Tax Planning

When it comes to comprehensive tax planning, there are five core strategies: deducting, deferring, dividing, disguising, and dodging. Let’s explore each one in simple terms.

Deducting

Tax deductions lower your taxable income. This means you pay taxes on a smaller amount. Common deductions include mortgage interest, student loan interest, and charitable donations. By maximizing these deductions, you can reduce your tax bill significantly.

Example: If you donate $5,000 to a charity, you can deduct that amount from your taxable income. If you’re in the 25% tax bracket, this could save you $1,250 in taxes.

Deferring

Deferring means postponing tax payments. You can do this by contributing to retirement accounts like a 401(k) or traditional IRA. These contributions reduce your taxable income now, and you pay taxes later when you withdraw the funds, ideally at a lower tax rate during retirement.

Consider This: Contributing $6,000 to a traditional IRA can reduce your taxable income by the same amount, potentially saving you hundreds in taxes today.

Dividing

Dividing involves spreading your income across different tax years or family members to reduce tax liability. This can be done through income splitting or by strategically timing income and expenses.

For example, if you expect a bonus, consider deferring it to the next tax year if it keeps you in a lower tax bracket this year.

Disguising

Disguising, in legal terms, means structuring your income to take advantage of lower tax rates. This could involve receiving income in the form of dividends or capital gains, which are often taxed at a lower rate than regular income.

Example: Long-term capital gains are typically taxed at 0%, 15%, or 20%, depending on your income. If you sell an asset held for over a year, you might pay less tax than on ordinary income.

Dodging

Dodging isn’t about avoiding taxes illegally; it’s about using legal means to minimize taxes. This includes utilizing tax credits, which directly reduce your tax bill. Unlike deductions, credits provide a dollar-for-dollar reduction.

Fact: A $1,000 tax credit reduces your tax bill by $1,000, while a $1,000 deduction only reduces taxable income.

By employing these strategies, you can ensure that your tax plan is both comprehensive and effective. Up next, we’ll look at how tax planning plays a crucial role in preparing for retirement.

Tax Planning for Retirement

Retirement planning is a crucial part of comprehensive tax planning. It’s about using tax-efficient strategies to maximize your savings and minimize taxes when you retire. Let’s dive into the key tools: retirement plans, IRAs, and 401(k)s.

Retirement Plans

Retirement plans are like a financial safety net for your golden years. They offer tax advantages that can help you save more money over time.

Types of Plans:

-

Traditional IRAs: Contributions may be tax-deductible, reducing your taxable income now. However, you’ll pay taxes when you withdraw the money in retirement.

-

Roth IRAs: Contributions are made with after-tax dollars, so they don’t reduce your taxable income now. The big benefit? Withdrawals in retirement are tax-free.

-

401(k) Plans: Offered by employers, these allow you to save a portion of your paycheck before taxes. Like traditional IRAs, you’ll pay taxes on withdrawals in retirement.

How They Work

Traditional IRAs and 401(k)s allow you to defer taxes. This means you pay less in taxes now and more when you withdraw the funds in retirement, ideally when you’re in a lower tax bracket.

Roth IRAs, on the other hand, provide tax-free growth. You pay taxes upfront, but your money grows tax-free, and you don’t pay taxes on withdrawals.

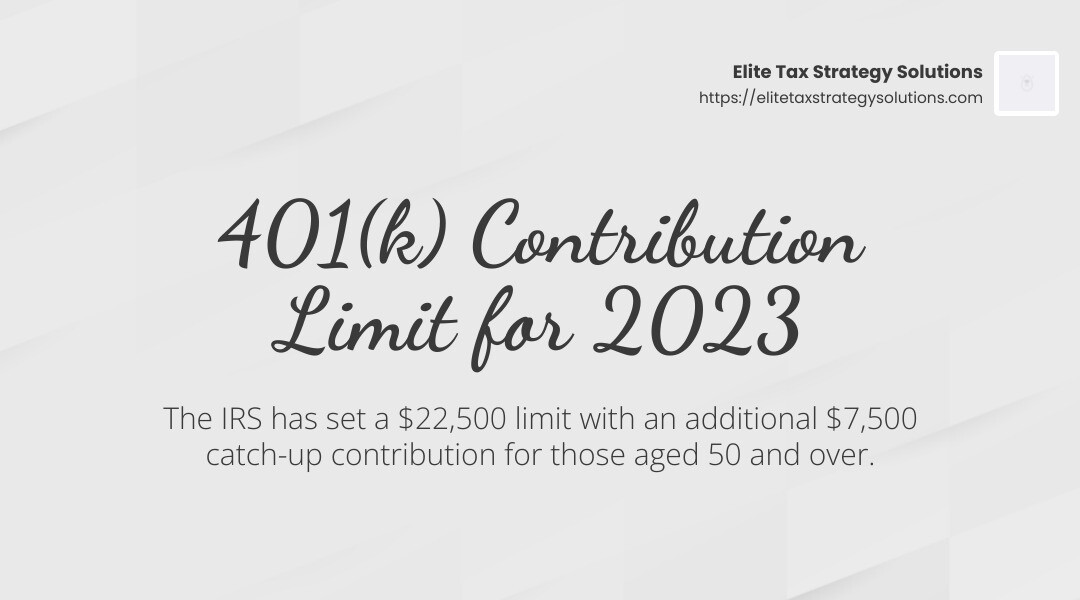

Stat: According to the IRS, the contribution limit for 401(k) plans in 2023 is $22,500, with an additional $7,500 catch-up contribution for those aged 50 and over.

Choosing the Right Plan

Choosing between these options depends on your current tax situation and future expectations.

-

If you expect to be in a higher tax bracket during retirement, a Roth IRA might be beneficial because withdrawals are tax-free.

-

If you’re currently in a high tax bracket and expect to be in a lower one in retirement, a traditional IRA or 401(k) could save you more in taxes over time.

Strategies for Maximizing Benefits

-

Max Out Contributions: Contribute the maximum allowed to take full advantage of tax benefits.

-

Employer Match: If your employer offers matching contributions to your 401(k), contribute at least enough to get the full match. It’s essentially free money.

-

Diversify Accounts: Consider having both traditional and Roth accounts. This gives you flexibility to manage your tax liability in retirement.

Tip: Regularly review your retirement plan with a tax advisor to ensure you’re on track to meet your goals and make adjustments as needed.

By understanding and utilizing these retirement planning tools, you can create a tax-efficient strategy that supports your financial goals. Next, let’s explore how tax-smart investing can further improve your retirement savings.

Tax-Efficient Investments

Investing wisely can transform your financial future. But to make the most of your investments, it’s crucial to consider the tax implications. Tax-efficient investments can help you keep more of your hard-earned money.

Tax-Smart Investing

Tax-smart investing means choosing investments that minimize your tax burden. Here are some strategies to consider:

-

Invest in Municipal Bonds: These bonds are often tax-free at the federal level and sometimes state and local levels if you live where the bond is issued. This makes them attractive to investors in high tax brackets.

-

Focus on Long-Term Gains: Holding investments for more than a year can reduce your tax rate on capital gains. The rates for long-term capital gains are generally lower than ordinary income tax rates.

-

Use Tax-Deferred Accounts: Accounts like 401(k)s and IRAs allow your investments to grow tax-deferred, meaning you won’t pay taxes on the gains until you withdraw the money.

Tax-Loss Harvesting

Tax-loss harvesting is a strategy to offset gains with losses. Here’s how it works:

-

Sell Underperforming Investments: By selling investments that have lost value, you can use those losses to offset gains from other investments, reducing your overall tax liability.

-

Avoid Wash Sales: If you sell a security at a loss and then buy the same or a substantially identical one within 30 days, it’s considered a wash sale, and you can’t claim the loss for tax purposes.

Example: Suppose you have $10,000 in long-term capital gains and $10,000 in long-term capital losses. These can offset each other, resulting in no tax liability on the gains.

Understanding Capital Gains

Capital gains are the profits from selling an asset. They can be short-term or long-term:

-

Short-Term Capital Gains: These are taxed at your ordinary income tax rate since the asset was held for less than a year.

-

Long-Term Capital Gains: These enjoy lower tax rates of 0%, 15%, or 20%, depending on your income. For single filers, gains up to $47,025 are taxed at 0% in 2024.

Strategies to Optimize Capital Gains

-

Hold Investments for Over a Year: This qualifies you for the lower long-term capital gains tax rate.

-

Plan Sales Strategically: Time your sales to stay within a lower tax bracket. For instance, spreading sales over multiple years can help manage your tax rate.

-

Use Tax-Advantaged Accounts: Place investments that generate high taxable income, like bonds, in tax-advantaged accounts to defer taxes.

By incorporating these tax-smart investing strategies, you can improve your financial portfolio while minimizing taxes. Next, let’s address some common questions about comprehensive tax planning.

Frequently Asked Questions about Comprehensive Tax Planning

What are the 5 pillars of tax planning?

Tax planning is built on five key pillars: deducting, deferring, dividing, disguising, and dodging.

-

Deducting: This involves identifying eligible expenses that can be subtracted from your taxable income. Common deductions include mortgage interest, charitable donations, and certain medical expenses. The goal is to lower your taxable income and thus reduce your tax liability.

-

Deferring: This strategy postpones tax payments to a future date. By deferring income or gains, you can potentially pay taxes at a lower rate. For example, contributing to a 401(k) or an IRA allows your investments to grow tax-deferred until retirement.

-

Dividing: This involves spreading income or gains over multiple tax periods or among family members to take advantage of lower tax brackets. For instance, gifting assets to family members in lower tax brackets can reduce the overall family tax burden.

-

Disguising: This refers to structuring transactions in a way that they appear differently for tax purposes. It’s crucial to follow legal guidelines to avoid crossing into illegal territory. For example, a business might lease equipment instead of purchasing it outright to spread the expense over several years.

-

Dodging: Legally minimizing taxes through various exemptions and credits. Tax credits, like those for energy-efficient home improvements or education expenses, directly reduce your tax bill and can be more beneficial than deductions.

Is tax planning worth it?

Absolutely! Comprehensive tax planning is a powerful tool for reaching your financial goals. By strategically managing your taxes, you can achieve significant tax savings.

Consider this: effective tax planning can reduce your tax liability, allowing you to allocate more funds toward your financial aspirations, whether that’s buying a home, saving for education, or ensuring a comfortable retirement.

In short, tax planning is an investment in your financial future. It helps you keep more of what you earn, paving the way for greater financial security.

What is tax planning in simple terms?

Tax planning is like a financial roadmap. It involves arranging your finances in a way that maximizes tax benefits while minimizing tax liabilities.

Think of it as a strategy to legally pay the least amount of taxes possible. By understanding your tax bracket, utilizing deductions and credits, and timing your income and expenses wisely, you can reduce your overall tax bill.

Tax planning is about making informed financial decisions throughout the year to ensure you’re not overpaying come tax time. It’s about being proactive, not just reactive, with your finances.

Next, let’s dive into how tax planning can specifically aid in retirement savings.

Conclusion

Comprehensive tax planning is not just about saving money; it’s about setting the foundation for long-term financial success. At Elite Tax Strategy Solutions, we believe that smart tax optimization can be a game-changer for high earners and small businesses. Our proactive approach means we don’t just react to tax season; we plan ahead to maximize tax savings and ensure financial stability.

Imagine having more funds available to invest in your business, save for retirement, or even take that dream vacation. That’s the power of effective tax planning. By aligning your tax strategy with your financial goals, you can pave the way for a more secure financial future.

Our team of experts is dedicated to navigating the complexities of the tax code for you. We offer personalized strategies that fit your unique financial situation. Whether it’s maximizing deductions, utilizing credits, or planning for retirement, we have the tools and knowledge to help you succeed.

Ready to take control of your financial future? Explore our custom tax planning services for small businesses here. Let’s work together to optimize your taxes and achieve your financial aspirations.