Why High-Income Earners Face Unique Tax Challenges

5 outstanding tax strategies for high income earners can make the difference between paying excessive taxes and keeping more of your hard-earned money. Here are the essential strategies every high earner should know:

- Maximize Tax-Advantaged Accounts – 401(k), HSA, and mega backdoor Roth contributions

- Amplify Charitable Giving – Donor-advised funds and charitable remainder trusts

- Optimize Investment Wins & Losses – Tax-loss harvesting and QSBS exclusions

- Control When & Where You Pay Tax – Income deferral and state residency planning

- Design an Estate & Legacy Blueprint – Gift tax exemptions and trust strategies

If you’re earning $200,000 or more annually, you’re in an exclusive club – but not necessarily one you want to be in. The top 20% of income-earning families in Canada pay 61% of the country’s personal income taxes. In the U.S., high earners face marginal tax rates of 37% at the federal level alone, before adding state taxes that can push your total rate above 50%.

The tax code wasn’t designed to be fair to high earners. From Alternative Minimum Tax to Medicare surtaxes, high earners face unique challenges that require sophisticated planning strategies.

But here’s the good news: smart tax planning can legally reduce your burden by tens of thousands of dollars annually. The ultra-wealthy didn’t get there by accident – they use advanced strategies that most high earners never learn about.

I’m David Fritch, and with 40 years of experience as both a CPA and attorney, I’ve helped thousands of high-income earners steer these complex tax waters. Through my firm Elite Tax Strategy Solutions, I’ve developed 5 outstanding tax strategies for high income earners that can dramatically reduce your tax liability while ensuring full compliance with IRS regulations.

Glossary for 5 outstanding tax strategies for high income earners:

– tax planning for dentists

– tax diversification strategy high income

– extra medicare tax for high earners

1. Boost Tax-Advantaged Accounts – One of the 5 outstanding tax strategies for high income earners

Tax-advantaged accounts are your personal tax shelter – completely legal and encouraged by the IRS. Most high earners are leaving serious money on the table by not maximizing these opportunities.

For 2024, you can contribute $23,000 to your 401(k), or $30,500 if you’re 50 or older. But that’s just the beginning. A high-earning couple can potentially shelter over $150,000 annually using what we call the “triple-stack approach” at Elite Tax Strategy Solutions.

Max Out 401(k)s & Mega Backdoor Roths

The mega backdoor Roth lets you contribute up to $69,000 total to your 401(k) in 2024, far beyond the standard $23,000 limit.

Here’s how: After maxing out your regular 401(k) contribution, you make additional after-tax contributions to your plan. Then you immediately convert these after-tax dollars to a Roth 401(k) or roll them to a Roth IRA. The result? Tax-free growth on substantially more money for the rest of your life.

There’s one catch – your employer’s 401(k) plan must allow both after-tax contributions and in-plan Roth conversions or in-service distributions. Check with your plan administrator first.

Over 20 years, that extra $46,000 annually growing tax-free could mean hundreds of thousands more in your pocket. For current rules and limits, check the Latest IRS contribution limits.

Harness Triple-Tax HSAs & FSAs

Health Savings Accounts are the holy grail of tax planning – the only account offering a triple tax shield: deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

For 2024, you can contribute $4,150 as an individual or $8,300 for family coverage. Here’s a strategy most people miss: use your HSA as a stealth retirement account. Pay medical expenses out-of-pocket now, save receipts, and let your HSA investments grow tax-free for decades.

After age 65, you can reimburse yourself tax-free for those old medical expenses – even ones from 20 years ago. Or withdraw funds for any purpose, paying ordinary income tax just like a traditional IRA.

Don’t forget Flexible Spending Accounts – they add another $3,200 in tax-free savings for 2024. For more comprehensive strategies, visit our guide on Tax Savings Strategies for High Income Earners.

Turbo-Charge Education Funding with 529 Plans

529 education savings plans offer high earners opportunities to reduce both current taxes and future estate tax liability. While contributions aren’t federally deductible, many states offer tax deductions for contributions to their own 529 plans.

The real power lies in “superfunding” – you can contribute up to five years’ worth of annual gift tax exclusions at once. That’s $90,000 per beneficiary ($180,000 for married couples) in 2024 without triggering gift taxes.

Here’s the game-changer: the SECURE Act 2.0 now allows unused 529 funds to be rolled over to a Roth IRA for the beneficiary, up to $35,000 lifetime. This eliminates concerns about “overfunding” a 529 plan.

2. Amplify Charitable Giving for Immediate & Future Savings

Strategic charitable giving becomes one of the most powerful weapons in your tax-fighting arsenal. You can deduct up to 60% of your adjusted gross income for cash donations to qualified charities. For appreciated property donations, that limit drops to 30%, but the tax benefits can be even more dramatic.

The secret? Timing and structure matter far more than the total amount you give. Instead of giving $50,000 to charity over five years, give it all in one high-income year and capture the maximum tax benefit.

Front-Load Gifts with Donor-Advised Funds

Donor-Advised Funds (DAFs) are like having a charitable checking account that gives you immediate tax benefits. Instead of writing $10,000 in charity checks every year, you contribute $50,000 to a DAF in one year. You get the full $50,000 deduction immediately, then distribute that $10,000 annually to your favorite charities over the next five years.

Here’s where it gets interesting – don’t donate cash, donate your appreciated stock instead. When you transfer stock that’s gained value to a DAF, you completely avoid capital gains tax while still getting a deduction for the full current market value.

I had a client who donated $100,000 worth of tech stock he’d bought for $20,000 years earlier. Instead of paying $15,200 in capital gains tax, he got a $100,000 charitable deduction. That’s a swing of over $115,000 in his favor.

Defer Gains via Charitable Remainder Trust

For high earners with substantial appreciated assets, Charitable Remainder Trusts (CRTs) offer the “have your cake and eat it too” strategy. You defer capital gains, generate steady income, claim a charitable deduction, and remove assets from your taxable estate.

You transfer highly appreciated assets into a CRT. The trust sells those assets without paying capital gains tax, then invests the proceeds and pays you an income stream for life or a specific number of years. You receive an immediate charitable deduction based on the present value of what will eventually go to charity.

Example: A client transferred $2 million of appreciated stock (originally purchased for $200,000) into a CRT. Instead of immediately paying $360,000 in capital gains tax, she received a $400,000 charitable deduction and now receives $120,000 annually for the next 20 years.

For those over 70½ with traditional IRAs, there’s the simpler Qualified Charitable Distribution strategy. You can transfer up to $100,000 annually directly from your IRA to qualified charities, avoiding income tax entirely. Check out the Qualified Charitable Distribution rules for complete requirements.

3. Optimize Investment Wins & Losses Like the Ultra-Wealthy

The difference between wealthy investors and everyone else isn’t just better stock picks – it’s how they manage taxes on their investments. Smart tax management can boost your after-tax returns by 1-2% annually, and over decades, that compounds into serious wealth.

You can deduct up to $3,000 annually against ordinary income from investment losses, with unlimited carryforward for excess losses. Advanced strategies can turn your investment account into a powerful tax-planning tool.

Harvest Losses & Gains Intelligently

Tax-loss harvesting isn’t just about selling losers. The real pros know how to harvest gains strategically too.

If you’re married filing jointly, you pay 0% tax on long-term capital gains up to $89,250 of taxable income in 2024. Having a low-income year? This creates a golden opportunity to sell winning investments, pay zero tax, and reset your cost basis higher for the future.

The beauty of gain harvesting is there’s no wash-sale rule. You can sell a position today to lock in gains at 0% tax, then buy it right back tomorrow. Try that with loss harvesting and the IRS will disallow your deduction if you repurchase within 30 days.

Real example: A client took a sabbatical year with unusually low income. We helped him harvest $85,000 in long-term gains from his taxable account, paying zero federal tax. When he returned to his high-paying job the following year, those same gains would have cost him over $20,000 in taxes.

For complete rules on capital gains taxation, check out IRS Topic 409 on capital gains.

Ride QSBS & Opportunity Zone Upside

Qualified Small Business Stock (QSBS) offers up to $10 million in completely tax-free gains (or 10 times your basis, whichever is greater). If you’re an entrepreneur, early employee at a startup, or investor in small businesses, this could be life-changing.

The requirements are specific: The company must be a C-corporation with gross assets under $50 million when your stock is issued, conduct an active business, and you must hold the stock for at least five years. When you sell qualifying QSBS after the five-year hold, the gains are completely federal tax-free.

Qualified Opportunity Zones offer different benefits. When you have capital gains from any source, you can invest those gains in a Qualified Opportunity Zone fund within 180 days. This defers the original gain until 2026, and if you hold the QOZ investment for 10 years, any new gains are completely tax-free.

4. Control When & Where You Pay Tax

You have more control over your tax bill than you think. It’s not just about how much you earn – it’s about when you recognize that income and where you pay taxes on it.

I’ve seen clients save $50,000 or more annually just by being strategic about timing and location. Income doesn’t always have to be taxed in the year you earn it, and not all states treat your money the same way.

Defer or Accelerate Income Strategically

Nonqualified Deferred Compensation (NQDC) plans let you earn money today but pay taxes on it years later when you might be in a lower bracket. This is especially powerful for executives who plan to retire early.

The catch – you must make these elections before the beginning of the year the compensation is earned. Miss that deadline, and you’ve lost the opportunity forever.

Roth conversions work in the opposite direction. If you’re having a low-income year, convert some of your traditional IRA or 401(k) money to a Roth account while you’re in a lower tax bracket. Pay taxes now at 22% instead of later at 37%.

Required Minimum Distributions don’t start until age 73, giving you more time for strategic conversions. For more advanced strategies, check out our comprehensive High Income Tax Planning guide.

Make State Residency Work for You

Moving to the right state can be like getting a massive raise. Nine states have zero personal income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. For someone paying California’s 13.3% top rate, relocating could mean keeping an extra $130,000 on every million earned.

But you can’t just buy a condo in Florida and call it a day. States are aggressive about challenging residency claims. You need real domicile indicators: spending more than 183 days per year in your new state, changing voter registration, getting a new driver’s license, opening local bank accounts.

Remote work has created opportunities and headaches. Some states try to tax you based on where your employer is located. These “convenience of the employer” rules can trip up remote workers.

Municipal bonds deserve mention here. For high earners in high-tax states, tax-free interest often beats taxable investments. A 4% tax-free municipal bond equals a 6.15% taxable return if you’re in the 35% federal bracket plus state taxes.

Don’t forget the $10,000 SALT deduction cap. Consider prepaying property taxes before year-end to maximize your deduction.

5. Design an Estate & Legacy Blueprint

Estate planning for high earners goes beyond preparing for what happens after you’re gone. It’s about creating a strategic blueprint that maximizes wealth transfer opportunities while you’re alive.

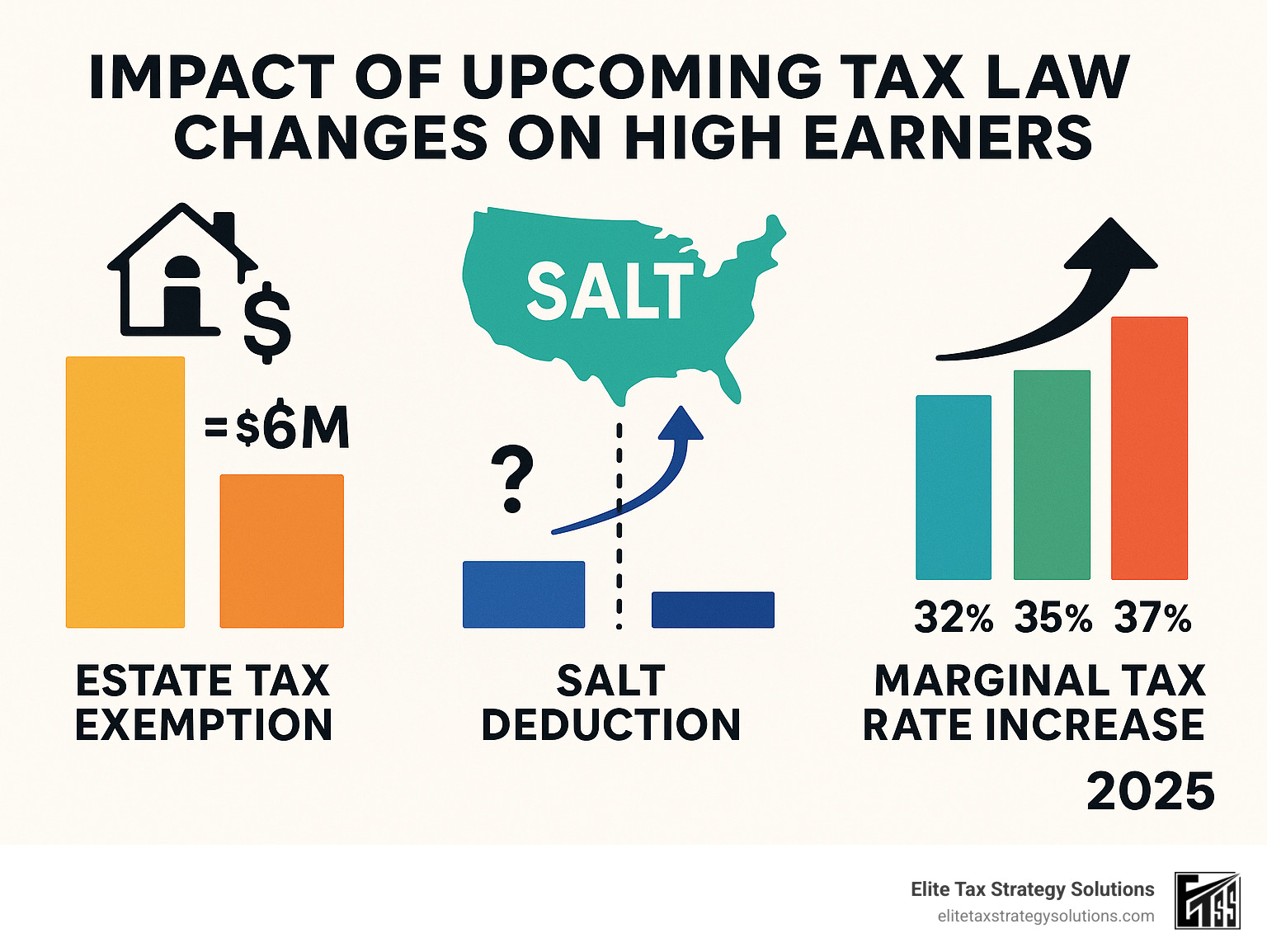

The current federal estate and gift tax exemption stands at $13.61 million per person ($27.22 million for married couples) in 2024. This historically high exemption is scheduled to sunset in 2026, potentially cutting your planning opportunities in half.

You have a narrow window to take advantage of generous tax laws. After 2025, the exemption will likely revert to around $6 million per person. That’s not just a reduction – it’s a massive shift that could cost wealthy families millions in additional taxes.

Lock In Today’s Generous Exemptions – a 5 outstanding tax strategies for high income earners essential

The “use it or lose it” nature of the current gift tax exemption creates real urgency. Every dollar of exemption you don’t use before 2026 may be permanently lost.

Grantor Retained Annuity Trusts (GRATs) allow you to transfer the appreciation potential of your assets while keeping an income stream. You maintain cash flow while moving future growth out of your taxable estate.

Family Limited Partnerships create opportunities to pool family assets and transfer interests at significant valuation discounts – often 20-40% – because you’re transferring minority interests in illiquid entities.

Sales to Intentionally Defective Grantor Trusts let you “sell” appreciating assets to trusts using promissory notes, effectively freezing the value in your estate while moving all future appreciation to your beneficiaries.

The 529 superfunding strategy becomes even more powerful from an estate planning perspective. By front-loading five years of annual exclusion gifts ($90,000 per beneficiary), you remove substantial assets from your estate.

For business owners, QSBS “stacking” offers incredible opportunities. Multiple family members can each claim up to $10 million in gain exclusion on the same company’s stock. A family of five could potentially shelter $50+ million in gains.

Preserve Wealth with Trusts & Tax-Smart Insurance

Irrevocable Life Insurance Trusts (ILITs) remove death benefits from your taxable estate while providing liquidity to pay estate taxes. This becomes critical when your estate consists of illiquid assets like closely-held businesses.

Cash-value life insurance offers additional tax-sheltered savings opportunities for high earners who have maxed out 401(k)s, IRAs, and HSAs. The cash value grows tax-deferred, and you can access it tax-free through policy loans.

Critical warning: Avoid Modified Endowment Contract (MEC) status by not overfunding policies in the first seven years. Cross that line, and you lose the tax advantages.

Policy loans offer tax-free access to your cash value, creating a tax-free income stream in retirement. For comprehensive estate planning strategies, explore our Advanced Tax Planning Strategies guide.

Frequently Asked Questions about High-Income Tax Planning

What qualifies as a high-income earner?

You’re officially in high-income territory when you hit $200,000 or more in Total Positive Income according to the IRS. The real pain starts in the top federal tax brackets.

If you’re single and earning $191,950 or more, you’re paying 32% on the top portion. Push past $243,725, and you’re in the 35% bracket. Hit $609,350, and you’ve reached the top 37% bracket.

For married couples filing jointly: $383,900 for the 32% bracket, $487,450 for 35%, and $731,200 for the maximum 37% rate.

Add state taxes, and you could face a combined marginal rate above 50% in California, New York, or New Jersey. That’s when implementing 5 outstanding tax strategies for high income earners becomes critical.

What common mistakes do high earners make?

The Form 8606 disaster is probably the most expensive oversight. This form tracks your tax-free basis in Roth accounts after conversions. Skip it, and the IRS assumes you have zero basis – meaning you’ll pay tax twice on the same money.

Equity compensation basis tracking trips up almost every executive. When restricted stock units vest, that’s taxable income. But many people report zero basis when they sell shares later, essentially paying tax twice. Your basis is the fair market value on the vesting date.

State residency planning creates the biggest dollar mistakes. You can’t just declare yourself a Florida resident while maintaining your New York lifestyle. States aggressively audit high earners, examining where you vote, where your kids go to school, where you get your hair cut.

The biggest mistake? Waiting until tax season to plan. Tax planning is a year-round process requiring proactive strategies, not reactive scrambling.

How will upcoming tax law changes impact me?

The Tax Cuts and Jobs Act expires after 2025, creating urgent opportunities and significant threats.

The estate tax exemption cliff is most urgent. Your current $13.61 million exemption ($27.22 million for couples) will likely plummet to around $6 million per person in 2026. If you don’t use current exemption levels before 2026, you lose them forever.

SALT deduction relief might arrive. The $10,000 cap could increase to $50,000 or disappear entirely. For high earners in expensive states, this could mean $10,000 to $20,000 in annual tax savings.

Income tax brackets will likely increase when current rates expire. The top rate could jump from 37% back to 39.6% or higher.

Planning recommendation: Consider accelerating income into 2024-2025 if you expect higher rates in 2026. More importantly, accelerate gift strategies immediately to lock in today’s generous exemption levels.

Conclusion

The journey through these 5 outstanding tax strategies for high income earners might feel overwhelming, but every ultra-wealthy family started exactly where you are now. They just decided to take action.

You’ve already mastered the hardest part of building wealth – earning a substantial income. Now it’s time to master keeping it. The difference between high earners who build generational wealth and those who simply maintain a high lifestyle often comes down to sophisticated tax planning.

At Elite Tax Strategy Solutions, I’ve watched this change hundreds of times over my 40-year career. A surgeon earning $800,000 annually was paying nearly $300,000 in taxes until we implemented coordinated strategies involving mega backdoor Roth contributions, charitable remainder trusts, and strategic state residency planning. Three years later, his effective tax rate dropped by 12 percentage points – over $95,000 staying in his family’s wealth-building accounts.

These strategies aren’t theoretical. Maximizing tax-advantaged accounts can shelter $150,000+ annually for married couples. Smart charitable giving provides immediate deductions while maintaining flexibility. Investment tax management adds 1-2% to your after-tax returns yearly. Income and residency timing can save six figures annually. Estate planning with today’s generous exemptions could save millions in future taxes.

These strategies work best when integrated, not implemented piecemeal. Your 401(k) strategy should complement your charitable giving plan. Your investment management should align with your state residency decisions.

The clock is ticking. The current estate tax exemption will likely drop to around $6 million after 2025. Tax rates may increase across the board. State governments are becoming more aggressive about taxing remote workers.

I’ve seen too many high earners wait until “next year” to start serious tax planning, only to miss opportunities that could have saved hundreds of thousands. The best time to plant a tree was 20 years ago. The second-best time is today.

Your success has put you in the top tier of income earners. Now let’s make sure you get to keep what you’ve earned. Visit our comprehensive guide on Tax Strategies for High Income Earners to dive deeper into how these strategies apply to your specific situation.

Elite Tax Strategy Solutions can tailor a personalized roadmap to keep more of your wealth in your pocket. Because at the end of the day, it’s not about what you earn – it’s about what you keep, grow, and pass on to the next generation.

The wealthy understand something many high earners are just finding: tax planning isn’t an expense, it’s an investment. And like all the best investments, the returns compound over time.