Why Tax Planning Matters for High Earners

The best tax avoidance strategies high income earners can use typically save them tens of thousands of dollars annually. For busy professionals focused on their careers or businesses, understanding these strategies is essential for wealth preservation.

Top 5 Tax Avoidance Strategies for High Income Earners:

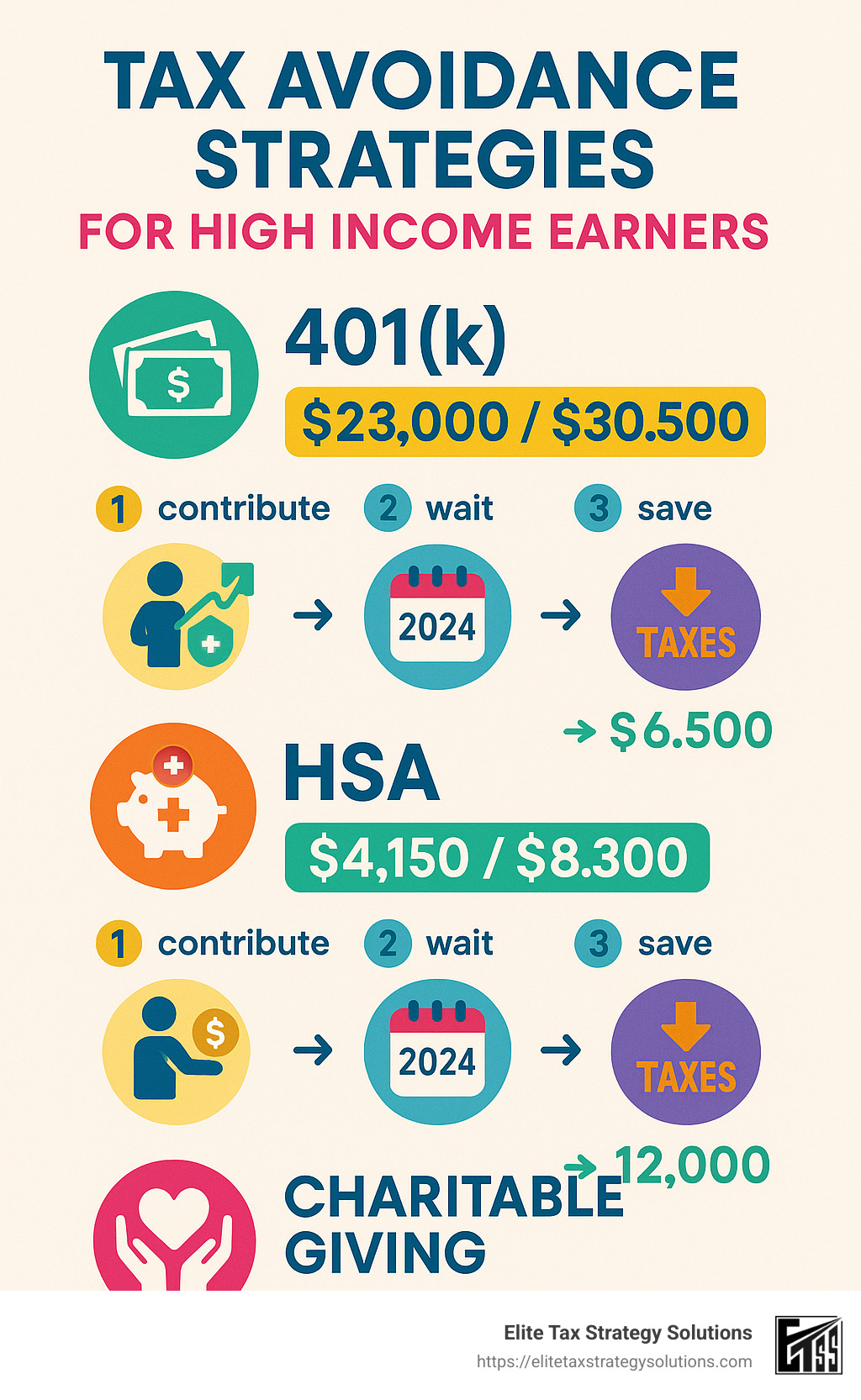

1. Maximize retirement accounts – Contribute the full $23,000 to 401(k)s ($30,500 if over 50)

2. Use Health Savings Accounts – Contribute $4,150 individual/$8,300 family in 2024

3. Harvest tax losses – Offset up to $3,000 in ordinary income annually

4. Consider charitable giving – Donate appreciated assets to avoid capital gains

5. Optimize business structure – S-corporations can reduce self-employment taxes

As Benjamin Franklin once wrote, “Nothing is certain except death and taxes.” While you can’t avoid taxes entirely, high-income earners have legitimate strategies to minimize their tax burden within the bounds of the law.

The U.S. tax code is progressive, meaning higher earners pay a larger percentage of their income in taxes. For 2024, the top federal bracket is 37% for single filers earning above $609,350 and married couples filing jointly above $731,200. Add state taxes, Medicare surtaxes, and other assessments, and your effective tax rate can approach or exceed 50% in high-tax states.

Tax avoidance (legal strategies to minimize taxes) differs significantly from tax evasion (illegal non-payment). The strategies outlined in this article focus exclusively on legal tax avoidance through proper planning and structure.

I’m David Fritch, a CPA with over 40 years of experience implementing the best tax avoidance strategies high income earners can use legally, including my time at Arthur Andersen and running my own tax practice focused on helping clients earning $200,000 to $2,000,000 annually save significantly on their tax bills.

Handy best tax avoidance strategies high income earners terms:

– extra medicare tax for high earners

– tax planning for partnerships

– wealth management tax planning

1. Define High Income & Know Your Bracket

Do you consider yourself a high-income earner? Before we dive into money-saving strategies, let’s get crystal clear on what this actually means and why understanding your tax bracket is the foundation of smart tax planning.

When the IRS looks at your tax return, they consider you a “high-income individual” if you report $200,000 or more in total positive income (TPI). But in the real world of tax planning, most professionals (including us at Elite Tax Strategy Solutions) typically work with clients earning $500,000+ annually in this category.

For 2024, the federal tax system tops out at a hefty 37% rate. This applies if you’re:

– Single and your taxable income exceeds $609,350

– Married filing jointly with taxable income over $731,200

Here’s what the complete 2024 federal income tax bracket landscape looks like:

| Tax Rate | Single Filers | Married Filing Jointly |

|---|---|---|

| 10% | $0 – $11,600 | $0 – $23,200 |

| 12% | $11,601 – $47,150 | $23,201 – $94,300 |

| 22% | $47,151 – $100,525 | $94,301 – $201,050 |

| 24% | $100,526 – $191,950 | $201,051 – $383,900 |

| 32% | $191,951 – $243,725 | $383,901 – $487,450 |

| 35% | $243,726 – $609,350 | $487,451 – $731,200 |

| 37% | Over $609,350 | Over $731,200 |

But wait, there’s more! (Isn’t there always when it comes to taxes?) High earners often face additional taxes beyond these base rates:

The 3.8% Net Investment Income Tax kicks in on your investment income when your Modified Adjusted Gross Income (MAGI) crosses $200,000 (single) or $250,000 (married filing jointly). And don’t forget the 0.9% Additional Medicare Tax that applies to wages exceeding those same thresholds.

Understanding the difference between your marginal rate (the tax on your last dollar earned) and your effective rate (your total tax divided by total income) is crucial. Many clients are surprised to learn their effective rate is much lower than their marginal rate, which opens up strategic planning opportunities.

Why the best tax avoidance strategies high income earners begin with clear definitions

“If you don’t know where you are, you can’t plan where you’re going.” This old adage perfectly applies to tax planning. Without knowing exactly which brackets and surtaxes affect you, you might implement strategies that miss the mark completely.

As tax expert Geoffrey Chen wisely notes: “Tax management can be important, particularly if you have worked hard to build up a business or a career. You want to be able to enjoy what you have earned and protect it.”

We’ve seen this play out countless times with our clients. Those who clearly understand their Adjusted Gross Income (AGI) and how it affects various deductions and credits are better positioned to make smart decisions about retirement contributions, charitable giving, and business expenses.

This clarity serves three important purposes:

-

Planning scope – It helps quantify potential savings (sometimes hundreds of thousands of dollars for our highest-earning clients)

-

Strategic focus – It directs attention to the most impactful strategies for your specific situation

-

Audit readiness – Clients who understand their tax situation can confidently explain their positions if the IRS comes knocking

Think of knowing your tax bracket as the foundation of your financial house. Everything else we’ll discuss builds on this essential knowledge. With this foundation in place, we can move on to exploring specific strategies that will help keep more of your hard-earned money in your pocket—legally and confidently.

2. Max Out Tax-Advantaged Retirement Accounts

When it comes to legally keeping more of your hard-earned money, few strategies are as powerful as retirement accounts. For high-income earners, these tax-advantaged accounts aren’t just about preparing for retirement—they’re about keeping tens of thousands of dollars out of the IRS’s hands right now.

In 2024, you have several opportunities to shield your income from taxes:

- Traditional 401(k) or Roth 401(k): $23,000 ($30,500 if you’re over 50 with that extra $7,500 catch-up contribution)

- SEP IRA: Up to 25% of your compensation or $69,000, whichever is less

- Solo 401(k): $23,000 in employee contributions plus employer contributions up to a total of $69,000

- Traditional or Roth IRA: $7,000 ($8,000 if you’re over 50)

- Health Savings Account (HSA): $4,150 for individuals, $8,300 for families (plus $1,000 catch-up if 55+)

- Flexible Spending Account (FSA): $3,200

Let me share a real-world example. Ted, a surgeon earning $750,000 annually, came to us at Elite Tax Strategy Solutions feeling frustrated about his tax bill. We helped him implement a comprehensive retirement strategy: maximizing his hospital’s 401(k) ($23,000), his wife’s 401(k) ($23,000), establishing a defined benefit plan through his private practice ($250,000 annual contribution), and making HSA contributions ($8,300).

The result? Ted reduced his taxable income by over $300,000, saving approximately $111,000 in federal taxes alone. That’s money that stayed in his family’s pocket rather than going to Uncle Sam.

Retirement savings: the best tax avoidance strategies high income earners can automate

What I love about retirement accounts is their simplicity. Once set up, these best tax avoidance strategies high income earners can use require almost no ongoing effort. Your payroll department or financial institution handles the contributions automatically, creating a true “set it and forget it” approach to tax savings.

This automation ensures you consistently benefit in three key ways:

First, you get immediate tax deductions. Every dollar you contribute to traditional retirement accounts is a dollar that doesn’t show up on your taxable income. For someone in the 37% bracket, each $10,000 contributed saves $3,700 in federal taxes alone.

Second, you enjoy tax-deferred growth. Your investments compound year after year without being taxed on dividends, interest, or capital gains. This tax-free compounding creates a snowball effect that can dramatically accelerate your wealth building.

Third, you create opportunities for future Roth conversions. Many of our clients at Elite Tax Strategy Solutions strategically convert portions of their pre-tax retirement savings to Roth accounts during lower-income years (like sabbaticals or early retirement), paying taxes at lower rates than they would have during peak earning years.

“Every penny counts for reducing your taxable income,” notes a tax specialist at SmartAsset. “If you’re a high earner, you’ll likely want to take advantage of as many tax breaks as possible.”

For business owners and self-employed individuals, the opportunity is even greater. SEP IRAs and Solo 401(k)s allow for significantly higher contribution limits than standard employer plans. Some of our entrepreneurial clients save over $50,000 annually in taxes through these vehicles alone.

The best part? These strategies are completely above-board. The tax code explicitly encourages retirement savings through these incentives. You’re not exploiting a loophole—you’re following the system exactly as designed.

More info about Tax Planning for High Earners

3. Backdoor & Mega Backdoor Roth Conversions

If you’re a high earner, you’ve probably finded that traditional Roth IRA contributions are out of reach due to income limitations. Fortunately, there are two powerful workarounds that can still give you access to tax-free growth: the Backdoor Roth IRA and its bigger sibling, the Mega Backdoor Roth conversion.

Backdoor Roth IRA

The Backdoor Roth strategy is like finding a side entrance to a club that wouldn’t let you through the front door. Here’s the simple dance:

First, you make a contribution to a traditional IRA (up to $7,000 in 2024, or $8,000 if you’re over 50). Since you’re a high earner, this contribution isn’t deductible on your taxes – but that’s actually part of the plan.

Next, you’ll need to file Form 8606 with your tax return to document this non-deductible contribution. This form is crucial – it establishes your “basis” so you won’t be taxed twice.

Then comes the magic: you convert this traditional IRA to a Roth IRA. If you do the conversion quickly (ideally within days of your contribution), you’ll pay taxes only on any tiny amount of earnings that accumulated between steps – often just pennies.

Take Sophia, for example. As a tech executive earning $350,000 annually, direct Roth IRA contributions were off the table. But by using the Backdoor Roth strategy consistently for five years, she’s built a $35,000+ nest egg that will grow completely tax-free for decades. That’s money the IRS can never touch again, no matter how large it grows.

Mega Backdoor Roth Conversion

If the Backdoor Roth is a side entrance, the Mega Backdoor is like finding a secret tunnel that lets you move substantially more money into tax-free territory. This strategy can potentially allow you to contribute up to $69,000 (minus your regular 401(k) contributions) into Roth accounts.

The Mega Backdoor works through your employer’s 401(k) plan, but with a twist. First, you max out your regular 401(k) contribution ($23,000 in 2024). Then, if your plan allows, you make additional after-tax contributions (not to be confused with Roth contributions) up to the overall limit of $69,000, minus your initial $23,000 and any employer matching.

The final step is converting these after-tax contributions to either a Roth 401(k) within your plan or rolling them into a Roth IRA.

As tax advisor Gio Bartolotta puts it: “The Mega Backdoor Roth is a strategy I love for folks with sufficient cash flow. It’s one of the most powerful wealth-building tools available to high-income earners.”

Step-by-step checklist

Before diving into these strategies, make sure you’re properly prepared:

Check eligibility: Not all 401(k) plans support the Mega Backdoor strategy. Call your plan administrator and specifically ask if they allow both after-tax contributions (beyond the regular pre-tax or Roth limits) and either in-plan Roth conversions or in-service distributions.

Beware the pro-rata rule: This is a common pitfall. If you have existing pre-tax money in any IRA accounts (including SEP or SIMPLE IRAs), the IRS will consider all your IRAs as one big pot when calculating taxes on your conversion. Consider rolling these into your employer’s 401(k) first if possible.

Coordinate with payroll: For the Mega Backdoor, work closely with your payroll department to ensure your contributions are properly classified. Timing matters here.

Review plan documents: Some 401(k) plans have specific requirements about when conversions or distributions can happen. Know the rules before you start.

Keep meticulous records: Document everything related to your contributions, conversions, and especially your Form 8606 filings. These records will be gold if questions ever arise.

One of our clients at Elite Tax Strategy Solutions, a physician earning $500,000 annually, implemented both strategies simultaneously. He maxed out his regular 401(k) ($23,000), made after-tax contributions ($35,000), and executed a backdoor Roth IRA ($7,000). The result? $65,000 moved into tax-advantaged accounts in a single year, with most headed for completely tax-free growth.

These strategies aren’t just clever tax tricks – they’re about creating a future where your retirement savings can grow and be withdrawn without Uncle Sam taking another bite. For high earners facing limited traditional retirement options, these backdoor approaches represent some of the best tax avoidance strategies high income earners can implement.

More info about Best Tax Saving Strategies for High Income Earners

4. Harness Health & Education Accounts

When you’re earning a high income, every tax advantage matters. Beyond your retirement accounts, health and education savings vehicles offer exceptional tax benefits that can significantly reduce your tax burden while helping you prepare for major life expenses.

Health Savings Accounts (HSAs)

The HSA might be the most underappreciated tax planning tool available today. It offers a unique triple tax advantage that even retirement accounts can’t match:

- Your contributions are tax-deductible (reducing your current tax bill)

- Your investments grow completely tax-free

- Withdrawals for qualified medical expenses are never taxed

For 2024, you can contribute $4,150 for individual coverage or $8,300 for family coverage. If you’re 55 or older, you can add another $1,000 as a catch-up contribution.

Here’s a strategy that savvy clients love: Instead of using your HSA funds for current medical expenses, pay those costs out-of-pocket and keep your receipts. Let your HSA investments grow tax-free for decades, then reimburse yourself tax-free years (or even decades) later. There’s no time limit on reimbursements!

“I’ve been telling my high-income clients for years that HSAs are the secret MVP of tax planning,” shares David Fritch, lead tax strategist at Elite Tax Strategy Solutions. “It’s like a retirement account with a medical emergency exit – completely tax-free.”

Flexible Spending Accounts (FSAs)

While not as powerful as HSAs, FSAs still offer valuable tax savings. In 2024, you can contribute up to $3,200 to a healthcare FSA and up to $5,000 to a dependent care FSA (for childcare or adult dependent care expenses).

Unlike HSAs, most FSA plans require you to use the funds within the plan year or forfeit them, though some employers offer a grace period or limited rollover option. The key is careful planning – estimate your expenses conservatively to avoid leaving money on the table.

Pro tip: If you have access to both an HSA and healthcare FSA, the FSA can be limited to dental and vision expenses only (a “limited purpose FSA”), allowing you to maximize both accounts simultaneously.

529 College Savings Plans

If you have children or grandchildren, 529 plans offer tremendous tax advantages for education funding. While contributions aren’t federally tax-deductible, many states offer income tax deductions or credits. The real power comes from tax-free growth and tax-free withdrawals for qualified education expenses.

One of the best tax avoidance strategies high income earners can use with 529 plans is front-loading contributions:

You can contribute up to five years’ worth of the annual gift tax exclusion in a single year without triggering gift taxes. For 2024, that’s a whopping $90,000 per beneficiary ($180,000 for married couples). This strategy removes a significant sum from your taxable estate while jumpstarting years of tax-free growth.

A new benefit starting in 2024: Beneficiaries can now roll over up to $35,000 from 529 plans into Roth IRAs over their lifetime. This addresses a common concern about overfunding 529s, as unused funds now have another tax-advantaged destination. The 529 account must have been open for at least 15 years, and annual Roth contribution limits still apply.

Jennifer, a corporate attorney client earning $450,000 annually, implemented all three strategies. She maxed out her family HSA ($8,300), contributed to her dependent care FSA ($5,000), and front-loaded two years of 529 contributions for her twins ($36,000 each). Her state offers a $10,000 annual deduction for 529 contributions, which she’ll claim over multiple years. The combined strategies reduced her taxable income significantly while building tax-advantaged assets for her family’s future.

“These accounts aren’t just about tax savings today,” Jennifer told us. “They’re about creating tax-free growth opportunities that compound over decades.”

More info about Tax Diversification Strategy High Income

5. Tax-Loss Harvesting & Capital-Gain Timing

Smart investors know that how you manage investment gains and losses can make a huge difference in your tax bill. When I work with clients at Elite Tax Strategy Solutions, I often find that tax-loss harvesting and thoughtful capital gain timing are among the best tax avoidance strategies high income earners can use to keep more of their investment returns.

Tax-Loss Harvesting

Think of tax-loss harvesting as finding the silver lining in investment clouds. When investments drop in value, you can turn that paper loss into a tax advantage by selling the investment and using the loss to offset other gains.

Here’s what happens: You sell investments that have declined in value, and these realized losses can offset capital gains from other investments that performed well. If your losses exceed your gains for the year, you can actually deduct up to $3,000 against your ordinary income. Any unused losses roll forward to future tax years, giving you a tax-reducing asset for years to come.

I remember working with Alex, a marketing executive with a $100,000 capital gain from selling company stock. We identified underperforming investments in her portfolio with $80,000 in losses. By selling these positions, she offset most of her gain, reducing her tax bill significantly. The remaining $20,000 was taxed at the preferential long-term capital gains rate, and she now has a tax-loss carry-forward she can use in future years.

One important warning: Watch out for the “wash-sale rule.” The IRS won’t let you claim a tax loss if you buy the same or a “substantially identical” security within 30 days before or after the sale. It’s their way of preventing people from creating artificial losses while maintaining the same investment position.

Capital-Gain Timing

When you sell an investment matters almost as much as what you sell. Long-term capital gains—from assets held more than a year—enjoy preferential tax rates:

- 0% if you’re in the 10% or 12% income tax brackets

- 15% for most middle-bracket taxpayers

- 20% for those in the top income bracket (plus potentially the 3.8% Net Investment Income Tax)

The difference between short-term and long-term rates can be dramatic. Short-term gains (assets held a year or less) are taxed at your ordinary income rate, which could be as high as 37% plus the 3.8% NIIT.

Timing your sales thoughtfully can lead to significant tax savings. Consider selling in years when your income is lower, spreading large gains across multiple tax years, or timing gains to coincide with charitable contributions that can offset the income.

Off-season gain harvesting playbook

While everyone talks about harvesting losses, strategic “gain harvesting” can be equally valuable in the right circumstances. This is especially true for bracket windows—times when your income temporarily places you in the 0% long-term capital gains bracket. During these windows, you can sell appreciated assets up to the bracket limit, pay zero federal tax on the gain, and immediately repurchase the investment to establish a higher cost basis. Unlike with losses, the wash-sale rule doesn’t apply to gains.

Charitable stacking is another powerful technique. By pairing large capital gains with substantial charitable donations in the same year, you can offset the tax impact while supporting causes you care about. One client of mine donated highly appreciated stock directly to charity instead of selling it first—avoiding capital gains tax entirely while still getting the full charitable deduction.

Be mindful of mutual fund distribution planning too. Many mutual funds distribute capital gains near year-end, which can create unexpected tax liabilities. If you’re planning to exit a fund position anyway, consider selling before these distribution dates.

I recently worked with a retired executive whose income fluctuates year to year. During a low-income year, we identified an opportunity to sell $80,000 of long-held appreciated stock that fell within his 0% capital gains bracket. He paid no federal capital gains tax, immediately repurchased the same investments, and reset his cost basis higher—positioning himself for smaller taxable gains in the future.

By approaching investment tax planning with the same care you give to investment selection, you can significantly improve your after-tax returns—keeping more of your money working for you rather than going to the IRS.

6. Charitable Giving Power Plays

Charitable giving represents one of the most fulfilling ways to reduce your tax burden while making a positive impact on causes you care about. For high-income earners, strategic philanthropy can transform generosity into powerful tax advantages.

Donor-Advised Funds (DAFs)

A donor-advised fund works like a charitable investment account, offering an neat solution for tax-conscious givers. When you contribute to a DAF, you receive an immediate tax deduction, then recommend grants to your favorite charities whenever it makes sense for you.

This approach offers remarkable flexibility for high earners. For instance, James, a software executive facing an unusually high-income year after his company’s acquisition, contributed $100,000 to a DAF at Fidelity Charitable. This allowed him to claim the full deduction immediately while spreading his actual charitable giving across several years.

Bunching your charitable contributions through a DAF is particularly powerful. Rather than giving $10,000 annually to charity, you might contribute $30,000 to your DAF every third year, helping you exceed the standard deduction threshold and maximize tax benefits through itemizing.

DAFs also excel for donating appreciated securities. When you contribute stocks or funds you’ve held for more than a year, you avoid capital gains tax completely while still receiving a deduction for the full market value. This double tax benefit makes DAFs one of the best tax avoidance strategies high income earners can implement.

“I always tell clients that DAFs are like having your own mini-foundation without the administrative headaches,” notes a tax advisor at Elite Tax Strategy Solutions. “The minimum to start is typically just $5,000 to $25,000, making it accessible to many successful professionals.”

Qualified Charitable Distributions (QCDs)

For those aged 70½ or older, Qualified Charitable Distributions offer a tax-efficient giving strategy that works directly from your IRA. You can transfer up to $105,000 annually (increased from $100,000 in prior years) directly to qualified charities.

What makes QCDs particularly valuable is that they count toward your Required Minimum Distributions without increasing your taxable income. Unlike regular withdrawals, QCDs don’t appear in your Adjusted Gross Income, potentially reducing Medicare premium surcharges and taxation of Social Security benefits.

Martha, a retired physician in Jasper, directed $50,000 from her IRA to her church’s building fund using a QCD. This satisfied a large portion of her RMD requirement without increasing her taxable income, effectively allowing her to donate pre-tax dollars.

Charitable Remainder Trusts (CRTs)

For substantial charitable intentions, Charitable Remainder Trusts offer sophisticated benefits. A CRT works by donating assets to an irrevocable trust that provides you or your beneficiaries with income for a specified period, after which the remainder goes to your chosen charities.

The immediate benefits include a partial tax deduction and potential avoidance of capital gains tax on appreciated assets. For business owners approaching retirement or those with highly appreciated assets, CRTs can be transformative.

Dr. Olivia, a 64-year-old physician and Elite Tax Strategy Solutions client, funded a Charitable Remainder Unitrust with $1 million of highly appreciated real estate. She received an immediate $400,000 tax deduction, avoided capital gains tax on the appreciation, and secured a lifetime income stream of 5% of the trust’s value annually.

Turning generosity into the best tax avoidance strategies high income earners respect

Effective charitable strategies align personal values with tax planning. The most successful philanthropists I’ve worked with follow these principles:

First, align with your mission by supporting causes you genuinely care about. Your giving should reflect your values, not just tax advantages. This personal connection makes your philanthropy more meaningful and sustainable.

Second, analyze your deduction situation carefully. Charitable strategies work best when you’re itemizing deductions rather than taking the standard deduction. With the higher standard deduction ($13,850 for singles and $27,700 for married filing jointly in 2024), strategic bunching of donations becomes even more important.

Third, be mindful of contribution limits. Cash donations are generally deductible up to 60% of your AGI, while appreciated property donations are limited to 30% of AGI. Excess contributions can be carried forward for up to five years.

Finally, consider Schedule A optimization by coordinating your charitable giving with other itemized deductions like mortgage interest and state/local taxes (capped at $10,000). This holistic approach maximizes the tax value of each charitable dollar.

“I’ve found that the most satisfied clients are those who view philanthropy as a dual opportunity—advancing their personal values while intelligently managing their tax liability,” observes David Fritch, founder of Elite Tax Strategy Solutions. “It’s not about avoiding taxes entirely, but rather about directing those dollars toward causes you believe in rather than sending them to the Treasury.”

charitable contribution deductions

7. Deferred Compensation & Executive Plans

As your income climbs, so do your tax obligations—but what if you could legally postpone paying taxes on a significant portion of your earnings? Deferred compensation plans offer exactly this opportunity for executives and high-earning professionals, creating a powerful tax-shifting strategy that can save you thousands.

Non-Qualified Deferred Compensation (NQDC) Plans

NQDC plans are the secret weapon in many executives’ tax planning arsenal. These arrangements let you postpone receiving a portion of your compensation—whether salary, bonus, or commissions—until a future date you choose.

“I was skeptical at first,” shares Jonathan, a 55-year-old sales executive earning $750,000 annually who became an Elite Tax Strategy Solutions client last year. “But deferring $200,000 of my compensation each year has dramatically reduced my current tax burden. I’ll receive these funds during retirement when my tax bracket will be much lower.”

The beauty of NQDC plans lies in their flexibility. You can specify exactly when you want to receive the deferred compensation—perhaps during a planned sabbatical, after retirement, or spread across several years to manage your tax brackets strategically.

However, there’s an important tradeoff to consider. Unlike qualified retirement plans like 401(k)s, NQDC plans are essentially a promise from your employer to pay you later. These “rabbi trusts” don’t offer the same protection from your company’s creditors. If your employer faces financial difficulties, your deferred compensation could be at risk.

Section 83(i) Stock Deferral

For employees at eligible private companies, Section 83(i) offers a valuable opportunity to defer income tax on certain stock options or restricted stock units for up to five years. This provision can be particularly valuable if you work for a growing company where equity compensation forms a significant part of your package.

To take advantage of this provision:

– Make the election within 30 days of when your equity compensation vests

– Ensure your company offers a broad-based equity compensation plan

– Be aware that certain events (like an IPO) will trigger the end of the deferral period

Bonus Timing Strategies

Even without formal deferred compensation plans, smart timing of your compensation can yield significant tax savings. Requesting bonus payment deferrals from December to January can shift income from one tax year to the next. Structuring multi-year performance bonuses to pay out strategically can keep you from being pushed into higher tax brackets. Timing stock option exercises thoughtfully can prevent unnecessary tax acceleration.

These strategies don’t require complex legal structures—just thoughtful planning and sometimes a simple conversation with your employer. As one of our clients put it, “Moving my $150,000 year-end bonus from December to January was probably the easiest $13,000 in tax savings I’ve ever created.”

Supplemental Executive Retirement Plans (SERPs)

SERPs represent another layer of retirement benefits beyond standard qualified plans. Unlike 401(k)s, these employer-provided plans don’t have contribution limits, allowing companies to offer significant retirement benefits to key executives.

Typically, SERPs are designed to replace a specific percentage of your pre-retirement income and may include attractive provisions for early retirement. Since they’re funded by your employer, they don’t reduce your current cash flow like other retirement savings might.

At Elite Tax Strategy Solutions, we help clients in Jasper, Indiana and beyond balance the opportunity of these plans with their inherent risks. For most executives, the best tax avoidance strategies high income earners can implement involve a diversified approach—combining qualified plans, after-tax savings, and strategic participation in deferred compensation arrangements.

“The key is creating a customized payout schedule that aligns with your life plans,” explains one of our senior tax strategists. “We had a client schedule her deferred compensation to coincide with her children’s college years—creating income when she needed it while keeping her in a reasonable tax bracket.”

More info about High Income Individual Tax Planning

8. Asset Location & Alternative Investments

When it comes to building wealth as a high-income earner, it’s not just what you invest in—it’s where you keep those investments. Strategic placement of your assets across different account types can significantly boost your after-tax returns without changing your overall investment approach.

Asset Location Strategy

Think of your investment accounts as different buckets, each with unique tax treatments. By placing investments in the most tax-advantaged location, you can keep more of what you earn.

For your tax-deferred accounts (like 401(k)s and traditional IRAs), focus on investments that would otherwise create tax headaches in taxable accounts. These include bonds that generate ordinary income, REITs with their non-qualified dividends, and actively managed funds that frequently buy and sell holdings.

Meanwhile, in your taxable brokerage accounts, prioritize tax-efficient investments like ETFs, which rarely distribute capital gains due to their unique structure. Low-turnover index funds and stocks you plan to hold for years (or even decades) also work well here since you control when to realize the gains.

Sarah, a physician earning $450,000 annually, worked with Elite Tax Strategy Solutions to reorganize her portfolio. By moving her bond funds and REITs into her IRA while keeping her ETFs and long-term stock holdings in her taxable account, she saved approximately $7,200 in taxes in the first year alone—without changing her overall asset allocation.

“This simple repositioning strategy can add 0.25-0.75% to annual after-tax returns,” notes a financial strategist. “That might not sound like much, but compounded over decades, it can add hundreds of thousands to your retirement nest egg.”

Municipal Bonds

For high-income earners, municipal bonds offer a straightforward tax advantage: interest income that’s exempt from federal taxes and, in many cases, state taxes if you buy bonds issued in your state of residence.

While the stated yield on municipal bonds is typically lower than comparable taxable bonds, the tax-equivalent yield often makes them more attractive for those in higher tax brackets. For someone in the 37% federal bracket plus state taxes, a municipal bond yielding 3% might deliver the same after-tax return as a taxable bond yielding 5% or more.

“Municipal bonds might not be the most exciting investment,” says a veteran tax advisor, “but they’re like finding money in the street for high-income clients—especially those living in high-tax states like California or New York.”

Just be mindful of the alternative minimum tax (AMT), as interest from certain municipal bonds (particularly “private activity bonds”) can trigger AMT liability.

Real Estate Investment Strategies

Real estate remains one of the most tax-advantaged investment vehicles available to high-income earners. Beyond potential appreciation and income, real estate offers numerous tax benefits:

Depreciation allows you to deduct the cost of buildings over time (27.5 years for residential properties and 39 years for commercial properties), creating a “paper loss” that can offset rental income.

Cost segregation takes this concept further by identifying components of a property that can be depreciated over shorter periods—5, 7, or 15 years instead of 27.5 or 39. This accelerated depreciation creates larger upfront deductions.

1031 exchanges let you defer capital gains taxes indefinitely by rolling proceeds from a property sale into a new “like-kind” property. This strategy allows real estate investors to trade up to larger properties while deferring taxes.

Carol, a 52-year-old business owner and Elite Tax Strategy Solutions client, used a 1031 exchange when selling a commercial property with a $500,000 gain. By exchanging into a larger property and implementing a cost segregation study, she deferred the gain indefinitely while generating over $100,000 in additional first-year depreciation deductions.

Opportunity Zone investments offer another avenue for tax-advantaged real estate investing. By reinvesting capital gains into designated economically distressed communities, investors can defer and potentially reduce their original capital gains tax liability.

Cryptocurrency and Digital Assets

Digital assets require particularly careful tax planning due to their volatile nature and evolving tax treatment:

Tracking cost basis for each acquisition is essential, as cryptocurrency transactions can quickly become complex with multiple buys, sells, and exchanges across different platforms.

Be aware that crypto-to-crypto exchanges (like trading Bitcoin for Ethereum) are taxable events—something many investors don’t realize until tax time.

Tax-loss harvesting opportunities abound in volatile crypto markets. When prices drop, consider selling to realize losses that can offset other capital gains, then reinvesting if you still believe in the long-term prospects.

Interestingly, the wash sale rule (which prevents claiming losses when you repurchase substantially identical securities within 30 days) may not currently apply to cryptocurrency—though legislation could change this treatment soon.

Private Equity and Alternative Investments

For accredited investors, private equity, venture capital, and hedge funds can offer unique tax advantages:

Carried interest provisions allow fund managers to receive profits at long-term capital gains rates rather than ordinary income rates (though the holding period requirement has been extended to three years).

These investments often pass through losses and deductions to investors, which can offset other income depending on your level of participation and basis.

Some early-stage investments may qualify for the Qualified Small Business Stock (QSBS) exclusion, which can shield up to $10 million in gains from federal taxes if certain requirements are met.

At Elite Tax Strategy Solutions, we help clients in Jasper, Indiana and surrounding areas develop comprehensive asset location strategies that minimize tax drag while maintaining appropriate risk levels and diversification. We believe that proper asset location is one of the best tax avoidance strategies high income earners can implement with minimal effort but significant long-term impact.

More info about Tax Diversification Strategy High Income

9. Business Owner Deductions & Entity Design

If you’re a business owner, you’re sitting on a gold mine of tax-saving opportunities. Let me walk you through some of the most powerful strategies that my clients have used to dramatically reduce their tax bills while staying completely within the bounds of the law.

Section 162 Ordinary and Necessary Business Expenses

The tax code allows you to deduct expenses that are “ordinary and necessary” for your business. This simple phrase opens up a world of legitimate deductions that many business owners don’t fully use.

Your home office can be a significant tax saver if you use a portion of your home regularly and exclusively for business. One client of mine transformed a spare bedroom into a dedicated office and deducted a proportional share of her mortgage interest, utilities, and even depreciation on her home, saving thousands annually.

Vehicle expenses represent another substantial opportunity. For 2024, you can claim 65.5 cents per mile driven for business purposes, or track your actual expenses if that’s more favorable. I always tell my clients to install a mileage tracking app on their phones – those business trips to meet clients or vendors add up quickly!

When you travel for business, nearly everything becomes deductible – airfare, hotels, and even 50% of your meals. And don’t overlook professional development costs like conferences, courses, and certifications that keep you at the top of your game.

For self-employed individuals, health insurance premiums can be 100% deductible for you and your family – a benefit that often saves my clients $15,000-$20,000 annually in pre-tax dollars.

“Claim ordinary and necessary business expenses under IRC Section 162,” advises Sherman Standberry, CPA. Just remember that documentation is your best friend. I recommend keeping digital records of all receipts with notes about the business purpose – this simple habit can save you tremendous headaches if the IRS ever comes knocking.

S-Corporation Salary Optimization

One of the best tax avoidance strategies high income earners who own businesses can implement is operating as an S-corporation with an optimized salary strategy.

Here’s why this works so beautifully: S-corporations pass profits directly to shareholders without self-employment tax. While you must pay yourself a “reasonable salary” subject to FICA taxes (15.3% on the first $168,600 in 2024), any remaining profits can be taken as distributions free from this tax.

I worked with Michael, a marketing consultant earning $300,000 annually, to restructure his business as an S-corporation. We carefully documented industry standards to justify setting his salary at $150,000, allowing him to take the remaining $150,000 as distributions. This simple change saved him approximately $21,000 in self-employment taxes in just one year.

As tax advisor Gio Bartolotta notes, “S corporations may make sense at $100,000–$120,000 of taxable business income.” The key is finding that sweet spot where your salary is defensibly “reasonable” while maximizing your tax savings.

Qualified Business Income (QBI) Deduction

The Tax Cuts and Jobs Act introduced a powerful deduction that allows many business owners to simply erase 20% of their qualified business income from their tax return. This deduction applies to pass-through entities including sole proprietorships, partnerships, and S-corporations.

For service businesses like doctors, lawyers, and consultants, the deduction begins to phase out at incomes of $191,950 for single filers and $383,900 for married couples filing jointly in 2024. For other businesses, the deduction may be limited based on W-2 wages paid or property owned.

This provision is currently set to expire after 2025, making it even more important to take advantage while it’s available. I’ve had clients intentionally accelerate income into current years to maximize this 20% deduction before it potentially disappears.

Augusta Rule (Section 280A)

This might be my favorite little-known strategy for business owners. Named after Augusta, Georgia (home of the Masters golf tournament), this provision allows you to rent your personal residence for up to 14 days per year completely tax-free.

Smart business owners can rent their home to their business for board meetings, planning sessions, or team retreats. The business gets a legitimate deduction for the rental expense, while you receive the income tax-free.

One client, a financial advisor, holds quarterly planning meetings at her home, charging her business a fair market rental rate of $500 per day. That’s $2,000 of completely tax-free income annually, plus her business gets a $2,000 deduction – a true win-win that’s perfectly legal when properly documented.

Retirement Plan Stacking

If you’re looking to shelter significant income, retirement plan stacking is one of the most powerful best tax avoidance strategies high income earners who own businesses can implement.

Unlike employees who are limited to their company’s 401(k), business owners can establish multiple retirement plans that work together. I helped Dr. James, a 57-year-old dentist, combine a Solo 401(k) with a cash balance plan. This allowed him to contribute over $200,000 annually to tax-deferred retirement accounts, generating approximately $74,000 in federal tax savings each year.

The beauty of this approach is that it’s completely above-board while creating enormous tax deductions. Plus, you’re building your retirement nest egg at an accelerated pace. For older business owners with strong cash flow, this strategy often provides six-figure annual tax deductions.

At Elite Tax Strategy Solutions, we work closely with business owners in Jasper, Indiana and surrounding areas to implement these strategies in a way that’s both tax-efficient and audit-resistant. The key is proper planning, immaculate documentation, and regular review as tax laws and your business evolve.

More info about Tax Avoidance Strategies for Small Business

10. Estate & Gift Strategies Before the 2026 Sunset

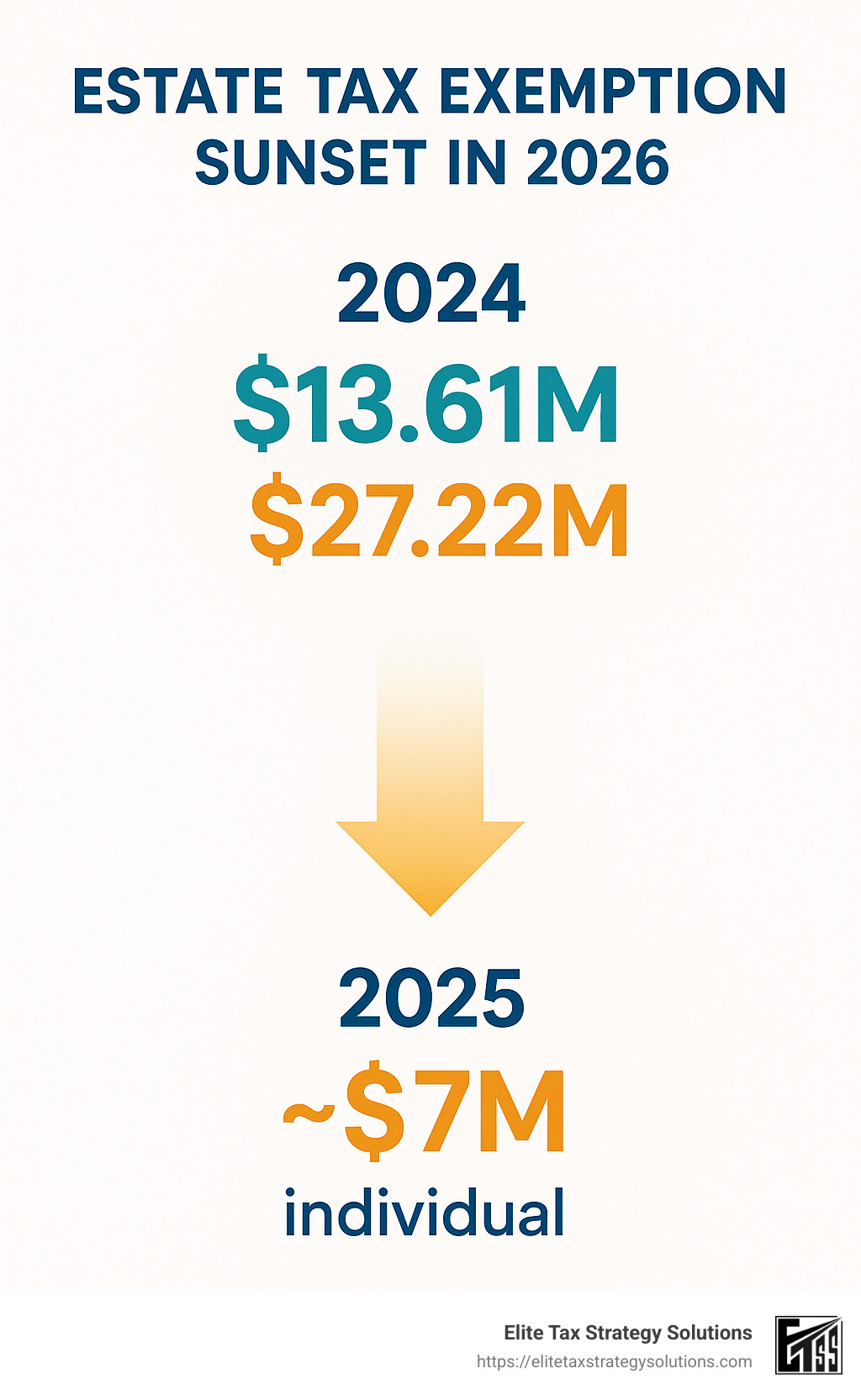

The clock is ticking on one of the most generous estate tax exemptions in American history. The Tax Cuts and Jobs Act (TCJA) dramatically increased how much wealth you can transfer tax-free, but this windfall is scheduled to disappear after 2025. For high-income earners with substantial assets, this creates an urgent planning opportunity you won’t want to miss.

Current Exemption Levels and 2026 Changes

Right now, in 2024, each individual can transfer an astonishing $13.61 million during life or at death without triggering federal estate or gift taxes. For married couples, that’s a combined $27.22 million shield against the 40% estate tax. Next year, this amount inches up slightly to $13.99 million per person.

But here’s where things get interesting—and potentially expensive. When the ball drops on December 31, 2025, these generous exemptions are set to plummet by roughly half, reverting to approximately $7 million per person (adjusted for inflation).

Think of it as a closing window of opportunity. Many of our clients at Elite Tax Strategy Solutions are accelerating their wealth transfer plans to lock in these historically high exemptions while they still can.

Annual Gift Tax Exclusion

Beyond the lifetime exemption, you can give away $18,000 per recipient in 2024 without touching your lifetime exemption amount. This is the annual gift tax exclusion, and it’s a powerful tool for methodical wealth transfer.

Married couples can double this amount through “gift-splitting,” allowing $36,000 per recipient annually. And remember, payments made directly for someone’s medical expenses or tuition are completely exempt from gift taxes, with no dollar limit. I’ve seen clients pay $50,000+ directly to medical providers or universities, removing substantial assets from their estate without using any exemptions.

One client of mine, a retired executive from Jasper, began gifting $18,000 to each of his three children and seven grandchildren annually. That’s $180,000 leaving his estate each year without using any lifetime exemption—a simple but powerful strategy.

Grantor Retained Annuity Trusts (GRATs)

GRATs are one of my favorite tools for transferring wealth, especially for assets likely to appreciate significantly. Here’s how they work: you transfer assets to an irrevocable trust and receive annuity payments over a set term (typically 2-10 years). Any appreciation above the IRS-assumed rate of return passes to your beneficiaries completely free of gift tax.

Carol, a retired business owner with substantial investments, implemented what we call “rolling GRATs” with our guidance. By funding a series of two-year GRATs with $2 million of volatile assets, she’s transferred over $3 million to her children gift-tax free over six years. The beauty of this strategy is that if investments underperform, you simply get all your assets back—there’s virtually no downside risk.

Qualified Small Business Stock (QSBS) Exclusion

If you’re a business owner or investor in qualifying small businesses, Section 1202 QSBS exclusion is potentially the most generous tax break in the entire tax code. When properly structured, it allows you to exclude from taxation the greater of $10 million or 10 times your basis in capital gains.

To qualify, you must hold the stock for at least 5 years, the company must be a C-corporation with assets under $50 million, and it must operate in qualifying industries (manufacturing, technology, and retail qualify; service businesses like law, medicine, and finance generally don’t).

What many don’t realize is that this benefit can be multiplied through gifts to family members or trusts—a technique called “QSBS stacking”—as each recipient gets their own $10 million exclusion. I’ve helped several tech entrepreneurs in our area save millions in taxes through careful QSBS planning.

Spousal Lifetime Access Trusts (SLATs)

Many clients hesitate to make large gifts, fearing they might need those assets later. This is where SLATs shine. A SLAT allows you to use your exemption while maintaining indirect access to the assets.

One spouse creates an irrevocable trust benefiting the other spouse and descendants. The assets leave the grantor’s estate for tax purposes, but the beneficiary spouse can still access them if needed. Often, both spouses create SLATs for each other, though careful planning is needed to avoid the “reciprocal trust doctrine” that could unwind the tax benefits.

James and Maria, business owners from southern Indiana, established SLATs for each other using their high exemptions. They transferred $20 million total to these trusts, protecting these assets from future estate taxes while maintaining access through each other.

Front-Loaded 529 Plans

Education planning offers another opportunity to remove assets from your estate. 529 plans allow you to front-load five years’ worth of annual exclusion gifts in a single year—that’s $90,000 per beneficiary ($180,000 for married couples).

William, a successful business owner in Jasper, front-loaded $180,000 into 529 plans for each of his four grandchildren. This removed $720,000 from his taxable estate while providing for their education. The best part? He only used one year’s worth of annual exclusion amounts, and he maintained control as the account owner.

At Elite Tax Strategy Solutions, we’re helping clients take advantage of the current high exemption amounts before they potentially vanish in 2026. The best tax avoidance strategies high income earners can implement often require careful planning and implementation, especially for estate planning. The time to act is now—once 2026 arrives, you’ll have lost half your exemption opportunity forever.

Frequently Asked Questions about the Best Tax Avoidance Strategies High Income Earners

What upcoming tax law changes could raise my bill?

Tax laws are constantly evolving, and staying ahead of these changes is crucial for high-income earners. Several significant shifts are on the horizon that could substantially impact your tax situation.

The most pressing concern is the scheduled sunset of the Tax Cuts and Jobs Act (TCJA) after 2025. This isn’t just a minor adjustment—it represents a potential seismic shift in your tax landscape. Those generous standard deductions you’ve been enjoying? They’ll shrink. The lower individual tax rates? They’ll climb back up. That helpful Qualified Business Income deduction that saves business owners up to 20% on pass-through income? It disappears unless Congress acts to extend it.

Perhaps most concerning for wealthy families is the estate tax exemption cliff we’re approaching. The current generous lifetime exemption of nearly $14 million per person is set to plummet to approximately $7 million (adjusted for inflation) in 2026. For married couples, that’s a difference of about $14 million of assets that could suddenly become subject to estate taxes at 40%.

“In 2026, a lot of the tax cuts that were implemented starting 2017 are set to expire,” warns tax advisor Gio Bartolotta. “This isn’t something to worry about in the distant future—it’s coming fast, and planning needs to happen now.”

Beyond the TCJA sunset, high earners should watch for potential expansion of the 3.8% Net Investment Income Tax to include active business income. There have also been persistent proposals to increase the top capital gains rate from 20% to as high as ordinary income rates for those earning over $1 million annually.

At Elite Tax Strategy Solutions, we’re helping clients implement strategies today that can mitigate these looming tax increases. Whether it’s accelerating income, maximizing current deductions, or completing wealth transfers while exemptions remain high, proactive planning is essential.

How can changing my domicile reduce state taxes?

Moving to a tax-friendly state can result in immediate, substantial tax savings for high-income earners. The difference can be dramatic—especially if you’re currently living in a high-tax state like California (13.3% top rate), New York (10.9%), or New Jersey (10.75%).

Nine states currently have no income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. For someone earning $1 million annually, moving from California to Nevada could save over $130,000 in state taxes each year—money that compounds significantly over time.

But here’s the catch—you can’t just buy a vacation home in Florida and claim residency while continuing to live in New York. State tax authorities are increasingly aggressive in auditing residency claims, particularly for high-income taxpayers.

The key distinction is between domicile and residency. Your domicile is your permanent legal home—the place where you intend to return even when you’re temporarily away. Most states consider you a resident for tax purposes if you spend more than 183 days there during the year (the so-called “183-day rule”), but domicile is about much more than just counting days.

“If your domicile state is California… even if you left to travel around the world in an RV for a year, California would still say you’re a resident,” cautions a tax expert. “They’re looking for your intent to permanently relocate, not just a temporary absence.”

To successfully establish a new domicile, you’ll need to create a paper trail that demonstrates your commitment to your new state. This includes changing your voter registration, driver’s license, and mailing addresses. You should purchase or rent a primary residence in the new state, join local organizations, establish community ties, and document time spent in each state through travel records and credit card receipts.

Even after establishing domicile in a tax-free state, you may still owe tax on income sourced from your former state. For example, if you own rental property in California, that rental income remains taxable in California regardless of where you live.

When should I hire a professional tax strategist?

While basic tax software might suffice for simple returns, high-income earners often reach a complexity threshold where professional guidance becomes not just helpful but necessary for optimal results.

Complex equity compensation is one of the most common triggers for seeking professional help. If you’re receiving RSUs, stock options, or participating in an Employee Stock Purchase Plan (ESPP), the tax implications can be substantial and mistakes costly. A skilled tax strategist can help you time exercises and sales to minimize your overall tax burden.

Multi-state income situations also warrant professional guidance. Whether you work across state lines, own property in multiple states, or are considering a domicile change as discussed above, navigating the intricacies of state taxation requires specialized knowledge.

Business transitions represent another critical juncture for professional tax planning. Starting, buying, selling, or restructuring a business involves numerous tax elections and entity choice decisions that can impact your financial picture for years to come.

Estate planning needs become increasingly important as your net worth approaches or exceeds the estate tax exemption. With the exemption scheduled to drop significantly in 2026, many more families will need sophisticated estate planning strategies to minimize transfer taxes.

Alternative investments like private equity, hedge funds, cryptocurrency, or other complex investments often generate complicated tax reporting requirements and planning opportunities that most self-preparers miss.

Finally, certain factors can increase your audit risk, including high income, self-employment, or large deductions. A professional can help ensure your return is not only tax-efficient but also defensible if questioned.

At Elite Tax Strategy Solutions, we specialize in creating comprehensive tax strategies for high-income individuals in Jasper, Indiana and surrounding areas. Our approach balances immediate tax savings with long-term wealth preservation, always maintaining a commitment to compliance and audit readiness.

The best tax avoidance strategies high income earners can implement often require professional guidance to execute properly and confidently. When the potential tax savings run into the tens or hundreds of thousands of dollars annually, professional fees become a wise investment rather than an expense.

Conclusion

Putting these best tax avoidance strategies high income earners can use into practice isn’t a one-time event—it’s more like tending a garden that needs regular attention. When thoughtfully implemented, these approaches can put tens or even hundreds of thousands of dollars back in your pocket each year.

I’ve seen clients transform their financial futures by starting with the basics and gradually incorporating more sophisticated techniques. The beauty of tax planning is that even small steps can yield significant results over time.

Begin with the fundamentals—max out your 401(k), contribute to IRAs and HSAs, and understand your tax bracket. These simple moves create the foundation for everything else. As one client told me after implementing just these basic strategies, “I can’t believe I’ve been leaving this money on the table for years!”

Tax planning works best when it’s proactive rather than reactive. Don’t wait until March or April to think about taxes—by then, most opportunities for the previous year have expired. Instead, check in quarterly to assess your tax situation and make adjustments. September and October are particularly good times to project your year-end tax position and implement last-minute strategies.

The real magic happens when multiple strategies work together. The business owner who combines an S-corporation structure with retirement plan stacking and strategic charitable giving will see exponentially better results than someone using just one approach. These strategies complement each other, creating tax-saving synergies that can dramatically reduce your overall tax burden.

Your tax plan should evolve as your life changes. Major events like marriage, children entering college, business transitions, or approaching retirement all trigger the need for strategy adjustments. Even without major life changes, tax laws themselves are constantly shifting—just look at the significant changes coming in 2026 when many TCJA provisions sunset.

Keep meticulous records, especially for more complex strategies. Good documentation is your best defense if the IRS comes knocking. As we like to tell clients at Elite Tax Strategy Solutions, “If it isn’t documented, it didn’t happen.”

I’ve worked with clients in Jasper, Indiana and throughout the region who’ve transformed their financial futures through thoughtful tax planning. One business owner reduced her tax bill by over $100,000 annually by implementing just a handful of the strategies we’ve discussed. Another client funded his children’s college education entirely through tax savings generated over a decade of disciplined planning.

The strategies outlined in this guide aren’t theoretical—they’re battle-tested approaches that work in the real world when properly implemented. While some may require professional guidance, many can be initiated on your own with proper research and care.

Remember what Benjamin Franklin wisely noted: “By failing to prepare, you are preparing to fail.” This wisdom rings especially true with taxes, where proactive strategy makes all the difference between building wealth and watching it slowly drain away through unnecessary taxation.

At Elite Tax Strategy Solutions, we specialize in creating personalized, audit-ready tax plans that maximize savings while ensuring compliance. Our team stays current on tax law changes and emerging planning opportunities to provide you with the most effective strategies for your specific situation.