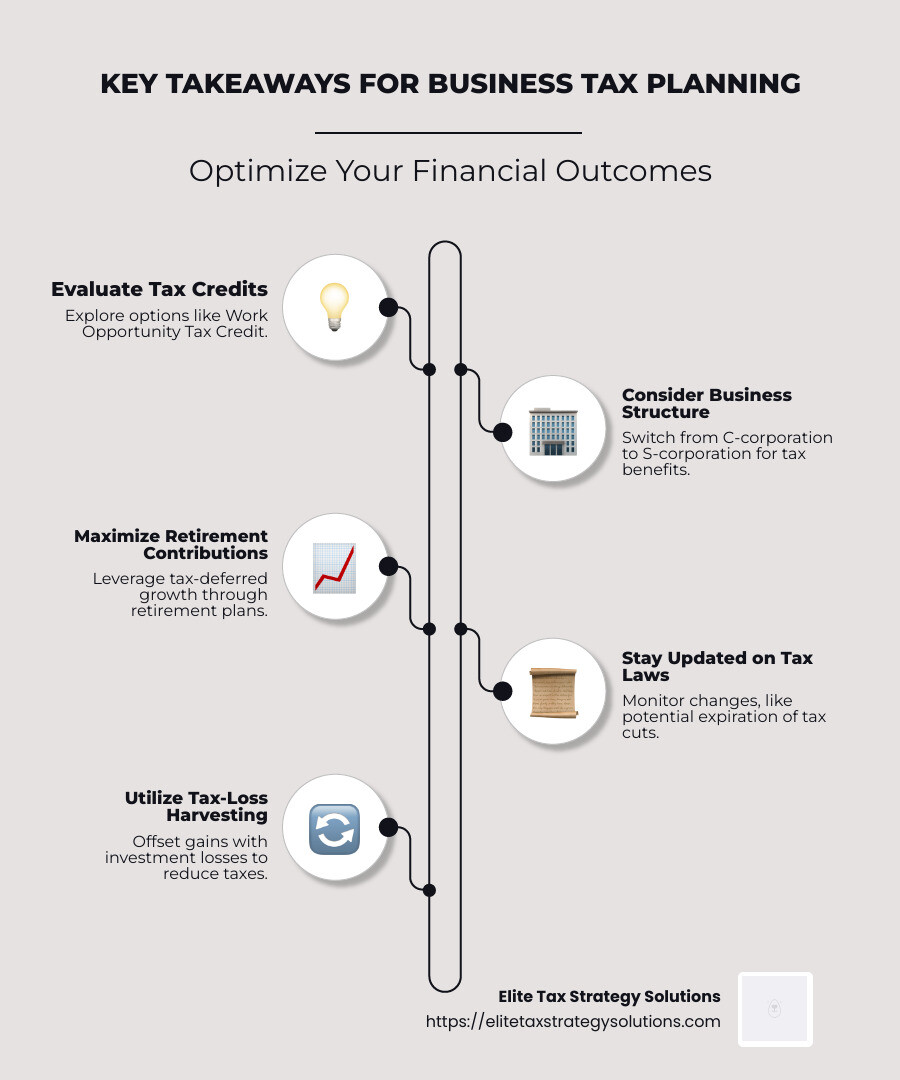

Business tax planning is the roadmap to enhancing your financial efficiency. For high-income earners and small business owners, it’s not just about preparing for tax season—it’s about optimizing financial outcomes and minimizing liabilities throughout the year. Here are the key takeaways for efficient business tax planning:

- Evaluate available tax credits, such as the Work Opportunity Tax Credit and Small Business Health Care Tax Credit, to lower your tax bill.

- Consider changing your business structure from a C-corporation to an S-corporation to potentially reduce tax liability.

- Maximize contributions to retirement plans, which can offer significant tax-deferred growth.

- Stay informed about changes in tax laws, such as the potential expiration of the Tax Cuts and Jobs Act provisions in 2025.

- Leverage tax-loss harvesting strategies to use investment losses for tax reduction.

These strategies can help manage tax burdens and bolster long-term financial stability.

My name is David Fritch, and I have over 40 years of experience in business tax planning, owning a law firm, and running a CPA practice. My mission is to simplify complex tax regulations and help you achieve financial efficiency.

Business tax planning word list:

– business tax reduction

– financial stability planning

– tax planning for small businesses

Understanding Business Tax Planning

Business tax planning is essential for optimizing your financial health. It’s not just about filing taxes; it’s about using smart strategies to reduce tax liabilities and increase savings.

Here’s how you can make business tax planning work for you:

Tax Strategies

Effective tax strategies can make a big difference. By planning ahead, you can take advantage of tax breaks and deductions. This involves understanding how various business decisions impact your taxes.

For example, choosing the right business structure can be crucial. If your business is a C-corporation, switching to an S-corporation might save you money. S-corporations don’t pay corporate income taxes. Instead, income is passed to owners, potentially lowering the overall tax burden.

Tax Credits

Tax credits are powerful tools. They reduce your tax bill dollar-for-dollar. Some credits to consider include:

- Small Business Health Care Tax Credit: If you provide health insurance, this credit can cover a portion of your premium costs.

- Work Opportunity Tax Credit: Hire individuals from certain groups and earn a credit.

- Disabled Access Credit: Make your business more accessible and get up to $5,000 in credits.

Tax Deductions

Deductions lower your taxable income. This means you pay less in taxes. Common deductions include:

- Business Expenses: Costs like rent, utilities, and supplies can be deducted.

- Depreciation: Spread out the cost of property over time and enjoy ongoing deductions.

- Home Office Deduction: Deduct a portion of your home expenses if you use it for business.

By understanding these elements of business tax planning, you can make informed decisions that lead to financial efficiency. Keep these strategies in mind to manage your tax responsibilities effectively and support your business’s growth.

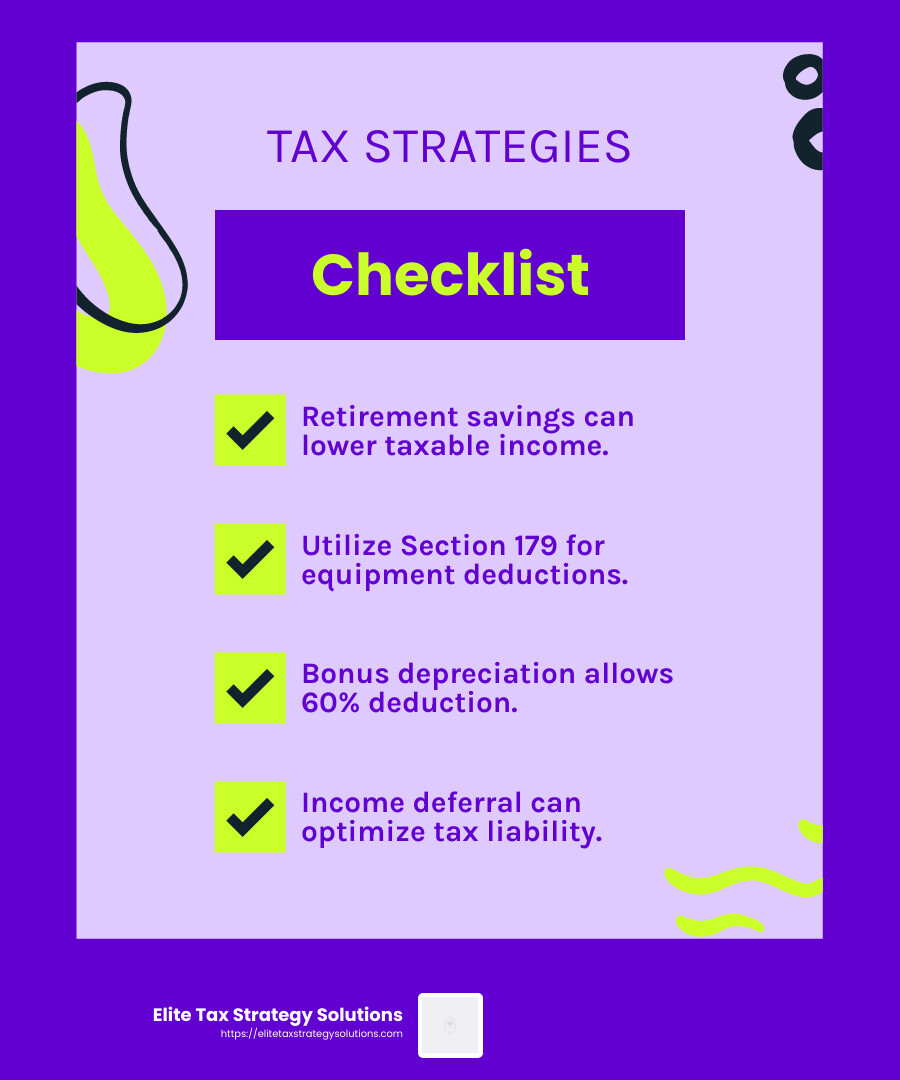

Key Tax Planning Strategies for Businesses

Business tax planning is more than just a yearly task. It’s an ongoing strategy to improve financial efficiency and minimize tax liabilities. Here are three key strategies to consider: retirement savings, equipment deductions, and income deferral.

Retirement Savings

Planning for retirement is not only good for your future but can also save you money on taxes now. Contributing to a retirement plan like a 401(k) or SEP IRA is a great way to reduce taxable income.

- Maximize Contributions: By contributing the maximum allowed amount to your retirement plan, you can lower your taxable income. This means you pay less in taxes while securing your future.

- Tax Credits: Small businesses can also qualify for tax credits to offset the costs of starting a retirement plan. This makes it easier to provide attractive benefits to employees while enjoying tax savings.

Equipment Deductions

Investing in new equipment can be a significant expense, but it comes with tax benefits.

- Section 179 Deduction: This allows businesses to deduct the full purchase price of qualifying equipment, up to $1,220,000. It’s a powerful tool to reduce taxes in the year of purchase.

- Bonus Depreciation: For property placed in service before the end of the year, businesses can deduct 60% of the cost. This applies to both new and used property and can provide substantial savings.

Income Deferral

Deferring income can help you manage your tax liability by pushing income into a future tax year.

- Timing is Key: If you expect to be in a lower tax bracket next year, consider deferring income. This might involve delaying invoices or payments until after the new year.

- Plan Purchases: If you anticipate higher income in the coming year, defer equipment purchases to maximize deductions when your tax rate is higher.

By incorporating these strategies into your business tax planning, you can improve your financial efficiency and support long-term growth. Up next, we’ll discuss the 5 Pillars of Effective Tax Planning to further optimize your tax strategy.

5 Pillars of Effective Tax Planning

When it comes to business tax planning, five key pillars can guide you towards financial efficiency: deducting, deferring, dividing, disguising, and dodging. Let’s break down each of these strategies to help you understand how they can benefit your business.

1. Deducting

Deducting is about reducing your taxable income by claiming all eligible business expenses. This includes costs like wages, rent, utilities, and more. For instance, leveraging the Section 179 Deduction allows businesses to deduct the full purchase price of qualifying equipment, up to $1,220,000. By maximizing deductions, you can significantly lower your tax bill.

2. Deferring

Deferring involves postponing income to a future tax year to manage tax liability. If you’re on a cash basis accounting method, you might delay sending invoices until next year to keep this year’s taxable income lower. This strategy is particularly useful if you expect to be in a lower tax bracket next year.

3. Dividing

Dividing refers to spreading income across different entities or family members to take advantage of lower tax brackets. For example, if you own a family business, you can gift business interests to family members, utilizing their lower tax rates. This strategy can also involve setting up multiple business entities to optimize tax outcomes.

4. Disguising

Disguising isn’t about hiding income but rather about smartly categorizing it. This can involve structuring transactions to qualify for more favorable tax treatments. For example, converting ordinary income into capital gains, which are often taxed at lower rates, can save a substantial amount in taxes.

5. Dodging

Dodging is about legally avoiding taxes through strategic planning and using available tax credits. For instance, the Work Opportunity Tax Credit offers a dollar-for-dollar reduction in taxes for hiring from certain groups, like veterans. By staying informed about such credits, businesses can effectively reduce their tax burden.

Each of these pillars offers unique advantages, and by integrating them into your tax strategy, you can improve your business’s financial efficiency. Next, we’ll explore how to maximize tax credits and deductions to further optimize your tax position.

Maximizing Tax Credits and Deductions

When it comes to business tax planning, one of the smartest moves is to maximize your tax credits and deductions. These can significantly reduce your tax liability, helping you keep more of your hard-earned money. Let’s explore some key credits and deductions that can boost your financial efficiency.

R&D Tax Credit

The Research and Development (R&D) Tax Credit is a powerful tool for businesses involved in innovation. If your company is working on developing new products, processes, or technologies, you might qualify for this credit. It’s designed to encourage businesses to invest in innovation by offering a dollar-for-dollar reduction in tax liability.

For small businesses with less than $50 million in gross receipts, the R&D credit can even offset payroll taxes. This means you can potentially reduce the amount you owe in payroll taxes, freeing up cash flow to reinvest in your business.

Employer Wage Credit

The Employer Wage Credit is available for businesses that continue to pay wages to employees who are called to active military duty. This credit equals 20% of the first $20,000 of wage payments per employee. It’s an excellent way to support your employees while also benefiting your business financially.

To qualify, you must have a written plan in place for providing differential wage payments. This credit not only helps your bottom line but also strengthens your commitment to supporting those who serve.

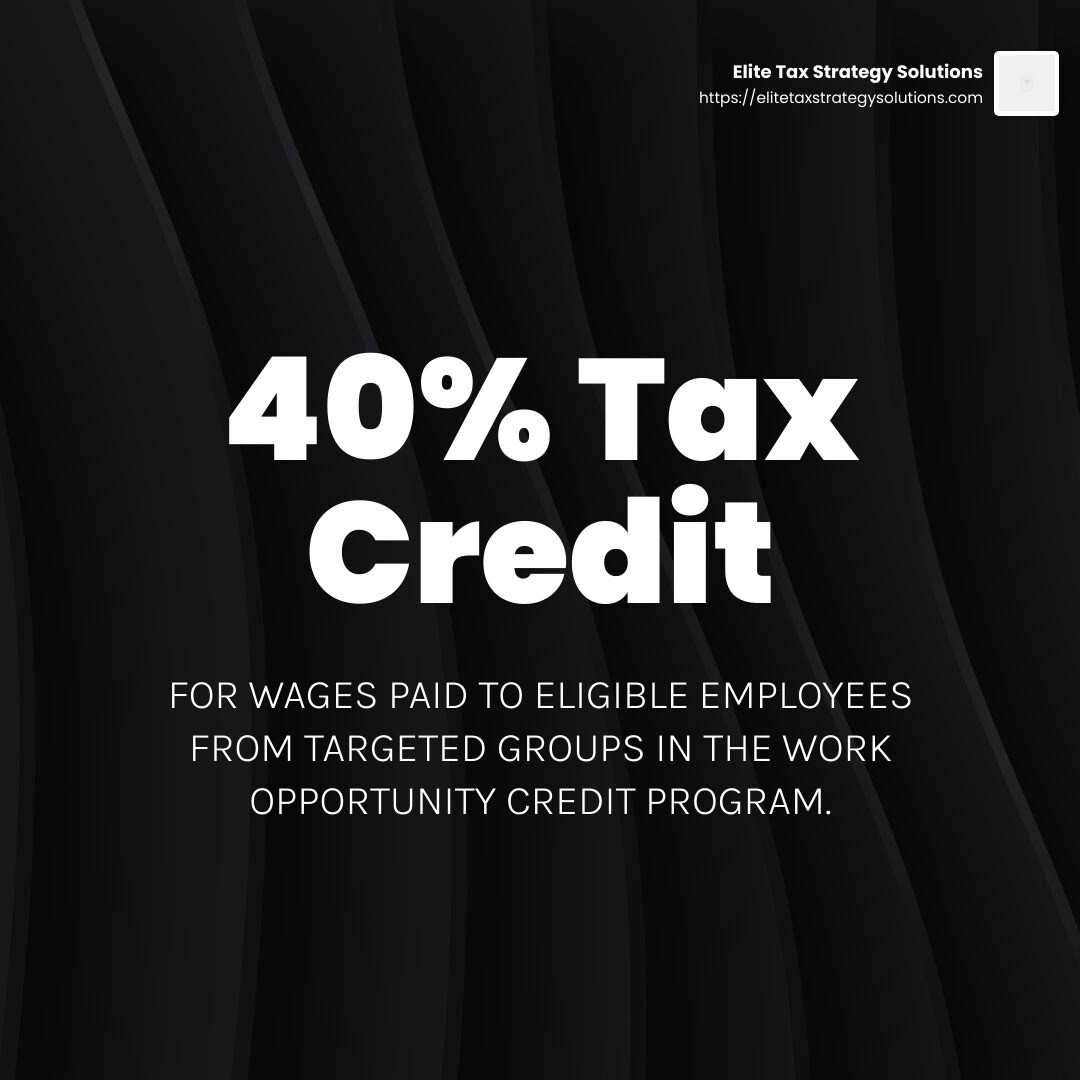

Work Opportunity Credit

The Work Opportunity Credit is another valuable incentive for businesses. It’s available to employers who hire individuals from certain targeted groups that have historically faced employment challenges. This includes veterans, long-term unemployed, and recipients of various public assistance programs.

By hiring from these groups, you not only gain a diverse workforce but also earn a tax credit. The credit is particularly beneficial for businesses looking to make a positive impact while also lowering their tax burden.

By leveraging these credits and deductions, your business can significantly reduce its tax liability. This allows you to reinvest savings into growth and innovation, driving your business forward. Next, we’ll address some frequently asked questions about business tax planning to further clarify how you can optimize your tax strategy.

Frequently Asked Questions about Business Tax Planning

How do I plan my business taxes?

Planning your business taxes starts with keeping accurate tax records. This means organizing all receipts, invoices, and other financial documents throughout the year. Good record-keeping helps identify business expenses that can be deducted, like office supplies, travel costs, and employee salaries.

Another key part of planning is understanding your tax obligations. Use tools like the IRS’s Small Business and Self-Employed Tax Center to stay informed. And don’t forget to consult with a tax professional for personalized advice.

What are the 5 pillars of tax planning?

-

Deducting: This involves identifying all eligible expenses to reduce taxable income. Common deductions include rent, utilities, and advertising costs.

-

Deferring: Deferring income to a future tax year can help manage tax liability, especially if you expect to be in a lower tax bracket.

-

Dividing: Splitting income among family members or business partners can reduce overall tax rates. This is often done through salary or dividend payments.

-

Disguising: This refers to legally structuring transactions to minimize taxes, not to be confused with illegal tax evasion.

-

Dodging: While it sounds shady, in tax planning, it means using legal means to avoid taxes, like investing in tax-exempt bonds.

How do LLC owners avoid taxes?

LLC owners can avoid double taxation by using a pass-through entity structure. This means the business itself is not taxed; instead, income is passed through to the owners’ personal tax returns.

Another strategy is electing to be taxed as an S Corporation. This allows owners to pay themselves a reasonable salary and take additional profits as distributions, potentially reducing self-employment taxes.

By understanding and applying these strategies, LLC owners can effectively manage their tax obligations and keep more of their earnings.

Now that we’ve covered these FAQs, you’re equipped with the basics to start optimizing your business tax strategy.

Conclusion

In today’s complex financial landscape, achieving financial stability requires more than just managing your day-to-day operations. It means strategically planning for the future, especially when it comes to taxes. This is where business tax planning becomes crucial.

Elite Tax Strategy Solutions is here to guide you through this intricate process. Our personalized services are designed to help high earners and closely held businesses maximize their tax savings while ensuring compliance with ever-changing tax laws. We understand that every business is unique, and so are its tax challenges.

Our proactive approach involves a deep dive into your financials to identify opportunities for tax optimization. Whether it’s leveraging tax credits like the R&D credit or structuring your business as a pass-through entity, we tailor strategies to your specific needs. Our goal is to not only reduce your tax liability but also align your tax plan with your broader financial goals.

By partnering with us, you gain access to a team of seasoned tax professionals who are committed to your financial success. We believe that with the right tax strategy, you can achieve greater financial stability and focus on what truly matters—growing your business.

For more information on how we can assist you with comprehensive financial planning, visit our service page. Let’s work together to secure your financial future.