Accounting and tax compliance are critical aspects for businesses and individuals alike, impacting financial health and legal standing. Non-compliance can lead to severe penalties and scrutiny from taxing authorities. Here are the key takeaways:

- Importance: Ensures financial accuracy and prevents costly penalties.

- Financial Health: Maintains proper cash flow and avoids unnecessary expenses.

- Penalties: Missed deadlines or incorrect filings can lead to fines.

In today’s business environment, keeping up with tax laws and regulations can be overwhelming. However, understanding these complexities is essential to safeguard your financial well-being. Accurate record-keeping and timely filings help in minimizing liabilities and ensuring compliance with current tax laws.

My name is David Fritch, and with 40 years of experience in both law and CPA practices, I’ve dedicated my career to assisting high-income earners and small business owners in managing their accounting and tax compliance obligations. Let’s explore together how these practices can benefit your financial stability in the long run.

Relevant articles related to accounting and tax compliance:

– foreign tax compliance

– international tax compliance

– tax compliance for companies

Understanding Tax Compliance in Accounting

What is Tax Compliance?

Tax compliance refers to the process of adhering to tax laws and regulations set by federal, state, and international bodies. This involves fulfilling taxpayer obligations, such as accurately reporting income, claiming deductions, and paying taxes on time. Compliance ensures that individuals and businesses meet all legal requirements, avoiding unnecessary scrutiny from tax authorities.

Tax laws can be complex and vary across different jurisdictions. For instance, the IRS Publication 4557 provides guidelines on safeguarding taxpayer data, while the FTC Safeguards Rule mandates financial institutions to protect customer information. These regulations highlight the importance of understanding and adhering to specific requirements to maintain compliance.

Importance of Tax Compliance

Adhering to tax compliance is crucial for several reasons:

-

Avoid Penalties and Legal Issues: Non-compliance can lead to severe penalties, including fines and interest charges. In some cases, it may even result in legal action. Timely and accurate tax filings help in avoiding these pitfalls.

-

Financial Stability: Ensuring tax compliance contributes to a business’s financial health. By maintaining accurate records and paying taxes on time, businesses can manage cash flow effectively and avoid unexpected expenses.

-

Accurate Records: Keeping detailed and accurate records is a cornerstone of tax compliance. This involves documenting all financial transactions, income, and expenses. Proper record-keeping supports accurate tax filings and aids in financial decision-making.

-

Timely Compliance: Meeting deadlines is a critical aspect of tax compliance. This includes filing tax returns by the due dates set by federal, state, and international tax authorities. Late filings can result in penalties and interest, impacting financial stability.

In a globalized economy, understanding international tax laws is also essential. Multinational companies must steer complex regulations, such as the OECD’s BEPS framework, to ensure compliance across different countries.

By staying informed and proactive, businesses and individuals can steer the complexities of tax compliance, safeguarding their financial well-being and avoiding costly mistakes.

Key Differences Between Accounting and Tax Accounting

When it comes to accounting and tax compliance, understanding the differences between GAAP (Generally Accepted Accounting Principles) and tax accounting is crucial. Let’s break down these concepts to make them more digestible.

GAAP vs. Tax Accounting

GAAP is the standard framework of guidelines for financial accounting used in the United States. It focuses on providing a clear picture of a company’s financial health. Tax accounting, on the other hand, is specifically designed to comply with tax laws and regulations. The two have several key differences:

-

Accrual Basis vs. Cash Basis: GAAP typically uses the accrual basis of accounting. This means revenue and expenses are recorded when they are earned or incurred, not necessarily when cash changes hands. Tax accounting, however, may use the cash basis, where transactions are recorded only when cash is received or paid. This can impact how income and expenses are recognized.

-

Economic Events and Income Recognition: Under GAAP, all economic events are recorded, providing a comprehensive view of a company’s financial status. In tax accounting, only those events that affect tax liabilities are considered. This can lead to differences in how income is recognized.

-

Expense Recognition: GAAP requires expenses to be matched with the revenues they help generate, following the matching principle. Tax accounting may allow for different timing in recognizing expenses, often to align with tax deduction opportunities.

Accounting vs. Tax Accounting

While accounting encompasses all financial transactions, tax accounting zeroes in on those that affect tax obligations:

-

Financial Transactions: Accounting tracks all financial transactions, providing data for financial statements. Tax accounting focuses on transactions that impact the company’s tax burden, ensuring compliance with tax laws.

-

Tax Burden and Calculation: In accounting, the tax burden is calculated according to GAAP. In tax accounting, it is calculated based on tax laws, which may allow for different methods, such as LIFO (Last-In, First-Out) inventory accounting for tax savings, even if FIFO (First-In, First-Out) is used for financial reporting.

-

Tax Document Preparation: Preparing tax documents involves specific forms and calculations required by tax authorities. This is distinct from preparing financial statements, which are used for internal and external reporting under GAAP.

Understanding these differences is vital for businesses to steer the complexities of both financial reporting and tax compliance. By aligning their accounting practices with both GAAP and tax requirements, companies can ensure accurate reporting and minimize their tax liabilities.

Next, we’ll explore best practices for ensuring tax compliance, including maintaining accurate records and using technology to streamline the process.

Best Practices for Ensuring Tax Compliance

Navigating accounting and tax compliance can be challenging, but following some best practices can make the journey smoother.

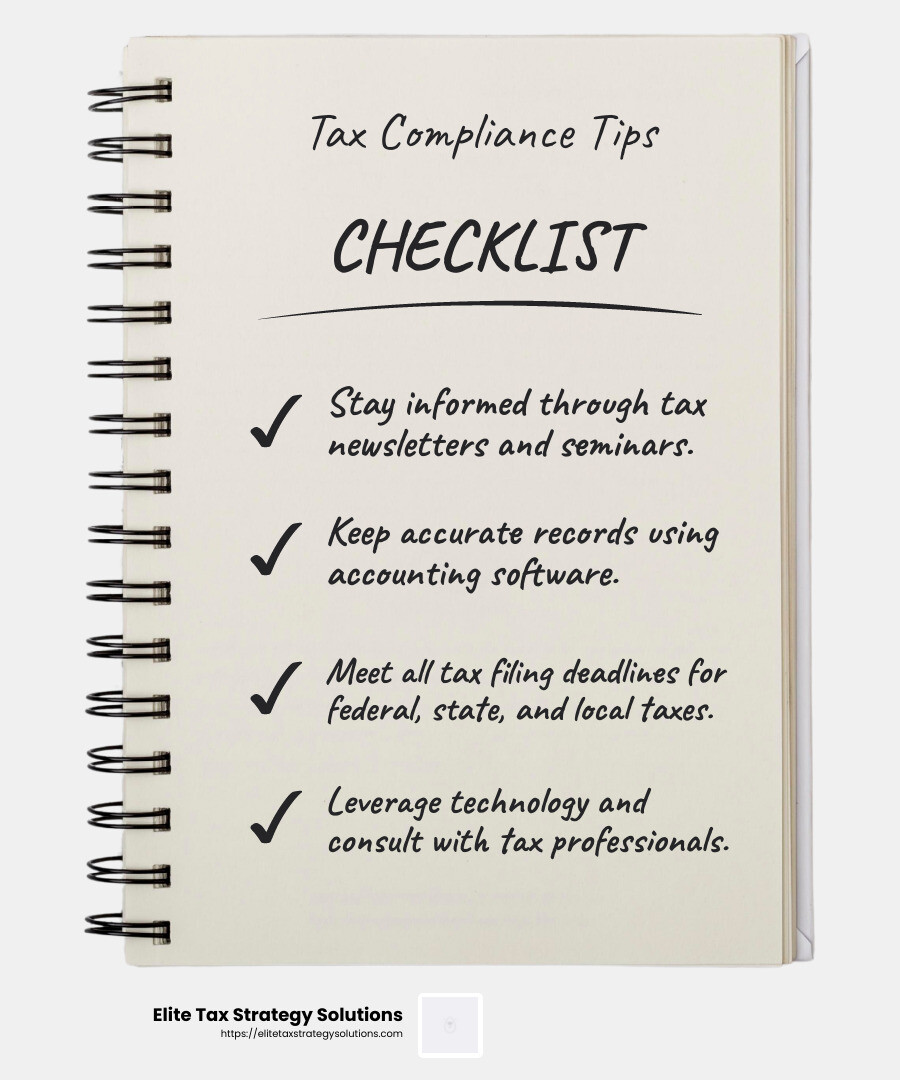

Staying Up-to-Date on Tax Laws

Tax laws are like a moving target—they change often. To stay on top of these changes, consider subscribing to tax newsletters or online publications. These resources provide regular updates on tax regulations. Attending seminars and workshops is another great way to keep informed. Tax professionals are also invaluable in this regard. They can offer insights and advice custom to your business needs.

Maintaining Accurate Records

Accurate record-keeping is the backbone of tax compliance. Your records should include all financial transactions like income, expenses, and receipts. Using accounting software can simplify this task. It automates bookkeeping and provides real-time financial data, making it easier to track and reconcile accounts.

Creating a record-keeping system that suits your business is also crucial. This system should include processes for documenting transactions and regularly reconciling accounts. Accurate records are essential for filing correct tax returns and avoiding penalties.

Filing Tax Returns on Time

Filing tax returns on time is crucial to avoid penalties. This includes federal, state, and local taxes. Deadlines vary, so knowing the specific dates for your business is important. Hiring a tax professional can help ensure that all returns are filed accurately and on time. They can also assist with tax planning strategies to minimize liabilities.

Tax filing software is another tool that can aid in timely tax filings. It automates the filing process and reduces errors. Plus, it offers real-time updates on tax regulations and deadlines.

Utilizing Technology and Professional Services

Technology is a game-changer in tax compliance. Accounting software and tax software streamline processes and reduce the risk of errors. These tools can automate many tasks and provide real-time updates on financial data.

Regular consultations with tax professionals are also beneficial. They offer expert advice on tax planning and compliance strategies. By using a combination of technology and professional services, you can ensure that your tax operations are effective and compliant with evolving tax rules.

By following these best practices, businesses can steer the complexities of tax compliance more effectively. Next, we’ll dig into the role of accounting in tax compliance, exploring how financial records and strategic decisions play a part.

The Role of Accounting in Tax Compliance

Link Between Accounting and Taxation

Accounting and tax compliance are like two sides of the same coin. Accounting provides the foundation for preparing accurate tax returns. It involves recording every financial transaction, which helps in determining the correct tax obligations.

Think of accounting as the detailed diary of a business’s financial life. It captures income, expenses, deductions, and credits. These records are crucial when tax season rolls around. Without accurate accounting, the risk of errors in tax determination increases, which can lead to penalties or audits.

For example, imagine a business that fails to record a significant expense. This oversight could result in a higher taxable income, increasing the tax burden unnecessarily. By carefully recording transactions, businesses can ensure they claim all eligible deductions and credits, minimizing their tax liability.

Planning and Decision-Making

Accounting is not just about keeping track of numbers. It’s a strategic tool that aids in making informed financial decisions. Understanding the tax implications of various business activities can help maximize profits and minimize tax liabilities.

Consider a company contemplating a major equipment purchase. Accounting can reveal the potential tax benefits of such an investment, like depreciation deductions. This insight can guide the decision, making it not only financially sound but also tax-efficient.

Moreover, by analyzing financial records, businesses can forecast future tax obligations. This foresight allows for better cash flow management and strategic planning. It ensures that funds are available to meet tax liabilities without disrupting operations.

Accounting acts as a navigator, guiding businesses through the complexities of tax compliance. It helps transform tax compliance from a daunting task into a strategic advantage, aligning financial decisions with long-term business goals.

Next, we’ll address some frequently asked questions about accounting and tax compliance, clarifying common queries and misconceptions.

Frequently Asked Questions about Accounting and Tax Compliance

What is tax compliance in accounting?

Tax compliance in accounting means following the rules set by federal, state, and international tax laws. It involves reporting income, expenses, and other financial data accurately and on time. Every taxpayer, whether an individual or a business, has obligations to file tax returns correctly and pay taxes due by the deadlines.

Keeping up with these obligations is crucial. Failure to comply can lead to penalties, legal troubles, and financial instability. Businesses often use accounting to ensure compliance by maintaining accurate financial records, which support their tax filings.

What is the difference between GAAP and tax accounting?

Generally Accepted Accounting Principles (GAAP) and tax accounting serve different purposes. GAAP focuses on the overall financial health of a business, using the accrual basis of accounting. This means recording income when it’s earned and expenses when they’re incurred, regardless of when cash changes hands.

Tax accounting, on the other hand, is all about preparing tax returns and calculating tax liabilities. It often uses the cash basis method, where income and expenses are recorded when cash is actually received or paid. This approach can affect how economic events, like income and expenses, are recognized.

For instance, under GAAP, a company might report revenue when a service is provided, even if payment hasn’t been received. But for tax purposes, that revenue might only be recognized once cash is received, affecting the timing and amount of taxable income.

What is the difference between accounting and tax accounting?

While both accounting and tax accounting deal with financial transactions, they have distinct goals. Accounting encompasses all financial dealings of a business, from tracking daily transactions to preparing financial statements. It’s about painting a complete picture of a business’s financial health.

Tax accounting narrows its focus to transactions that affect a business’s tax burden. It involves tax calculation and preparation of tax documents, ensuring compliance with tax laws. This includes identifying deductions and credits to minimize tax liabilities.

Imagine a business preparing its financial statements. For accounting purposes, it might use different methods to value inventory or depreciate assets. However, for tax purposes, it might choose methods that offer the best tax advantage, like using accelerated depreciation to reduce taxable income.

In summary, while accounting provides a broad view of financial health, tax accounting zeroes in on tax obligations, ensuring compliance and optimizing tax outcomes.

Conclusion

Tax compliance is more than just a legal requirement; it’s a cornerstone of financial health for any business. Failing to comply with tax laws can lead to severe penalties and legal issues, which can significantly impact a company’s bottom line and reputation.

At Elite Tax Strategy Solutions, we understand these challenges and offer a personalized approach to tax planning. Our proactive strategies are designed to optimize your tax position while ensuring you remain compliant with ever-changing regulations. By focusing on accurate record-keeping, timely filings, and leveraging technology, we help you avoid costly mistakes and penalties.

Our team is committed to helping you steer the complexities of tax compliance. We provide ongoing support, so you can focus on what you do best: running your business. Whether it’s through strategic planning or ensuring timely filings, our goal is to maximize your financial stability and minimize your tax liabilities.

For more information on how we can assist with your tax compliance needs, visit our Tax Support and Compliance Services page. Let us help you achieve peace of mind and financial success through effective tax management.